Key takeaways

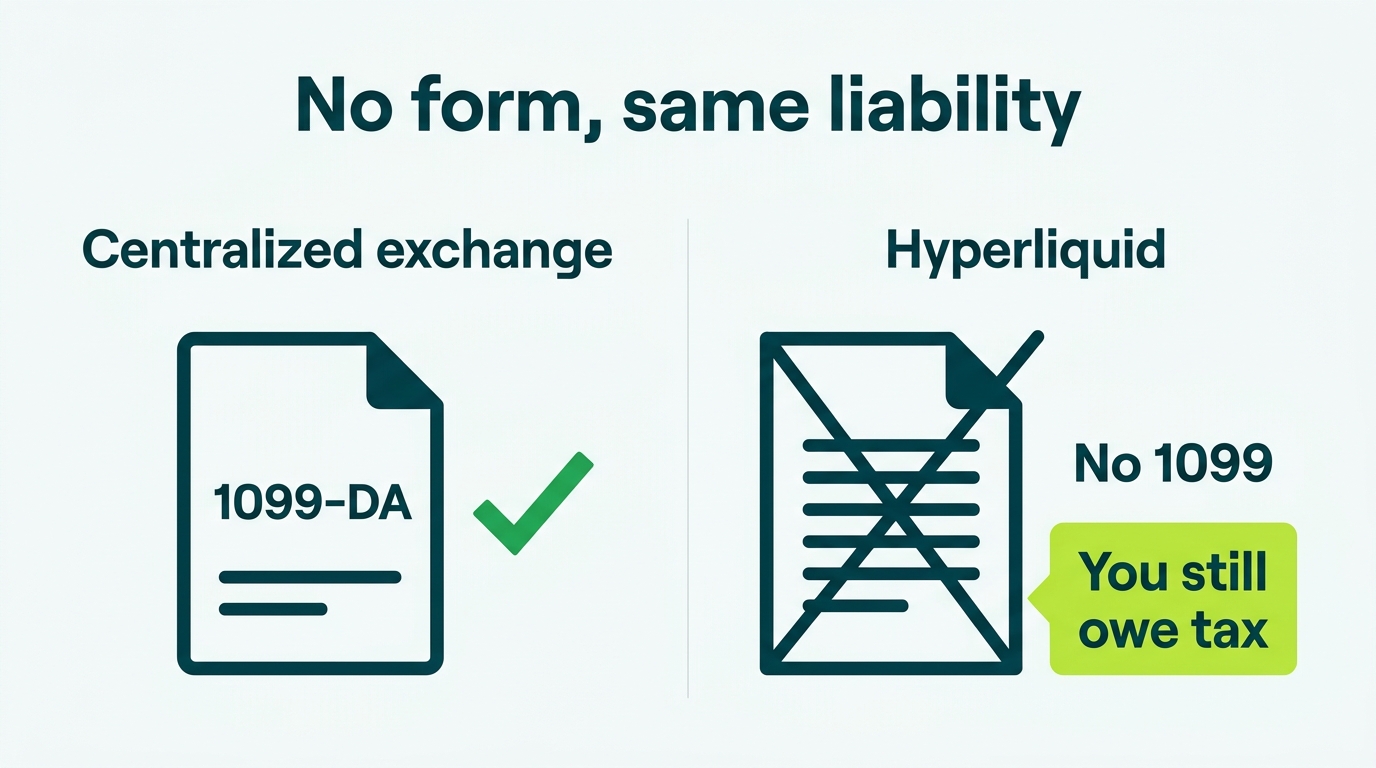

- No 1099, full self-report. Hyperliquid is non-custodial and non-KYC, so it issues no tax forms and reports nothing. The liability is still 100% yours.

- Perps are not 60/40. Hyperliquid perps almost certainly fail the Section 1256 test, so the safe position is short-term capital gain or loss on each closed position.

- Funding payments are unsettled. Conservatively, funding received is ordinary income and funding paid is an expense. Document whichever method you pick.

- The HYPE airdrop was taxable income. Tokens received in November 2024 were ordinary income at value on receipt, a real bill even for people who never sold.

Hyperliquid is the hardest major venue to report correctly, and it is not close. It is a decentralized exchange on its own Layer 1, running on-chain perpetual futures with leverage, plus spot markets, with no broker, no KYC, and no tax forms. That combination means high-frequency trading, funding payments, and a large airdrop all land on you to track and characterize. We will be honest where the law is unsettled, because pretending these questions are simple is exactly how people get audited.

Does Hyperliquid report to the IRS?

