Key takeaways

- Everyone answers it. The question sits at the top of Form 1040 and applies to every filer, crypto or not.

- Yes means received or disposed. Getting crypto as income, selling, trading, exchanging, or spending it all make the answer yes.

- No means held or moved. Buying with USD, holding, and transferring between your own wallets are a no on their own.

- It is under penalty of perjury. A false no can support penalties and, in serious cases, fraud exposure. Answer honestly.

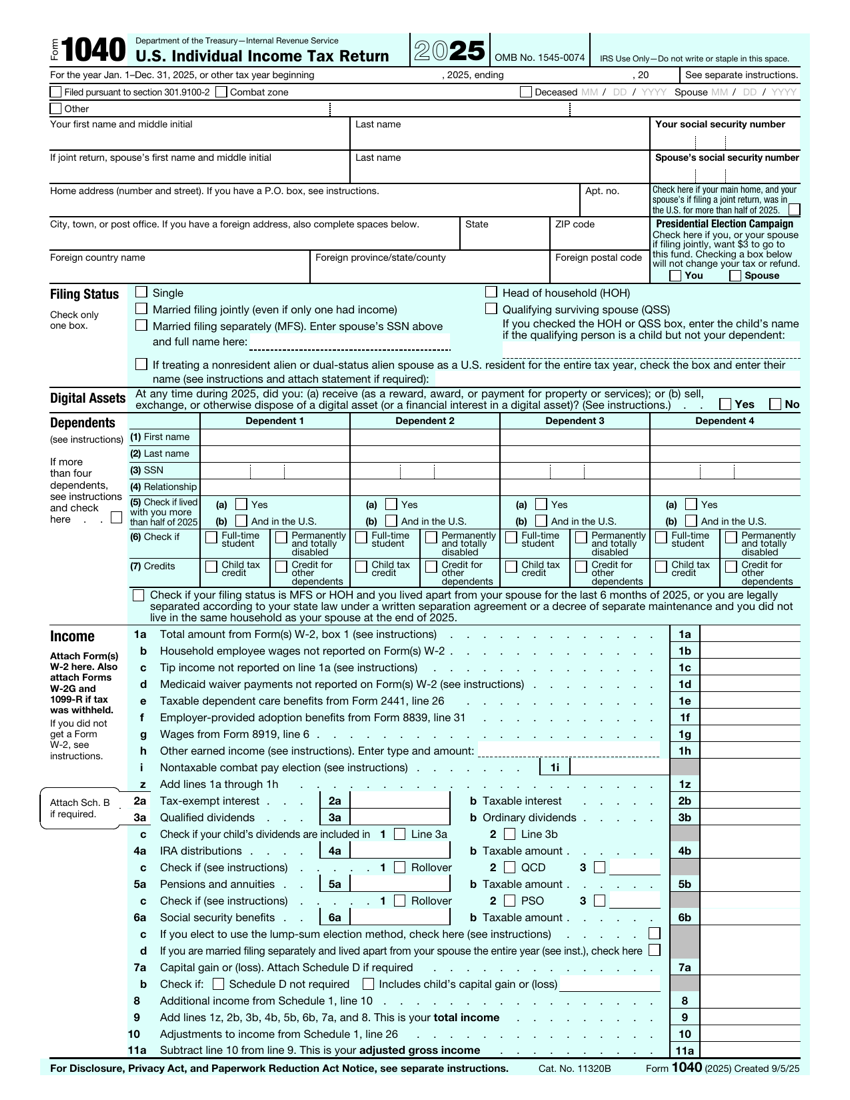

Before you report a single number, Form 1040 asks one blunt question about digital assets, and you cannot skip it. The IRS placed it at the top of the return on purpose, so that crypto activity is a conscious decision rather than an afterthought buried deep in the schedules. The wording is precise, and the difference between a yes and a no comes down to whether you received or disposed of a digital asset during the year. This guide breaks down exactly what counts, what does not, and why the honest answer is the only safe one.

What the question is

At the top of Form 1040, just below your name and address, is a question that reads, in substance: "At any time during the year, did you receive (as a reward, award, or payment for property or services) or sell, exchange, or otherwise dispose of a digital asset or a financial interest in a digital asset?" There are two boxes, Yes and No, and you must check one. There is no option to leave it blank.

The question applies to everyone who files a 1040, not just to crypto investors. Even a taxpayer who has never touched crypto has to check "no." That universal reach is what makes it powerful: the IRS now has a signed statement, on every return, about digital asset activity.

The phrase to focus on is otherwise dispose of. The question is not limited to selling for cash, which is what most people picture. Disposing covers any way you part with a digital asset, including trading it for another coin, spending it, or otherwise giving it up in a taxable exchange. Combined with the receiving half of the question, which captures rewards, payments, and similar inflows, the wording is deliberately broad. The drafters wanted to catch the full range of crypto activity, not just the obvious cash-out, which is why so many ordinary crypto behaviors land on the yes side once you read the language carefully.

