Key takeaways

- Gifting is not a sale. The giver realizes no capital gain by giving crypto away, so there is generally no income tax on the act of gifting.

- About $19,000 per recipient for 2026. Gifts at or under the annual exclusion need no Form 709 at all.

- Over the exclusion means filing, not tax. The excess reduces your lifetime exemption. Actual gift tax only starts once that exemption is exhausted.

- Carryover basis to the recipient. The recipient inherits your cost basis and holding period, and tax arises only when they later sell.

Gifting crypto is one of the few moves in this whole hub that usually costs nothing in tax, and yet it confuses people constantly. The confusion comes from mixing up two different things: whether the gift is taxable now (almost never) and what the recipient owes later (it depends on the carryover basis). Form 709 is the reporting mechanism that ties it together. This guide explains when you file, the 2026 exclusion and lifetime exemption, how carryover basis works, and the valuation that ties the whole thing to a date.

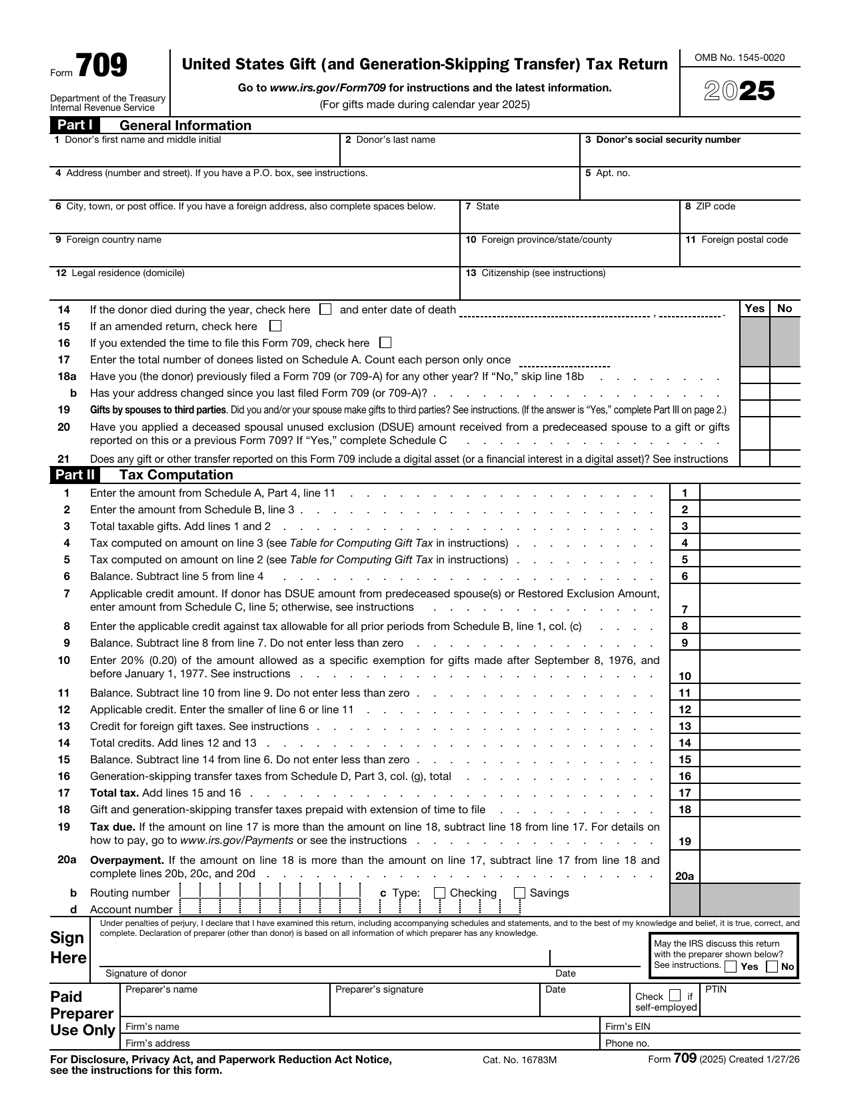

What Form 709 is

Form 709 is the "United States Gift (and Generation-Skipping Transfer) Tax Return." It is how you report gifts that exceed the annual exclusion to a single recipient. Filing it does not usually mean paying tax. For the vast majority of people, Form 709 is a tracking form: it tells the IRS how much of your lifetime exemption you have used, so the running total is correct if your estate is ever large enough to owe estate tax.

Crucially, the giver, not the recipient, files Form 709. And the act of gifting crypto is not a taxable disposal for the giver, so there is no capital gain to report on Form 8949 just because you gave coins away.

This is the single most important idea on the page, so it is worth stating plainly. Selling crypto is a disposal that triggers capital gains tax. Gifting crypto is not a sale, so it triggers no capital gains tax for you, regardless of how much the coin appreciated while you held it. The built-in gain does not vanish, but it is not taxed to you at the moment of the gift. Instead it travels with the coin to the recipient through carryover basis, surfacing only when they eventually sell. Separating those two ideas, no tax now versus deferred gain later, clears up most of the confusion people have about gifting crypto.

