Where you live can change what you owe on crypto by tens of thousands of dollars. The IRS treats cryptocurrency as property at the federal level, but each state adds its own layer of taxation (or none at all). In 2026, the difference between holding crypto in Texas versus California can mean the difference between keeping your gains and handing over more than 13% of them to the state.

This guide breaks down how four major states handle crypto taxes: Texas, Florida, California, and New York. We also cover several other notable states and explain the residency rules that matter if you are considering a move.

Federal vs. State Crypto Taxes: A Quick Overview

Before comparing states, it helps to understand the two layers of crypto taxation every U.S. investor faces.

Federal taxes apply uniformly. The IRS taxes crypto disposals (sales, trades, spending) as capital gains. Short-term gains (assets held under one year) are taxed at ordinary income rates up to 37%. Long-term gains (assets held over one year) are taxed at 0%, 15%, or 20% depending on your income. Crypto received as income (mining, staking, airdrops) is taxed as ordinary income. For a deeper look at how these rules work, see our guide on how crypto is taxed in the U.S.

State taxes vary dramatically. Some states piggyback on federal rules and apply their own income tax rates on top. Others have no income tax at all. A few have unique regulations that add compliance burdens for crypto businesses and investors alike.

Texas: No State Income Tax

Texas is one of nine states with no personal income tax. This makes it one of the most tax-friendly states for crypto investors.

What this means for you:

- Zero state tax on crypto capital gains (short-term or long-term).

- Zero state tax on crypto income from mining, staking, or airdrops.

- You still owe federal taxes on all taxable crypto events.

Texas also has no state-level capital gains tax of any kind. The state funds itself primarily through property taxes and sales taxes, neither of which apply to crypto holdings.

For crypto investors with large portfolios, Texas offers a straightforward advantage. There is no additional state paperwork, no state-level crypto reporting, and no extra tax bill.

Florida: No State Income Tax

Florida mirrors Texas in one critical way: it has no state income tax. The Florida Constitution actually prohibits a state income tax, making this protection more durable than in most other states.

What this means for you:

- Zero state tax on crypto capital gains.

- Zero state tax on crypto income.

- Federal taxes still apply in full.

Florida also has no estate income tax. This can matter for crypto investors thinking about gifting or estate planning with digital assets.

The combination of no income tax and no estate tax makes Florida a popular destination for high-net-worth crypto investors looking to minimize their overall tax exposure.

California: Up to 13.3% on Crypto Gains

California sits at the opposite end of the spectrum. The state conforms closely to federal tax treatment of cryptocurrency, meaning crypto gains are taxed as income. The problem for investors is that California has the highest marginal income tax rate in the country.

California’s tax brackets for crypto gains (2026):

- 1% on the first $10,756 of taxable income (single filer)

- Rates increase through nine brackets

- 12.3% on income over $721,315

- An additional 1% Mental Health Services Tax on income over $1 million (bringing the effective top rate to 13.3%)

Key details:

- California does not offer a preferential long-term capital gains rate. All crypto gains are taxed as ordinary income at the state level.

- The Franchise Tax Board (FTB) has been increasingly active in crypto enforcement.

- California follows federal rules for determining cost basis and holding periods.

