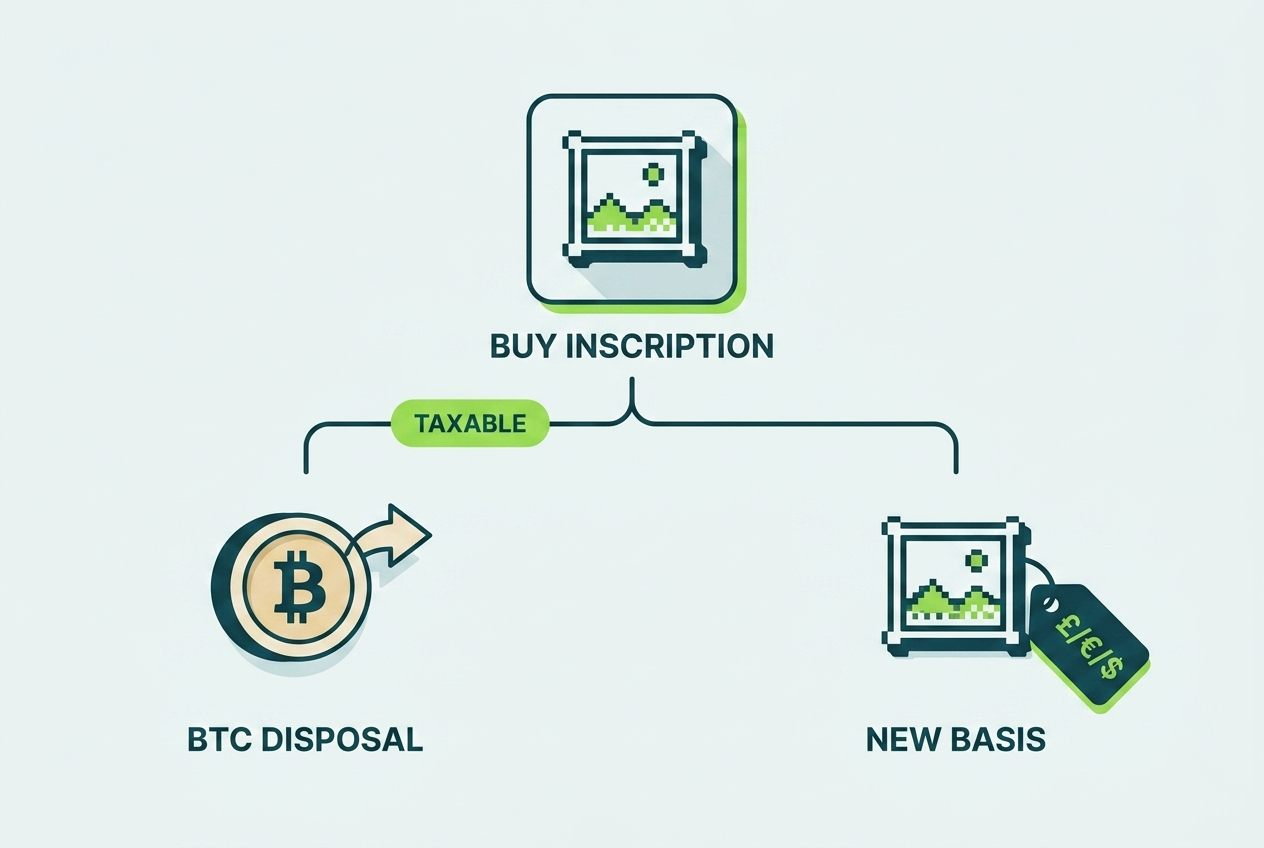

Are Bitcoin Ordinals taxable? Yes. Inscriptions, BRC-20 tokens, and Runes are property, and every purchase, sale, swap, and mint interacts with the same capital gains rules that govern Bitcoin itself. Buying an inscription with BTC is two events at once: a disposal of the BTC you spent and an acquisition of the inscription. Most Ordinals traders have never reported either.

Ordinals turned Bitcoin, the chain famous for doing one thing, into a home for digital artifacts: images inscribed onto individual satoshis, meme tokens minted through BRC-20 and Runes, and a collector market for rare sats mined in Bitcoin’s earliest blocks. Volume on marketplaces like Magic Eden has moved billions of dollars of BTC through trades that no exchange reports and no form summarizes.

