Key takeaways

- Schedule D nets the totals. It pulls short-term and long-term subtotals from Form 8949 and combines them into one capital gain or loss.

- The loss limit is $3,000 a year. Net capital losses offset up to $3,000 of ordinary income annually, or $1,500 if married filing separately.

- Losses carry forward. Whatever you cannot use this year carries to future years, keeping its short-term or long-term character.

- You need both forms. Form 8949 is the detail, Schedule D is the summary. Crypto filers almost always file both.

Schedule D is where the long list of crypto disposals on Form 8949 becomes a single, clean result. It is the form that answers the bottom-line question: across everything you sold, traded, and spent this year, did you come out ahead or behind, and by how much? For crypto investors, Schedule D also holds two of the most valuable tools in the tax code, the loss deduction against ordinary income and the loss carryforward that can shelter gains for years. This guide explains how netting works, how the loss rules apply, and how Schedule D and Form 8949 fit together.

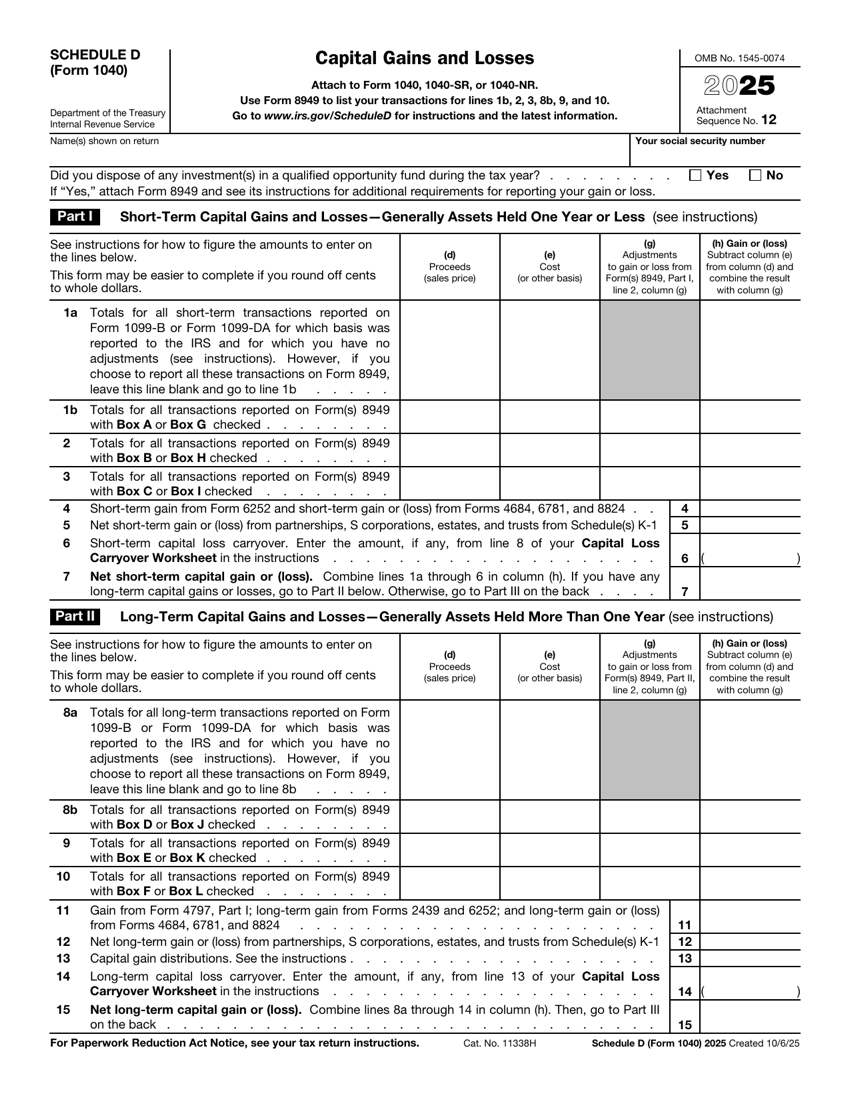

What Schedule D is for

Schedule D is titled "Capital Gains and Losses." Its purpose is to summarize every capital transaction you had during the year into a net result that flows onto your Form 1040. It does almost none of the detail work itself. Instead, it relies on Form 8949, which lists every individual disposal, and it simply carries those totals up and nets them.

For crypto, the chain runs like this: each disposal lands on Form 8949, the box totals carry to Schedule D, Schedule D nets them, and the final capital gain or loss lands on your 1040. If you understand that flow, the form is straightforward.

It helps to remember what Schedule D does not do. It does not list individual trades, it does not calculate any single gain, and it does not decide your holding period. All of that happens upstream on Form 8949. Schedule D simply gathers the period totals, applies the netting rules, brings in any prior-year carryforward, and reports one bottom-line figure. Keeping that division of labor clear is what prevents people from trying to force trade-level detail onto a form that was never meant to hold it.

How netting works

Netting happens in two stages. First, you net within each holding period. Then you combine the two.

