Key takeaways

- Holding XRP is free; disposing of it is taxable. Selling, swapping, or spending XRP triggers capital gains. Buying and holding does not, no matter how far the price runs.

- The Ripple lawsuit never touched taxes, and neither did any Trump policy. There is no XRP tax exemption. Both myths are settled below, with the receipts.

- XRP has no native staking. Anything marketed as XRP staking is an exchange lending or rewards program, and those payouts are ordinary income when received.

- Flare, Songbird, and Spark airdrops are taxable income at the value on the day the tokens became yours to sell, which for many XRP holders was January 2023, not the December 2020 snapshot.

- 1099-DA reporting is live. US brokers began reporting XRP sale proceeds for tax year 2025, and cost basis reporting expands for 2026. Long-time holders with missing basis need to fix that before selling, or the broker's form will tax their entire sale price as gain.

XRP holders are a distinct crowd at tax time. Many bought in 2017 or 2018, held through a delisting era and a four-year lawsuit, collected an airdrop or two along the way, and are only now selling into strength or rotating into the new spot ETFs. That long, messy history creates specific problems: cost basis scattered across dead exchanges, airdrop income nobody reported, and a stubborn set of myths about XRP being tax free. This guide walks through how XRP taxes actually work, what the SEC case did and did not change, how the XRP Ledger's own DEX, AMM, and NFTs are taxed, and how to report cleanly now that brokers send the IRS a copy of your sales.

Do you have to pay taxes on XRP?

Yes, in two different ways: capital gains when you dispose of XRP, and ordinary income when you earn it. The IRS classifies XRP as property under Notice 2014-21, the same framework that covers Bitcoin, stocks, and real estate, and that single classification drives everything else about XRP taxes.

- Capital gains apply when you dispose of XRP: selling for dollars, swapping it for another token (including stablecoins), or spending it. Your gain or loss equals what you received minus your cost basis, which is what you paid for the XRP including fees.

- Ordinary income applies when you earn XRP or related tokens: exchange reward programs, getting paid in XRP, and airdrops like Spark and Flare are all taxed at fair market value on the day you receive them.

Buying XRP with dollars and holding it is never taxable, no matter how much it appreciates. An XRP position that went from $0.30 to $2 creates exactly zero tax until you dispose of some. Moving XRP between your own wallets is not taxable either, though the basis has to travel with the coins on paper. Tax attaches only when something happens: a sale, a swap, a purchase, or income hitting your account.

The property classification also means XRP has no special treatment in either direction. It does not get the favorable rules that apply to some foreign currencies, and it does not get punished with any crypto-specific surcharge. It is taxed like a share of stock you track yourself: gains measured lot by lot, holding periods that flip rates from short term to long term at one year, and losses that offset gains.

What counts as a taxable event for XRP?

Any transaction that disposes of your XRP or puts new value in your hands is taxable; holding and self-transfers are not. Here is how the common XRP actions are treated.

| Action | Taxable? | Treatment |

|---|---|---|

| Buy XRP with USD | No | Sets your cost basis. |

| Hold XRP | No | No tax while holding, even through big rallies. |

| Sell XRP for USD | Yes | Capital gain or loss (proceeds minus basis). |

| Swap XRP for another crypto | Yes | Disposal of XRP; capital gain or loss. |

| Spend XRP on goods or services | Yes | Treated as selling XRP; capital gain or loss. |

| Trade tokens on the XRPL DEX or AMM | Yes | Each swap is a disposal at fair market value. |

| Buy an XRPL NFT with XRP | Yes | Disposal of the XRP spent; gain or loss on it. |

| Exchange "staking" or earn payouts | Yes | Ordinary income at value when received. |

| Get paid in XRP | Yes | Ordinary income at value when received. |

| Airdrops (Spark/FLR, Songbird/SGB) | Yes | Ordinary income at value on receipt. |

| Set a trust line on the XRPL | No | Authorization only; nothing moves. |

| Move XRP between your wallets | No | Not taxable; basis and holding period carry. |

The swap row deserves emphasis. Trading XRP for Bitcoin, Ethereum, or a stablecoin feels like a sideways move, but the IRS sees a completed sale of your XRP at that moment's price. Crypto-to-crypto trades are the single most missed category on self-prepared returns, and rotating XRP into a stablecoin to sit out volatility realizes every dollar of gain just as surely as cashing out to your bank.

