Key takeaways

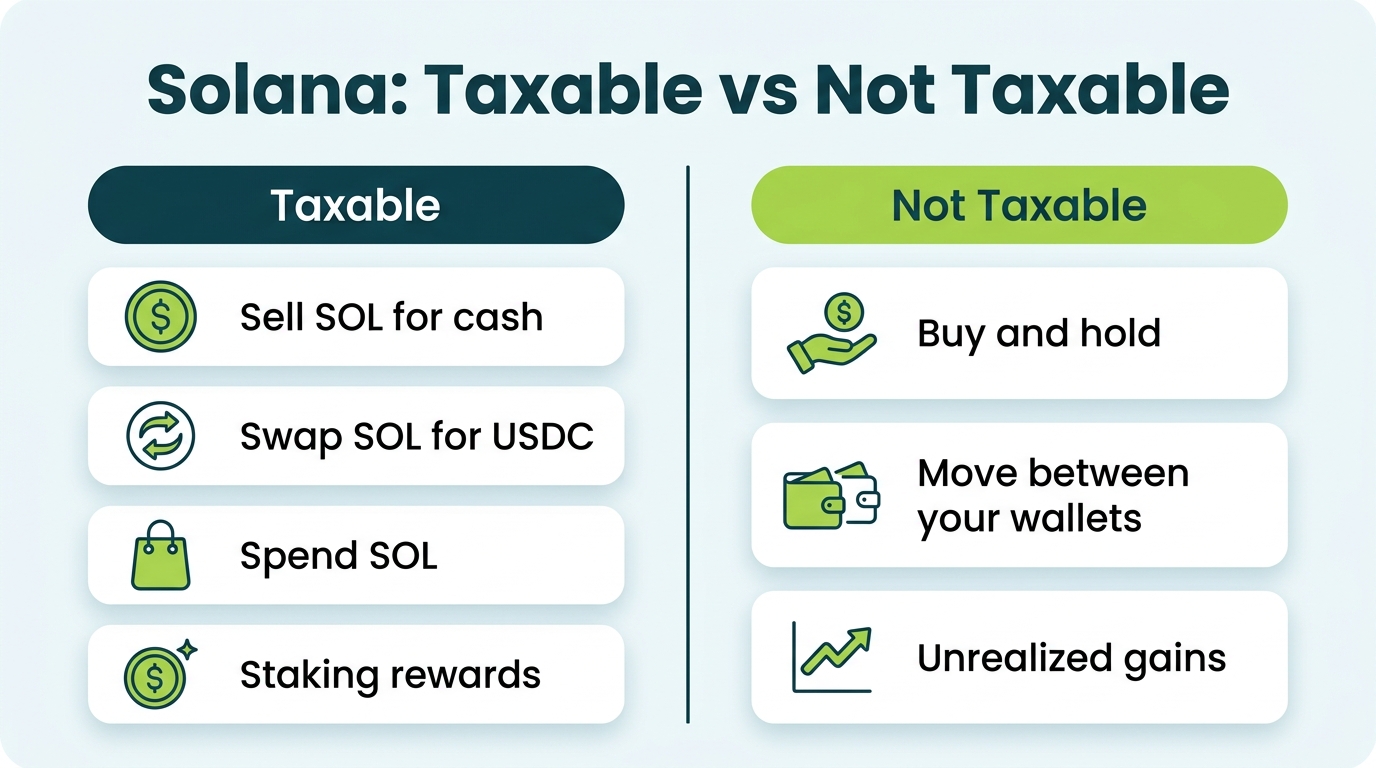

- Holding SOL is free; disposing of it is taxable. Selling, trading, or spending SOL triggers capital gains. Buying and holding does not, no matter how much it appreciates.

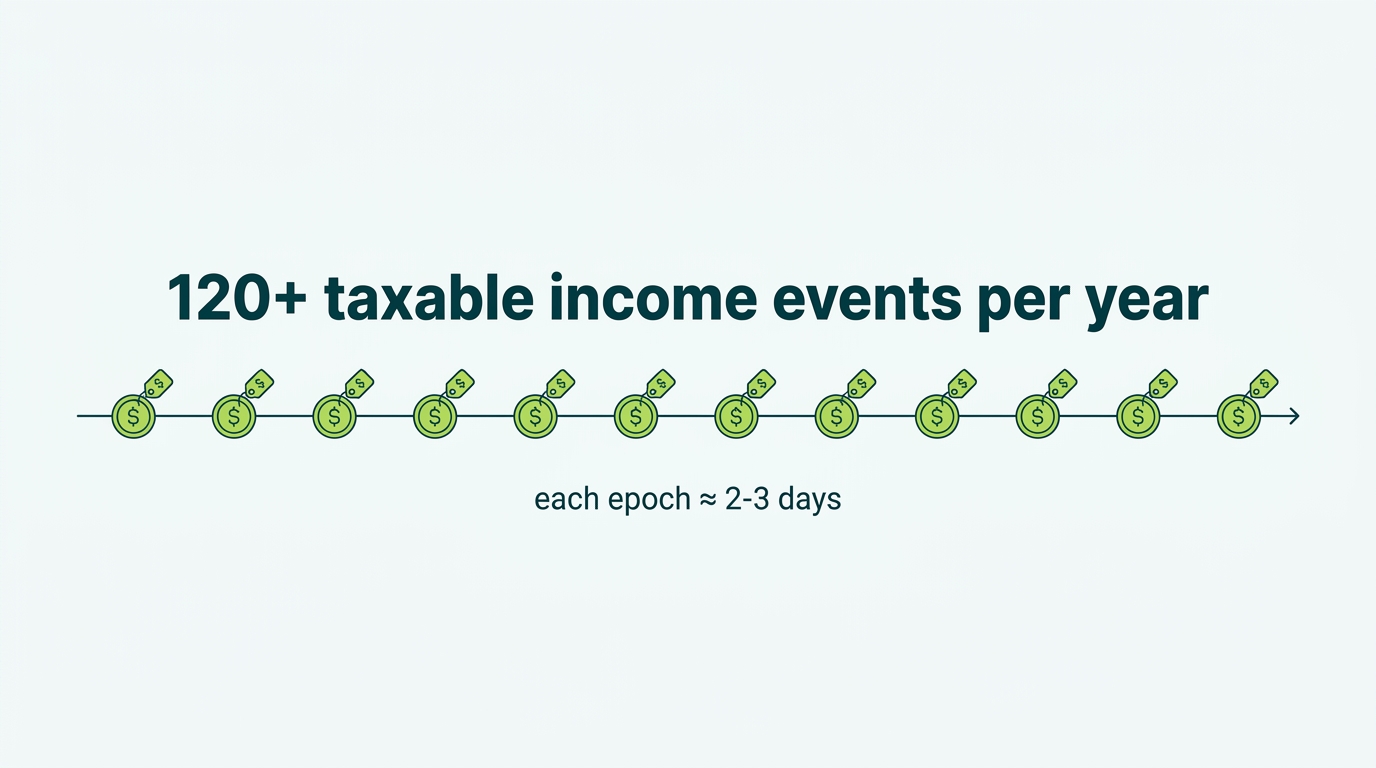

- Staking rewards are income, epoch by epoch. Each reward of roughly every 2 to 3 days is ordinary income at that day's value, which can mean 120+ dated income events per year per stake account, even though the rewards auto-compound and you never press claim.

