How is selling Bitcoin taxed? Every sale, swap, or spend of Bitcoin is a disposal of property that produces a capital gain or loss: proceeds minus cost basis. Hold more than one year and the gain gets long-term rates of 0%, 15%, or 20%. Hold a year or less and it is taxed like wages, at rates up to 37%. High earners add 3.8% NIIT on top.

That is the short version. The long version is where the money actually moves. Which lots you sell determines whether a sale produces a $5,000 gain or a $50,000 gain. The wallet-by-wallet basis rules that took effect January 1, 2025 quietly rewired how every Bitcoin holder must track those lots. And Form 1099-DA now tells the IRS your gross proceeds whether or not you report them, while saying nothing about your basis, which puts the burden of proving what you paid squarely on you.

This guide covers selling Bitcoin taxes end to end for 2026: the exact rate brackets, cost basis methods and how to qualify for specific identification, the Rev. Proc. 2024-28 migration, 1099-DA mechanics, spending and gifting rules, tax loss harvesting while the wash sale window stays open, and what to do when a decade-old stack has no purchase records. It is one piece of our full Bitcoin tax guide, alongside our guides to Bitcoin mining taxes, Bitcoin ETF taxes, Ordinals and BRC-20 taxes, and wrapped Bitcoin and DeFi taxes.

Disclaimer: This guide is for informational purposes only and is not tax or legal advice. Cryptocurrency rules change quickly. Always consult a qualified CPA about your specific situation.

What Counts as Selling: More Than You Think

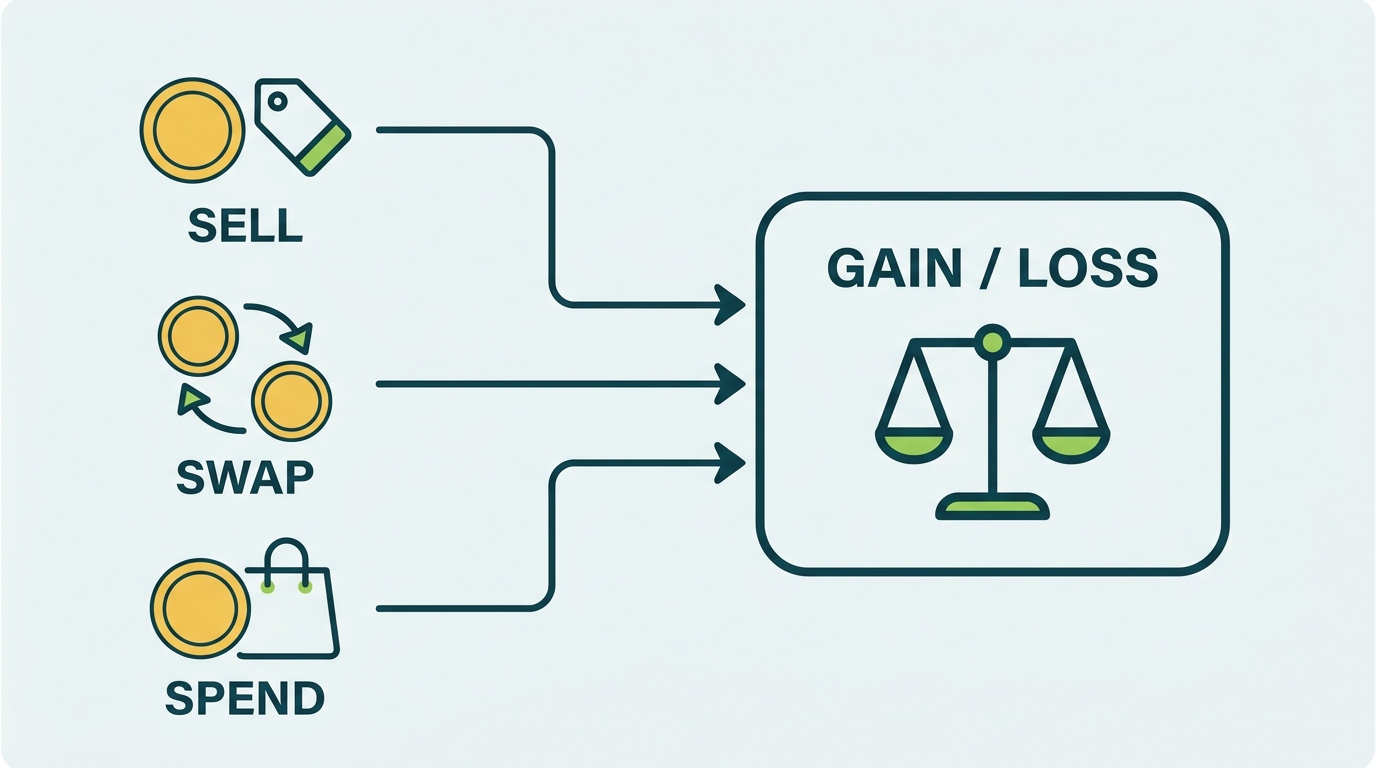

The tax law does not care whether you clicked a sell button. It cares whether you disposed of property. For Bitcoin, disposals include:

- Selling for dollars on an exchange or through an OTC desk.