Spending works the same way. Pay for something with XRP that you bought at $0.50 when the price is $2, and you have a capital gain on the difference, plus whatever you bought. XRP settles in seconds and costs a fraction of a cent to send, which makes it genuinely useful for payments and simultaneously means heavy spenders generate a long list of small disposals to report.

XRP capital gains tax rates for 2026

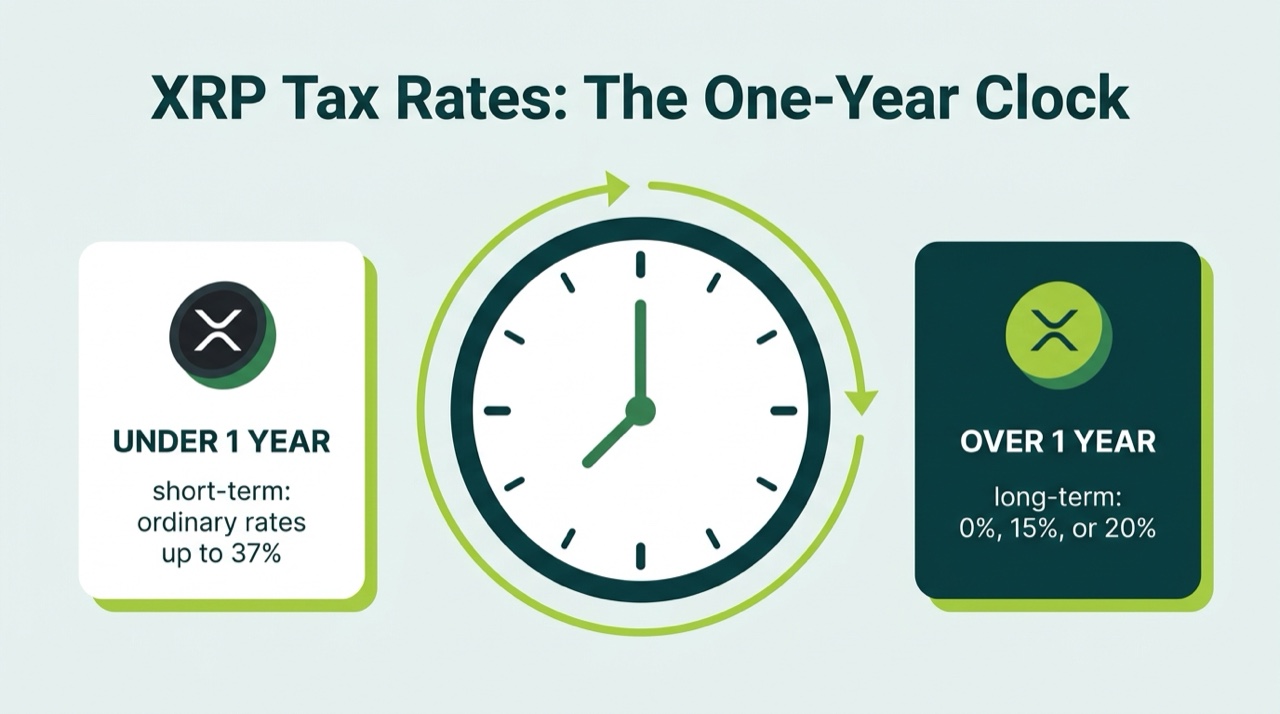

There is no special XRP tax rate; your rate depends on how long you held before selling and on your total income. Like all property, XRP follows the standard capital gains schedule.

- Short-term gains (held one year or less) are taxed at your ordinary federal rate, 10% to 37%.

- Long-term gains (held more than a year) are taxed at 0%, 15%, or 20%. Most filers land at 15%.

- High earners may owe an extra 3.8% Net Investment Income Tax once modified adjusted gross income passes $200,000 single or $250,000 married filing jointly. A single large XRP sale can push you over that line on its own.

