Key takeaways

- Holding BTC is free; disposing of it is taxable. Selling, trading, or spending Bitcoin triggers capital gains. Buying and holding does not, no matter how much it appreciates.

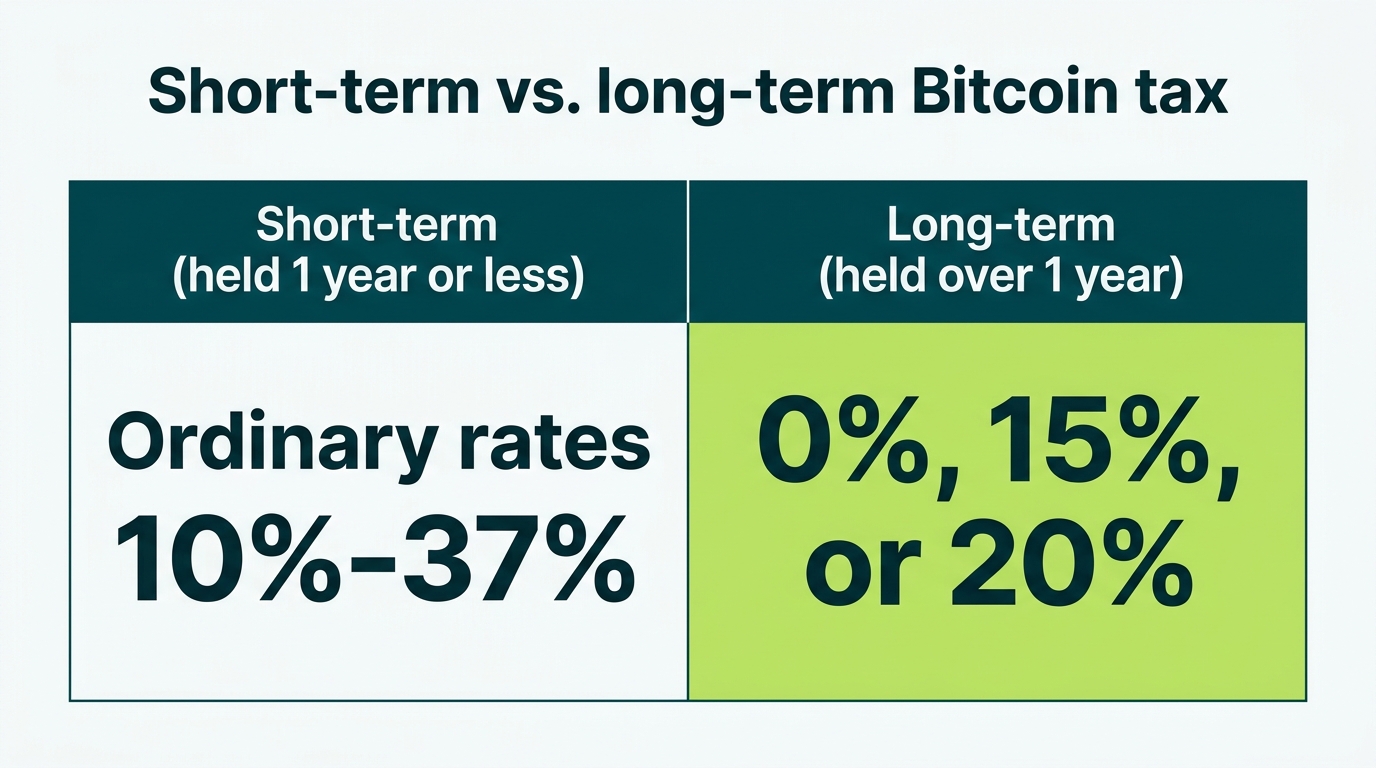

- Holding period sets the rate. Over a year gets long-term rates (0%, 15%, or 20%); a year or less is taxed at your ordinary rate of up to 37%.

- The IRS now gets a copy. Form 1099-DA reporting is live: US exchanges report your Bitcoin sale proceeds directly to the IRS, and cost basis reporting expands for 2026.