- Liquid staking is the biggest gray area in crypto tax. Whether minting or redeeming mSOL, JitoSOL, or bSOL is taxable is unsettled. There is a conservative position and an aggressive one, and the rule that protects you is consistency.

- The IRS now gets a copy of exchange sales. Form 1099-DA reporting is live for SOL sold on US platforms, while your Phantom wallet activity stays your responsibility to reconstruct and report.

Solana attracts the most active users in crypto: stakers, airdrop farmers, DeFi traders, NFT minters, and wallets with thousands of transactions a year. That activity is exactly what makes SOL one of the hardest assets to report correctly. The surface rules are settled, but several of the most common Solana actions land in territory where the IRS has said nothing and your reporting choice genuinely matters. Most guides gloss over those questions. This one answers them directly, flags every gray area as a gray area, and shows the conservative and aggressive positions so you can choose deliberately instead of by accident.

Do you have to pay taxes on Solana?

Yes, in two different ways. The IRS classified cryptocurrencies as property under Notice 2014-21, and SOL is no exception. The same framework that covers stocks and real estate covers Solana.

- Capital gains apply when you dispose of SOL: selling it for dollars, trading it for another token (including stablecoins), or spending it on anything, from an NFT to a coffee. Your gain or loss equals what you received minus your cost basis.

- Ordinary income applies when you earn SOL or other tokens: staking rewards, airdrops, validator commissions, lending interest, and getting paid in SOL are all taxed at fair market value on the day you receive them.

What is never taxable matters just as much. Buying SOL with dollars is not taxable; it just sets your cost basis. Holding is not taxable through any amount of appreciation, because the US does not tax unrealized gains. And moving SOL between wallets you own, from Coinbase to Phantom for example, is not a disposal. The basis and holding period travel with the coins.

What counts as a taxable event for Solana?

Here is how the common Solana actions are treated for the 2026 tax year.

| Action | Taxable? | Treatment |

|---|---|---|

| Buy SOL with USD | No | Not taxable. Sets your cost basis. |

| Hold SOL | No | No tax while holding, even through big rallies. |

| Sell SOL for USD | Yes | Capital gain or loss (proceeds − basis). |

| Trade SOL for another token | Yes | Disposal of SOL; capital gain or loss. |

| Spend SOL (incl. buying an NFT) | Yes | Treated as selling SOL; capital gain or loss. |

| Native staking rewards | Yes | Ordinary income at value when received, each epoch. |

| Airdrops (JUP, JTO, W, PYTH) | Yes | Ordinary income at value on receipt. |

| Validator commissions | Yes | Ordinary income; usually a Schedule C business. |

| Lending interest (marginfi, Kamino) | Yes | Ordinary income at value when received. |

| Move SOL between your own wallets | No | Not taxable; basis and holding period carry. |

| Wrap SOL to wSOL | Gray | Usually treated as non-taxable (see DeFi section). |

| Mint or redeem mSOL / JitoSOL / bSOL | Gray | Unsettled. Conservative view: taxable trade (see below). |

The trade row catches more people than any other. Swapping SOL for USDC or JUP on Jupiter feels like a sideways move, but the IRS sees a completed sale of your SOL at that moment's price. No dollars need to touch your bank account for a taxable gain to exist, and a DEX will never send you a form reminding you.

Solana tax rates for 2026

There is no special "Solana tax rate." For disposals, the rate depends on how long you held before selling and your total taxable income. One date does most of the work: the one-year mark.

- Short-term gains (held one year or less) are taxed at your ordinary federal rate, 10% to 37%.

- Long-term gains (held more than a year) are taxed at 0%, 15%, or 20%. Most filers land at 15%.

- Staking rewards, airdrops, and other earned SOL are ordinary income at receipt, regardless of how long you later hold the tokens. Each reward starts its own one-year holding clock.

- High earners may owe an extra 3.8% Net Investment Income Tax once modified income passes $200,000 single or $250,000 married filing jointly. SOL capital gains clearly count toward it.

- State tax can apply on top; most states tax crypto gains as ordinary income, while a handful (Texas, Florida, Wyoming, and others) have no state income tax at all.

Here are the 2026 federal long-term capital gains brackets that apply to SOL held more than one year:

| 2026 long-term rate | Single / MFS | Married Filing Jointly | Head of Household |

|---|---|---|---|

| 0% | Up to $49,450 | Up to $98,900 | Up to $66,200 |

| 15% | $49,451–$545,500 | $98,901–$613,700 | $66,201–$579,600 |

| 20% | Above $545,500 | Above $613,700 | Above $579,600 |

Short-term gains stack on top of your other income and get taxed at whatever ordinary bracket they land in. For active Solana traders flipping tokens inside a year, that means DEX profits are taxed like salary, not like investments.

How are Solana staking rewards taxed?

Staking rewards are ordinary income. Under IRS Revenue Ruling 2023-14, staking rewards are taxed at fair market value when you gain "dominion and control," meaning the moment you can sell or move them. The ruling explicitly covers staking through an exchange like Coinbase or Kraken as well as native delegation from your own wallet.

On Solana, the timing question has a specific answer that surprises people. Rewards are distributed once per epoch, roughly every 2 to 3 days, and for native stake accounts they auto-compound straight back into your delegated stake. There is no claim button. The conservative, majority position is that each epoch's reward is its own income event, valued in dollars at that epoch's timestamp, because you could deactivate and withdraw it at any time. The absence of a claim step does not defer the income.

How to report staking rewards on your tax forms

The mechanics are simpler than the tracking. For a typical delegator:

- Total the year's rewards at receipt value. Sum the fair market value of every epoch's reward on the day it landed. That total is your staking income for the year.

- Report it on Schedule 1, Line 8 as other income. Exchange staking programs may also send you a 1099-MISC once rewards pass $600; report the income either way.

- Record each reward as a cost basis lot. The value you reported as income becomes the basis of that reward SOL, so it is not taxed twice when you sell.

- Report later sales on Form 8949 and Schedule D, measuring gain or loss from each lot's reward-date value, short-term or long-term based on each lot's own clock.

Validators and anyone staking as a business report the income on Schedule C instead, which changes the deduction and self-employment tax picture (covered next). Our guide to staking, mining, and airdrop income covers the income side in more depth.