That combination, real money and zero reporting infrastructure, makes Ordinals one of the highest-risk blind spots in crypto tax. This guide covers it end to end for 2026: the tax mechanics of inscribing, buying and selling on marketplaces, BRC-20 and Runes activity, rare sat hunting, creator royalties, the unresolved 28% collectibles question, valuing illiquid pieces, spam inscriptions, and the record-keeping that substitutes for the forms marketplaces do not send. It is one piece of our full Bitcoin tax guide, alongside our guides to selling Bitcoin, Bitcoin mining, Bitcoin ETFs, and wrapped Bitcoin and DeFi.

Disclaimer: This guide is for informational purposes only and is not tax or legal advice. Cryptocurrency rules change quickly. Always consult a qualified CPA about your specific situation.

Ordinals in Sixty Seconds, for Tax Purposes

A quick map of the asset types, because each one gets slightly different treatment.

Inscriptions attach data (an image, text, video, or code) to an individual satoshi, the smallest unit of Bitcoin. The inscribed sat becomes a unique digital artifact that can be held, transferred, and sold, functionally an NFT living directly on Bitcoin. Ownership moves through ordinary Bitcoin transactions.

BRC-20 tokens are fungible tokens built by convention on top of inscriptions: a deploy inscription defines the token, mint inscriptions create supply, and transfer inscriptions move it. ORDI and SATS made the format famous. It is inefficient and it clogs the chain, and it moved billions of dollars anyway.

Runes are the cleaner fungible token protocol launched at the 2024 halving, encoding token operations in Bitcoin transactions directly rather than through inscription workarounds.

Rare sats are ordinary satoshis that collectors prize because of their position in Bitcoin’s history: the first sat of a block, sats from early blocks, sats with notable ordinal numbers. The Ordinals numbering scheme made them identifiable, and a market prices them above face value.

For tax purposes, all four are property. There is no Ordinals-specific IRS guidance, so general digital asset principles apply: disposals trigger gains and losses, receipts of value trigger income, and basis tracks what you paid. The interesting questions are in the details, so let’s take them in order of how people actually encounter them.

Inscribing: What Creating an Ordinal Costs You

Creating an inscription means paying Bitcoin network fees (and usually a service fee to an inscription tool) to attach your data to sats you control. Two tax consequences follow, one obvious and one that surprises people.

The surprise first: paying fees in BTC is a disposal of that BTC. If you spend 0.001 BTC on inscription fees, you disposed of 0.001 BTC at its fair market value that day, realizing a small gain or loss against its basis. Heavy inscribers generate hundreds of these micro-disposals. They are individually trivial and collectively reportable, exactly like the fee treatment covered in our guide to selling Bitcoin.

The main event: the inscription itself is generally not income when you create it. You did not receive property from someone else; you made property out of sats you already owned plus fees you paid. Its cost basis is what creation cost you: the basis of the inscribed sats plus the dollar value of the fees at the time. If you later sell the inscription, gain or loss is measured against that basis, with the holding period question for the inscribed artifact typically starting at creation.

Inscribing and Flipping a 10k Collection Piece

You inscribe an image onto sats using 0.0008 BTC in fees when BTC trades at $75,000, so $60 of fees. That BTC had a basis of $42, so the fee payment itself realizes an $18 gain. Your inscription’s basis is roughly $60 plus the negligible basis of the inscribed sat. Three months later the collection catches a bid and you sell for 0.025 BTC, worth $2,000 in that moment. You realize a $1,940 short-term capital gain on the inscription, and you now hold 0.025 BTC with a $2,000 basis. Three assets touched, two gains realized, one log entry that took ninety seconds to write down.

Buying and Selling on Marketplaces

Marketplace trading is where most Ordinals tax events happen, and every trade has two halves.

Buying an inscription with BTC is a disposal of the BTC at fair market value plus an acquisition of the inscription at that same value. If the BTC you spent had appreciated since you acquired it, the purchase itself realizes a gain, before the inscription ever moves in price. This is the mechanic that catches almost everyone: people think of buying as a non-event, but paying with appreciated property never is.