The 2026 annual exclusion

The annual gift tax exclusion lets you give a certain amount to any number of recipients each year with no gift tax consequences and no filing. For 2026, that amount is about $19,000 per recipient. The exclusion is per recipient, so you can give $19,000 to each of several people in the same year and stay under the line for each of them. A married couple can effectively double this by gift-splitting, electing to treat a gift as made half by each spouse.

When you file Form 709

You file Form 709 when a gift to a single recipient exceeds the annual exclusion in a year. Filing is the trigger, not tax. Here is the decision in plain terms.

| Gift to one recipient | File Form 709? | Tax owed? |

|---|---|---|

| At or under the annual exclusion | No | No. |

| Over the annual exclusion | Yes | Usually no, reduces lifetime exemption. |

| Over the lifetime exemption | Yes | Gift tax begins on the excess. |

| To a US-citizen spouse | No | Unlimited marital deduction. |

The lifetime exemption

Behind the annual exclusion sits a much larger lifetime gift and estate tax exemption, a multi-million-dollar amount you can transfer above the annual exclusions before any gift tax is actually owed. When you make a gift over the annual exclusion and file Form 709, the excess does not create tax, it simply chips away at this lifetime exemption. Only once you have given away more than the entire lifetime exemption does real gift tax begin. For almost everyone, Form 709 is bookkeeping that protects the exemption math, not a tax bill.

The $50,000 gift is valued on the gift date. The first $19,000 is covered by the annual exclusion, leaving a $31,000 reportable gift on Form 709. No tax is due. Instead, your lifetime exemption drops by $31,000, which only matters if you eventually give away amounts approaching that large lifetime figure.

Carryover basis to the recipient

This is the part people miss, because the tax does not disappear, it shifts to the recipient and to a later date. When you gift crypto, the recipient generally takes your cost basis and your holding period. That is carryover basis. The recipient owes nothing on receiving the gift, but when they eventually sell, their gain is measured from your original basis, not the value at the time of the gift.

Planning a large crypto gift?

Gifts are simple until appreciation and carryover basis get involved. We document the gift-date value, basis, and holding period so the Form 709 and the recipient's future sale both come out right.

See how it worksValuation at the gift date

Crypto is valued at its fair market value in US dollars on the date of the gift. Because crypto prices move constantly, the gift date matters: it sets whether you exceeded the annual exclusion, how much lifetime exemption you used, and the reference value for the recipient's special loss rule. Keep a record of the exact date, the asset, the quantity, and a reasonable price source. For a volatile asset, a defensible valuation method and timestamp protect both you and the recipient.

Gift versus inheritance

One important contrast: a gift carries over your basis, but crypto inherited at death generally receives a stepped-up basis to its value on the date of death. That difference can be large for highly appreciated coins, and it is why the timing and method of transferring crypto to family is a planning question, not just a paperwork question. This is an area to coordinate with an estate professional.

The special loss rule on gifted crypto

There is a wrinkle that catches people when the gifted asset had dropped in value before the gift. Normally the recipient takes your basis. But if the fair market value on the gift date was lower than your basis, a special dual-basis rule applies to protect against shifting losses between taxpayers. In that case, the recipient uses your original basis to figure a gain and the lower gift-date value to figure a loss, and a sale in between the two values produces neither a gain nor a loss.

Because $15,000 is below the $20,000 gain basis but above the $12,000 loss basis, the sale falls in the dead zone where the recipient reports nothing. This is exactly why you record both the gift-date value and your original basis. Without both numbers, the recipient cannot apply the rule correctly years later.

Practical gifting strategies

Used well, gifting is a legitimate way to move value to family and, in some cases, to shift future gains to someone in a lower tax bracket. A few patterns come up often.

- Annual exclusion gifting. Giving up to the annual exclusion per recipient each year moves meaningful value over time with no filing and no use of the lifetime exemption.

- Gift-splitting between spouses. A married couple can elect to treat a gift as made half by each spouse, effectively doubling the per-recipient exclusion, reported on Form 709.

- Gifting to lower-bracket family. Because the recipient inherits your basis and holding period, gifting appreciated crypto to someone in a lower capital gains bracket can reduce the tax paid when it is eventually sold, subject to rules that can apply to minors.

- Charitable gifts. Donating appreciated crypto held long term to a qualified charity can avoid the capital gain entirely and support a deduction, a different path from a gift to an individual and worth separate analysis.

Each of these depends on facts and current limits, so treat them as starting points to discuss with a professional, not as guarantees. The common thread is documentation: the gift-date value, your basis, the holding period, and the recipient, recorded at the time of the gift.

The 2025/26 Crypto Tax Guide. Built by former Big 4 accountants.

A printable, step-by-step guide and checklist to reconcile every coin and wallet, recover missing cost basis, and file accurately before the deadline.

- Form 8949, Schedule D, and Schedule 1 walkthroughs

- How to handle staking, DeFi, NFTs, and lost coins

- The $0-basis 1099-DA trap (and how to avoid it)

- FBAR, Form 8938, and foreign exchange reporting