- State tax can apply on top; most states tax crypto gains as ordinary income, and a move from a high-tax state matters more than most planning tricks.

| 2026 long-term rate | Single / MFS | Married Filing Jointly | Head of Household |

|---|---|---|---|

| 0% | Up to $49,450 | Up to $98,900 | Up to $66,200 |

| 15% | $49,451–$545,500 | $98,901–$613,700 | $66,201–$579,600 |

| 20% | Above $545,500 | Above $613,700 | Above $579,600 |

For long-time XRP holders this is mostly good news. If you bought years ago and held, your gains are long-term, which caps the federal rate at 20% and lands most people at 15%. The worked example below shows what that looks like in dollars.

The same $19,000 gain realized short term in the 32% bracket would cost about $6,080. Holding period is usually the single biggest lever on an XRP tax bill, and for a position built years ago the lever is already pulled. The remaining questions are which lots to sell, in which year, and from which wallet, all of which you control. We cover the mechanics of exiting a large position, including bracket management and multi-year sales, in our guide to selling XRP and what you will owe.

Is XRP tax free? The Ripple lawsuit and the Trump exemption myths

No, XRP is not tax free, and it never has been. Search interest around XRP taxes is saturated with two hopeful myths, one born from a courtroom and one from social media, so let us settle both with specifics.

Myth 1: The Ripple ruling made XRP tax free

The SEC sued Ripple, the company, in December 2020 over whether its sales of XRP were unregistered securities offerings. The 2023 ruling found that programmatic sales on exchanges were not securities transactions while institutional sales were, Ripple was ordered to pay a $125 million penalty in 2024, and the case fully ended in 2025 when both sides dropped their appeals. None of that has anything to do with your tax bill. Securities law decides how an asset can be sold and marketed. Tax law decides how gains are taxed, and the IRS taxes XRP as property regardless of whether regulators call it a security, a commodity, or anything else. Stocks are securities and fully taxable. Commodities are not securities and fully taxable. There was never a version of the Ripple outcome that could have made XRP gains tax free, because the question was never on the table.

The lawsuit does matter for your taxes in one indirect, practical way: many US exchanges suspended or delisted XRP trading in early 2021 and only relisted it after the 2023 ruling. Holders scrambled coins off delisting platforms into wallets and offshore venues, sometimes in a single panicked weekend. If that was you, your transaction records may be scattered across accounts that no longer exist, which is a cost basis problem, not a legal one. We cover how to fix it below.

One more distinction the myth blurs: the case was between the SEC and Ripple the company. You, the XRP holder, were never a party to it. Nothing a court decided about Ripple's conduct in 2020 changes what you owe on a coin you sell in 2026.

Myth 2: A Trump policy exempted XRP from capital gains tax

No such policy exists. Rumors of a zero capital gains tax on US-based cryptocurrencies, with XRP always named in the list, have circulated on social media since 2024. They resurface every time crypto policy makes headlines, and they are wrong every time. Capital gains rates are set by Congress in the tax code. A president cannot exempt an asset from capital gains tax by announcement, and as of the 2026 tax year no bill doing so has been enacted. There is no crypto exemption, no XRP carve-out, and no de minimis rule that lets small XRP gains go unreported.

The practical danger of this myth is not embarrassment, it is under-reporting. Brokers now send the IRS a copy of your XRP sale proceeds on Form 1099-DA. A filer who skips reporting because a post said XRP was tax free will get a matching notice with penalties and interest attached. If a genuine exemption ever arrives, it will come as legislation with an effective date, and every crypto tax professional in the country will be talking about it. Until then, plan on paying capital gains tax on every profitable XRP disposal.