No. Hyperliquid is a decentralized exchange built on its own blockchain, with on-chain settlement, no central broker, and no KYC. Because of that, it does not issue Form 1099-DA and does not report your activity to the IRS. The new broker-reporting rules that put exchanges like Coinbase and Kraken on the hook for 1099-DAs target custodial, centralized brokers; pure self-custody DeFi activity falls outside that mandatory third-party reporting.

The trap is reading "no form" as "no tax." Your obligation to report every taxable event is unchanged. The only thing missing is the paperwork that would have helped you (and reminded the IRS). You still answer "Yes" to the Form 1040 digital-asset question and report all of it.

How are Hyperliquid perpetual futures taxed?

This is the most uncertain area on the page, so treat it carefully. There is no IRS guidance directly addressing on-chain crypto perpetual swaps. A perp is economically a cash-settled derivative with no expiry, settled in USDC margin.

Why perps are not 60/40 (no Section 1256)

Section 1256 gives certain regulated contracts a favorable 60/40 split (60% long-term, 40% short-term regardless of holding period). To qualify, a contract generally must trade on a regulated US board of trade or qualified exchange, like the CME. Regulated US crypto futures (CME Bitcoin and Ether futures) can qualify. Hyperliquid does not. It is offshore, unregulated, on-chain, and not on the qualified-exchange list, so do not report its perps on Form 6781 as 60/40. That would be a clear overreach.

Conservative vs. aggressive on perp PnL

| Question | Conservative (our lean) | Aggressive |

|---|---|---|

| Character of realized perp PnL | Short-term capital gain/loss per closed position (Form 8949 / Schedule D) | Ordinary, or trader §475(f) mark-to-market election |

| 60/40 treatment | Do not claim, fails Section 1256 | Claim 60/40 (not supportable here) |

| Year-end open positions | Not deemed sold; recognize on close | Mark continuously (only with a §475(f) election) |

The defensible default is to treat each closed position's realized PnL as a short-term capital gain or loss. High-volume traders who may qualify as a trader in commodities should get specialist advice before considering a mark-to-market election. Whatever you choose, document the method and apply it consistently.

Funding payments: the other gray area

Perps charge periodic funding between longs and shorts, and no IRS guidance addresses it. Two framings:

- Conservative (our lean): funding received is ordinary income at value when received (Schedule 1); funding paid is a trading expense. This is the safer reporting posture.

- Aggressive / simplifying: net funding into each position's PnL, so it folds into the capital gain or loss on close. Cleaner operationally, but not blessed by the IRS and can understate ordinary income in net-positive years.