Auto-compounded rewards from stake pools and yield aggregators

Stake pools and yield aggregators that compound rewards for you do not make the income question go away; they change whose hands the rewards land in. If a service claims and restakes rewards into your own stake account or wallet, each compounding event is still your income at that day's value. If you hold a pool token whose redemption value grows instead (the liquid staking model), the analysis shifts to the token itself, which is the next section. The practical rule: know which structure you are in, because the tax answers diverge sharply.

Staking also has its own deep dive: our full guide to Solana staking taxes walks through per-epoch income tracking, price sourcing, and how to clean up past years.

Validator and node operator taxes: business or hobby?

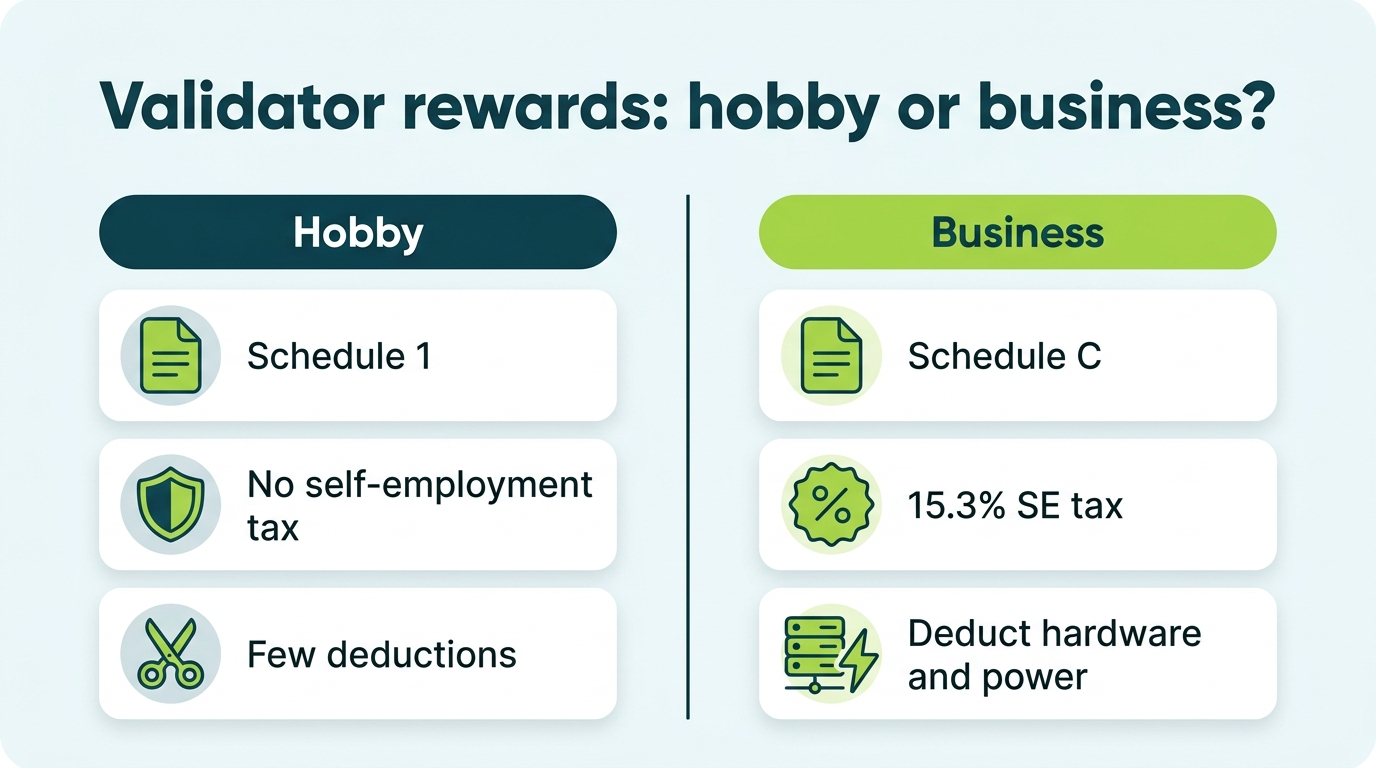

Running a Solana validator is a different tax animal from delegating. Commission income skimmed from delegators' rewards, block rewards, and priority fees and MEV tips (for operators running the Jito client) are all ordinary income at fair market value when received. The real question is whether the operation is a business or a hobby, and for validators the answer is usually business, because the activity is continuous, profit-motivated, and expensive to run.

- Business (Schedule C). Report all validator income, deduct real expenses: server hardware or bare-metal hosting, data center fees, and crucially Solana's vote transaction costs, which run around 1 SOL per day and are one of the largest genuine operating expenses in the ecosystem. Bonus depreciation lets you write off hardware in the year it enters service. The trade-off is 15.3% self-employment tax on net profit and quarterly estimated payments.

- Hobby (Schedule 1). A small operator without profit motive reports income as other income and deducts essentially nothing. For anyone burning a SOL a day on vote fees, hobby treatment is usually both implausible and expensive.

Either way, every SOL received creates a dated income lot with its own basis, and the later sale is a separate capital gain or loss. Validator books are effectively small-business books, and they deserve the same rigor.