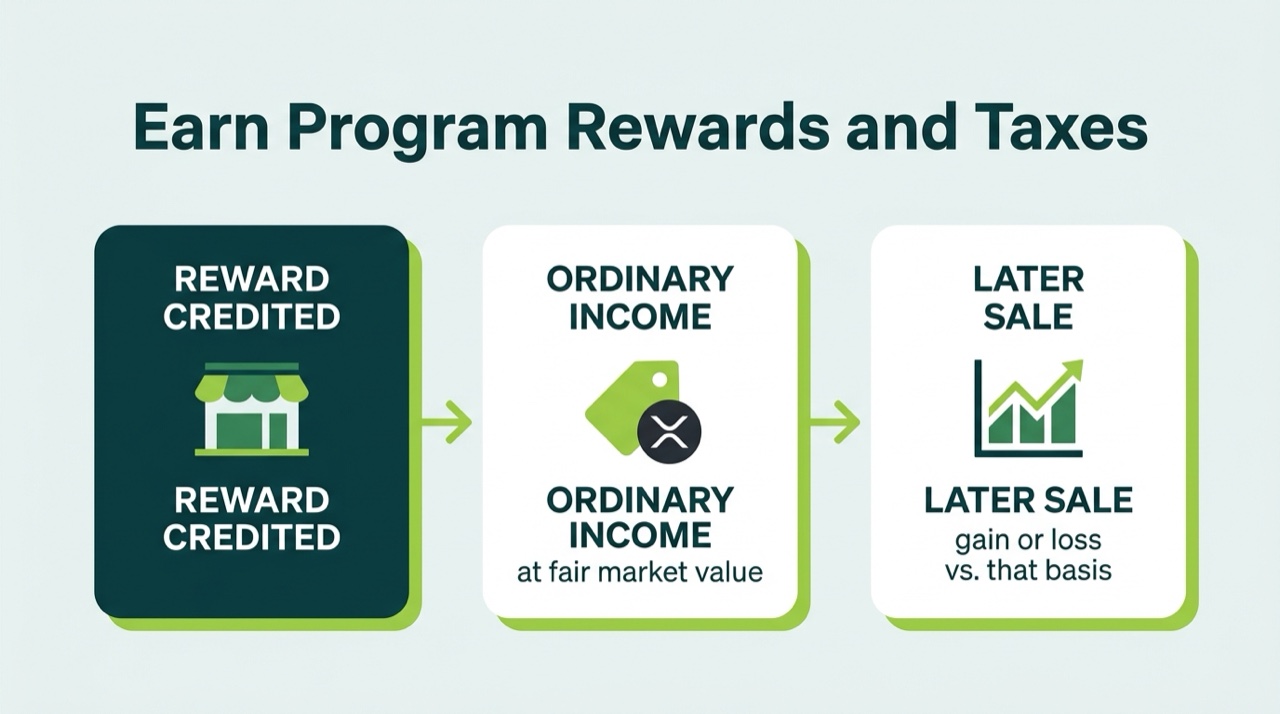

XRP income: earn programs, payments, and getting paid in XRP

XRP you earn, rather than buy, is ordinary income at its fair market value on the day you receive it. This covers exchange reward programs, salary or invoices paid in XRP, and referral or promotional payouts. Income treatment matters because the rate is your ordinary bracket, up to 37%, not the friendlier capital gains schedule, and because each receipt starts its own cost basis clock.

XRP has no native staking, and that changes the tax answer

The XRP Ledger does not use proof of stake. It reaches consensus through a network of validators that are not paid in new XRP, so there is no protocol-level staking, no validator rewards, and no delegation. This is not a gap in XRP; it is the design. But it means every product marketed as "XRP staking" is actually something else, usually a lending or rewards program where a platform pays you for parking your XRP with it.

The tax treatment of those programs is more straightforward than real staking, not less. Genuine staking rewards raise timing questions that courts and the IRS have wrestled with. Exchange earn payouts do not: they are ordinary income at fair market value when they hit your account, reported on Schedule 1. Each payout also becomes its own basis lot, so when you later sell the reward XRP, you measure capital gain or loss from that value, not from zero.

The label matters for risk, too. Lending programs put your XRP on the platform's balance sheet, and holders of similar programs learned during the 2022 bankruptcies what that means when a platform fails. Frozen or lost earn balances raise loss-deduction questions that are messier than the income side. We break down every flavor of these products, platform by platform, in our guide to XRP staking and lending taxes.