- Swapping BTC for another crypto, including stablecoins. Trading BTC for USDC is a sale of BTC at that moment’s price.

- Spending BTC on goods or services, from a Tesla to a sandwich.

- Paying network fees in BTC when the fee comes out of your own coins.

- Using BTC in DeFi in ways that surrender ownership, covered in our wrapped Bitcoin and DeFi guide.

Just as important is what does not count. Moving Bitcoin between your own wallets is not a disposal. Neither is holding through any amount of price movement, buying more, or borrowing against your coins. Our taxable events guide maps the full boundary line.

Every disposal produces the same arithmetic: proceeds minus cost basis equals gain or loss. Proceeds are the fair market value of whatever you received. Basis is what you paid for the specific coins you gave up, including fees. Everything else in this guide is about getting those two numbers, and the rate applied to their difference, right.

The Rates: Short-Term, Long-Term, and the 2026 Brackets

Your holding period is the single biggest rate lever. The clock starts the day after acquisition and the line sits at exactly one year.

Short-term gains (held one year or less) are taxed as ordinary income at your marginal bracket, from 10% up to 37%. A high-earning trader flipping BTC after eleven months pays the same rate as on salary.

Long-term gains (held more than one year) get preferential rates. For 2026, the brackets are:

| Rate | Single (taxable income) | Married filing jointly |

|---|---|---|

| 0% | Up to $49,450 | Up to $98,900 |

| 15% | $49,451 to $545,500 | $98,901 to $613,700 |

| 20% | Over $545,500 | Over $613,700 |

Two mechanics trip people up. First, the brackets run on taxable income, meaning after the standard deduction, and your gains stack on top of ordinary income. A retiree with $30,000 of other income and a $40,000 long-term Bitcoin gain does not pay 0% on all of it; the gain fills the 0% bracket to its ceiling and the rest spills into 15%.

Second, the net investment income tax adds 3.8% for filers with modified adjusted gross income above $200,000 (single) or $250,000 (married filing jointly). A big sale can push you over the threshold by itself, which means the top practical federal rate on long-term Bitcoin gains is 23.8%, and short-term gains can reach 40.8% before state tax.

Eleven Months vs Thirteen Months

A single filer earning $150,000 sells Bitcoin for a $50,000 gain. Sold at eleven months, the gain is short-term, taxed at ordinary rates in the 24% bracket: roughly $12,000 of federal tax. Sold at thirteen months, it is long-term at 15%: $7,500. Two months of patience saved $4,500, before even considering NIIT and state tax. Check the calendar before you check the price.

The full bracket mechanics, including how gains interact with the standard deduction and state taxes, are in our crypto capital gains guide.

Cost Basis: The Number That Decides Everything

Proceeds are easy; the exchange tells you what you got. Basis is where Bitcoin taxes are won or lost, because most holders bought at many different prices over many years. When you sell 0.5 BTC out of a stack accumulated since 2017, which 0.5 BTC you sold determines the gain.

