Key takeaways

- Earned crypto is ordinary income. Staking, airdrops, forks, rewards, and interest are income, not capital gains, when you receive them.

- Value at receipt. The fair market value in dollars when you gain control is both your income and your future cost basis.

- Line 8, other income. Non-business crypto income lands on Schedule 1 as other income and flows to your 1040.

- Then a second tax event. Selling the earned coins later is a separate capital gain or loss measured from that receipt value.

Not all crypto income is a capital gain. When you earn crypto rather than dispose of it, you have ordinary income, and for most individuals that income lands on Schedule 1. This is the form that catches staking rewards, airdrops, hard forks, and crypto interest for people who are not running a crypto business. Getting it right matters in two directions: you owe income tax on the value when you receive it, and that same value protects you from being double-taxed when you sell. This guide explains what belongs here, how to value it, and where exactly it goes.

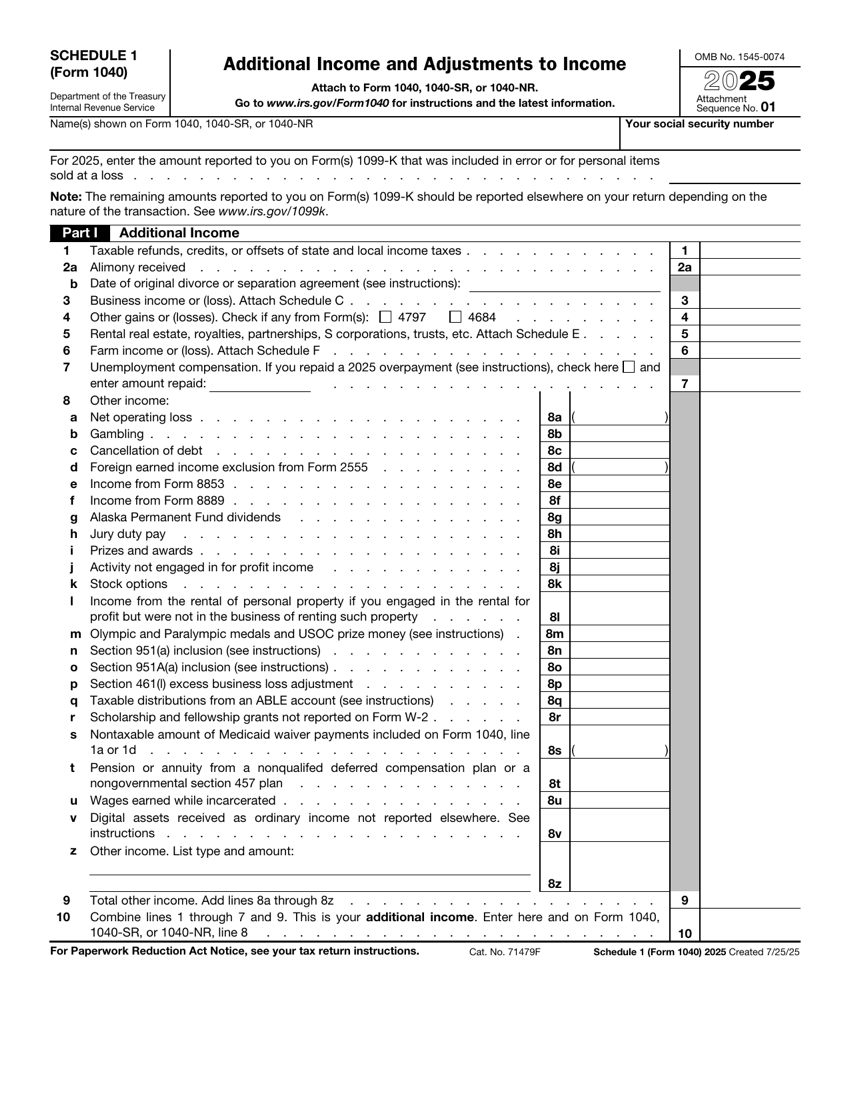

What Schedule 1 is for

Schedule 1 is titled "Additional Income and Adjustments to Income." It is the catch-all attachment to Form 1040 for income that does not fit neatly on the main form, along with certain deductions. For crypto, the relevant part is the income section, specifically the "other income" line, line 8, which has a dedicated entry for digital asset income that is not from a business.

The key distinction is non-business. If your crypto earning rises to the level of a trade or business, such as mining run as a business, it belongs on Schedule C instead, where it can carry self-employment tax. Schedule 1 is for the investor and hobbyist side: rewards you receive without running a business around them.

The reason earned crypto goes here at all is that the IRS treats receiving it as accession to wealth, the same principle that makes a cash bonus or interest payment taxable. You did not buy these coins, you received them, and that receipt is income measured in dollars even though no dollars changed hands. Once you internalize that earned crypto is income at the moment it lands, the rest of the form follows naturally: total it, report it as other income, and remember the value for later.