Getting paid in XRP

XRP settles in three to five seconds for a fraction of a cent, which makes it one of the few large-cap assets people actually use for payments. If you receive XRP for work or sales, it is ordinary income at the dollar value on receipt, plus self-employment tax if you are in business. Spending or selling that XRP later is a second, separate taxable event: a capital gain or loss measured from the value you already reported as income. Freelancers who invoice in XRP should record the dollar value on every payment date, because reconstructing dozens of receipt-day prices in April is exactly the kind of work that turns a simple return into a project.

Flare, Songbird, and Spark: how XRP airdrops are taxed

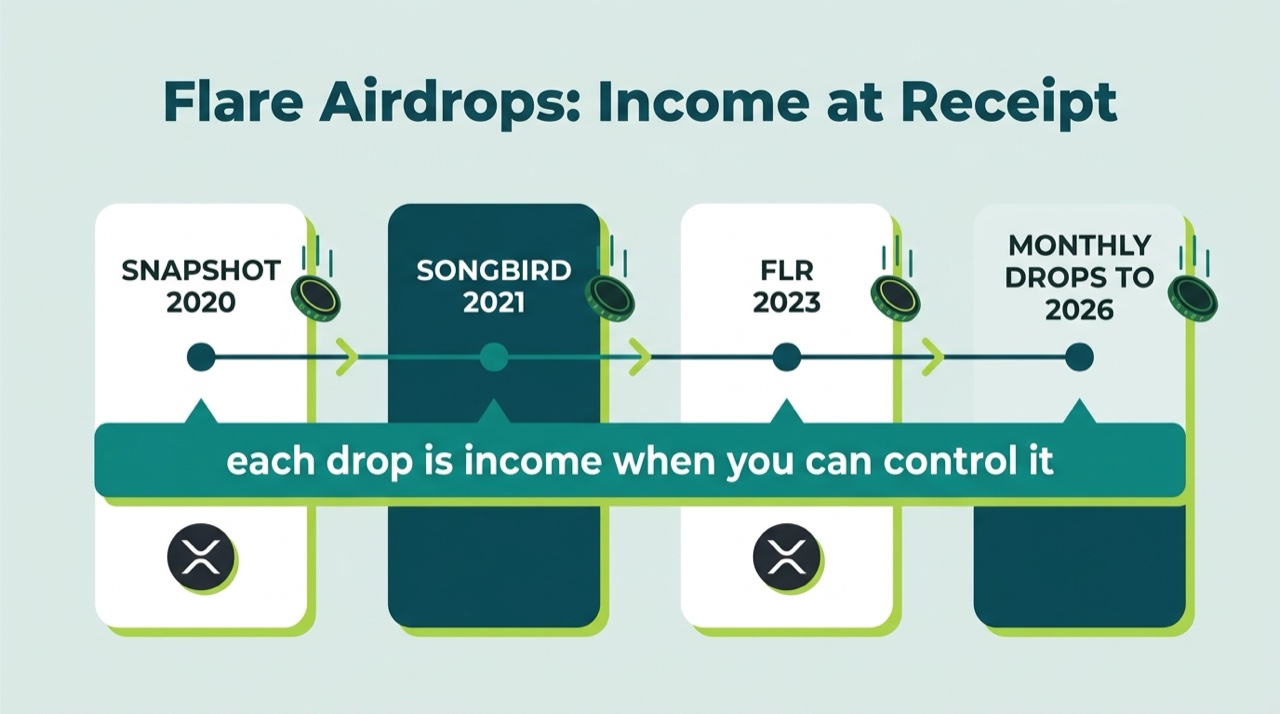

Airdropped tokens are ordinary income at fair market value on the day you gain dominion and control, meaning the day the tokens actually become yours to sell. That rule, from Revenue Ruling 2019-24, hits XRP holders harder than almost any other community, because XRP holders have lived through the most drawn-out airdrop in crypto history.

The timeline matters, so here it is. In December 2020, Flare Networks snapshotted XRP balances for the Spark (FLR) distribution. Nothing arrived for two years. Songbird (SGB), Flare's canary network token, went out to participants in late 2021. The first 15% of FLR finally landed in January 2023, and the remaining 85% was restructured into 36 monthly FlareDrop distributions that ran into 2026 and went to holders of wrapped FLR, not to XRP wallets.

