Key takeaways

- 1099-DA is broker reporting. US exchanges and certain platforms file it with the IRS and send you a copy for every year you sold or exchanged digital assets.

- 2025 is proceeds only, 2026 adds basis. The first forms report gross proceeds. Cost basis reporting for covered assets begins with 2026 transactions.

- The missing-basis trap is the danger. Transferred-in crypto is generally noncovered, so the form may leave basis blank and you must supply it from your records.

- It feeds Form 8949, it does not replace it. You still list each disposition and net the totals on Schedule D.

For years, crypto investors filed in a fog. Some exchanges sent a 1099-MISC, some sent a 1099-B that did not really fit, some sent a 1099-K that scared people with huge gross numbers, and many sent nothing at all. Form 1099-DA was created to end that confusion with one purpose-built digital asset return. This guide explains what the form is, who receives it, what it reports in 2025 versus 2026, the traps that inflate your tax bill, and exactly how it flows into the rest of your return.

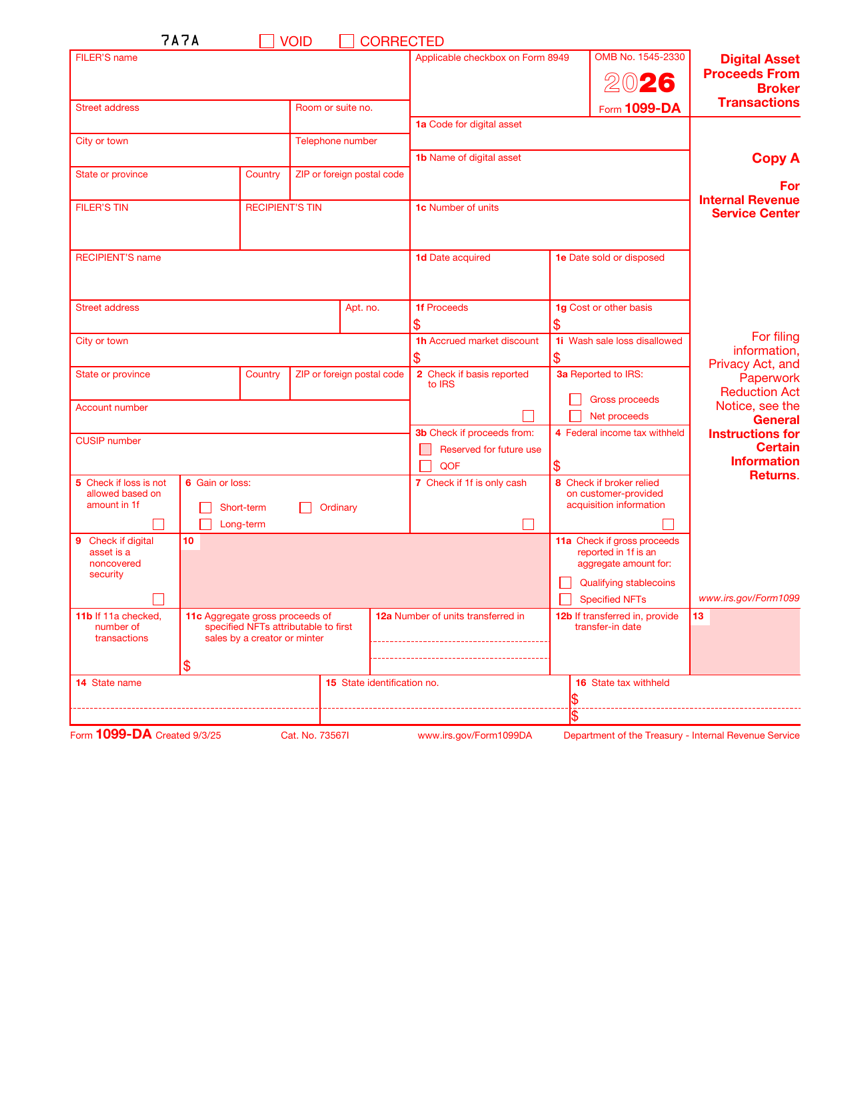

What is Form 1099-DA?