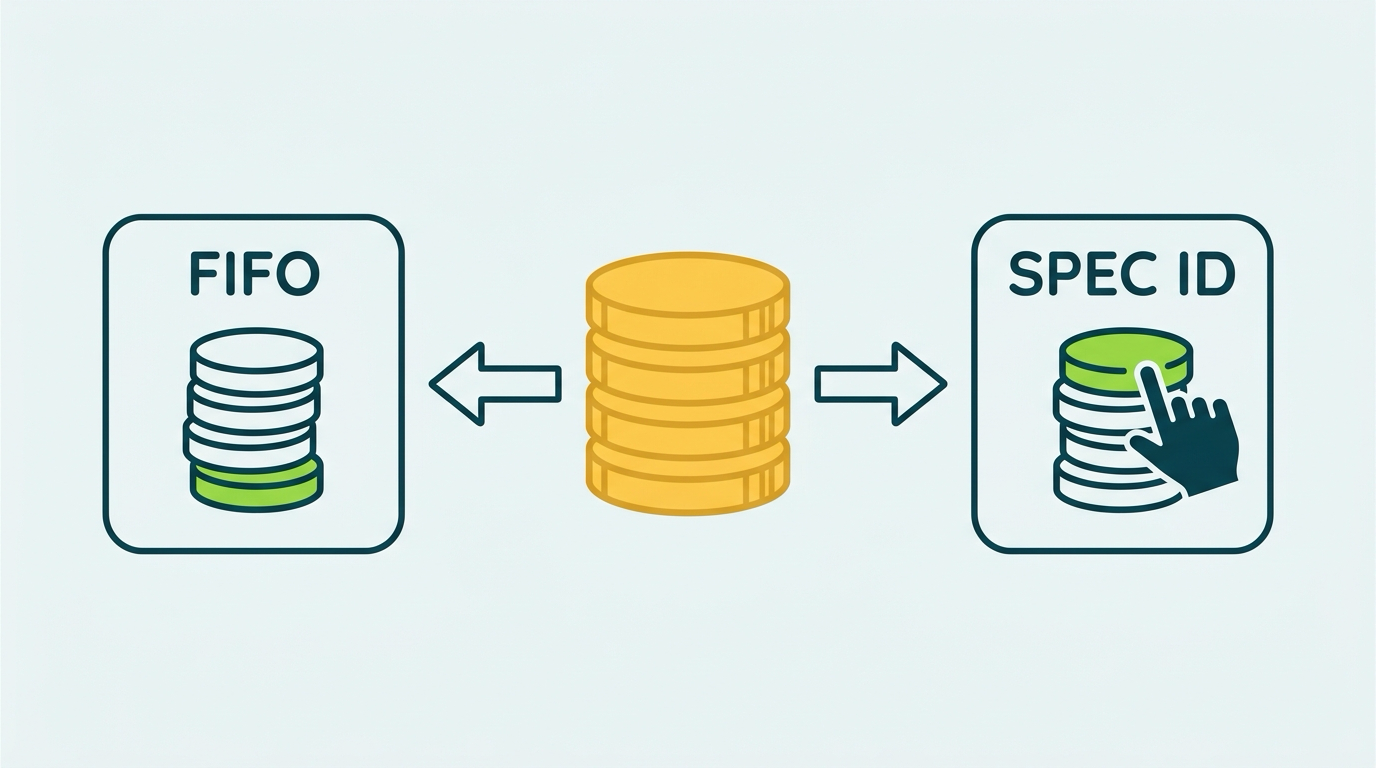

FIFO: The Default

Absent an election, the IRS assumes first in, first out: your oldest coins sell first. For long-time holders, oldest usually means cheapest, so FIFO tends to maximize reported gains. It is simple and safe, and it quietly overpays for anyone who accumulated through multiple cycles.

Specific Identification and HIFO

The alternative is specific identification: you choose exactly which lots each sale disposes of. The most common ordering is HIFO (highest in, first out), which sells the most expensive lots first and minimizes current gains.

Spec ID is powerful but conditional. To use it you must:

- Identify the units no later than the time of sale. The identification has to reference the specific lots (acquisition date and cost) being sold, recorded in your books or through your exchange or software settings before or at the disposal.

- Keep records proving it. Lot-level history showing when each unit was acquired, its basis, and when it was sold.

Retroactively cherry-picking lots at filing time does not qualify. Configure your tax software’s method before the sale, not after. The full comparison, with worked numbers, is in our FIFO vs HIFO vs Spec ID guide.

FIFO vs HIFO on the Same Sale

You hold three lots: 0.5 BTC bought at $15,000 total in 2019, 0.5 BTC bought at $30,000 in 2021, and 0.5 BTC bought at $52,000 in 2025. You sell 0.5 BTC for $60,000 in 2026. FIFO disposes of the 2019 lot: $45,000 of long-term gain. HIFO disposes of the 2025 lot: $8,000 of gain, though short-term if sold within a year of purchase. Same sale, same wallet, a five-figure difference in reported gain. The method election is the cheapest tax planning available to Bitcoin holders.