- Short-term first. Add up all short-term gains and losses (assets held one year or less). The result is your net short-term gain or loss.

- Long-term next. Add up all long-term gains and losses (assets held more than a year). The result is your net long-term gain or loss.

- Combine. Add the net short-term and net long-term figures together. A loss in one category can offset a gain in the other.

Here the $3,500 net short-term loss offsets part of the $10,000 net long-term gain, leaving a $6,500 net gain. Because the surviving gain is long-term in character, it is taxed at the favorable long-term rate even though short-term losses were used to reduce it.

The $3,000 capital loss limit

What if your losses outweigh your gains for the year? This is common after a down crypto market. When your total capital losses exceed your total capital gains, you have a net capital loss, and the tax code limits how much of it you can use against ordinary income in a single year.

The limit is $3,000 per year ($1,500 if married filing separately). That means a net capital loss can reduce up to $3,000 of your wages, business income, or other ordinary income each year. Anything above $3,000 does not vanish, it carries forward.

Loss carryforwards

A capital loss carryforward is the unused portion of a net capital loss that rolls into future years. It keeps going, year after year, deducting up to $3,000 against ordinary income each year and offsetting any new capital gains in full, until it is used up. The carryforward also keeps its character: a short-term carryforward stays short-term, and a long-term carryforward stays long-term, which affects how it nets against future gains.

That $15,000 loss wiped out an $11,000 gain entirely, shaved $3,000 off ordinary income, and still left $1,000 to carry again. This is why tracking and reporting losses matters even in years when you owe nothing.

Down year in crypto?

A losing year can become a multi-year tax asset if the losses are reconciled and reported correctly. We make sure every realized loss is captured and carried forward.

See how it worksThe interplay with Form 8949

Schedule D and Form 8949 are a pair. The detail lives on the 8949, and the summary lives on Schedule D. Each box on Form 8949 totals to a specific Schedule D line.

| Form 8949 source | Goes to Schedule D | Result |

|---|---|---|

| Short-term boxes A, B, C totals | Part I short-term lines | Net short-term gain or loss. |

| Long-term boxes D, E, F totals | Part II long-term lines | Net long-term gain or loss. |

| Prior-year carryforward | Carryforward lines | Reduces this year's net. |

| Combined net | Bottom of Schedule D | Flows to Form 1040. |

The practical lesson is that Schedule D is only as accurate as the Form 8949 behind it. If your 8949 has a wrong basis or a missing disposal, Schedule D inherits the error. Fix the detail first, and the summary takes care of itself.

A note on wash sales and crypto

One question that comes up constantly: do wash sale rules apply to crypto? As of the 2026 tax year, the wash sale rule that disallows a loss when you rebuy a substantially identical security within 30 days is written for securities, and crypto is treated as property, not a security. Many practitioners take the position that the rule does not currently apply to crypto, which can allow loss harvesting. This is an area lawmakers have repeatedly proposed to change, so treat it as a live issue and get a professional read before building a strategy around it.

Loss harvesting and Schedule D

Because losses on Schedule D can offset gains in full and shave $3,000 off ordinary income, deliberately realizing losses, often called loss harvesting, is one of the most practical tax moves in a down crypto year. The idea is simple: if you hold a coin worth less than you paid, selling it crystallizes a loss you can use, even if you believe in the asset long term.

The conservative way to think about it is that harvesting changes the timing of when you recognize a loss, not whether the loss is real. A few principles keep it clean. First, the loss is only realized when you actually dispose of the asset, so it has to be a genuine sale or trade, not a paper markdown. Second, the character carries: a short-term loss first offsets short-term gains, a long-term loss first offsets long-term gains, and only then do they cross over. Third, because the wash sale rule is currently written for securities and crypto is property, many filers take the position that they can repurchase quickly, though as noted that is a live legislative target and worth professional input.

Common Schedule D crypto mistakes

Schedule D itself rarely contains the error. The mistakes almost always come from the data feeding it.

- Not reporting a losing year. Skipping the return because no tax was due throws away the deduction and the carryforward you could have used later.

- Mismatched holding periods. Misclassifying short-term as long-term, or the reverse, distorts both the netting and the rate that applies to the surviving gain.

- Inheriting a wrong basis from Form 8949. A zero or missing basis on the 8949 flows straight through, so Schedule D overstates the gain. Fix the detail first.

- Forgetting a prior-year carryforward. A carryforward from a previous year reduces this year's net, but only if you remember to bring it forward. Lost carryforwards are lost deductions.

- Ignoring the $3,000 cap. Expecting a giant net loss to wipe out all ordinary income in one year. It does not. The annual limit is $3,000 against ordinary income, with the rest carried forward.

The 2025/26 Crypto Tax Guide. Built by former Big 4 accountants.

A printable, step-by-step guide and checklist to reconcile every coin and wallet, recover missing cost basis, and file accurately before the deadline.

- Form 8949, Schedule D, and Schedule 1 walkthroughs

- How to handle staking, DeFi, NFTs, and lost coins

- The $0-basis 1099-DA trap (and how to avoid it)

- FBAR, Form 8938, and foreign exchange reporting