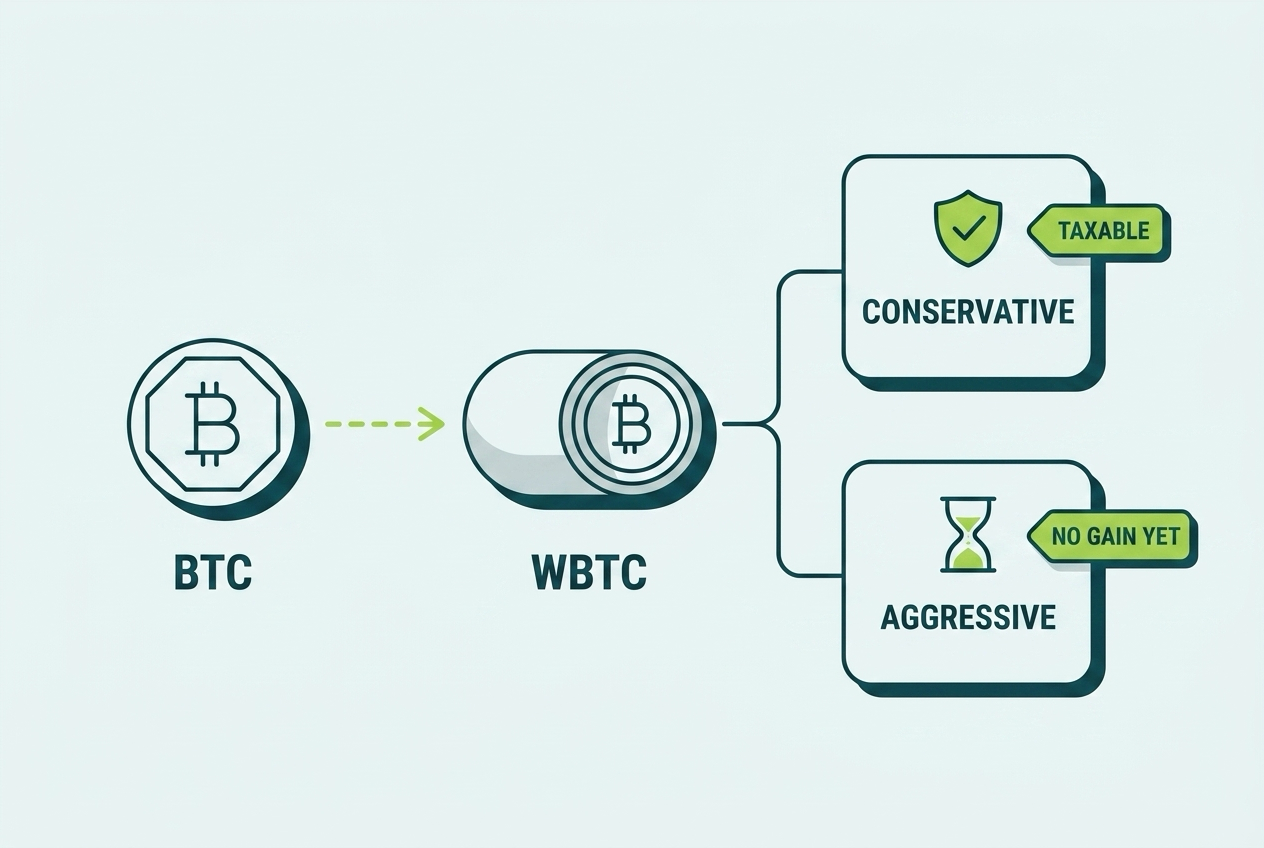

Is wrapping Bitcoin taxable? Nobody can tell you with certainty, because the IRS has never ruled on it. The conservative position treats BTC to WBTC as a taxable crypto-to-crypto exchange. The aggressive position says your Bitcoin exposure never changed, so nothing was disposed of. Everything else in Bitcoin DeFi is clearer: lending interest is income, loans are not, liquidations are, Lightning spends are disposals, and staking yield is income at receipt.