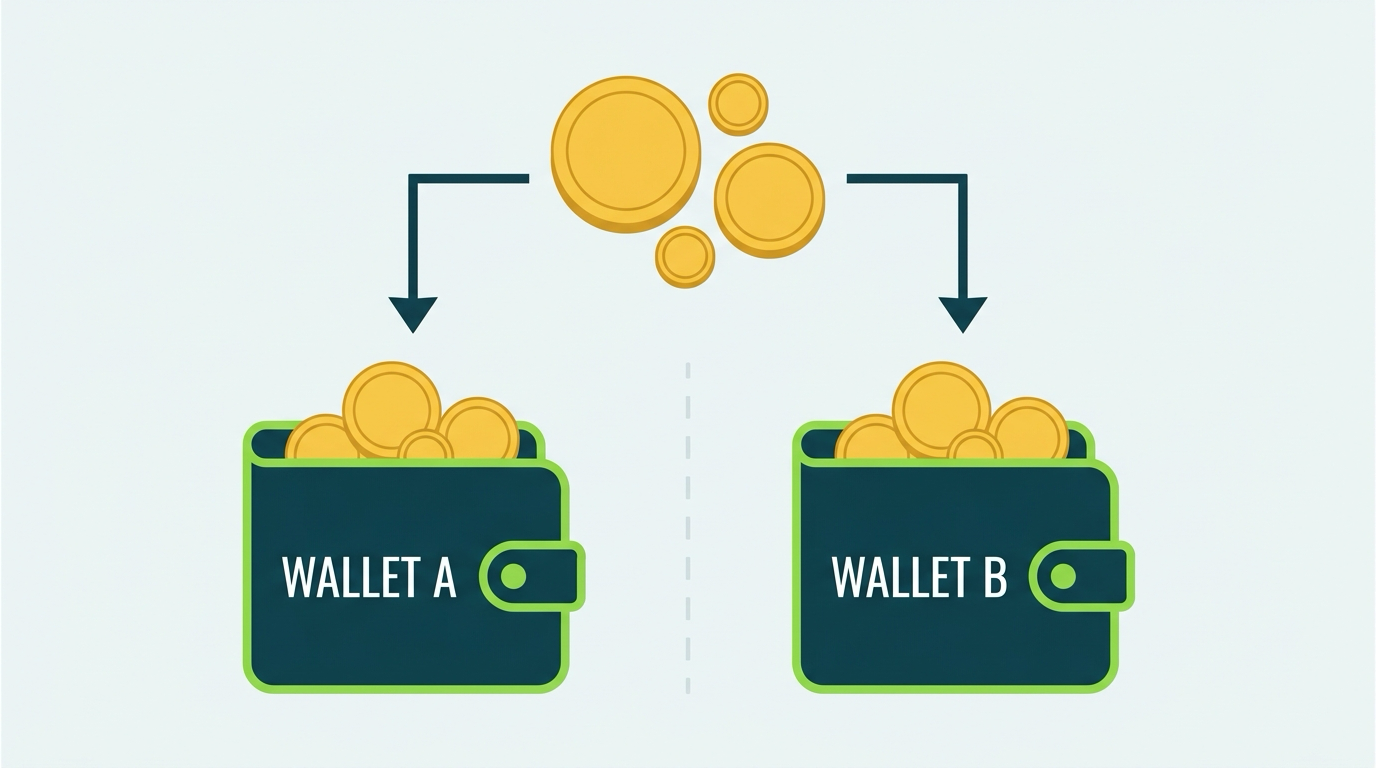

Rev. Proc. 2024-28: The Wallet-by-Wallet Migration

The biggest structural change for Bitcoin sellers took effect on January 1, 2025, and many holders still have not dealt with it.

Before 2025, most people and most software used universal tracking: all wallets pooled together, so a sale on Coinbase could be matched against basis from coins sitting in cold storage. Rev. Proc. 2024-28 ended that. Since January 1, 2025, basis must be tracked wallet by wallet and account by account. A sale from a given wallet can only consume basis from lots actually held in that wallet.

The revenue procedure included a one-time safe harbor: taxpayers could allocate their existing unused basis across their wallets as of January 1, 2025, either by specific units or under a written global allocation rule established before that date. Done properly, the allocation became your starting point for the new regime.

If you never did the allocation, you are not doomed, but your records are now out of spec. Your software may still be silently pooling basis across wallets in a way the rules no longer permit, and a future sale could be reported with basis you cannot defend. The fix is to establish a reasonable, documented allocation now and correct your lot tracking going forward, ideally before your next large sale, and a crypto tax specialist can run the allocation with you in a single working session. Our Rev. Proc. 2024-28 guide covers the mechanics in detail.

Form 1099-DA: What the IRS Now Sees

Broker reporting for digital assets arrived in two waves, and understanding the gap between them explains most of the notices that will go out over the next few years.

Wave one: gross proceeds. For sales on or after January 1, 2025, custodial brokers (Coinbase, Kraken, Gemini, and the rest) file Form 1099-DA reporting what you sold and what you received. The first forms landed in early 2026 covering 2025 sales.

Wave two: basis. Starting with assets acquired on or after January 1, 2026, brokers must also report cost basis, but only for covered assets: coins bought and held at the same broker until sale. Bitcoin you transferred in from a wallet, another exchange, or a decade of self-custody is non-covered, and the broker reports proceeds with no basis or a blank.