Each of those events is taxed on its own date, not on the snapshot date:

- The December 2020 snapshot was not taxable. Being included in a future distribution is not income. You had no tokens and no control.

- SGB was income when it arrived in your wallet or exchange account in 2021, at its market value that day.

- The January 2023 FLR distribution was income at that day's price. If your exchange held the FLR and only credited it later, your income date is when you could actually sell or withdraw, which varied by platform.

- Each monthly FlareDrop was its own income event at the value on receipt, which means an active claimer has dozens of small income entries to report.

- Selling any of these tokens is a separate capital gain or loss, measured from the value you reported as income. FLR traded well below its early prices for long stretches, so many holders have harvestable losses sitting next to the income they owe.

If you claimed FLR or SGB and never reported it, clean it up before the IRS asks. And note the pattern for the future: the XRPL ecosystem keeps producing snapshot-based distributions, and every one follows the same two-step tax shape, income on receipt, gains or losses on sale. We walk through the full Flare timeline, exchange-by-exchange income dates, and the wrapped-FLR wrinkle in our guide to Flare airdrop taxes for XRP holders.

XRPL DEX, AMM, trust lines, and NFT taxes

Activity on the XRP Ledger is taxed exactly like activity on any other chain: every swap is a disposal, every earn event is income, and no broker files a form for any of it. The XRPL has had a built-in order-book exchange since 2012, added an automated market maker (the XLS-30 amendment) in 2024, and supports native NFTs (XLS-20) since 2022. Self-custody users get the full tax treatment with none of the paperwork, so the tracking burden is entirely yours.

- DEX swaps are taxable. Trading XRP for an issued token (a stablecoin, an ecosystem token, a wrapped asset) through the ledger's order books is a disposal of your XRP at fair market value, exactly like a trade on Coinbase. The reverse trade disposes of the token.

- AMM swaps are taxable the same way. Whether your trade routes through an order book, an AMM pool, or both, the tax result is identical: you disposed of one asset and acquired another.

- AMM liquidity deposits are likely disposals. When you deposit XRP and a token into an XRPL AMM pool, you receive LP tokens representing your share. The conservative reading treats that exchange as a disposal of both deposited assets, and the withdrawal as a disposal of the LP tokens. The IRS has not ruled on AMM deposits specifically, so document your method and apply it consistently.

- AMM earnings are not free money. Your pool share grows from trading fees, and single-sided or unbalanced withdrawals can leave you with different assets than you deposited. Those differences surface as gains, losses, or income when you exit.

- Trust lines are not taxable to open. Setting a trust line just authorizes your account to hold a token. Tax happens when tokens move, not when the line is created.

- Reserves are locked, not spent. The ledger requires a small XRP reserve per account and per object. Reserved XRP is still yours, so locking it is not a disposal. Nothing to report.

- Transaction fees are burned. Every XRPL transaction destroys a tiny amount of XRP. Strictly, each burn is a micro-disposal with a basis; in practice the amounts are fractions of a cent and good software nets them into your totals. The volume, not the value, is what makes hand-tracking impossible.

- XLS-20 NFTs follow NFT rules. Buying an XRPL NFT with XRP disposes of the XRP spent, so you can owe gain on the purchase itself. Selling the NFT is a disposal of the NFT. Creator royalties, which the XRPL enforces at the protocol level, are ordinary income to the creator on each resale. And if an NFT counts as a collectible, long-term gains on it can be taxed at up to 28% instead of the usual 20% cap.

- Ripple's escrow is irrelevant to you. The escrowed XRP that Ripple releases on a schedule, and the institutional On-Demand Liquidity flows built on XRP, affect market supply, not your return. Retail holders have nothing to report from any of it.

The common thread: XRPL activity is cheap and fast, which encourages exactly the kind of high-frequency, small-value transacting that produces enormous transaction lists. A hundred DEX trades at $0.0002 in fees cost you two cents to execute and hours to reconcile by hand. Start with a crypto tax software import of your XRPL address, then fix what the software gets wrong. For the full treatment of pools, LP tokens, and NFT edge cases, see our guide to XRP Ledger DeFi taxes.