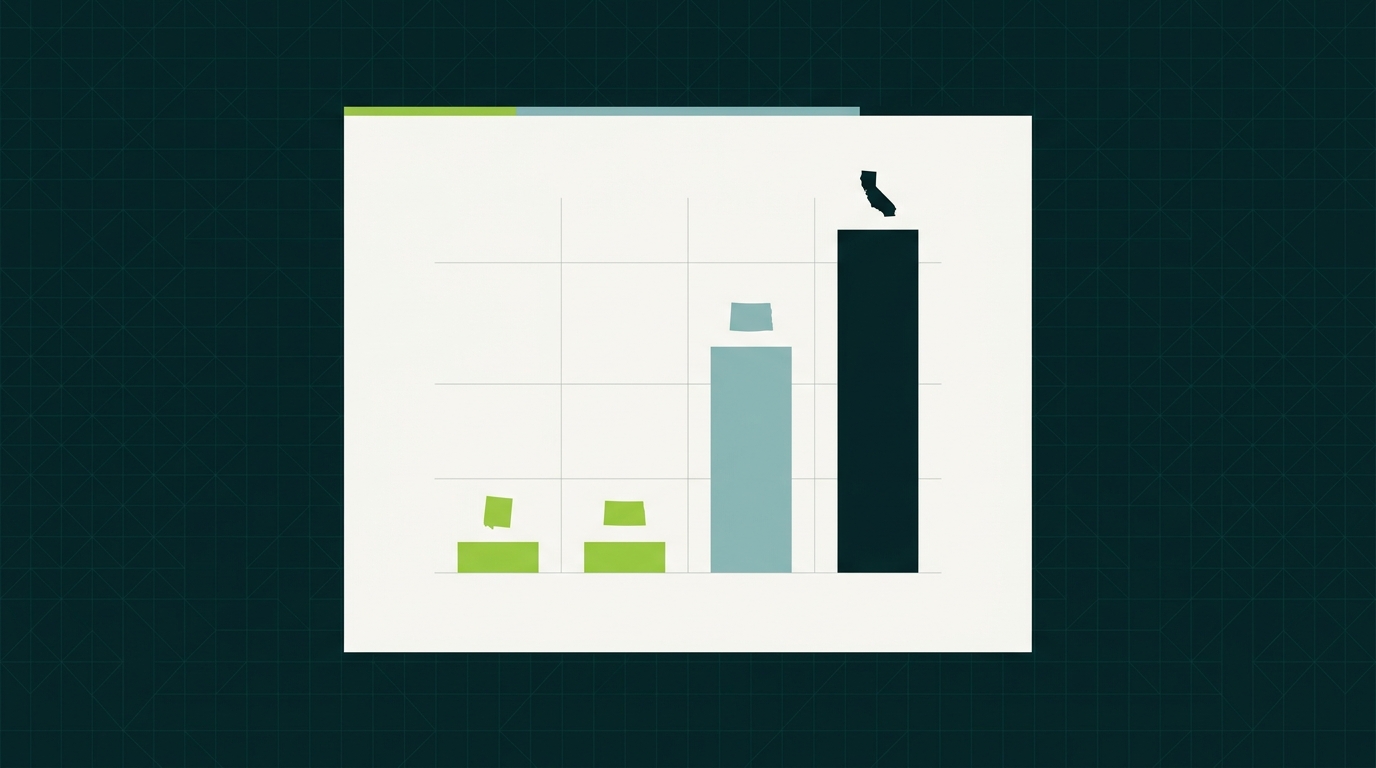

Real Dollar Example: $100,000 Crypto Gain in California vs. Texas

Single filer with $100,000 in W-2 income realizes a $100,000 long-term crypto gain. At this income level, the gain stays in the federal 15% long-term capital gains bracket and falls inside California’s 9.3% marginal state income tax bracket.

No State Income Tax

Federal tax at the 15% LTCG rate: $15,000. State tax: $0. Texas has no personal income tax.

9.3% State Tax in This Example

Federal tax at 15%: $15,000. California state tax on the crypto gain: ~$9,300. California does not offer a preferential long-term rate at the state level.

Over several years of active trading, the cumulative difference can be substantial.

New York: Up to 10.9% Plus BitLicense Rules

New York presents a double challenge for crypto participants. Individual investors face state income tax rates up to 10.9%, and crypto businesses must comply with the state’s BitLicense framework.

State income tax on crypto:

- New York taxes crypto gains as ordinary income.

- State rates range from 4% to 10.9%.

- New York City residents face an additional city income tax of 3.078% to 3.876%, pushing the combined state and city rate above 14% for top earners.

The BitLicense: New York’s Department of Financial Services (NYDFS) requires any business engaged in virtual currency activity to obtain a BitLicense. This applies to exchanges, custodians, and certain other crypto service providers operating in the state. Individual investors do not need a BitLicense, but the regulation has caused some crypto platforms to restrict services for New York residents.

Other Notable States

Several other states are worth mentioning for crypto investors evaluating where to live.

No income tax states (like TX and FL):

- Nevada: No state income tax. Popular with crypto miners due to relatively low energy costs in certain areas.

- Wyoming: No state income tax. Wyoming has also passed crypto-friendly legislation, including a legal framework for DAOs and exemptions for certain digital assets from state money transmitter laws.

- Washington: No state income tax. However, Washington does impose a 7% capital gains tax on gains exceeding $270,000 (as of 2026). This makes it less straightforward than Texas or Florida for high-volume crypto traders.