Liquid staking taxes: mSOL, JitoSOL, and bSOL

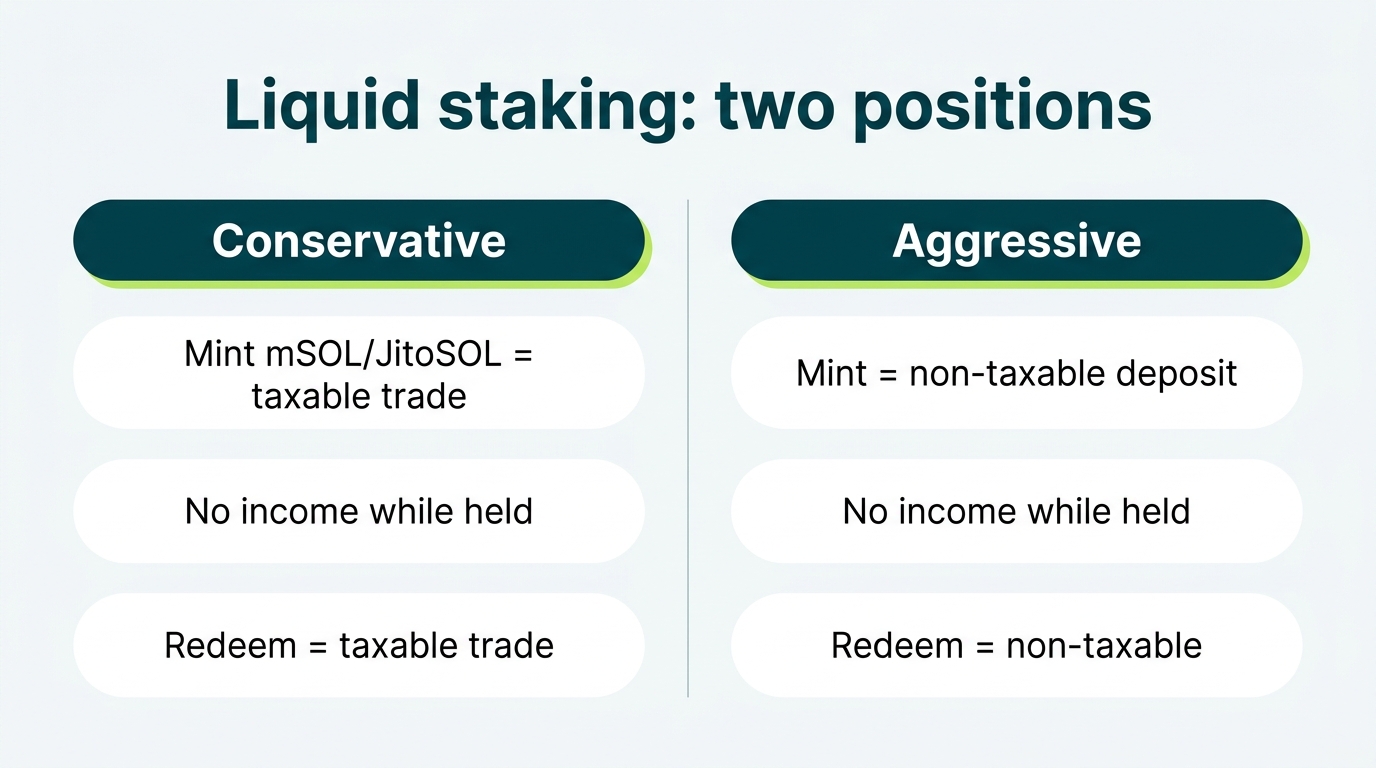

This is the sharpest unsettled question in Solana taxation, and one almost every serious SOL holder touches. Liquid staking tokens (LSTs) like Marinade's mSOL, Jito's JitoSOL, and BlazeStake's bSOL are value-accrual tokens: your token count stays the same while each token's redemption value against SOL grows as staking rewards build in the pool. Three moments matter, and the IRS has issued guidance on none of them.

| Event | Conservative position | Aggressive position |

|---|---|---|

| SOL → mint mSOL / JitoSOL / bSOL | Taxable crypto-to-crypto trade; gain or loss on the SOL | Non-taxable deposit |

| Holding while redemption value grows | No income during the hold; growth is captured as gain at disposal | No income during the hold |

| Redeem token → SOL | Taxable trade; gain or loss on the token | Non-taxable withdrawal |

| Swap one LST for another (mSOL → JitoSOL) | Taxable trade both ways | Taxable trade (hard to argue otherwise) |

Jito Labs commissioned a legal memorandum (a Fenwick analysis) arguing that minting and redeeming JitoSOL are not taxable events, essentially treating the LST as a receipt for deposited SOL. The memo is thoughtful, but it is not IRS guidance, not binding, and untested in court. The cautious route treats the mint and the redemption as taxable trades, exactly like any other token swap.

Notice what both positions share: no ordinary income lands while you hold the token. That is the structural tax difference between LSTs and native staking. A native staker recognizes income every epoch at ordinary rates. An LST holder's reward accrual shows up as a higher redemption value, taxed as capital gain when the position is disposed of, and at long-term rates if held over a year. Under current law that makes LSTs arguably the more tax-efficient way to stake, which is exactly the kind of asymmetry the IRS may eventually close. Until it does, the rule that protects you is consistency: do not treat the mint as non-taxable and then also skip the gain on redemption, or you invite the worst of both outcomes on audit.

We cover mSOL, JitoSOL, and bSOL in much more depth, including both tax positions and what to do about prior years, in our full guide to Solana liquid staking token taxes.