Selling an inscription for BTC disposes of the inscription (gain or loss against its basis) and acquires BTC with a fresh basis equal to its value at receipt. That new BTC lot then lives under the normal per-wallet tracking rules.

Trading inscription for inscription disposes of both: each side realizes gain or loss on what they gave up, measured by the value of what they received.

Marketplace fees and network fees on a sale reduce proceeds; fees on a purchase add to basis. Magic Eden, the dominant ordinals venue, operates non-custodially through partially signed Bitcoin transactions, which matters for reporting (covered below) but changes nothing about the tax events themselves.

BRC-20 and Runes: Fungible Token Taxes on Bitcoin

The meme token economy on Bitcoin runs through mints, trades, and transfers, and each maps onto familiar tax territory.

Minting. Paying fees to mint a BRC-20 token or a Rune during an open mint is best understood as creating property at a cost. Your basis is the fees paid (valued in dollars at the time), and the fee payment in BTC is itself a micro-disposal. Under this view there is no income at mint, which fits mints where you paid roughly what the tokens were worth or where no market existed yet. The aggressive fact pattern is different: minting tokens that instantly trade for far more than the fees paid starts to resemble receiving value, and a conservative filer with large profitable mints should discuss income-at-receipt treatment with a crypto tax professional. The uncertainty is real and the dollar amounts in 2023 to 2024 BRC-20 season were not small.

Trading. Selling BRC-20 tokens or Runes for BTC, or swapping between tokens, is ordinary capital gain and loss mechanics: proceeds minus basis, short-term or long-term by holding period. Most BRC-20 activity is rapid-fire, so expect short-term treatment at ordinary rates.

Receiving. Tokens received as payment, rewards, or airdrops are ordinary income at fair market value on receipt, the same dominion and control analysis that governs all crypto income. The income value becomes basis.

Transfer inscriptions. Moving BRC-20 tokens requires inscribing transfer operations, which cost BTC fees: more micro-disposals, and for transfers between your own wallets, add the fee to your cost records rather than expecting software to catch it.

Runes simplify the mechanics but not the taxes. Etch, mint, trade, receive: same framework, same answers.

Rare Sats: Taxes on Digital Numismatics

Sat hunting, the practice of identifying and extracting collectible satoshis, produces some genuinely novel tax questions with reassuringly boring answers.

Finding a rare sat is not a taxable event. If a sat from block 9 has been sitting in your UTXO since a withdrawal years ago, discovering its significance changes its market value, not your tax position. No disposal, no receipt, no income. Its basis remains the sliver of your original purchase price attributable to it.

Extracting and isolating the sat through carefully constructed transactions is self-transfer plus fees: not taxable beyond the usual fee micro-disposals, but document the lineage, because you will need to show which basis lot that sat came from when you sell.

Selling the rare sat is where tax lands. A collector pays a premium far above face value; nearly the entire sale price is capital gain over a tiny basis. Holding period runs from when you originally acquired the underlying BTC, which for old UTXOs means comfortably long-term.

Buying rare sats works like any inscription purchase: BTC disposal on the spend, new basis in the collectible sat.

The unresolved question is whether a rare sat is still just Bitcoin (plain capital gains) or a collectible (potentially the 28% rate discussed next). A sat prized purely for its numeric position has a decent argument that it is simply Bitcoin with provenance; an inscribed artifact is a harder case. Nobody has authoritative answers yet, which is itself worth knowing before you build a position.