Bitcoin was designed to sit still, and an entire industry now exists to make it do otherwise. Holders wrap BTC into WBTC, cbBTC, and tBTC to reach Ethereum and Base DeFi, lend it for yield, post it as loan collateral, stake it through Babylon to secure other networks, and spend it instantly over Lightning. Every one of those moves has a tax consequence, and several of them sit in genuinely unsettled law where the difference between the conservative and aggressive position can be an entire tax bill.

This guide covers wrapped Bitcoin and BTC DeFi taxes end to end for 2026: the wrap question in both directions, lending on CeFi and DeFi, collateralized borrowing and the liquidation trap, yield on Bitcoin L2s and sidechains, Lightning payments and routing income, Babylon-style staking, bridging, and how to keep basis intact as coins change form. It is one piece of our full Bitcoin tax guide, alongside our guides to selling Bitcoin, Bitcoin mining, Bitcoin ETFs, and Ordinals and BRC-20 tokens.

Disclaimer: This guide is for informational purposes only and is not tax or legal advice. Cryptocurrency rules change quickly. Always consult a qualified CPA about your specific situation.

The Wrap Question: Two Defensible Answers and No Referee

Wrapping is the doorway to everything else in BTC DeFi, so start with the hard part. When you wrap Bitcoin, you hand BTC to a custodian or protocol (BitGo for WBTC, Coinbase for cbBTC, the Threshold network for tBTC) and receive a token on another chain that tracks BTC one to one. Did you just sell your Bitcoin?

The conservative position: yes, it is an exchange. You gave up one asset (BTC on Bitcoin) and received a different one (an ERC-20 token on Ethereum, issued by an identifiable counterparty, carrying custodial risk BTC does not have). Crypto-to-crypto exchanges are taxable, so wrapping realizes gain or loss on your BTC, and the wrapped token takes a fresh basis. This reading fits the letter of the property rules and is the harder position to attack.

The aggressive position: no, nothing happened. Your economic exposure is unchanged: one BTC in, one BTC-pegged claim out, redeemable at par. Wrapping resembles moving an asset between your own accounts or changing its form, not disposing of it. There is no realization because nothing was gained or lost in substance. Plenty of practitioners find this persuasive, especially for trust-minimized wraps like tBTC, and industry groups have pushed the IRS to adopt exactly this rule.

What the IRS has actually said: nothing definitive. No ruling, no regulation, no case. The closest signal is procedural: Notice 2024-57 temporarily exempted wrapping and unwrapping transactions from broker reporting requirements, pending further study, which tells you the government itself has not decided how to characterize them.

How to operate inside the uncertainty:

- Pick a position deliberately, ideally with advice from a crypto tax specialist scaled to your dollar amounts. A $2 million wrap deserves a memo; a $2,000 wrap deserves a consistent software setting.

- Apply it symmetrically. Wrap and unwrap must use the same theory. Treating the wrap as non-taxable and then claiming a stepped basis at unwrap is indefensible.

- Be consistent across years and across wraps. WBTC this year and cbBTC next year should get the same answer.

- Document the choice and keep the values at every wrap date regardless, so you can recompute under either theory if guidance arrives.

One Wrap, Two Tax Outcomes

You bought 1 BTC at $30,000 and wrap it into WBTC when BTC trades at $68,000. Conservative treatment: you recognized a $38,000 long-term capital gain today, and your WBTC basis is $68,000. Aggressive treatment: no gain today, and your WBTC carries the original $30,000 basis and holding period. If you unwrap and sell later at $75,000, both roads eventually tax the same total $45,000 of gain; what differs is when it lands, and paying tax years early on a position you never exited is exactly what the aggressive camp objects to.

Lending Bitcoin: Interest Is Income, Everywhere

Lend BTC through a CeFi platform or supply wrapped BTC to Aave, Morpho, or Compound, and the yield is ordinary income at fair market value when you receive or gain control of it. There is no meaningful conservative-versus-aggressive debate here; income from lending property is income.