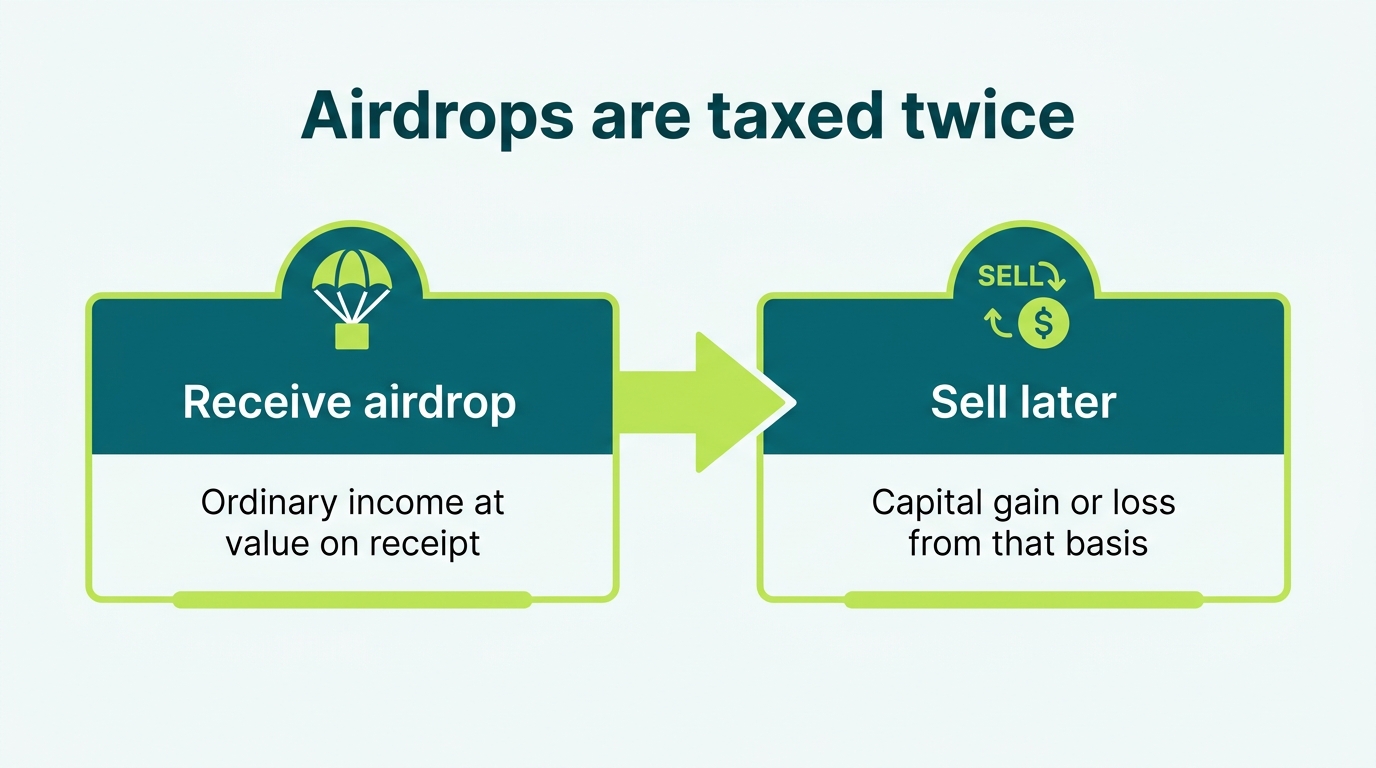

Solana airdrop taxes: JUP, JTO, PYTH, and Wormhole

Airdropped tokens are ordinary income at fair market value when you gain dominion and control, reported on Schedule 1, Line 8. That value becomes your cost basis, and selling later is a separate capital gain or loss. In effect, airdrops are taxed in two layers: income when received, then gain or loss when sold.

The 2024 Solana airdrop season (JTO, JUP, PYTH, Wormhole's W, and dozens of smaller drops) handed active users large one-time income even if they never sold a token. When those tokens later fell, many were left with "phantom income": a real tax bill measured at claim-day prices on value that had since evaporated. The lesson for every future drop is the same: know the income hit on the day you claim, and decide deliberately whether to sell enough to cover the tax.

Airdrops and the net investment income tax

Large airdrops interact with the 3.8% Net Investment Income Tax in a way almost nobody prices in. Capital gains from selling SOL or airdropped tokens clearly count as net investment income. Whether the airdrop income itself counts is less settled, but the bigger effect is mechanical: a five-figure JUP claim raises your modified adjusted gross income, and once MAGI crosses $200,000 (single) or $250,000 (joint), the 3.8% surtax switches on for your investment income, including gains you realized elsewhere that year. A big claim year is exactly the wrong year to also realize large gains casually. If a drop pushed your income near the threshold, model the surtax before selling anything else.

Staked, minted, farmed, or claimed on Solana?

Per-epoch rewards, liquid staking positions, and airdrop claims are exactly the activity DIY tools get wrong. We reconcile your full Solana history, gray areas included, into defensible, CPA-ready numbers.

Claim timing, valuing illiquid tokens, spam triage, and the NIIT math all get full treatment in our dedicated guide to Solana airdrop taxes.

Solana DeFi taxes: Raydium, Orca, marginfi, and Kamino

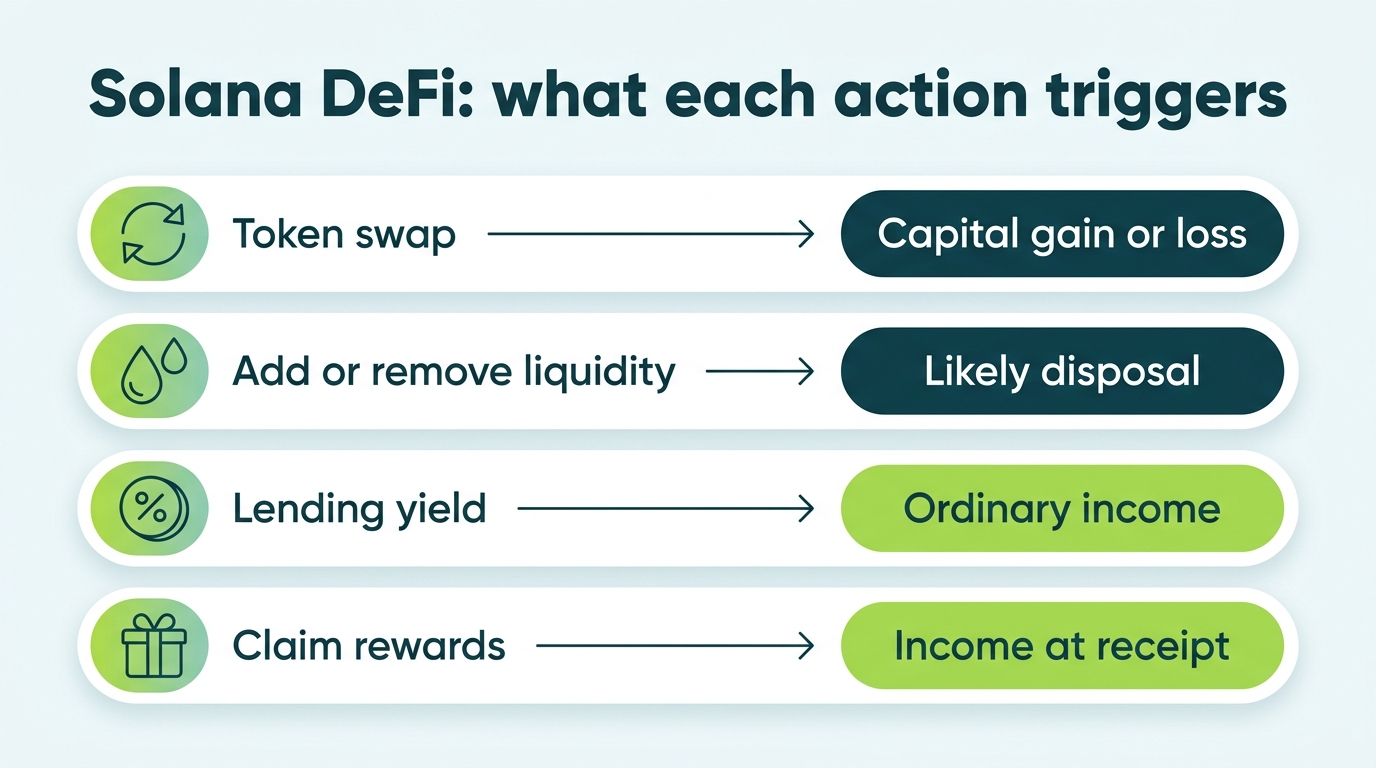

Solana DeFi compounds every problem above, because a single strategy can chain swaps, deposits, receipts, and rewards into dozens of taxable touchpoints. The conservative treatment of the common actions:

- DEX swaps on Jupiter, Raydium, or Orca are taxable crypto-to-crypto trades, every single one, including stablecoin legs.

- Adding liquidity to a Raydium or Orca pool and receiving an LP token or position NFT is often treated as a taxable disposal of the deposited tokens. This is unsettled, with an aggressive non-taxable-deposit view mirroring the LST debate.

- Trading fees and farming rewards are ordinary income at value when earned or claimed.

- Removing liquidity disposes of the LP position; impermanent loss becomes a realized gain or loss at that point.