High-tax states to watch:

- New Jersey: State income tax rates up to 10.75%. Like California, New Jersey taxes crypto gains as ordinary income with no preferential long-term rate.

- Hawaii: State income tax rates up to 11%. Hawaii has historically been restrictive toward crypto exchanges operating in the state.

State-by-State Comparison Table

| State | Income Tax on Crypto | Top Rate | Long-Term Preference? | Special Crypto Rules |

|---|---|---|---|---|

| Texas | None | 0% | N/A | None |

| Florida | None | 0% | N/A | None |

| Nevada | None | 0% | N/A | None |

| Wyoming | None | 0% | N/A | DAO-friendly laws |

| Washington | Capital gains tax only | 7% (gains > $270K) | No | Capital gains excise tax |

| California | Yes, as ordinary income | 13.3% | No | FTB enforcement |

| New York | Yes, as ordinary income | 10.9% (+ NYC tax) | No | BitLicense for businesses |

| New Jersey | Yes, as ordinary income | 10.75% | No | None |

Residency Considerations: Moving to Save on Crypto Taxes

Relocating to a no-income-tax state is a legitimate tax planning strategy. Many crypto investors have moved to Texas, Florida, Wyoming, or Nevada for exactly this reason. However, there are important rules to follow.

Key residency rules to know:

-

California’s “safe harbor” rule. California considers you a resident if you are in the state for more than nine months in a taxable year. Even after you move, the FTB may claim you are still a resident if you maintain significant ties (a home, a spouse, a business) in California.

-

New York’s 183-day rule. New York considers you a statutory resident if you maintain a “permanent place of abode” in the state and spend more than 183 days there. Selling or vacating your New York home is critical when establishing residency elsewhere.

-

The “tax year” matters. If you move mid-year, you may owe state taxes to your former state on crypto gains realized before the move. Plan the timing of large disposals carefully.

-

Federal taxes do not change. Moving states does not reduce your federal tax bill. It only affects the state layer.

The same $500,000 crypto gain costs roughly $46,500 more in California state taxes compared to Texas. For many investors, that difference alone justifies the cost of relocating.

When to Consult a CPA

State crypto tax rules interact with federal rules in ways that can be tricky to manage on your own. Consider working with a tax professional if:

- You are planning a move between states and want to time your crypto disposals correctly.

- You live in a high-tax state and have unrealized gains exceeding $100,000.

- You earn crypto income from multiple sources (mining, staking, DeFi) and need help with state-level reporting.

- You have received a residency audit notice from a former state.

- You operate a crypto business that may trigger BitLicense or state money transmitter requirements.

At CountOnSheep, our team specializes in crypto accounting and tax preparation for investors across all 50 states. We can help you understand your state-level obligations and plan around them.

Bottom Line: What to Do Next

Your state of residence has a real, measurable impact on how much you keep from your crypto investments. Texas and Florida offer the clearest advantage with zero state income tax. California and New York impose some of the highest rates in the country, and both states actively enforce residency rules.

Here is what to do now:

- Know your state’s rules. Check whether your state taxes crypto gains as ordinary income or offers any preferential rates.

- Track your transactions. Accurate records are essential for both federal and state reporting. See our 2026 crypto tax guide for tools and methods.

- Plan large disposals carefully. If you are considering a move, time your sales to occur after you have established residency in your new state.

- Talk to a specialist. State and federal crypto taxes together can be complex. Book a consultation with our team to get a clear picture of what you owe and how to plan ahead.

Your crypto tax situation is unique. The right state-level strategy can save you thousands of dollars every year.

Frequently Asked Questions

Does Texas tax crypto gains?

No. Texas has no state income tax, so crypto capital gains and income are not taxed at the state level. You still owe federal taxes.

Does Florida tax crypto gains?

No. Florida has no state income tax. Crypto gains are only subject to federal taxes.

How does California tax crypto?

California conforms to federal tax rules and taxes crypto gains as regular income. State rates range from 1% to 13.3%, making it one of the highest-tax states for crypto investors.

Does New York have special crypto regulations?

Yes. New York requires crypto businesses to obtain a BitLicense. For individual investors, crypto gains are taxed at state income rates of 4% to 10.9%.

Can I move to a no-income-tax state to avoid crypto taxes?

You can reduce your state tax burden by establishing residency in a no-income-tax state. However, you must genuinely relocate. Your former state may audit you to verify the move.