What counts as "yes"

You check yes if, during the year, you received or disposed of a digital asset in a way the question describes. The two big buckets are receiving crypto and disposing of crypto.

| Activity | Answer | Why |

|---|---|---|

| Received crypto as a reward or airdrop | Yes | Receiving a digital asset. |

| Got paid in crypto for goods or services | Yes | Received as payment. |

| Sold crypto for cash | Yes | Disposition of a digital asset. |

| Traded one coin for another | Yes | Exchange of a digital asset. |

| Spent crypto on goods | Yes | Disposed of a digital asset. |

| Received mining or staking rewards | Yes | Received a digital asset. |

What counts as "no"

You can check no if your only crypto activity during the year was holding it, buying it with US dollars, or moving it between accounts you own. These are not receipts or dispositions, so on their own they do not require a yes.

| Activity | Answer | Why |

|---|---|---|

| Bought crypto with US dollars | No | Acquisition with cash, not a disposal. |

| Held crypto without selling | No | Holding is not a taxable event. |

| Transferred between your own wallets | No | A self-transfer, not a disposal. |

| Moved crypto exchange to your own wallet | No | Still your asset, ownership unchanged. |

A worked example

Walking through a real year makes the logic concrete.

Most of this taxpayer's activity points to no, but the $40 of staking rewards is a receipt of a digital asset, so the honest answer is yes. That yes also means the $40 should appear as income on Schedule 1. The size of the activity does not matter, $40 counts the same as $40,000 for the checkbox.

Not sure if your year is a yes or a no?

The checkbox is simple once your activity is laid out clearly. We reconcile your full year so the answer is obvious and the income behind a yes is actually reported.

See how it worksWhy the IRS put the question where it did

The placement of this question is deliberate, and understanding the strategy behind it helps you treat it with the seriousness it deserves. For years, the IRS struggled to get a clear picture of who held and used digital assets, because crypto income could be scattered across schedules, omitted entirely, or simply never reported by anyone. By moving a direct question to the very front of the most common tax form in the country, the IRS turned a hidden compliance problem into a conscious, signed decision that every single filer has to make.

The question first appeared in a limited form and has been refined over several filing seasons. The wording has tightened from broad phrasing about virtual currency to the current language about receiving or disposing of a digital asset, and the term digital asset itself now reaches beyond cryptocurrencies to cover stablecoins and many tokens recorded on a distributed ledger. That broadening matters: an asset you might not think of as crypto can still fall within the definition, so the safe habit is to read the current year instructions rather than assume last year's understanding still holds.

There is also an enforcement logic at work. A signed answer creates a clean record the IRS can hold up later. If a return checks no, and broker data, blockchain analysis, or an exchange summons later shows reportable activity, the false answer strengthens the case that the omission was knowing rather than accidental. The question is a low-cost way for the IRS to raise the stakes on non-disclosure without auditing everyone.

Edge cases worth thinking through

Most years are clearly a yes or a no, but a few situations deserve a careful read rather than a reflex.

- Receiving a genuine gift. The instructions treat receiving a bona fide gift of crypto differently from receiving it as a reward or payment. Read the wording for the year, and remember that selling the gifted coins later is its own yes.

- Wrapping or bridging tokens. Converting a token into a wrapped version or bridging it across chains can be treated as an exchange, which points toward yes. The treatment is not always settled, so document what you did.

- Receiving an asset from a hard fork. Gaining control of new coins from a fork is a receipt of a digital asset and points to yes, with the value reported as income.

- Using crypto to pay a fee. Spending even a small amount of crypto on a network fee is technically a disposal, which is one reason heavy on-chain users almost always answer yes.

- Holding through a fund or ETF. Owning a security that holds crypto, rather than the crypto itself, generally does not by itself make the answer yes, since you hold the fund, not the underlying digital asset.

When an edge case is genuinely unclear, the conservative instinct is to answer yes and report the underlying activity honestly, rather than to reach for a no that you would struggle to defend. A yes with proper reporting carries no penalty. A no that turns out to be wrong can carry several.

Consequences of answering wrong

The digital asset question is part of a return you sign under penalty of perjury. That signature is what gives the question its teeth. Checking no while knowing you had reportable crypto activity is a false statement on a sworn document.

In practice, a wrong answer rarely stands alone. It usually travels with unreported income or gains, and the combination is what creates exposure: accuracy penalties on the tax you underpaid, failure-to-pay and interest, and in deliberate cases the potential for civil fraud penalties or criminal referral. The IRS also increasingly receives third-party data, such as the Form 1099-DA, that can contradict a false no. The honest path is straightforward: answer truthfully, and report the activity that makes the answer yes.

The 2025/26 Crypto Tax Guide. Built by former Big 4 accountants.

A printable, step-by-step guide and checklist to reconcile every coin and wallet, recover missing cost basis, and file accurately before the deadline.

- Form 8949, Schedule D, and Schedule 1 walkthroughs

- How to handle staking, DeFi, NFTs, and lost coins

- The $0-basis 1099-DA trap (and how to avoid it)

- FBAR, Form 8938, and foreign exchange reporting