Key takeaways

- Business mining goes on Schedule C. Regular, profit-motivated mining is a business, with income and deductions reported here.

- Self-employment tax applies. Net Schedule C profit carries about 15.3% self-employment tax through Schedule SE, on top of income tax.

- Expenses are deductible. Hardware, electricity, hosting, repairs, and pool fees can offset mining income when it is a business.

- Hobby is different. A hobby reports income on Schedule 1 with no business deductions and no self-employment tax.

Most crypto users never touch Schedule C. But if you mine, run validators, or operate nodes as a genuine business, this is the form that turns your crypto activity into a small business on your tax return, with all the upside of deductions and the cost of self-employment tax. The stakes are real in both directions: classify a profitable operation as a hobby and you lose your deductions, classify a casual setup as a business and you can invite scrutiny. This guide explains when Schedule C applies, what you can deduct, how self-employment tax works, and where the hobby line sits.

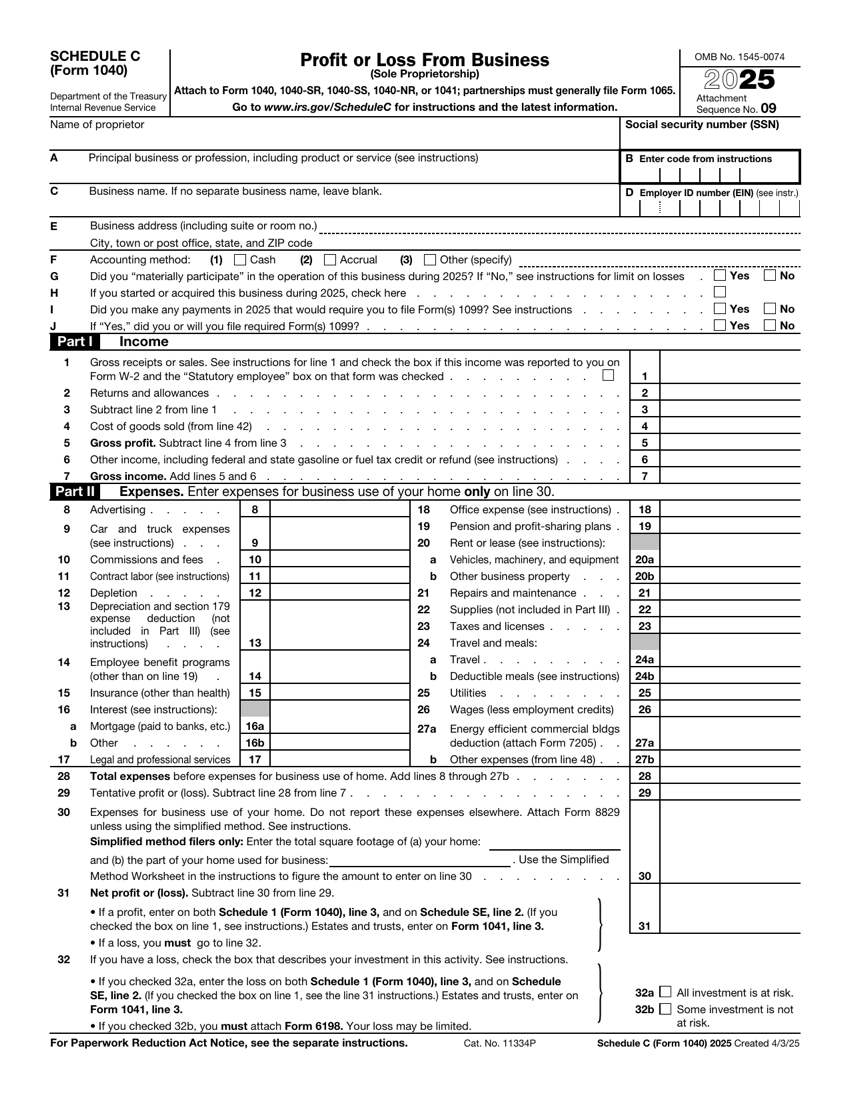

What Schedule C is for

Schedule C is titled "Profit or Loss From Business" and is used by sole proprietors and single-member LLCs to report income and expenses from a business they run. For crypto, the classic case is mining operated as a business, but it also covers node and validator operations run for profit, and other crypto services you provide as a trade or business.

The defining feature of Schedule C is that it is a business, which brings two things the investor side does not have: you can deduct your ordinary and necessary business expenses against your income, and your net profit is subject to self-employment tax. That trade-off is the heart of the form.

That trade-off is not automatically good or bad, it depends on your facts. A miner with heavy electricity and hardware costs may come out far ahead on Schedule C, because the deductions can shrink taxable income dramatically, even after the self-employment tax. A casual holder who picked up a few rewards has little to deduct and would only be adding self-employment tax for no benefit. The form rewards real businesses with real costs and penalizes people who claim business treatment without the substance to back it up.