The mechanics worth getting right:

- Each payment is its own income event at that day’s price. Daily accrual paid in kind means many small lots, each with its own basis equal to the income recognized. Software handles this if the wallet or account is connected; it does not if the platform’s statements never make it into your records.

- Interest paid in platform tokens is valued at the token’s price on receipt, not BTC’s.

- DeFi supply positions that issue receipt tokens (aTokens and their cousins) add a wrap-like wrinkle: depositing WBTC and receiving aWBTC raises the same exchange-versus-form question as wrapping itself. Most filers treat pure deposit receipts as non-events and the yield as income, but the position deserves the same consistency discipline. Our NFT and DeFi tax guide covers pool and receipt-token mechanics in depth.

- CeFi failures taught the ugly lesson. Celsius, BlockFi, and Voyager depositors learned that lent coins are unsecured claims. Bankruptcy losses are generally deductible only when fixed and determinable, often years later at plan confirmation, and partial recoveries in kind reset basis in ways that need care. If you carried claims through those bankruptcies, those returns are worth a look from a crypto tax professional, and our lost and stolen crypto guide maps the framework.

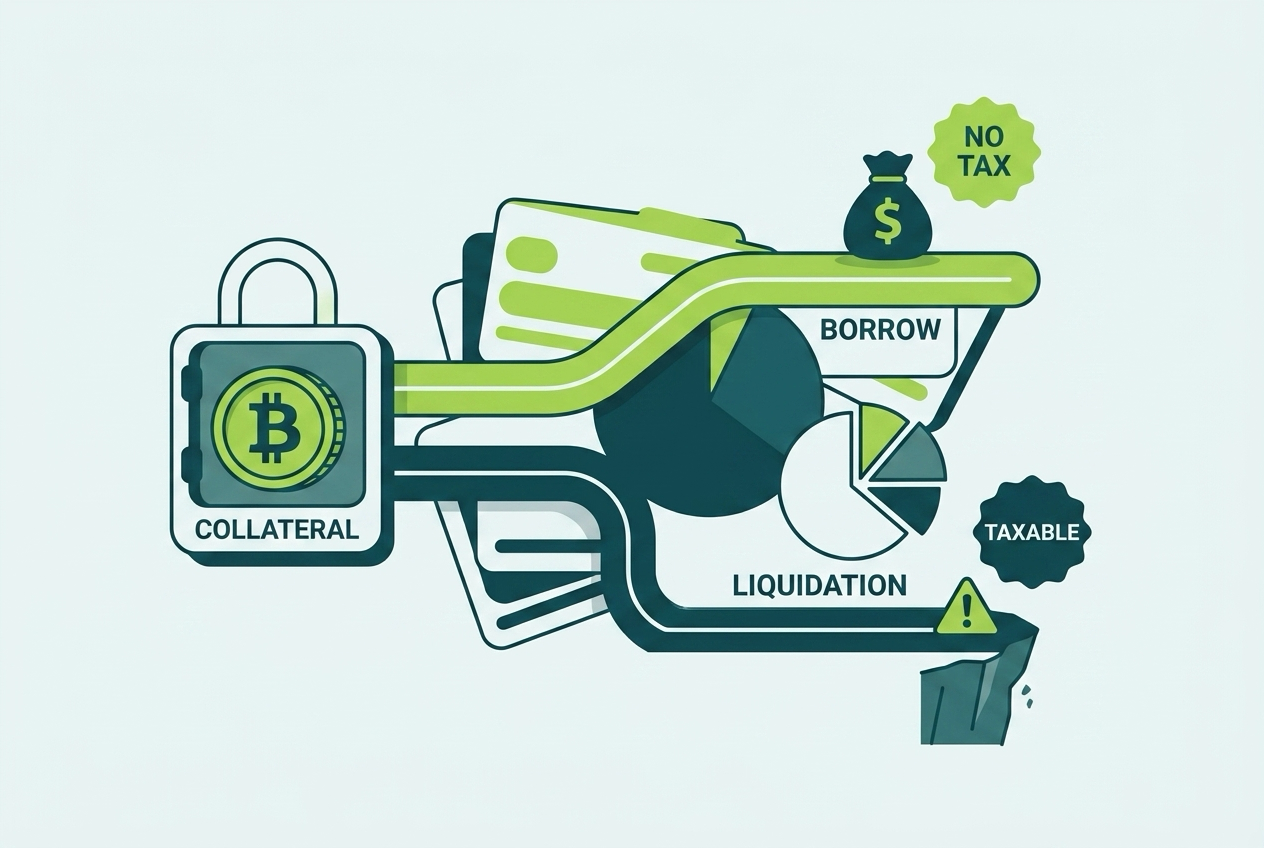

Borrowing Against Bitcoin: The Non-Taxable Move With a Taxable Cliff

Borrowing is the clean way to extract liquidity from a Bitcoin position, and its tax profile explains its popularity with long-time holders sitting on enormous unrealized gains.

Posting BTC as collateral is not a disposal so long as you retain ownership, and loan proceeds are not income; you owe them back. A holder with $20,000-basis coins worth $500,000 can borrow cash against them without recognizing a dollar of the appreciation, a strategy that works identically whether the lender is a DeFi protocol or a regulated desk.

Three edges of the cliff:

Liquidation is a sale. If BTC drops and the platform liquidates your collateral, that is a disposal of your coins at the liquidation price, with gain measured against your original basis. The market crashed, your position was seized, and you owe capital gains tax anyway, because the gain from $20,000 to the liquidation price was real even if the last month was painful. Liquidation events are the single nastiest surprise in BTC DeFi.