What crypto income belongs on Schedule 1

These are the common types of earned crypto that an individual reports here, all valued at fair market value when received.

| Income type | On Schedule 1? | How it is treated |

|---|---|---|

| Staking rewards | Yes | Ordinary income at FMV when you gain control. |

| Airdrops | Yes | Ordinary income at FMV when you can transfer or sell. |

| Hard fork coins | Yes | Ordinary income at FMV when you receive control. |

| Rewards and bonuses | Yes | Ordinary income at FMV when received. |

| Crypto interest (lending) | Yes | Ordinary income at FMV when received. |

| Selling earned coins later | No | Capital gain or loss on Form 8949, not Schedule 1. |

How to value crypto income

The rule is fair market value in US dollars at the moment you gain control of the crypto. "Gain control" usually means the moment the rewards or tokens are yours to move, sell, or use, not necessarily when they were generated on-chain. For most exchange staking, that is when the reward posts to your account. For an airdrop, it is when the tokens are claimable and transferable by you.

That receipt value does double duty. It is the income you report on Schedule 1, and it becomes the cost basis of those specific coins. When you sell them later, your capital gain or loss is the sale price minus that basis, so the income you already paid tax on is not taxed again.

The $2,640 is ordinary income this year on Schedule 1. The later sale of the staked coins for $2,300 produces a separate $500 capital gain on Form 8949, because their basis was the $1,800 already taxed as income. Two events, two forms, no double tax on the same dollars.

Exactly where it goes

On Schedule 1, your total earned crypto income goes in the income section as "other income." The current Form 1040 and Schedule 1 include a specific line for digital asset income that is not reported elsewhere, within line 8. The total from Schedule 1 then carries to the income summary on your Form 1040.

- Total your earned crypto at fair market value on receipt across the year.

- Enter it as other income on Schedule 1, using the digital asset other-income entry.

- Carry the Schedule 1 total to Form 1040.

- Answer the digital asset question "Yes" at the top of the 1040, since receiving crypto counts.

Lots of small rewards adding up?

Hundreds of tiny staking deposits each have a value at receipt and a basis to track. We total your income correctly and set the basis so you are not taxed twice.

See how it worksHonest take on the gray areas

A few areas are genuinely unsettled, and the conservative versus aggressive choice is worth understanding.

- Staking timing. The conservative position, supported by IRS guidance, is that rewards are income when you gain control. A more aggressive position some have argued is that newly created tokens should not be income until sold. Courts and the IRS have leaned toward the conservative receipt-based view, so most filers report at receipt.

- Airdrop control. If you cannot yet move or sell an airdropped token, a reasonable position is that you have not gained control, so income is deferred until you can. Document the date control began.

- Locked or illiquid rewards. Where rewards are locked, the value and timing of "control" can be debatable. Keep records of vesting and unlock dates.

On all of these, the safe default is to report at receipt with good records. If you take a more aggressive position, do it with professional advice and documentation, not by guessing.

A closer look at each income type

The forms treat all of these as ordinary income, but they arrive differently, and knowing the mechanics keeps you from missing any.

- Staking rewards. Whether through an exchange or your own validator delegation, rewards are income at their value when they post to your control. They often arrive in small, frequent amounts, which makes them easy to undercount. The cumulative total across a year can be substantial even when each deposit looks trivial.

- Airdrops. Tokens dropped to a wallet are income once you can transfer or sell them. The timing question matters: if the tokens are not yet claimable or movable, a reasonable position is that you have not gained control. The value can swing wildly right after an airdrop, so record the value at the moment control begins, not the headline price.

- Hard forks. When a blockchain splits and you receive new coins, those coins are income at their value when you gain control. If you never gain control, for example because your platform does not support the forked asset, there may be no income until you do.

- Rewards and bonuses. Sign-up bonuses, referral rewards, and card rewards paid in crypto are generally income at receipt. Some card rewards that function like a rebate on your own spending can be treated as a reduction of purchase price rather than income, which is a distinction worth confirming.

- Crypto interest. Interest from lending or yield programs is ordinary income at the value received. It is economically similar to bank interest, but it arrives in crypto, so each payment has a dollar value and a basis to track.

Common Schedule 1 crypto mistakes

A handful of errors show up again and again with earned crypto, and each one costs money or invites a notice.

- Skipping income because it was under a reporting threshold. Rewards under the level that triggers a broker form are still taxable. No form does not mean no income.

- Valuing at the wrong moment. Using the price when coins were generated on-chain, or the price at year end, instead of the value when you gained control, produces the wrong income figure and the wrong basis.

- Double-counting at sale. Forgetting that income already taxed becomes the basis, and then paying tax again on the full sale price. Setting the basis to the receipt value prevents this.

- Putting business income here. If the activity is really a business, it belongs on Schedule C with deductions and self-employment tax, not buried as other income.

The 2025/26 Crypto Tax Guide. Built by former Big 4 accountants.

A printable, step-by-step guide and checklist to reconcile every coin and wallet, recover missing cost basis, and file accurately before the deadline.

- Form 8949, Schedule D, and Schedule 1 walkthroughs

- How to handle staking, DeFi, NFTs, and lost coins

- The $0-basis 1099-DA trap (and how to avoid it)

- FBAR, Form 8938, and foreign exchange reporting