- ETF Bitcoin and wallet Bitcoin are taxed differently at the edges. Spot ETF shares are securities with broker-tracked basis and wash sale exposure. Self-custodied BTC is property you track yourself, wallet by wallet.

Bitcoin is usually the first coin people buy and the last one they think about at tax time. That combination causes real problems. Fifteen years of price history means holders are sitting on some of the largest unrealized gains of any asset, often spread across old exchanges, hardware wallets, and accounts they barely remember. Meanwhile the reporting rules changed more in the last two years than in the previous ten: brokers now send your sale proceeds straight to the IRS, and cost basis must be tracked wallet by wallet. This guide walks through exactly when Bitcoin is taxed, the 2026 rates, how ETFs and mining fit in, and how to report everything cleanly.

Do you have to pay taxes on Bitcoin?

Yes, in two different ways. The IRS classified Bitcoin as property back in 2014 under Notice 2014-21, and that single decision drives everything else. Property has well-settled tax treatment: the same framework that covers stocks and real estate covers BTC.

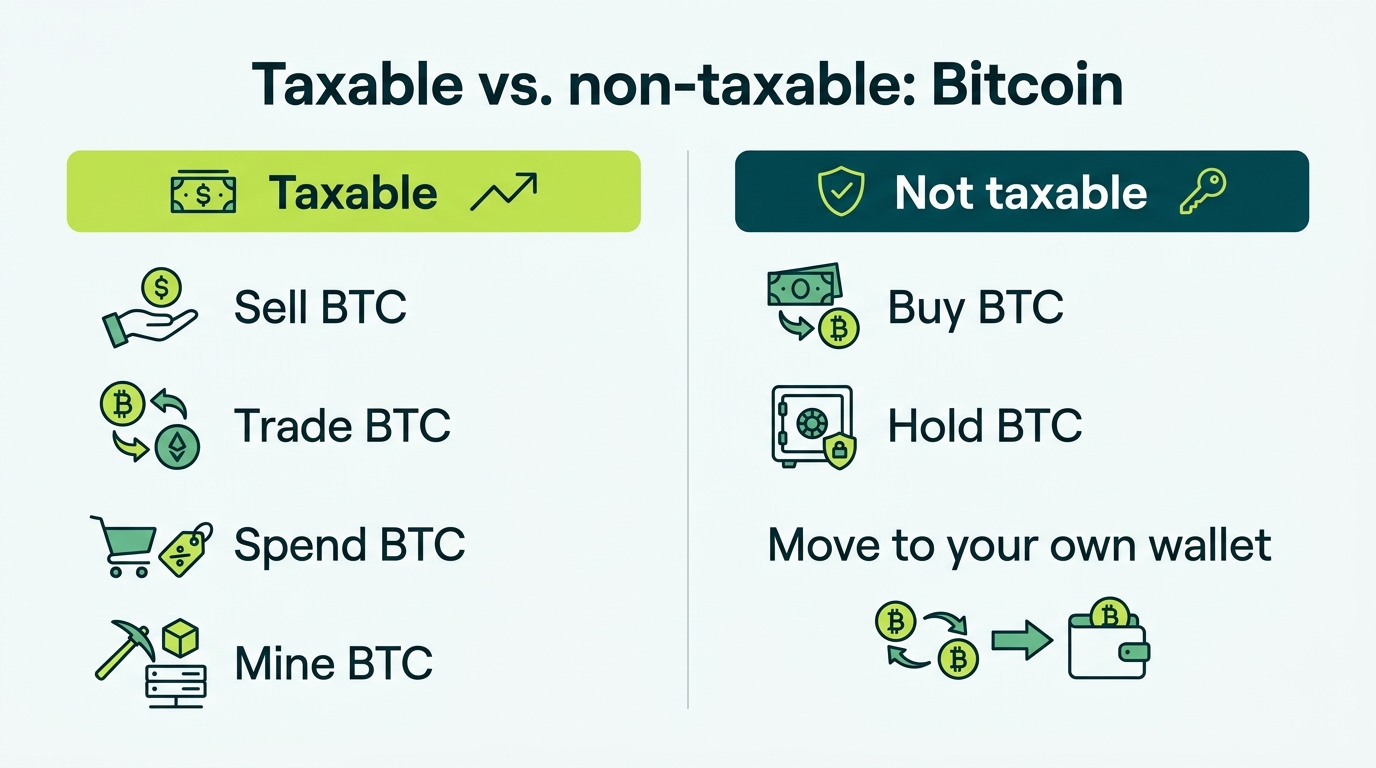

- Capital gains apply when you dispose of Bitcoin: selling it for dollars, trading it for another coin, or spending it on anything. Your gain or loss equals what you received minus your cost basis.

- Ordinary income applies when you earn Bitcoin: mining rewards, interest-style payouts, and getting paid in BTC are all taxed at fair market value on the day you receive them.

What is never taxable matters just as much. Buying Bitcoin with dollars is not taxable; it just sets your cost basis. Holding is not taxable through any amount of appreciation, because the US does not tax unrealized gains. And moving BTC between wallets you own, from Coinbase to a hardware wallet for example, is not a disposal. The basis and holding period travel with the coins.

What counts as a taxable event for Bitcoin?

Here is how the common Bitcoin actions are treated for the 2026 tax year.

| Action | Taxable? | Treatment |

|---|---|---|

| Buy BTC with USD | No | Not taxable. Sets your cost basis. |

| Hold BTC | No | No tax while holding, even through big rallies. |

| Sell BTC for USD | Yes | Capital gain or loss (proceeds − basis). |

| Trade BTC for another crypto | Yes | Disposal of BTC; capital gain or loss. |