Title matters. Some CeFi lending arrangements historically took ownership of collateral, rehypothecated it, or structured the “loan” in ways that look like a disposal at inception. Read the terms; on-chain protocols where coins sit in a contract you can redeem from are cleaner on this point than custodial agreements.

Spending borrowed funds is fine; repaying in BTC is not. Repaying a loan with appreciated BTC is a disposal of that BTC at repayment-date value. Borrowers who mentally treat the loan as “spending my Bitcoin without selling” sometimes complete the irony by actually selling BTC to repay it.

The Liquidation That Cost Twice

You post 1 BTC (basis $27,000) as collateral and borrow $40,000 in stablecoins. BTC falls hard and the protocol liquidates your collateral at $68,000 to cover the debt. You just realized a $41,000 capital gain, in a down market, with no cash proceeds in hand beyond the loan you already spent. The tax bill arrives the following April regardless. Conservative loan-to-value ratios are tax planning, not just risk management.

Lightning Network: Small Payments, Real Rules

Lightning makes Bitcoin spendable at coffee speed, and the tax rules follow the payments at the same speed.

Spending over Lightning is a disposal. The rule from our selling Bitcoin guide applies without modification: paying a 40,000-sat invoice disposes of those sats at fair market value against their basis. There is no de minimis exemption under current law, so high-frequency Lightning spenders generate high-frequency micro-disposals. A dedicated spending wallet funded with recent, high-basis coins keeps each event’s gain near zero and the records tractable.

Channel management is self-transfer. Opening a channel moves your BTC into a 2-of-2 multisig you co-control; closing returns it. Between your own wallets and channels, these are non-taxable transfers whose fees join your cost records. Force closes and splices are more of the same, with worse fee documentation.

Routing fees are income. Run a routing node and every forwarded payment pays you sats: ordinary income at value when earned. A serious routing operation with meaningful capital deployed starts to look like a trade or business, with Schedule C treatment, self-employment tax, and deductible costs (hardware, channel fees, hosting), the same hobby-versus-business analysis that governs miners.

Receiving Lightning payments for goods or services is ordinary income at receipt value, identical to being paid in on-chain BTC.