That asymmetry is the trap. The IRS sees the full proceeds of your sale. It does not see the $37,000 you paid across nine buys since 2018. If you report nothing, the automated matching systems can treat the entire proceeds as gain. Your own records are the only thing standing between a correct return and a notice priced off zero basis.

Two more points worth knowing. Wrapping, lending, staking, and similar DeFi transactions are temporarily exempt from broker reporting under Notice 2024-57, pending further guidance. And self-custody sales generate no 1099-DA at all, which changes what the IRS sees but changes nothing about what you owe. Our Form 1099-DA guide covers reconciliation line by line.

Spending Bitcoin Is Selling Bitcoin

The rule people most want to be wrong about: using Bitcoin to buy anything is a disposal at fair market value. Buy a $6 coffee with BTC you acquired at a basis of $2, and you have a $4 capital gain. Buy a $70,000 truck with BTC you bought years ago for $10,000, and you have a $60,000 gain, taxed as if you had sold the coins and paid cash.

There is currently no de minimis exemption. Proposals to exempt small personal transactions (a few hundred dollars per purchase) have circulated in Congress for years, including in the 2025 legislative sessions, but none had become law as of this writing. Until one does, every spend is technically a reportable disposal.

Practical guidance for people who actually spend BTC:

- Spend from a dedicated wallet funded with recent, high-basis coins, so each disposal generates minimal gain and clean records.

- Let software do the math. Connected wallets and cards report each spend as a disposal automatically; manual reconstruction of a year of coffee purchases is misery.

- Do not assume BTC debit cards are invisible. Card providers that liquidate your BTC are exactly the kind of broker 1099-DA was built for.

Bitcoin promised to be money you can spend. The tax code treats every spend as a stock sale. Until a de minimis rule passes, the coffee is a capital transaction, and pretending otherwise just means reporting it late.

Gifting and Donating Bitcoin

Not every way of parting with Bitcoin triggers gain. Two routes move coins out of your hands without a disposal, and one of them is genuinely one of the best deals in the tax code.

Gifts

Giving Bitcoin is not a taxable event for the giver. No gain, no loss, regardless of appreciation. For 2026, gifts up to $19,000 per recipient (per year, per giver) require no gift tax return; larger gifts require Form 709 but almost never actual tax, since they just consume lifetime exemption.

The recipient takes your carryover basis and holding period for gains. If you bought at $5,000 and gift at $100,000, the recipient’s gain basis is $5,000, and your holding period tacks on. For losses, a special rule uses the value at the gift date if lower, which kills the strategy of gifting losses to relatives. Full rules, including estate step-up treatment, are in our crypto gift tax guide.

Donations

Donating appreciated Bitcoin held more than one year to a qualified charity is the single most tax-efficient exit. You deduct the full fair market value (up to 30% of AGI, with carryforward) and you never recognize the built-in gain. Donating $50,000 of BTC with a $5,000 basis deducts $50,000 and erases $45,000 of gain from ever being taxed.

Requirements matter: donations over $5,000 need a qualified appraisal (an exchange printout does not count), Form 8283, and the charity must actually take the coins. Donating short-term BTC limits the deduction to basis, so hold past a year before giving. Large planned donations are worth a quick conversation with a crypto tax advisor before the transfer, because the appraisal and paperwork sequence is unforgiving after the fact.

Tax Loss Harvesting: The Window That Is Still Open

Bitcoin’s volatility cuts both ways, and losses have real value. Selling BTC below basis produces a capital loss that offsets capital gains dollar for dollar, then up to $3,000 of ordinary income per year, with the remainder carrying forward indefinitely.

What makes crypto harvesting unusual is the wash sale rule, or rather its absence. Section 1091 disallows losses on securities repurchased within 30 days. Spot Bitcoin is property, not a security, so under current law you can sell at a loss and rebuy immediately, banking the loss while keeping the position. Note the distinction: shares of spot Bitcoin ETFs are securities, and their tax quirks live in our Bitcoin ETF tax guide.

Three cautions before you harvest aggressively:

- Congress keeps aiming at this. Proposals to extend wash sale treatment to digital assets have appeared in multiple budget bills and legislative packages since 2021, including in the 2025 to 2026 sessions. None had passed as of this writing, but any enacted change could apply going forward, and structuring your affairs around the loophole surviving forever is not a plan.

- Economic substance still matters. A loss sale and instant rebuy has been blessed by the absence of a statute, not by the IRS. Wash-sale-like patterns executed purely on paper, with no market exposure at any point, carry more risk than a real sale and a real repurchase.

- Per-wallet tracking applies. Post Rev. Proc. 2024-28, the harvested lot must actually exist in the wallet you sell from, and the rebuy creates a new lot with a new date, which restarts the long-term clock.