Years of XRP history across dead exchanges and wallets?

Delistings, defunct platforms, airdrops, and self-custody moves are exactly where XRP cost basis falls apart. We reconcile your full history into defensible, CPA-ready numbers.

Spot XRP ETF taxes: shares vs holding XRP directly

Spot XRP ETF shares are taxed as capital assets, and because most of the US spot XRP ETFs that launched in late 2025 are structured as grantor trusts, shareholders are treated for tax purposes as owning a proportional slice of the trust's underlying XRP. That structure, the same one used by the spot Bitcoin and Ether funds, produces a few effects worth knowing before you decide which wrapper to hold.

- Selling shares at a profit is a capital gain, short term or long term by your holding period, at the same rates as selling XRP itself. The ETF is not a tax shelter in a taxable account.

- The sponsor fee creates tiny disposals you did not order. Grantor trusts sell small amounts of XRP to pay the management fee, and each shareholder recognizes a proportional micro-gain or micro-loss on those sales. The trust publishes a tax reporting statement each year with the math; expect a long list of small entries, not a single number.

- Your broker does the bookkeeping. ETF sales land on a standard 1099-B with cost basis included. No wallets, no lost records, no per-wallet allocation, no zero-basis surprises.

- Wash sale treatment differs, and it cuts in XRP's favor. Direct XRP is property, so the wash sale rule does not currently apply: sell at a loss, claim it, rebuy immediately. ETF shares are securities, where the rule clearly does apply. Loss harvesting is more flexible with coins than with shares.

- In retirement accounts, the ETF wins by default. Holding a spot XRP ETF inside an IRA or 401(k) defers or eliminates tax on the gains entirely, something you cannot easily replicate with self-custodied XRP.

Neither route is tax free. Both produce capital gains when sold at a profit in a taxable account. The real difference is who does the bookkeeping, which rules apply at the edges, and whether you value self-custody and XRPL utility enough to carry the reporting burden yourself. Switching between them is itself a taxable event: selling XRP to buy the ETF realizes your gain, and there is no like-kind path between the two. We compare the wrappers line by line, including the fee-sale statements and IRA mechanics, in our guide to XRP ETF taxes.

How XRP is reported: 1099-DA, Form 8949, and per-wallet basis

XRP disposals are reported on Form 8949 and Schedule D, XRP income lands on Schedule 1 or Schedule C, and since tax year 2025 US brokers file Form 1099-DA reporting your gross sale proceeds to both you and the IRS. Cost basis reporting on the form expands for 2026. If you sold XRP on Coinbase, Uphold, Kraken, or another US platform, the IRS already has a copy of your proceeds, and matching what you file to what they see is no longer optional.

Here is the filing flow for a typical XRP holder:

- Collect every 1099-DA from each exchange where you sold XRP. Check the proceeds figures against your own records; broker forms are new and errors happen in both directions.

- Fix the basis. If you transferred XRP into an exchange before selling, the broker may report zero or missing basis, because it has no idea what you paid years ago somewhere else. Supply your true acquisition cost from your records so you are not taxed on the full sale price.

- List each disposal on Form 8949: date acquired, date sold, proceeds, cost basis, and gain or loss, split short-term and long-term.

- Total everything on Schedule D, where gains and losses net against each other.

- Report XRP income on Schedule 1 (or Schedule C for a business): earn program payouts, airdrops like FLR and SGB, and payments received in XRP.

- Answer "Yes" to the digital asset question on Form 1040 if you sold, swapped, or received XRP during the year. Answering it falsely is the cheapest mistake to avoid on the whole return.

Self-custody and XRPL activity never appear on any broker form. Your DEX trades, AMM exits, and wallet-to-wallet sales are reportable on the same Form 8949 with no 1099 behind them. The IRS treats unreported self-custody activity the same as unreported exchange activity; the only difference is which database catches it first.

Lost cost basis from 2017 or 2018? How to rebuild it

Rebuild your basis before you sell, because the alternative is paying capital gains tax on your entire sale price. This is the defining XRP tax problem. A large share of XRP holders bought during the 2017 to 2018 run on platforms that no longer exist, then shuffled coins through wallets like Toast Wallet (long discontinued) and through the 2021 delisting scramble. Now they are selling at prices that dwarf their cost, and they cannot prove what they paid.