Staking Bitcoin: Babylon and the Yield Frontier

Bitcoin staking, popularized by Babylon, lets holders lock BTC in self-custodied scripts that provide economic security to proof-of-stake networks, earning yield paid in those networks’ tokens or in BTC-denominated rewards.

The framework comes from Rev. Rul. 2023-14, the staking ruling: rewards are ordinary income at fair market value when you gain dominion and control over them. Applied to BTC staking:

- The lock itself is generally not a disposal. Babylon-style staking keeps BTC in a script you control, closer to a channel open than a wrap. Liquid staking wrappers that hand you a tradeable receipt token reintroduce the wrap question on top.

- Rewards are income at receipt, valued at the reward token’s price when claimable, and that value becomes basis. Rewards in an illiquid new token deserve documented pricing evidence at claim time.

- Slashing is a loss event whose character (capital versus other) depends on structure; document any slashed principal carefully and get advice, because the law here is as new as the products.

Yield programs on Bitcoin L2s and sidechains (Stacks, Rootstock, and the newer rollup crowd) follow the same skeleton: getting BTC onto the L2 usually means a bridge or wrap (see the next section), yield is income at receipt, and disposals of L2 assets are capital events. The chain changes; the framework does not.

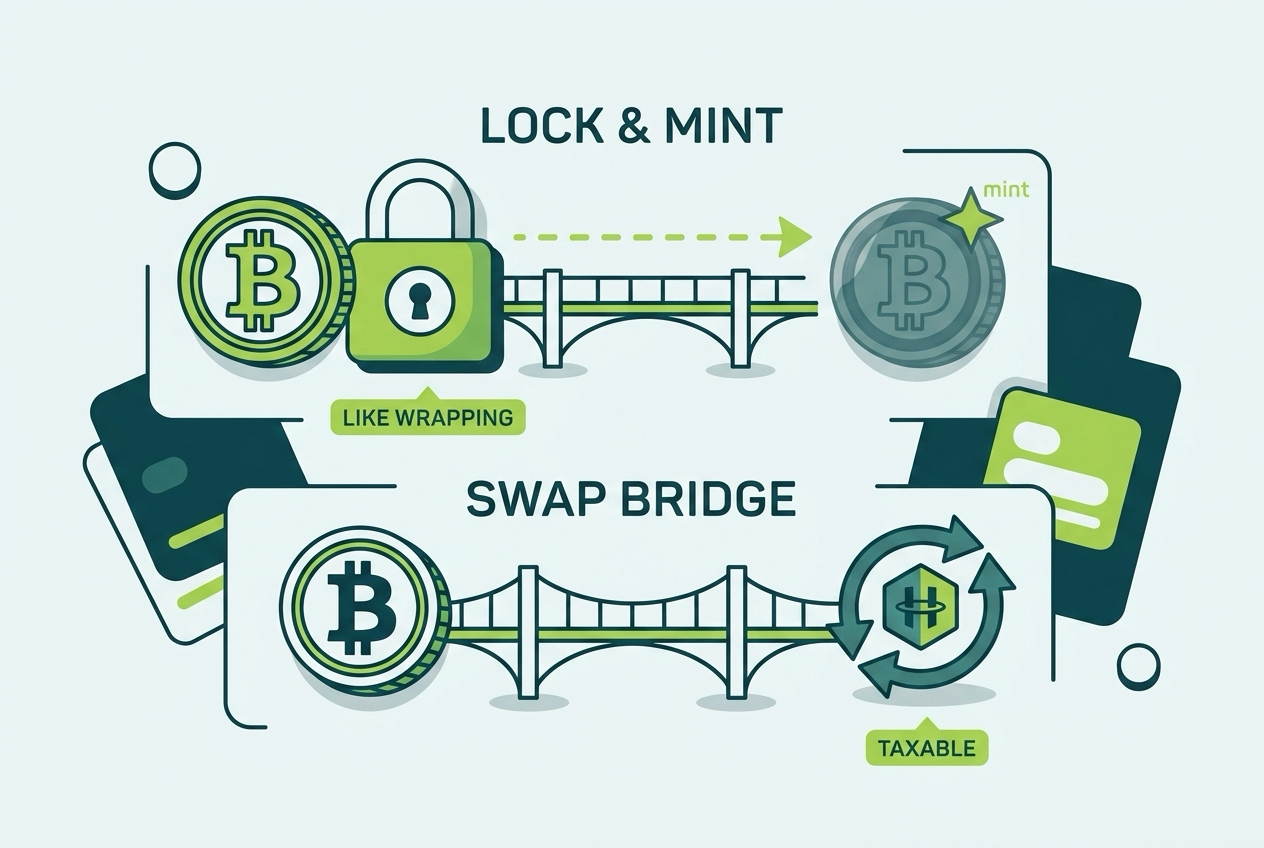

Bridging: Know What the Bridge Actually Does

“Bridging” describes at least two different mechanisms with different tax profiles, and users rarely check which one they used.

Lock-and-mint bridges hold your asset on the origin chain and issue a representation on the destination chain. This is wrapping by another name, and it inherits the full conservative-versus-aggressive analysis from above.

Liquidity and swap bridges take your BTC and give you a different asset from a pool on the destination chain. Two assets, two owners, an exchange: this looks taxable under ordinary swap rules, whatever the marketing calls it.

The practical rule: identify the mechanism at transaction time, not at filing time. A screenshot of the bridge’s documentation and the transaction hashes on both chains turns an unanswerable April question into a two-minute log entry.

Tracking Basis Across Wraps: The Bookkeeping That Holds It Together

Whatever positions you take, one discipline makes them all defensible: the lot must remain traceable through every change of form.