Form 1099-DA is an information return titled "Digital Asset Proceeds From Broker Transactions." A broker fills it out, files a copy with the IRS, and sends a matching copy to you. Its job is to tell the IRS that you disposed of digital assets through that broker during the year, and for how much. The "DA" stands for digital asset, and it covers cryptocurrencies, stablecoins, and many tokens that trade on centralized platforms.

The form exists because the Infrastructure Investment and Jobs Act of 2021 extended broker reporting rules to digital assets. Before the 1099-DA, brokers borrowed forms built for stocks and cash, which produced numbers that rarely matched a crypto investor's real gain. The 1099-DA is the first form designed from the start for crypto, so the figures are meant to line up with how the IRS expects you to report.

Who gets a Form 1099-DA?

You get a 1099-DA if you are a customer of a US digital asset broker and you sold or exchanged digital assets during the year. In practice that means most active users of centralized US exchanges and certain payment apps and platforms that handle crypto. The reporting follows the broker, not the asset, so each broker reports only the activity that happened on its own platform.

That last point matters more than it sounds. If you traded on three different exchanges in one year, you can receive three separate 1099-DA forms, each covering a slice of your activity. None of them sees the whole picture, and your self-custody wallet and DeFi activity are not covered by any of them. You are responsible for stitching it all together.

- Covered by a 1099-DA: sales for cash and crypto-to-crypto trades on a US broker, and in many cases certain spends and swaps the broker processes.

- Not covered: self-custody wallet activity, most decentralized exchange trades, peer-to-peer transfers, and anything on a platform that is not a US broker.

What the 1099-DA reports: 2025 vs 2026

The single most important thing to understand about this form is that it phases in over two years. The first version is deliberately limited, and the second version is far more complete.

| Tax year | Proceeds reported? | Cost basis reported? | What you must supply |

|---|---|---|---|

| 2025 (filed early 2026) | Yes | No | All cost basis, from your own records. |

| 2026 (filed early 2027) | Yes | For covered assets | Basis for transferred-in and pre-coverage lots. |

For the 2025 tax year, the 1099-DA reports gross proceeds only. That is the total dollar amount you received from sales and exchanges, with no subtraction for what you paid. A form that shows only proceeds is not telling you your gain. It is telling you half of the equation, and the half it leaves out, your cost basis, is the half that lowers your tax.

Beginning with 2026 transactions, brokers must also report cost basis, but only for "covered" assets. A covered asset is one you acquired after 2025 in a custodial account with that broker and held there until disposition, so the platform actually knows your purchase price. Anything you acquired before 2026, or bought elsewhere and moved in, is not covered, and its basis will still be missing or blank even on the 2026 form.

The transferred-in missing-basis trap

This is where 1099-DA forms can lead to an overstated gain. When you transfer crypto into an exchange from another wallet or platform, the receiving broker usually has no record of what you originally paid. It sees the coins arrive and later sees the sale. Because transferred-in assets are generally noncovered, the broker may report the proceeds while leaving basis blank.

A blank basis does not mean your basis is zero. The risk appears when tax software or a worksheet converts that blank field to zero and calculates the full sale price as gain. You must supply the supported basis from your own records so Form 8949 reflects the real result.

In that example, letting tax software substitute zero for the blank basis would create an extra $42,000 of phantom gain. At a 24% rate, that is over $10,000 of tax you do not actually owe. The fix is to supply your real $42,000 basis on Form 8949 and keep the records that prove it. This is why every transfer between platforms needs to be tracked in your own ledger, not left to the broker.

Moved crypto between exchanges this year?

Transferred-in coins are exactly where the 1099-DA may leave basis blank. If that missing basis is treated as zero, your gain is overstated. We rebuild the real cost basis across every wallet so your return reflects what you actually made.

See how it worksHow the 1099-DA reconciles to Form 8949

The 1099-DA does not go on your return by itself. It is the broker's report, and your job is to reconcile it against your own records on Form 8949, then net the totals on Schedule D. Here is the flow in plain terms.

- Collect every 1099-DA. One per broker. Each covers only that platform's sales and exchanges.