- Lending deposits on marginfi, Kamino, or Save earn interest that is ordinary income as it is received or credited. The deposit itself, where you receive a receipt token, raises the same gray-area question as LP deposits.

- Borrowing is not taxable. Loan proceeds are not income. But getting liquidated is: a liquidation forcibly disposes of your collateral at market value, realizing gain or loss, often at the worst possible moment.

One more Solana-specific wrinkle: wrapped SOL (wSOL). It is a 1-to-1, no-yield wrapper that programs use to handle SOL like any other token. There is no IRS guidance, but most practitioners treat wrapping and unwrapping as non-taxable, like moving funds between your own pockets, because ownership and value do not change. Even under a strict crypto-to-crypto reading, the gain or loss is approximately zero. The real burden is volume: active DeFi wallets wrap and unwrap constantly, and every event still needs to be logged and matched. Our DeFi taxes guide goes deeper on protocol-level treatment.

For a swap-by-swap map of Raydium LPs, Kamino and marginfi lending, and Jito strategies, see the full guide to Solana DeFi taxes.

Solana NFT taxes: mints, royalties, and compressed NFTs

Solana runs one of the largest NFT markets (Magic Eden, Tensor), and NFTs are taxed as property too.

- Buying an NFT with SOL is two events in one. You disposed of the SOL (capital gain or loss on it) and acquired an NFT with a basis equal to the SOL's value that day.

- Selling an NFT is a capital gain or loss against your basis, short-term or long-term by holding period.

- Minting sets your basis at the SOL you spent, including the mint price and fees. Flipping a mint inside a year is short-term gain at ordinary rates.

- Creator royalties are ordinary income at value when received, and a creator operating as a business reports them on Schedule C with self-employment tax.

- Compressed NFTs (cNFTs) follow the same property rules. Their near-zero mint costs changed the economics, not the tax law: a cNFT airdropped to your wallet is still income if it has real value, and spam cNFTs with no market are best documented at zero and ignored until disposed of.

- The collectibles question is open. The IRS has signaled that some NFTs may be taxed as collectibles at a higher 28% long-term rate under a look-through analysis. Heavy NFT traders should treat this as a live risk, not a footnote.

Mints, royalties, compressed NFTs, and worthless-NFT losses are covered in detail in our guide to Solana NFT taxes.

Rent, gas, and micro-fees: do tiny SOL costs matter?

Solana's fees are famously small, and its rent mechanic is unique: opening a token account parks a small refundable SOL deposit (about 0.002 SOL) that comes back when you close the account. Rent deposits are best treated as transfers to yourself, not disposals, since you get the same SOL back. Transaction fees are technically disposals of SOL at market value, but at fractions of a cent each, their gain or loss is immaterial. The defensible, practical treatment: fees paid to acquire an asset add to its basis, fees paid to sell reduce proceeds, and standalone fees are tiny disposals your software can net automatically. What you should not do is let thousands of dust-level fee events distract from the material items: staking income, LST positions, and airdrop basis. Materiality is a real concept in tax; use it in the right direction.

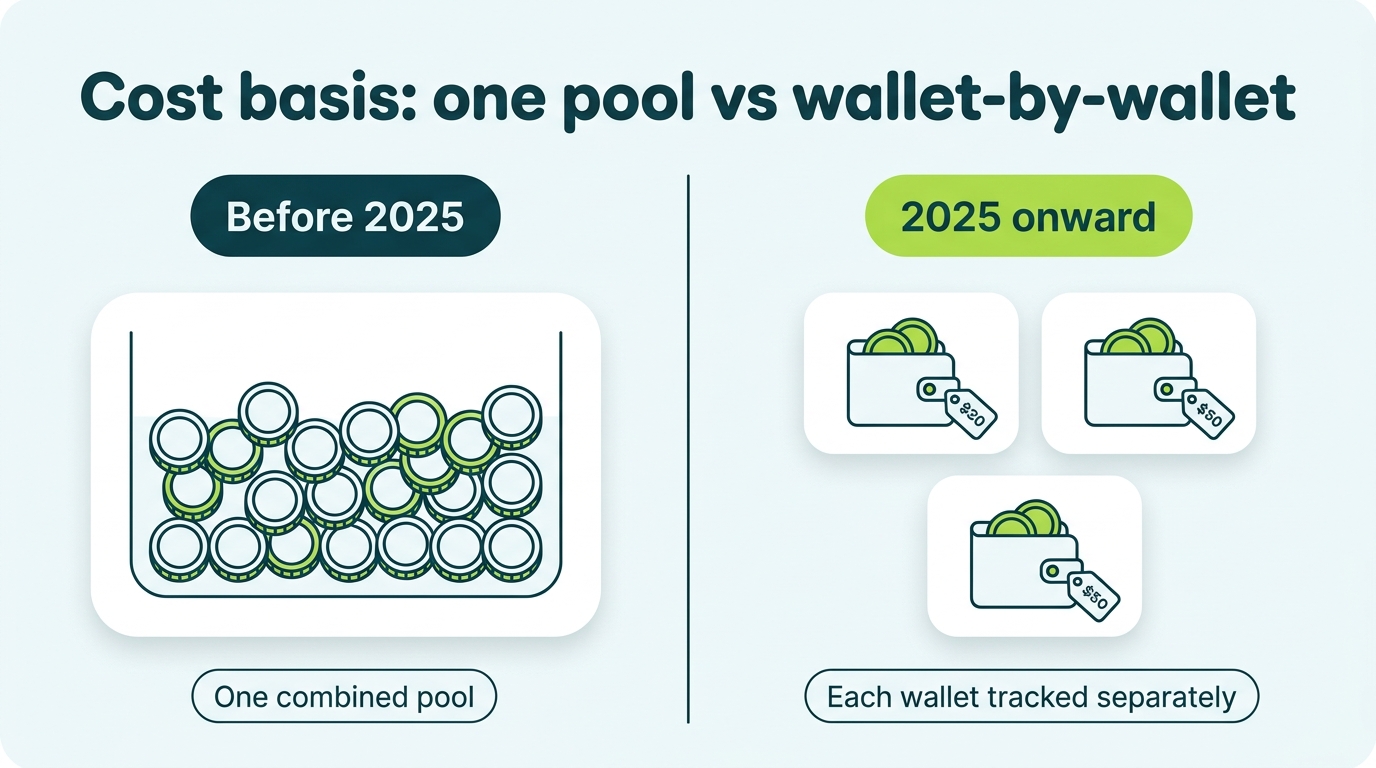

Cost basis and the wallet-by-wallet rule

Your cost basis is what you paid for the SOL, including fees, or the value you already reported as income for earned SOL. Two rules changed recently, and active Solana users are exactly the people they affect.