- Inventory every venue you ever touched. Old emails are the map: signup confirmations, deposit receipts, and trade confirmations from exchanges, plus wallet backup reminders. Search your inbox for "XRP" and the names of platforms you half-remember.

- Export what still exists. Active exchanges hold years of history. Download full CSV transaction exports, not just recent statements, from every account that still opens, including accounts you emptied during the delistings.

- Pull your on-chain history. The XRP Ledger is public and complete back to 2013. A ledger explorer can list every transaction your address ever made, with dates and amounts. This anchors when coins arrived and moved, even when the exchange side is gone.

- Match deposits to bank records. Card and ACH records from 2017 and 2018 establish what you actually spent, which supports a defensible acquisition cost even without the exchange's records.

- Price the gaps with documented historical data. For acquisition dates you can establish, apply a documented historical XRP price from a reputable source and keep the printout. A reasonable, documented method beats both guessing and zero basis.

- Handle truly lost coins separately. XRP stranded in a dead wallet or a collapsed platform raises a different question, a loss deduction, with its own rules. See our guide to lost and stolen crypto deductions before writing anything off.

- Get help if the pile is deep. Reconstructing basis across defunct platforms is exactly the work a crypto tax professional does routinely, and it usually pays for itself in avoided overreporting.

How to reduce your XRP taxes legally

The biggest legal levers are holding past one year, harvesting losses, and choosing which lots you sell; none of them require anything exotic.

- Hold past one year. Long-term rates of 0%, 15%, or 20% beat ordinary rates of up to 37%. For appreciated XRP, patience is the cheapest tax strategy available, and most 2017-era holders already qualify on every lot.

- Harvest losses. Sell underwater lots to realize capital losses that offset gains, plus up to $3,000 of ordinary income per year, with the rest carried forward. Under current law the wash sale rule does not apply to XRP, so you can rebuy immediately, though proposed legislation could change that. Airdrop tokens trading below their income-date value are a common, overlooked source of harvestable losses for XRP holders.

- Mind your bracket. Realizing long-term gains in a lower-income year can land some or all of the gain in the 0% or 15% band. Spreading a large sale across two tax years can keep you out of the 20% tier and under the 3.8% surtax threshold.

- Use specific identification. Choosing which XRP lots you sell, documented properly and per wallet, lets you sell high-basis lots first and defer the big 2017 gains until you choose to realize them.

- Donate appreciated XRP. Gifting long-held XRP to a qualified charity avoids the capital gain entirely while supporting a deduction at fair market value.

- Use retirement accounts for new exposure. You cannot move existing XRP into an IRA without selling it, but new XRP exposure can live inside one through a spot ETF, where gains compound untaxed.

Want a professional to handle it?

Book a free 15-minute call and we will map out exactly what your XRP tax situation needs, from dead-exchange records to airdrop income to rebuilt cost basis.

Book a free 15-min callXRP tax FAQ

Do I have to pay taxes on XRP?

Is XRP tax free after the Ripple lawsuit?

Did Trump make XRP exempt from capital gains tax?

Will I be taxed on $1,000 of XRP profit?

Do I need to report XRP gains under $3,000?

Is swapping XRP for another cryptocurrency taxable?

Are XRP staking rewards taxable?

Are Flare (FLR) airdrops taxable for XRP holders?

How are spot XRP ETFs taxed?

Will I get a 1099-DA for my XRP?

Does the wash sale rule apply to XRP?

I bought XRP in 2017 and lost my records. What do I do?

The 2025/26 Crypto Tax Guide. Built by former Big 4 accountants.

A printable, step-by-step guide and checklist to reconcile every coin and wallet, recover missing cost basis, and file accurately before the deadline.

- Form 8949, Schedule D, and Schedule 1 walkthroughs

- How to handle staking, DeFi, NFTs, and lost coins

- The $0-basis 1099-DA trap (and how to avoid it)

- FBAR, Form 8938, and foreign exchange reporting