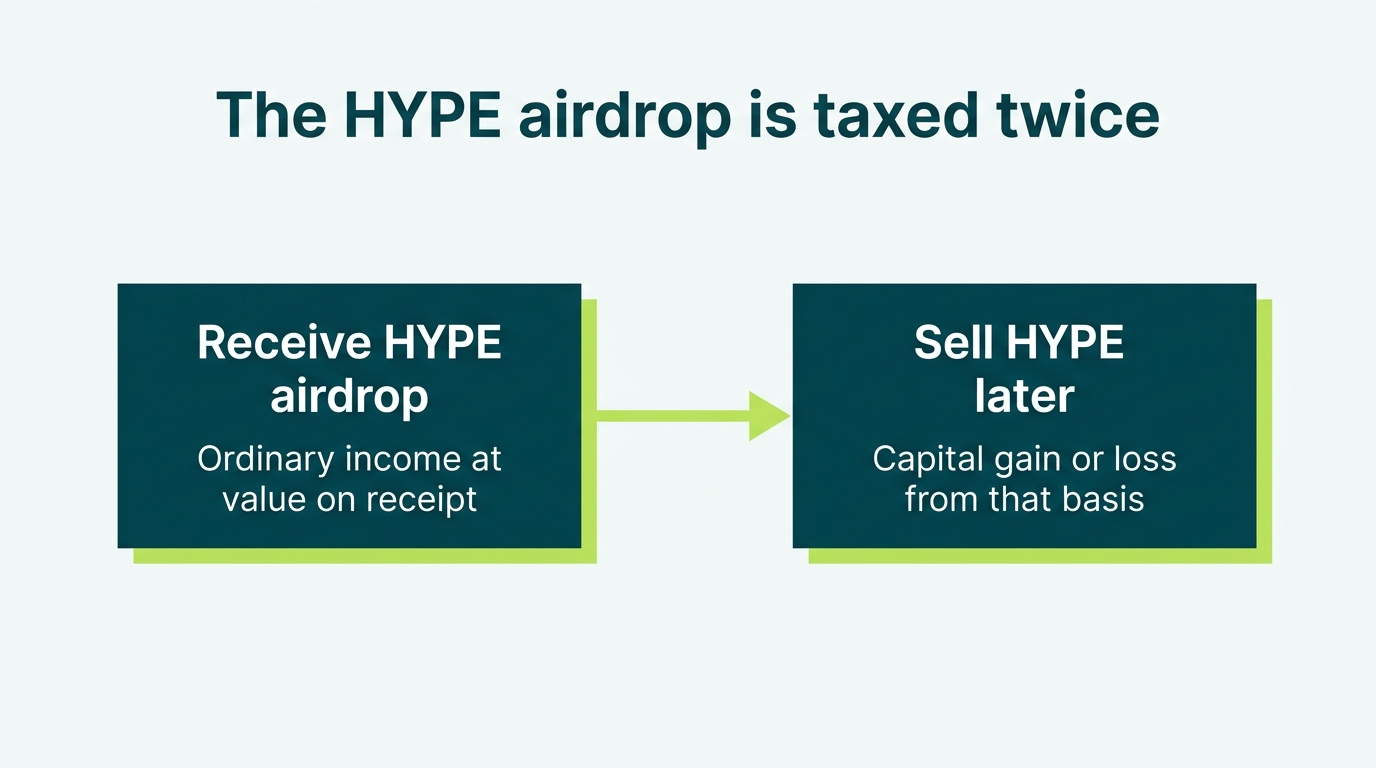

The HYPE airdrop tax trap

On November 29, 2024, Hyperliquid's genesis event distributed roughly 310 million HYPE (about 31% of supply) to early users. For US recipients, this was a major taxable event.

- Layer 1, at receipt: ordinary income equal to the HYPE's fair market value when you gained dominion and control (following the IRS airdrop and staking-reward framework). That FMV becomes your cost basis. Reported on Schedule 1.

- Layer 2, at sale: a separate capital gain or loss equal to your sale proceeds minus that basis.

Points and pre-token programs

Hyperliquid ran points-based programs before the token launch, and may again. The conservative consensus: accruing points is generally not a taxable event, because points typically have no ascertainable value and confer no present property right. Income arises when points convert to an actual token with value that you control, taxed as ordinary income at that value (the same airdrop logic as HYPE). This is unsettled, so the safe posture is no income until a controllable token with value is received.

Spot trading and per-wallet basis

Hyperliquid spot trading follows standard crypto property rules. Every crypto-to-crypto swap is a taxable disposal (USDC to HYPE, HYPE to another token), with gain or loss measured from your cost basis. Since January 1, 2025, basis must be tracked per wallet under Rev. Proc. 2024-28, with FIFO as the default and specific identification allowed if documented. For a self-custodied Hyperliquid wallet, track its basis separately from your other wallets and exchanges. Gas and fees paid in crypto are themselves small disposals.

Thousands of perp fills, funding events, and an airdrop?

Hyperliquid is the hardest venue to reconcile, period. We pull the full on-chain history and characterize perps, funding, and HYPE correctly.

Wash sales and loss harvesting

Under current law, the wash-sale rule (Section 1091) applies only to securities, and crypto is treated as property, so it does not currently disallow crypto losses, spot or perp. Proposed legislation could extend a wash-sale rule to digital assets, but even if enacted it would most likely target spot assets, not cash-settled perps, which are contracts rather than the underlying asset. Confirm the current-year status before harvesting, and avoid transactions with no purpose beyond the loss.

The reporting gap and where people go wrong

Accurate Hyperliquid reporting is hard for real reasons, and that is exactly where filers slip:

- Assuming "no 1099" means "no tax." The single most common and most dangerous mistake.

- Wrongly claiming 60/40 on perps, which do not qualify.

- Ignoring funding payments entirely.

- Skipping the HYPE airdrop income in the year of receipt.

- Treating crypto-to-crypto spot swaps as non-taxable.

- Using pooled basis instead of per-wallet after 2025.

- Answering "No" to the 1040 digital-asset question after trading.

How to report Hyperliquid on your tax return

- Form 8949 and Schedule D for capital dispositions: spot trades, crypto-to-crypto swaps, gas-spends, perp realized PnL (conservative position), and later sales of HYPE.

- Schedule 1 for ordinary income: the HYPE airdrop at receipt, any points-token receipts, vault yield, and net funding received under the conservative method.

- Not Form 6781. Hyperliquid perps are not Section 1256 contracts.

- The Form 1040 digital-asset question must be answered "Yes."

The 2025/26 Crypto Tax Guide. Built by former Big 4 accountants.

A printable, step-by-step guide and checklist to reconcile every coin and wallet, recover missing cost basis, and file accurately before the deadline.

- Form 8949, Schedule D, and Schedule 1 walkthroughs

- How to handle staking, DeFi, NFTs, and lost coins

- The $0-basis 1099-DA trap (and how to avoid it)

- FBAR, Form 8938, and foreign exchange reporting