- Basis is now tracked per wallet. Since January 1, 2025, under Revenue Procedure 2024-28, cost basis must be tracked wallet by wallet and account by account. The old approach of pooling every lot you own into one universal average is no longer allowed. The IRS offered a one-time safe harbor to allocate existing basis across wallets as of that date; if you never did that allocation, do it before your next sale. Our multi-wallet compliance guide walks through the mechanics.

- FIFO is the default, specific identification is the opportunity. Within each wallet, first-in-first-out applies unless you specifically identify which lots you are selling, documented at or before the sale. For a staker holding a 2021 lot next to last month's epoch rewards, lot choice can be the difference between a long-term gain and a short-term one.

For Solana this rule has teeth, because typical users run a Phantom hot wallet, a Ledger, an exchange account, and a few burners. Every transfer between them is non-taxable, but the basis must ride along, and the receiving side of a transfer with missing records becomes a zero-basis time bomb. Reconstruct the trail now, from the public chain and exchange exports, not during an audit.

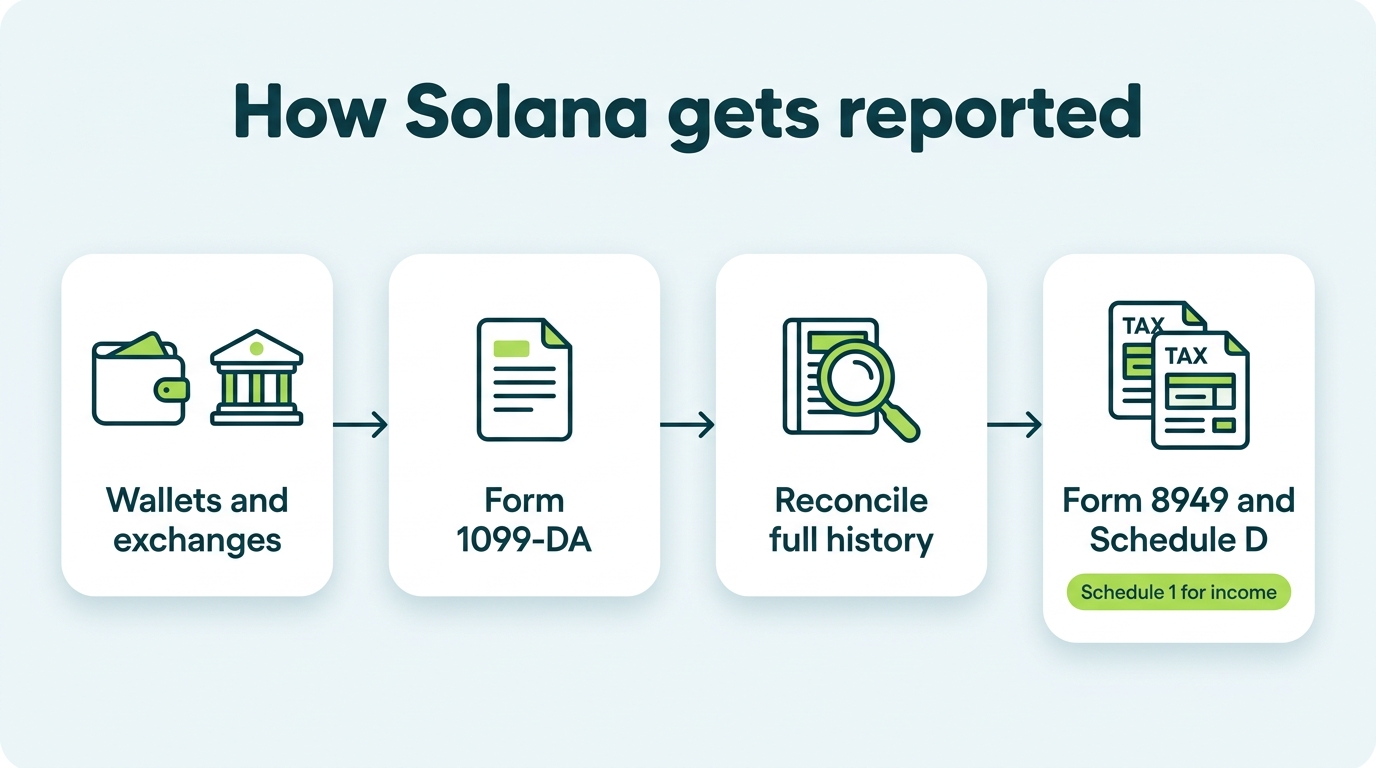

Form 1099-DA and how to report Solana on your return

Starting with tax year 2025, US brokers must file Form 1099-DA, reporting gross proceeds from your SOL sales to both you and the IRS, with cost basis reporting expanding for 2026 sales of covered lots. If you sold SOL on Coinbase, Kraken, or any other US platform, the IRS already has a copy. Our Form 1099-DA guide covers the form line by line.

The catch for Solana holders is what the form does not cover. Self-custody is invisible to 1099-DA. Phantom swaps, DEX trades, staking rewards, LST mints, NFT flips: none of it appears on any broker form, and all of it is reportable. That creates a two-track reconciliation:

- Collect every 1099-DA from each exchange where you sold, and check the proceeds against your own records.

- Fix the basis. If you transferred SOL from Phantom into an exchange before selling, the broker may report zero or missing basis. Supply your true acquisition cost, or the reward-date value for staked SOL, so you are not taxed on the entire sale price.

- Rebuild the on-chain side with software that indexes Solana well, then review the gray-area calls (LST positions, LP deposits) yourself. Software gets you most of the way; judgment closes the gap. See our crypto tax software hub for comparisons.

- List each disposal on Form 8949, total everything on Schedule D, and report staking, airdrop, and other earned income on Schedule 1 (or Schedule C for a validator business).

- Answer "Yes" to the digital asset question on Form 1040 if you sold, traded, spent, or received SOL during the year.

The wash sale rule and Solana tax-loss harvesting

Under current law, the wash sale rule does not apply to SOL. The rule (IRC Section 1091) disallows a loss when you sell a security and rebuy it within 30 days, and the IRS treats SOL as property, not a security. You can sell SOL at a loss, harvest the deduction, and buy it back immediately without waiting out a 30-day window. Harvested losses offset capital gains dollar for dollar, then up to $3,000 of ordinary income per year, with the remainder carried forward indefinitely.

Solana portfolios often hide the best harvesting candidates in plain sight: airdropped tokens trading below their receipt-date basis. A JUP or W position that has fallen since the claim carries a built-in capital loss measured from the income value you already reported. Selling realizes that loss even though the tokens were "free." Three caveats keep this honest: Congress has repeatedly proposed extending the wash sale rule to digital assets, so confirm the current-year law; the economic substance doctrine gives the IRS a tool against trades that exist purely on paper; and if SOL ETFs holding staked SOL sit in your brokerage account, those shares are securities where the wash sale rule does apply. Our crypto wash sale guide covers the strategy and its limits.