Under the per-wallet tracking rules of Rev. Proc. 2024-28, basis lives in specific lots in specific wallets. A BTC lot that wraps to WBTC, bridges to Base, gets supplied to a lending market, and comes back eighteen months later has changed form four times. Your records need to answer, at every step: which lot, what basis, what date, what theory.

The working system:

- One row per transformation. Date, direction (wrap, bridge, deposit, unwrap), amounts, fair market value, transaction hashes on both chains.

- Carry basis explicitly. Under a non-taxable theory, write the carried basis and original acquisition date on the new asset’s row. Under a taxable theory, write the recognized gain and the fresh basis.

- Reconcile quantities. WBTC out should equal BTC in minus fees; when it does not, find out why before your software invents a phantom disposal or a zero-basis deposit.

- Keep yield separate from principal. Interest and rewards are new lots with income-value basis; never let them blend into the wrapped principal’s lot.

Crypto tax software handles the common paths (major wraps, major lending markets) reasonably well and fails quietly on everything novel. Review its guesses on every wrap and bridge rather than trusting defaults, because a silent misclassification compounds across every later transaction in the chain. If your history includes years of wraps and bridges that were never tracked, a crypto tax specialist can reconstruct the lot lineage from the chains themselves.

What Gets Reported, and What Does Not

The reporting landscape for BTC DeFi tilted sharply in 2025, and the result is counterintuitive: less third-party reporting, more personal burden.

Custodial platforms report. Sell BTC on an exchange, or use a custodial lender that disposes of your coins, and Form 1099-DA tells the IRS your gross proceeds, with basis reporting phasing in for assets acquired and held at the same broker from 2026.

DeFi generally does not. The regulation that would have treated DeFi front-ends as brokers was repealed by Congress under the Congressional Review Act in 2025. And Notice 2024-57 temporarily exempts wrapping, unwrapping, lending, staking, and similar transactions from broker reporting even by covered brokers, pending further guidance.

The gap this creates should look familiar by now: the IRS eventually sees BTC and wrapped BTC arriving at exchanges with no reported history, while the wraps, yield, and bridges that produced them generated no paperwork at all. Unexplained proceeds plus visible on-chain history is the pattern enforcement is built to flag. Your transaction log is not a nicety; it is the only account of events that exists.