The hobby versus business test

Whether your mining belongs on Schedule C depends on whether it is a trade or business or merely a hobby. The IRS weighs a set of factors, and no single one decides it.

| Factor | Points to business | Points to hobby |

|---|---|---|

| Regularity | Ongoing, continuous operation. | Occasional or sporadic. |

| Profit motive | Run to make money, with a plan. | For interest or fun, profit incidental. |

| Effort and time | Significant, businesslike effort. | Minimal, set-and-forget. |

| Records | Books, receipts, separate accounts. | Little or no recordkeeping. |

| Scale | Meaningful rigs, hosting, expense. | A single machine in spare time. |

Reporting mining income

When you mine as a business, each block reward or payout is income at its fair market value in US dollars when you receive it. That total is your business gross income on Schedule C. As with other earned crypto, the receipt value also becomes the cost basis of those coins, so a later sale is a separate capital gain or loss, not double-counted income.

Deductible expenses

This is where the business classification pays off. Ordinary and necessary costs of running the operation reduce your taxable income.

- Mining hardware. Rigs, ASICs, and GPUs are usually capitalized and depreciated over time, though some elections can accelerate the deduction. Track purchase dates and costs.

- Electricity. Often the largest cost. Deduct the business portion, and if you mine from home, allocate carefully between business and personal use.

- Hosting and rack fees. Colocation, data center, and hosting charges are deductible.

- Internet and connectivity. The business portion of internet costs.

- Repairs and maintenance. Fans, parts, and servicing to keep rigs running.

- Pool fees. Fees paid to mining pools.

- Home office, where a dedicated space qualifies under the rules.

Self-employment tax

The cost of business treatment is self-employment tax. Your net profit from Schedule C (income minus deductions) flows to Schedule SE, which computes self-employment tax at about 15.3%, covering Social Security (12.4%) and Medicare (2.9%). This is in addition to regular income tax on the same profit. You do get to deduct half of the self-employment tax as an adjustment to income, which softens the blow slightly.

The $48,000 of mined coins is business income, the $24,000 net profit after deductions carries roughly $3,391 of self-employment tax (after the standard net earnings adjustment), and income tax applies to that profit at your ordinary rate. Selling the mined coins later is a separate capital gain or loss on Form 8949, measured from the $48,000 receipt value.

Running a mining or validator operation?

Business crypto means income, depreciation, expenses, and self-employment tax all in one place. We build clean books so your Schedule C deductions hold up and your numbers tie out.

See how it worksNode and validator operations

Running validator nodes or other infrastructure for rewards can also rise to a business. If you operate validators regularly, with real effort and a profit motive, the rewards are business income on Schedule C and your costs (servers, bandwidth, hardware, monitoring) are deductible, with self-employment tax on the net. By contrast, passively delegating or occasionally staking is more likely ordinary income on Schedule 1 without business treatment. The line is the same trade-or-business test, applied to your actual operation.

A note on entities

Many serious miners eventually consider an entity, such as an S corporation, to manage self-employment tax exposure. That can make sense at scale, but it adds payroll, filings, and complexity, and it is a decision to make with a professional based on your numbers, not a default. Schedule C as a sole proprietor is the starting point for most individual operators.

How mining equipment depreciation works

Hardware is usually the second largest cost after electricity, and the way you deduct it is more nuanced than simply writing off what you spent. Equipment with a useful life of more than a year is generally a capital asset, which means its cost is recovered over time through depreciation rather than deducted all at once. The default schedule spreads the deduction across several years, matching the deduction to the period the rigs actually produce income.

There are elections that can accelerate this. Provisions that allow immediate expensing of qualifying equipment, and bonus depreciation rules, can let a mining business deduct a large portion of new hardware in the year it is placed in service. That can be powerful in a profitable year, but it is a timing choice with consequences: a big upfront deduction means smaller deductions later and a lower remaining basis if you sell the rigs. The right answer depends on your income curve, so this is a classic place to plan rather than guess.

Recordkeeping for a mining business

The difference between deductions that hold up and deductions that get disallowed is almost always records. A mining business should keep documentation that would satisfy an examiner without a scramble.

- Income log. Every block reward or payout, with the date, the coin and quantity, and the fair market value in dollars at receipt. This is both your income and the basis of those coins.

- Expense receipts. Invoices for hardware, monthly utility bills, hosting statements, internet bills, repair receipts, and pool fee records.

- Electricity allocation. If you mine from home, a defensible method for splitting business electricity from household use, such as a dedicated meter or a reasonable square-footage and load calculation.

- Depreciation schedule. A running list of each machine, its cost, its in-service date, the method used, and the deduction taken each year.

- A separate account. A dedicated bank account and wallet for the business keeps personal and business activity from blending, which is one of the strongest signals of a real business.

Strong records do double duty. They support the deductions that lower your tax now, and they preserve the cost basis you need when you eventually sell the mined coins, so the capital gains side of the operation is accurate too.

The 2025/26 Crypto Tax Guide. Built by former Big 4 accountants.

A printable, step-by-step guide and checklist to reconcile every coin and wallet, recover missing cost basis, and file accurately before the deadline.

- Form 8949, Schedule D, and Schedule 1 walkthroughs

- How to handle staking, DeFi, NFTs, and lost coins

- The $0-basis 1099-DA trap (and how to avoid it)

- FBAR, Form 8938, and foreign exchange reporting