| Spend BTC on goods or services | Yes | Treated as selling BTC; capital gain or loss. |

| Sell spot Bitcoin ETF shares | Yes | Capital gain or loss; broker reports on 1099-B. |

| Mine BTC | Yes | Ordinary income at fair market value when received. |

| Get paid in BTC | Yes | Ordinary income at fair market value when received. |

| Move BTC between your own wallets | No | Not taxable; basis and holding period carry. |

| Gift BTC (within limits) | No* | Generally not taxable to give; large gifts may need a gift tax return. |

| Donate BTC to charity | No | No capital gain; possible fair market value deduction. |

The trade row catches more people than any other. Swapping BTC for Ethereum or a stablecoin feels like a sideways move, but the IRS sees a completed sale of your Bitcoin at that moment's price. No dollars need to touch your bank account for a taxable gain to exist.

Spending Bitcoin is a sale

This is the rule that surprises people most. When you pay for something with Bitcoin, the IRS treats it as if you sold the BTC for its dollar value and then spent the dollars. Buy 0.1 BTC at $4,000, spend it on a laptop when it is worth $6,000, and you have a $2,000 capital gain along with your new laptop. The same logic applies to Lightning payments and small purchases: there is no de minimis exemption, so every coffee bought with appreciated BTC is technically a reportable disposal. Congress has floated small-transaction exemptions for years, but as of the 2026 tax year none has passed. If you actually spend Bitcoin regularly, good tracking software is not optional, and our crypto tax software guide compares the tools that handle spending well.

Bitcoin tax rates for 2026

There is no special "Bitcoin tax rate." Like all property, the rate depends on how long you held before selling and your total taxable income. One date does most of the work: the one-year mark.

- Short-term gains (held one year or less) are taxed at your ordinary federal rate, 10% to 37%.

- Long-term gains (held more than a year) are taxed at 0%, 15%, or 20%. Most filers land at 15%.

- Mined or earned BTC is ordinary income at receipt, regardless of how long you later hold it.

- High earners may owe an extra 3.8% Net Investment Income Tax once modified income passes $200,000 single or $250,000 married filing jointly.

- State tax can apply on top; most states tax crypto gains as ordinary income, while a handful (Texas, Florida, Wyoming, and others) have no state income tax at all.