Congress repealed the rule that would have made DeFi report you, and the IRS paused the rules for wraps and staking. None of that repealed the tax. It just made you the only record-keeper in the room.

Common Wrapped BTC and DeFi Mistakes

The recurring failures from DeFi cleanups, cheapest first.

Letting Software Guess on Wraps

Default classifications treat some wraps as taxable swaps and others as transfers, inconsistently, in the same account. Review every wrap row; the default is whatever the parser guessed.

Asymmetric Wrap Positions

Non-taxable on the way in, stepped-up basis on the way out. Indefensible under every theory, and common because each half was decided in a different year.

Unlogged Yield Streams

Two years of daily interest in kind, never valued, never recorded, discovered when the receiving wallet hits an exchange. Reconstructing it is possible; logging it monthly would have taken minutes.

Treating Liquidations as Losses

The market crashed, so the borrower assumed the liquidation produced a loss. Against an early-cycle basis it produced a five-figure gain, unreported, with the platform’s records available to examiners.

Repaying BTC Loans With Appreciated BTC

A disposal hiding inside a debt payment. The loan was tax-free; the repayment was not.

Ignoring Bridge Mechanics

A “bridge” that was actually a cross-chain swap, filed as a transfer. The destination asset’s basis and the origin asset’s unreported gain are both wrong until someone checks the mechanism.

Your Wrapped BTC and DeFi Tax Checklist

- Pick your wrap position (taxable exchange or non-event), document it, and apply it in both directions.

- Log every wrap, unwrap, and bridge with dates, values, hashes, and the mechanism used.

- Record every yield payment at receipt-date fair market value, in a lot separate from principal.

- Know your loan terms: who holds title to collateral, and at what price liquidation triggers.

- Keep loan-to-value conservative; a liquidation is a taxable sale at the worst time.

- Track Lightning spending from a dedicated high-basis wallet, and log routing income if you run a node.

- Value staking rewards at claim with documented pricing, especially for new tokens.

- Reconcile wrapped quantities against origin lots so software cannot invent phantom disposals.

- Carry lot lineage per wallet under Rev. Proc. 2024-28 through every change of form.

- Review platform bankruptcy claims from CeFi failures before assuming a loss year.

Bottom Line

Bitcoin DeFi taxes split into the settled and the unsettled. Settled: lending interest, staking yield, and routing fees are ordinary income at receipt; Lightning spends and loan liquidations are disposals; borrowing itself is tax-free. Unsettled: whether wrapping and lock-and-mint bridging are disposals at all, a question the IRS has conspicuously declined to answer while exempting those very transactions from its new reporting regime. Operating well means taking documented, symmetric positions on the unsettled parts and keeping immaculate records on all of it, because after the 2025 reporting rollbacks, nobody else is keeping them for you.

If your BTC has been through wraps, lending markets, a liquidation, or a bridge or five, and your records are a wallet address and a prayer, the reconstruction is standard work: the chains recorded everything, and the lot lineage can be rebuilt. Count On Sheep does exactly this, from single-wrap cleanups to multi-year DeFi histories, all grounded in the same framework as our complete Bitcoin tax guide. A 15-minute call with a crypto tax specialist will tell you which of your positions need attention, or reach out to our team for a full DeFi review.

Not sure your crypto taxes are right?

Talk to a Count On Sheep specialist. We will spot the costly errors before you file. No obligation.

Book My Free Review- Reviewed by Former Big 4 Accountants

- Keep your CPA

- No pressure, no sales pitch

Related Reading

- Selling Bitcoin Taxes: Rates, Basis & Reporting

- Bitcoin Mining Taxes: Hobby vs Business

- Bitcoin ETF Taxes: IBIT, FBTC & Grantor Trusts

- Bitcoin Ordinals & BRC-20 Taxes

- NFT & DeFi Taxes: Liquidity Pools, Staking & Lending

- Per-Wallet Cost Basis: Rev. Proc. 2024-28

- Form 1099-DA Explained

Frequently Asked Questions

Is wrapping Bitcoin into WBTC a taxable event?