- Match proceeds. Confirm the gross proceeds on each form agree with your own exported history. If they do not, find out why before you file.

- Fill the basis gaps. For transferred-in or pre-coverage lots, enter your real cost basis from your purchase records instead of accepting a blank.

- List each disposition on Form 8949. Description, date acquired, date sold, proceeds, basis, and the gain or loss. Use a basis adjustment code when you correct the broker figure.

- Net it on Schedule D. Total short-term and long-term, then confirm it ties back to what the IRS received.

What to do if your 1099-DA is wrong

Wrong forms are common in these early years, especially for proceeds tied to transfers, wrapped assets, and platform migrations. You are not required to file an incorrect number just because a broker printed it. Your options depend on what is wrong.

| What is wrong | What it looks like | What to do |

|---|---|---|

| Missing basis | Proceeds shown, basis blank. | Enter your supported basis on Form 8949. A basis adjustment code is not automatic when basis was not reported to the IRS. |

| Incorrect basis reported to the IRS | Box 2 indicates basis was reported, but your records support a different amount. | Use code B and the Form 8949 adjustment mechanics. Keep the reconciliation that supports the correction. |

| Wrong proceeds | Sale amount does not match your records. | Ask the broker for a corrected 1099-DA. Document the discrepancy. |

| Double-counted transfers | A wallet move shown as a sale. | Exclude non-taxable transfers and reconcile from your own ledger. |

| Duplicate forms | Two forms covering the same activity. | Reconcile to avoid reporting the same disposal twice. |

The guiding principle: report what is true, and document why your number differs from the form. The IRS matching system flags mismatches, so the goal is not to ignore the form, it is to account for every dollar of proceeds it reports while correcting the basis it gets wrong.

Covered versus noncovered assets

The word covered does a lot of work in the 1099-DA rules, and it is worth slowing down on. A covered asset is one the broker has enough information to report basis for, which in practice means you acquired it after 2025 in a custodial account with that broker and held it there until disposition. When a coin is covered, starting with 2026 transactions the broker reports your basis along with your proceeds, and the form is close to complete on its own.

A noncovered asset is the opposite: the broker saw the disposition but the asset falls outside mandatory basis reporting, often because you transferred it in or acquired it before 2026. For noncovered assets, even the 2026 form may show proceeds with no basis, and you are responsible for supplying the cost from your own records. This is why two coins sold on the same exchange in the same year can be treated differently on the form.

When you have several 1099-DA forms

A multi-platform year is where the form is most likely to mislead, precisely because each broker only sees its own slice. Suppose you bought on one exchange, moved coins to a second to trade, and cashed out on a third. Each platform issues a 1099-DA reflecting only what happened on it, and none of them traces the basis that followed your coins across the moves. Stacking the proceeds from three forms without reconciling the transfers between them is a recipe for both double-counting and missing basis.

The discipline that fixes this is a single, unified ledger that spans every platform and wallet. When you reconcile all activity into one timeline, transfers cancel out, basis follows the coins, and the proceeds on each 1099-DA simply confirm a piece of a picture you already have complete. The forms become a cross-check against your records rather than the records themselves.

How to get your 1099-DA

Brokers generally make the form available in your account, usually under a documents, statements, or tax section, and many also mail or email a copy. Forms are typically issued in late January or February for the prior tax year.

- Log in to each broker you used during the year and open the tax documents area.

- Download the 1099-DA and any other forms, such as a 1099-MISC for rewards.

- Export your full transaction history as a CSV so you can verify proceeds and rebuild basis.

- Repeat for every platform, then combine with your self-custody and DeFi records.

The 2025/26 Crypto Tax Guide. Built by former Big 4 accountants.

A printable, step-by-step guide and checklist to reconcile every coin and wallet, recover missing cost basis, and file accurately before the deadline.

- Form 8949, Schedule D, and Schedule 1 walkthroughs

- How to handle staking, DeFi, NFTs, and lost coins

- The $0-basis 1099-DA trap (and how to avoid it)

- FBAR, Form 8938, and foreign exchange reporting