Here are the 2026 federal long-term capital gains brackets that apply to Bitcoin held more than one year:

| 2026 long-term rate | Single / MFS | Married Filing Jointly | Head of Household |

|---|---|---|---|

| 0% | Up to $49,450 | Up to $98,900 | Up to $66,200 |

| 15% | $49,451–$545,500 | $98,901–$613,700 | $66,201–$579,600 |

| 20% | Above $545,500 | Above $613,700 | Above $579,600 |

Short-term gains stack on top of your other income and get taxed at whatever ordinary bracket they land in. The 2025 tax law changes (the One Big Beautiful Bill Act) made the current bracket structure permanent, so the 10% through 37% ladder is the stable planning baseline rather than something scheduled to expire.

Notice the 0% band. A married couple with total taxable income under $98,900 in 2026, including the gain itself, pays zero federal tax on long-term Bitcoin gains. Retirees and lower-income years are genuine opportunities to realize gains for free.

The same $40,000 gain realized inside a year by someone in the 32% bracket costs about $12,800. Holding past the one-year mark saved $6,800 here, before state tax even enters the picture.

Bitcoin ETF taxes: how IBIT, FBTC, and GBTC are taxed

Since spot Bitcoin ETFs began trading in January 2024, a huge share of Bitcoin exposure now lives in ordinary brokerage accounts. The tax treatment is close to holding BTC directly, but the differences matter, and one of them surprises almost everyone.

- ETFs are grantor trusts. Funds like IBIT, FBTC, and GBTC hold nothing but Bitcoin, and the tax code looks through the wrapper. You are treated as owning your fractional share of the trust's BTC directly.

- Selling shares is a capital gain or loss at the same short-term and long-term rates as Bitcoin itself. There is no collectibles rate and no special ETF rate. Your broker tracks basis and reports sales on a standard 1099-B.

- The sponsor fee creates tiny taxable sales you did not make. Each month the trust sells a sliver of its Bitcoin to pay the management fee. As a grantor trust owner, a proportional piece of each sale passes through to you. The fund publishes a year-end grantor trust tax statement with the figures, and your basis shrinks slightly as it happens. The amounts are small, but they are reportable, and most DIY filers miss them entirely.

- The wash sale rule applies to ETF shares. ETF shares are securities. Sell them at a loss and rebuy within 30 days, and the loss is disallowed. Self-custodied Bitcoin is property, where the rule currently does not reach. That asymmetry makes direct BTC more flexible for loss harvesting under current law.

- In retirement accounts, ETFs win by default. A Bitcoin ETF inside an IRA or 401(k) grows tax-deferred or tax-free, something you cannot easily replicate with a hardware wallet.

Neither route is tax free. Both produce capital gains when sold at a profit in a taxable account. The real difference is who does the bookkeeping (your broker versus you) and which edge rules apply.

Grantor trust mechanics, the phantom expense sales, and how spot ETFs compare with direct BTC in taxable accounts and IRAs all get full treatment in our dedicated guide to Bitcoin ETF taxes.

Bitcoin mining taxes and earned BTC

Mining is the one part of Bitcoin taxation where income tax, not capital gains, does the heavy lifting. Mined Bitcoin is taxed in two layers, and the order matters.

- Income at receipt. The moment mined BTC hits your wallet, its fair market value that day is ordinary income. A block reward or pool payout worth $600 on arrival is $600 of income even if Bitcoin crashes the next week.

- Capital gain or loss at sale. That same value becomes your cost basis. Sell the mined BTC later for more and the difference is a capital gain; sell for less and it is a loss.

How you report the income depends on scale:

- Hobby mining goes on Schedule 1 as other income. No self-employment tax, but deductions are extremely limited.

- Business mining goes on Schedule C. You can deduct electricity, hardware, hosting, and repairs, and 100% bonus depreciation (restored permanently by the 2025 tax law) lets you write off mining rigs in the year they go into service. The trade-off is 15.3% self-employment tax on net profit, and quarterly estimated payments once the numbers are real.

Getting paid in Bitcoin for work follows the same two-step logic: ordinary income at the value received (plus self-employment tax if you are a contractor), then a separate capital gain or loss when you eventually sell or spend those coins. Interest-style rewards from exchanges and Lightning routing fees land the same way: income first, basis established, gains later.