Our tax loss harvesting guide and wash sale rule explainer cover strategy and timing in depth. If you are sitting on six-figure paper losses and are not sure how to sequence the harvest, that is a fifteen-minute conversation with a crypto tax specialist, not a guess.

Harvesting a Drawdown Without Losing the Position

You hold 1 BTC bought at $95,000, now trading at $68,000. You sell, realizing a $27,000 loss, and rebuy 1 BTC minutes later at essentially the same price. The loss offsets $27,000 of gains you took earlier in the year on other assets, saving roughly $4,000 to $6,400 of tax depending on rate. Your Bitcoin exposure never meaningfully changed. Your new lot has a $68,000 basis and a fresh holding period, so plan any near-term sale accordingly.

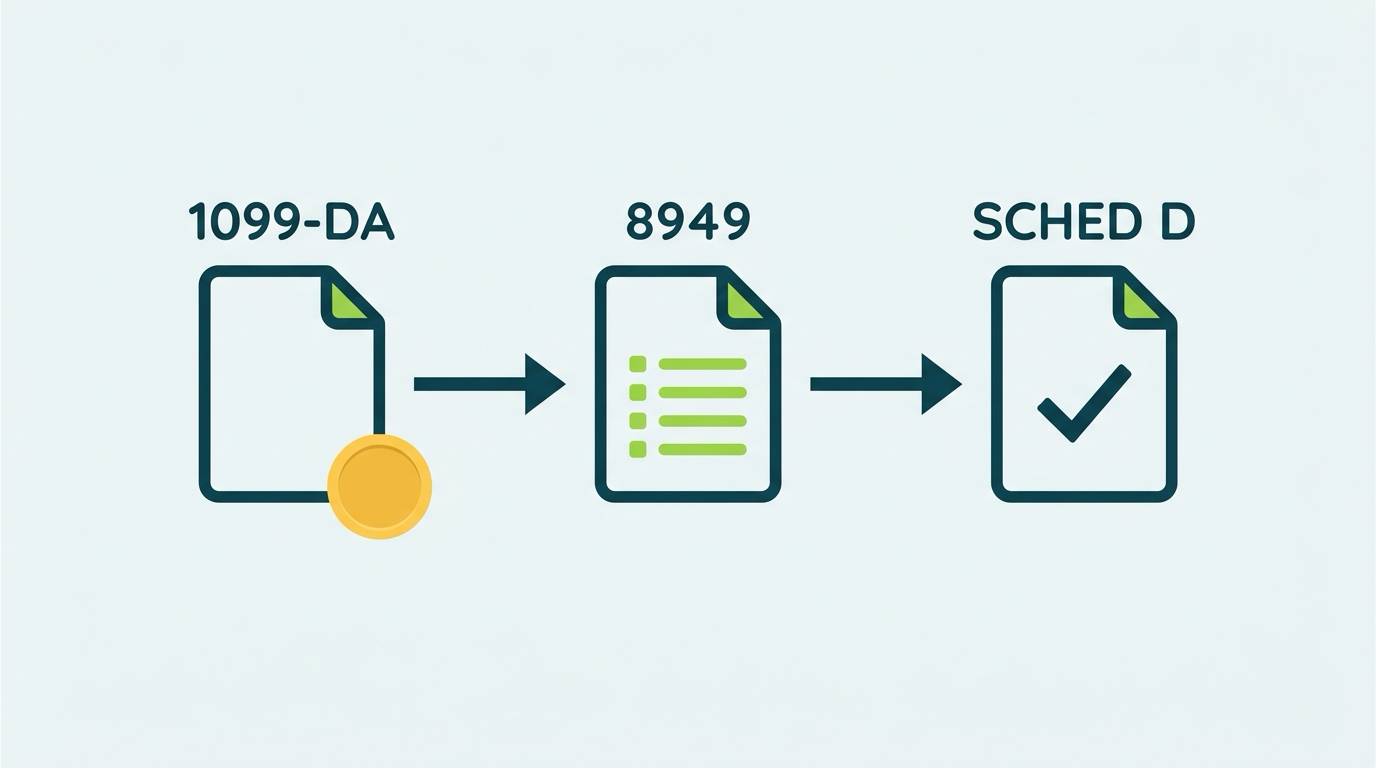

Form 8949 and Schedule D: The Mechanics

Every Bitcoin disposal lands on the same two forms, and the pipeline is the same whether you sold once or a thousand times.

- Assemble every disposal for the year: sales, swaps, spends. Exchange exports plus wallet imports into crypto tax software (Koinly, CoinTracker, CoinLedger) get you the raw list.

- Match transfers. Every wallet-to-exchange move must be linked as a self-transfer, not a fresh zero-basis deposit. This is where most overstated gains come from.