The IRS has never answered directly. The conservative position treats BTC to WBTC as a crypto-to-crypto exchange, taxable like any swap. The aggressive position treats it as a non-taxable change of form because your economic exposure to Bitcoin never changes. Most professionals lean conservative; whichever you choose, apply it consistently and document it.

Does the same analysis apply to cbBTC and tBTC?

Broadly yes, with nuance. All wrapped forms present the same unresolved question. Custodial wraps like WBTC and cbBTC involve handing BTC to a custodian and receiving a different token on a different chain, which looks more exchange-like. Threshold's tBTC is trust-minimized, which strengthens the non-disposal argument slightly. None of them have direct IRS guidance.

Is interest earned from lending Bitcoin taxable?

Yes, as ordinary income at fair market value when you receive or gain control of it, whether the platform is CeFi or a DeFi protocol. The income value becomes your basis in the interest coins. This applies to interest paid in BTC, wrapped BTC, or a platform token.

Is borrowing against my Bitcoin taxable?

No. A loan is not income and posting BTC as collateral is not a disposal, provided you retain ownership. This is why borrowing is a popular way to unlock liquidity without selling. The danger is liquidation: if the platform sells your collateral, that sale is your disposal, with full gain recognition at the worst possible moment.

How are Lightning Network payments taxed?

Spending BTC over Lightning is a disposal, exactly like an on-chain spend: gain or loss on the difference between the payment's value and the basis of the sats spent. Opening and closing your own channels is a self-transfer, not a disposal. Routing fees earned by running a node are ordinary income.

Is Babylon-style Bitcoin staking yield taxable?

Yield is ordinary income at fair market value when you gain dominion and control over it, following the staking framework of Rev. Rul. 2023-14. The staking lock itself, where your BTC stays in a self-custodied script, is generally not a disposal. Rewards paid in other tokens are valued at receipt like any other crypto income.

Is bridging Bitcoin between chains taxable?

It depends on what the bridge does. A bridge that locks your asset and issues a wrapped representation raises the same unresolved wrap question. A bridge that swaps your BTC for a different asset on the destination chain looks like an exchange, which is taxable. Know the mechanism before assuming the answer.

What happens to my cost basis when I wrap BTC?

Under the non-taxable position, your original basis and holding period carry into the wrapped token and back out when you unwrap. Under the taxable position, wrapping realizes gain or loss and the wrapped token takes a fresh basis at that day's value. Either way, you must track the lot through every wrap, bridge, and unwrap, per wallet.

Do DeFi platforms report my BTC activity on Form 1099-DA?

Generally no. The rule that would have treated DeFi front-ends as brokers was repealed by Congress in 2025, and wrapping, lending, and staking transactions are temporarily exempt from broker reporting under Notice 2024-57. Custodial platforms still report sales. Less reporting means more record-keeping burden on you, not less tax.

Was my Celsius or BlockFi loss deductible?

CeFi bankruptcy losses are real but the timing and character are messy: losses generally become deductible when they are fixed and determinable, often at plan confirmation or distribution, and recoveries in kind complicate the math. If you have unresolved claims or received partial recoveries, that year's returns deserve professional review.

Is unwrapping WBTC back to BTC taxable?

It mirrors the wrap. Under the conservative view, unwrapping is a second exchange: you dispose of WBTC and realize gain or loss against its basis. Under the aggressive view, nothing happens and your original BTC basis simply continues. Using one view for wrapping and the other for unwrapping is the one clearly wrong answer.

What records do I need for BTC DeFi activity?

Every wrap and unwrap with dates and values, every interest or yield payment at receipt-date value, loan agreements and liquidation notices, Lightning node earnings, and bridge transactions with the mechanism identified. DeFi tax software gets you partway; a manual log of the unusual events fills the gaps that generate notices later.