Years of Bitcoin buys, sells, and transfers?

Cost basis across wallets and years is where BTC returns go wrong. We reconcile your full history into clean, CPA-ready figures.

Hobby versus business classification, Schedule C, equipment depreciation, and quarterly estimates are covered in depth in our full guide to Bitcoin mining taxes.

Cost basis and the wallet-by-wallet rule

Your cost basis is what you paid for the Bitcoin, including fees. Get it wrong in one direction and you overpay tax; get it wrong in the other and you underreport to an agency that now has your sale proceeds on file. Two rules changed recently, and long-time Bitcoin holders are exactly the people they affect.

- Basis is now tracked per wallet. Since January 1, 2025, under Revenue Procedure 2024-28, cost basis must be tracked wallet by wallet and account by account. The old approach of pooling every satoshi you own into one universal average is no longer allowed. The IRS offered a one-time safe harbor to allocate existing basis across wallets as of that date; if you never did that allocation, do it before your next sale.

- FIFO is the default, specific identification is the opportunity. Within each wallet, first-in-first-out applies unless you specifically identify which lots you are selling, documented at or before the sale. For a holder with 2015 coins and 2024 coins in the same account, choosing the lot can be the difference between a small gain and an enormous one.

Transfers are the other trap. Moving BTC between your own wallets is not taxable, but the receiving exchange has no idea what you originally paid. When you later sell there, its records show coins that appeared from nowhere, which is how brokers end up reporting your basis as zero. Long-time holders with coins that have passed through Mt. Gox-era exchanges, old desktop wallets, and multiple hardware devices should rebuild their basis trail now, from old exchange exports, the public blockchain record, and bank statements, rather than during an audit.

Basis methods, the safe harbor allocation, and what to do when records are missing get a full walkthrough in our guide to selling Bitcoin taxes.

Form 1099-DA and how to report Bitcoin on your return

Reporting is where Bitcoin taxes changed the most. Starting with tax year 2025, US brokers must file Form 1099-DA, reporting your gross proceeds from Bitcoin sales to both you and the IRS. The first forms arrived in early 2026, and cost basis reporting on the form expands for 2026 sales of covered lots. If you sold BTC on Coinbase, Kraken, or any other US platform, the IRS already has a copy. Matching what you file to what they see is no longer optional. Our full Form 1099-DA guide covers the form line by line.

Here is the filing flow for a typical Bitcoin holder:

- Collect every 1099-DA from each exchange where you sold. Check the proceeds against your own records before anything else.

- Fix the basis. If you transferred BTC into an exchange before selling, the broker may report zero or missing basis. Supply your true acquisition cost so you are not taxed on the entire sale price.

- List each disposal on Form 8949: date acquired, date sold, proceeds, cost basis, and gain or loss, split into short-term and long-term.

- Total everything on Schedule D, where gains and losses net against each other.

- Report Bitcoin income on Schedule 1 (or Schedule C for a mining or freelance business): mining rewards, interest payouts, and payments received in BTC.

- Answer "Yes" to the digital asset question on Form 1040 if you sold, traded, spent, or received Bitcoin during the year.

Self-custody sales, peer-to-peer deals, and BTC spent from your own wallet never appear on a 1099-DA, but they are just as reportable. The form covers what brokers see, not what you owe.

The wash sale rule and Bitcoin tax-loss harvesting

Under current law, the wash sale rule does not apply to Bitcoin. The rule (IRC Section 1091) disallows a loss when you sell a security and rebuy it within 30 days, and the IRS treats BTC as property, not a security. That means you can sell Bitcoin at a loss, harvest the deduction, and buy it back immediately without waiting out a 30-day window. Harvested losses offset your capital gains dollar for dollar, then up to $3,000 of ordinary income per year, with the remainder carried forward indefinitely.

Three caveats keep this honest. First, the rule does apply to spot Bitcoin ETF shares, so harvesting inside a brokerage account plays by stock rules. Second, Congress has repeatedly proposed extending the wash sale rule to digital assets, so confirm the current-year law before relying on the gap. Third, the economic substance doctrine gives the IRS a tool against trades that exist purely on paper, so avoid round trips with no real market exposure. Our crypto wash sale guide covers the strategy and its limits in detail.