- Confirm the basis method your software applied (FIFO or your spec ID election) and that it matches what you actually configured at sale time.

- Complete Form 8949. Each disposal gets a row: description, date acquired, date sold, proceeds, basis, gain or loss. Broker-reported covered transactions go in different sections than non-covered ones; your software sorts them.

- Flow totals to Schedule D, which nets short-term against short-term, long-term against long-term, and produces the number that hits your 1040.

- Reconcile any 1099-DA. Proceeds on the form must be findable in your 8949. Basis gaps on the form get filled from your records.

- Answer the digital asset question on Form 1040 truthfully. Selling means yes.

The full walkthrough with screenshots lives in our Form 8949 and Schedule D guide.

The Long-Time Holder Problem: Missing Basis

A specific and common emergency: you bought Bitcoin between 2013 and 2018, the exchange is dead (Mt. Gox, Cryptsy, QuadrigaCX) or you bought peer to peer, you have no records, and now you want to sell a position worth hundreds of thousands of dollars.

Reporting zero basis is the default catastrophe: you pay capital gains tax on 100% of proceeds. Reporting a guessed basis with nothing behind it invites an adjustment you cannot fight. The right answer is reconstruction, and it works far more often than people expect:

- Bank records. Wire and ACH transfers to exchanges establish how much fiat went in and when. Banks can retrieve statements going back many years.

- Email archives. Trade confirmations, deposit receipts, and withdrawal notices from dead exchanges usually still exist in your inbox.

- The blockchain itself. Coins arriving in your wallet are timestamped forever. The receipt date bounds the acquisition date, and historical price data converts dates to defensible values.

- Old devices and files. Wallet files, CSV exports, and screenshots from prior tax years.

A reconstructed basis built from converging evidence, documented and consistently applied, is a defensible position. It is painstaking work, and it is exactly the kind of forensic project a crypto tax specialist does every week. The difference between zero basis and reconstructed basis on an early stack is routinely six figures of tax.

Common Mistakes When Selling Bitcoin

The recurring errors from cleanup engagements, ordered by expense.

Selling With Unmatched Transfers

Coins moved from cold storage to an exchange, logged as a deposit instead of a transfer, sold with zero basis. The single most common overstatement of gain in crypto tax software.

Ignoring the Holding Period Line

Selling at eleven and a half months instead of twelve, converting a 15% gain into a 32% or 37% gain out of impatience.

Cherry-Picking Lots After the Fact

Deciding in March which lots you “sold” last August. Specific identification must be contemporaneous. Set the method before the sale.

Forgetting Swaps and Spends

BTC to USDC conversions and card spends are disposals. People who “didn’t sell anything” often disposed of Bitcoin dozens of times.

Assuming the 1099-DA Is the Return

The form has proceeds and, for most legacy holders, no basis. Filing straight off the form without supplying basis means overpaying, sometimes by the full tax on your original investment.

Skipping the Rev. Proc. 2024-28 Allocation

Selling in 2026 with software still pooling basis universally across wallets. The reported basis may be indefensible even when the economic gain is right.

Your Bitcoin Selling Checklist

- Know each lot you hold: acquisition date, basis, and current wallet.

- Confirm your per-wallet allocation under Rev. Proc. 2024-28 is documented.

- Choose the basis method before selling, and configure it in your software.

- Check the holding period on the lots you plan to sell; wait out the one-year line when it is close.

- Estimate the tax, including NIIT and state, before the sale so the cash is reserved.

- Match every self-transfer in your records the day it happens.

- Harvest losses deliberately, with documentation, while the wash sale window remains open.

- Consider gifting or donating appreciated coins instead of selling when giving is the goal anyway.

- Reconcile the 1099-DA against your own records before filing.

- Reconstruct missing basis before selling, not after.

Bottom Line

Selling Bitcoin is taxed on a simple formula and a mountain of record-keeping. The formula: proceeds minus basis, at 0/15/20% long-term or ordinary rates short-term, plus 3.8% NIIT for high earners. The records: lot-level basis, tracked per wallet since January 1, 2025, provable through a reporting system that now shows the IRS your proceeds but not your costs.

Selling is also only one chapter of the Bitcoin tax story. Mining income, ETF quirks, Ordinals, and DeFi each carry their own rules, and our complete Bitcoin tax guide ties the whole picture together.

The holders who get hurt are almost never the ones who owed the most tax. They are the ones who sold first and organized never: unmatched transfers, phantom zero-basis lots, universal tracking that no longer complies, and a decade-old stack with no paperwork. All of it is fixable, and it is dramatically cheaper to fix before the sale than after the notice. Count On Sheep reconstructs basis, runs the per-wallet migration, and delivers CPA-ready numbers for positions of any vintage. A 15-minute call with a crypto tax specialist will tell you exactly where your records stand, or reach out to our team for a full review before your next sale.