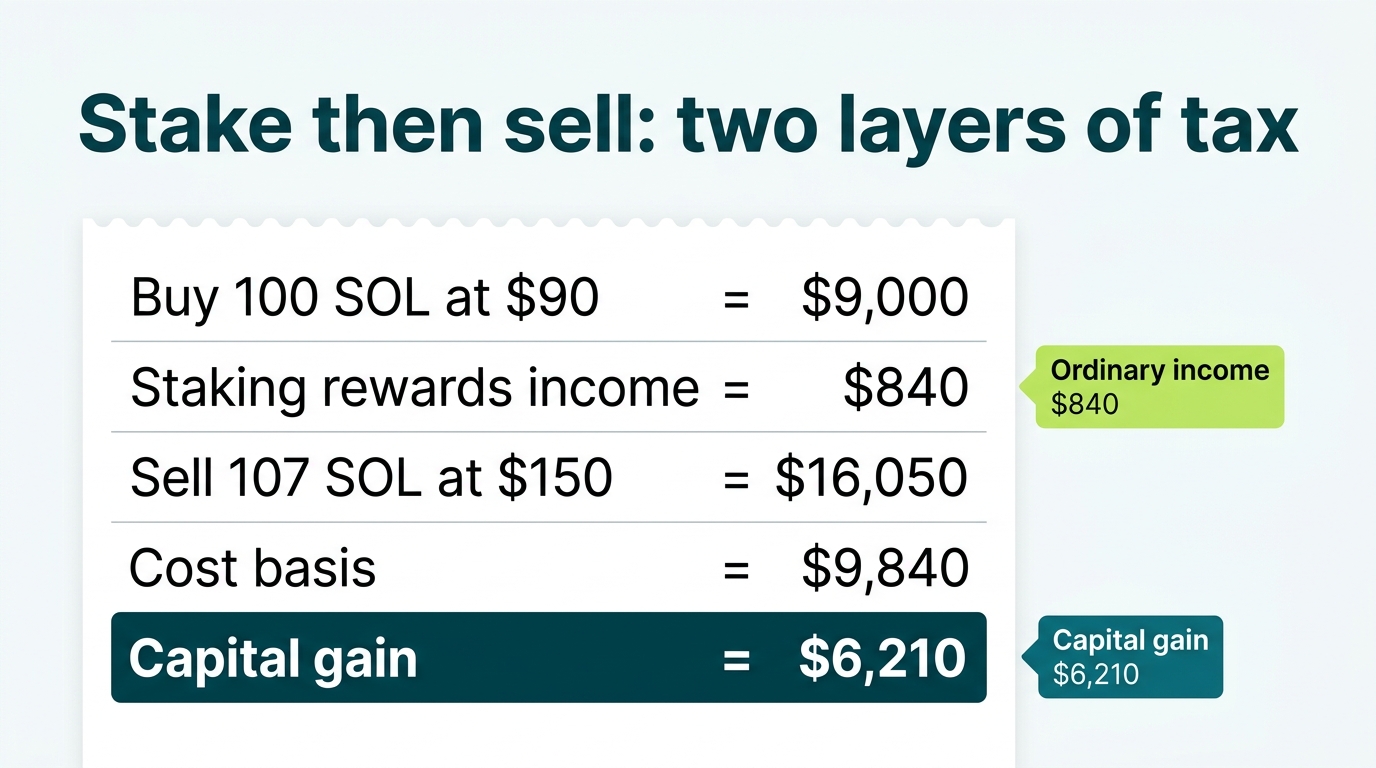

How to calculate your Solana taxes (worked example)

Say you bought 100 SOL at $90 each, staked it for a year, and then sold everything. Here is the simplified two-layer picture.

You are taxed twice in the right way: $840 of ordinary income when the rewards arrived, then a $6,210 capital gain when you sold (long-term for the original lot; each reward lot's holding period runs from its own epoch). The reward SOL's $840 basis is what stops it from being taxed again as if it were free. Miss that basis step and you overpay. In real life those 7 SOL arrived across 150+ epochs at 150+ different prices, which is why this calculation needs software and review, not a weekend and a spreadsheet.

How to reduce your Solana taxes legally

- Hold past one year. Long-term rates of 0%, 15%, or 20% beat ordinary rates of up to 37%. Remember each staking reward lot has its own clock.

- Harvest losses, including airdrop lots. Tokens trading below your receipt-date basis carry real capital losses, and under current law you can rebuy SOL immediately after harvesting.

- Mind your bracket and the NIIT line. Realizing long-term gains in a lower-income year can land in the 0% or 15% band, and keeping MAGI under $200k/$250k avoids the 3.8% surtax. Big airdrop years deserve extra care.

- Consider the LST structure deliberately. Native staking generates ordinary income every epoch; an LST accrues value taxed as capital gain at disposal. Under current law that difference is real money for large positions. Get advice before restructuring.

- Donate appreciated SOL. Giving long-held SOL to a qualified charity avoids the capital gain entirely and can support a fair market value deduction.

- Use specific identification. Choosing which lots to sell, documented per wallet, lets you sell high-basis lots first and leave the 2021 coins undisturbed until you choose to realize them.

- Track reward basis meticulously. The most common overpayment on Solana is forgetting that staked and airdropped tokens already carry a taxed basis.

If your situation spans staking, LSTs, DeFi, and a validator, a crypto tax professional will usually find more than these basics. The rest of our coin-by-coin tax guides cover how the same framework applies to Bitcoin, Ethereum, and other assets you might hold alongside SOL.

Want a professional to handle it?

Book a free 15-minute call and we will map out exactly what your Solana tax situation needs, from per-epoch staking lots to a documented position on your liquid staking tokens.

Solana tax FAQ

Do you have to pay taxes on Solana?

How are Solana staking rewards taxed?

Do I owe tax on staking rewards I never unstaked or sold?

Is swapping SOL for mSOL or JitoSOL taxable?

Is redeeming a liquid staking token back to SOL taxable?

Were Solana airdrops like JUP and JTO taxable even if I never sold?

How do I report Solana staking rewards on my tax return?

Does the wash sale rule apply to Solana?

Do I have to track each Solana wallet separately?

Does the IRS know about my Solana trades?

Is wrapping SOL into wSOL taxable?

Are Solana NFT sales taxable?

The 2025/26 Crypto Tax Guide. Built by former Big 4 accountants.

A printable, step-by-step guide and checklist to reconcile every coin and wallet, recover missing cost basis, and file accurately before the deadline.

- Form 8949, Schedule D, and Schedule 1 walkthroughs

- How to handle staking, DeFi, NFTs, and lost coins

- The $0-basis 1099-DA trap (and how to avoid it)

- FBAR, Form 8938, and foreign exchange reporting