Lost, stolen, and bankrupt-exchange Bitcoin

Bitcoin has been around long enough to accumulate every kind of loss story, and the tax treatment varies more than people expect.

- Lost keys are not a deductible loss. Forgetting a seed phrase or sending BTC to a wrong address feels like a theft, but with no closed and completed transaction there is generally nothing to deduct. The coins are simply frozen, along with their basis.

- Stolen Bitcoin depends on why you held it. Personal theft losses have been nondeductible since 2018, and the 2025 tax law made that permanent. But the IRS confirmed in 2025 that theft losses from profit-motivated arrangements, like investment scams and fraudulent platforms, can still be deductible. The facts matter enormously here.

- Exchange bankruptcies resolve on their own clock. Mt. Gox, Celsius, and FTX creditors generally could not claim a loss while proceedings were open. Tax consequences land when distributions arrive or claims are finally settled, and distributions of appreciated coins create their own gain calculations.

This area is genuinely fact-specific, and the difference between deductible and nondeductible is often how the arrangement is documented. Our guide to lost and stolen crypto deductions goes deeper on each scenario.

How to reduce your Bitcoin taxes legally

- Hold past one year. Long-term rates of 0%, 15%, or 20% beat ordinary rates of up to 37%. For appreciated BTC, patience is the cheapest tax strategy available.

- Harvest losses in down markets. Sell underwater lots to realize losses that offset gains plus $3,000 of ordinary income, and under current law you can rebuy BTC immediately.

- Mind your bracket. Realizing long-term gains in a lower-income year can land some or all of the gain in the 0% or 15% band. Splitting a large sale across two tax years can keep you under the 20% tier and the 3.8% surtax threshold.

- Donate appreciated BTC. Giving long-held Bitcoin to a qualified charity avoids the capital gain entirely and can support a deduction at full fair market value.

- Gift strategically. Gifts within the annual exclusion ($19,000 per recipient in 2026) transfer BTC without tax, and the recipient takes your basis. A family member in the 0% long-term bracket can sell with no federal tax at all.

- Remember the step-up. Inherited Bitcoin gets a basis step-up to date-of-death value, which erases a lifetime of unrealized gains for heirs. It is a morbid strategy, but for early adopters it is often the largest number on the whiteboard.

- Use specific identification. Choosing which lots to sell, documented per wallet, lets you sell high-basis coins first and keep the 2013 lots undisturbed until you choose to realize them.

If your situation spans mining income, ETF positions, and a decade of wallets, a crypto tax professional will usually find more than these basics. The rest of our coin-by-coin tax guides cover how the same framework applies to Ethereum, Solana, and other assets you might hold alongside BTC.

Want a professional to handle it?

Book a free 15-minute call and we will map out exactly what your Bitcoin tax situation needs, from ETF statements to 2013 cold-storage lots.

Book a free 15-min callBitcoin tax FAQ

Do you have to pay taxes on Bitcoin?

How much tax do you pay on Bitcoin?

Do you pay taxes on Bitcoin if you don't sell?

Does the IRS know if you buy or sell Bitcoin?

Do I have to report small Bitcoin gains?

Is converting Bitcoin to another cryptocurrency taxable?

How are spot Bitcoin ETFs taxed?

Is Bitcoin mining taxed?

Does the wash sale rule apply to Bitcoin?

What happens if I don't report my Bitcoin?

How do I report Bitcoin on my taxes?

Is inherited or gifted Bitcoin taxable?

The 2025/26 Crypto Tax Guide. Built by former Big 4 accountants.

A printable, step-by-step guide and checklist to reconcile every coin and wallet, recover missing cost basis, and file accurately before the deadline.

- Form 8949, Schedule D, and Schedule 1 walkthroughs

- How to handle staking, DeFi, NFTs, and lost coins

- The $0-basis 1099-DA trap (and how to avoid it)

- FBAR, Form 8938, and foreign exchange reporting