Not sure your crypto taxes are right?

Talk to a Count On Sheep specialist. We will spot the costly errors before you file. No obligation.

Book My Free Review- Reviewed by Former Big 4 Accountants

- Keep your CPA

- No pressure, no sales pitch

Related Reading

- Bitcoin Mining Taxes: Hobby vs Business

- Bitcoin ETF Taxes: IBIT, FBTC & Grantor Trusts

- Bitcoin Ordinals & BRC-20 Taxes

- Wrapped Bitcoin & BTC DeFi Taxes

- Crypto Capital Gains Tax Guide

- FIFO vs HIFO vs Spec ID

- Form 1099-DA Explained

Frequently Asked Questions

How much tax do I pay when I sell Bitcoin?

It depends on your holding period and income. Bitcoin held more than one year gets long-term capital gains rates of 0%, 15%, or 20% based on your taxable income. Bitcoin held one year or less is taxed as ordinary income at rates up to 37%. High earners may also owe the 3.8% net investment income tax on top of either rate.

What are the 2026 long-term capital gains brackets?

For 2026, single filers pay 0% on taxable income up to $49,450, 15% from $49,451 to $545,500, and 20% above that. Married filing jointly pays 0% up to $98,900, 15% from $98,901 to $613,700, and 20% above. Your Bitcoin gain stacks on top of your other income to determine which bracket applies.

Is spending Bitcoin a taxable event?

Yes. Using Bitcoin to buy anything, from a car to a coffee, is a disposal of property. You realize a capital gain or loss equal to the difference between the item's price and your cost basis in the Bitcoin you spent. There is no de minimis exemption under current law, so even small purchases technically count.

What cost basis method should I use for Bitcoin?

FIFO (first in, first out) is the default. You can use specific identification instead, which lets you choose which lots to sell, including highest cost first (HIFO), but you must identify the units no later than the time of sale and keep records supporting the identification. Spec ID usually produces lower gains for long-time holders.

What did Rev. Proc. 2024-28 change for Bitcoin holders?

It ended universal basis tracking. Starting January 1, 2025, cost basis must be tracked wallet by wallet and account by account. The revenue procedure gave a one-time safe harbor to allocate old basis across wallets as of that date. If you never did the allocation, your basis records need attention before you sell.

Will the IRS know I sold my Bitcoin?

If you sold on a US exchange, yes. Brokers began reporting gross proceeds on Form 1099-DA for 2025 transactions, and basis reporting for assets bought and sold on the same platform starts with 2026 acquisitions. Self-custody sales generate no form, but the deposit and sale still leave a permanent on-chain trail.

Does the wash sale rule apply to Bitcoin?

Not under current law. The wash sale rule in Section 1091 covers securities, and spot Bitcoin is treated as property, not a security. You can sell at a loss and rebuy immediately while keeping the loss. Congress has proposed extending wash sale treatment to digital assets several times, so this window may not stay open.

How do I report a Bitcoin sale on my tax return?

Each disposal goes on Form 8949 with the acquisition date, sale date, proceeds, and cost basis. Totals flow to Schedule D, which nets short-term and long-term results. You also answer yes to the digital asset question on Form 1040. If you received a 1099-DA, reconcile it against your own records before filing.

What if I do not know my Bitcoin cost basis?

Reconstruct it. Old exchange records, bank statements showing fiat transfers, wallet histories, and blockchain timestamps can usually rebuild acquisition dates and prices. Reporting zero basis means paying tax on your entire proceeds, which massively overstates the real gain for most long-time holders. A specialist can usually recover most of it.

Is gifting Bitcoin taxable?

Giving Bitcoin is not a taxable disposal for the giver. Gifts up to the $19,000 annual exclusion per recipient for 2026 require no gift tax return. The recipient takes your basis and holding period for gains. Donating Bitcoin held over a year to charity is even better: a fair market value deduction with no capital gain.

Do I owe the 3.8% net investment income tax on Bitcoin gains?

You might. NIIT applies to net investment income, including Bitcoin capital gains, once modified adjusted gross income exceeds $200,000 for single filers or $250,000 for married filing jointly. A large Bitcoin sale can push you over the threshold by itself, adding 3.8% on top of your capital gains rate.

Can I still harvest Bitcoin losses in 2026?

Yes. Selling Bitcoin below your basis realizes a capital loss that offsets other gains plus up to $3,000 of ordinary income per year, with the rest carried forward. Because the wash sale rule does not currently apply, you can repurchase immediately. Document each harvest carefully in case the law changes.