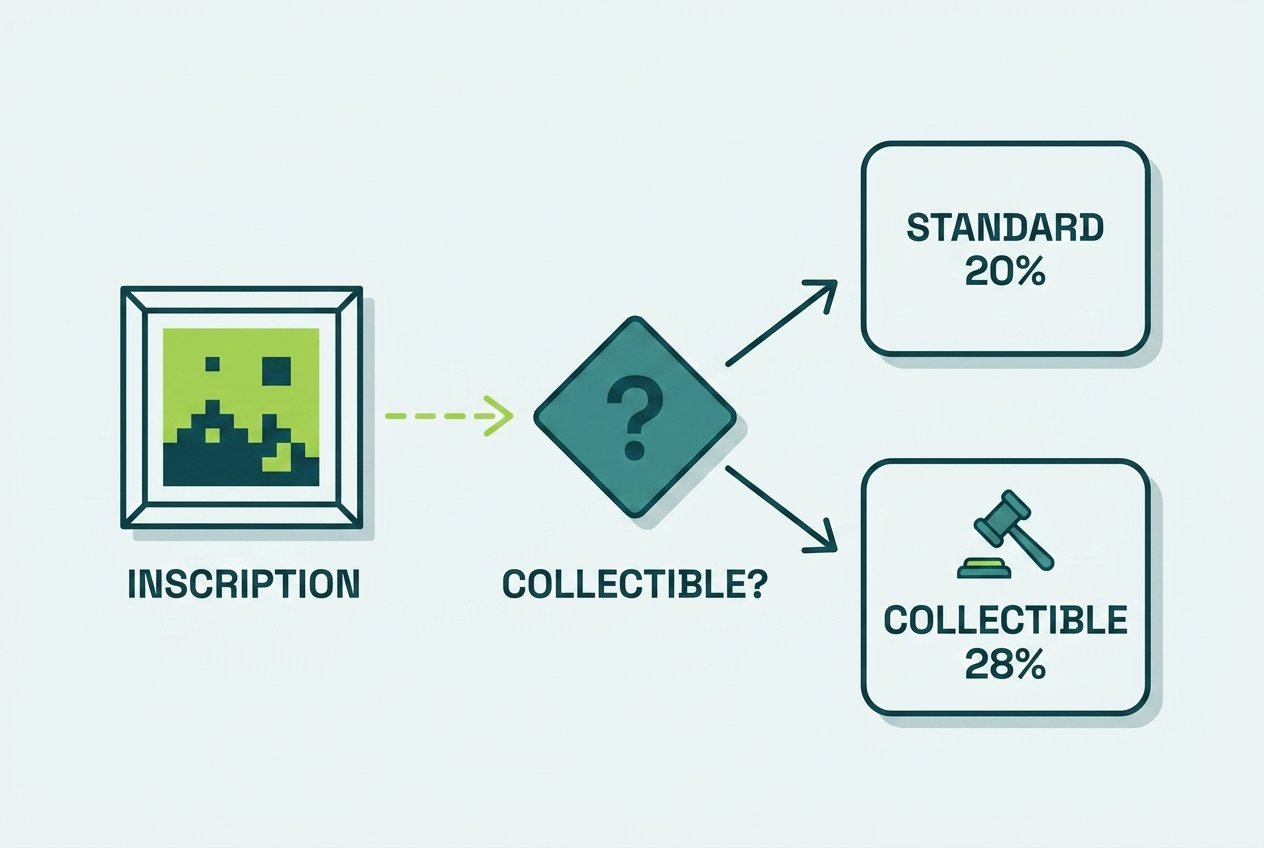

The Collectibles Question: Is Your Inscription Taxed at 28%?

Long-term capital gains normally top out at 20%. Collectibles (art, antiques, gems, stamps, coins) are carved out under Section 408(m) and taxed at up to 28% when held over a year. Where do Ordinals fall?

The only guidance is IRS Notice 2023-27, issued for NFTs generally, which announced a look-through analysis: an NFT is a collectible if the right or asset it represents is itself a collectible. An NFT certifying ownership of a physical painting: collectible. An NFT representing virtual land or a game item: probably not.

Inscriptions complicate the frame because there is no “represented asset” at all; the artifact is the on-chain data. A reasonable reading says an image inscription functioning as digital art looks like “a work of art” under the look-through, pulling it toward 28%. An equally reasonable reading says the statute’s collectibles list contemplates physical objects and tangible-asset certificates, and a pure data artifact falls outside it. The IRS requested comments in 2023 and, as of this writing, has not finalized guidance, has not addressed Ordinals by name, and has not litigated the question.

Practical posture while the fog lasts:

- Short-term traders can ignore it. The collectibles rate only touches long-term gains, and most Ordinals activity is short-term anyway.

- Long-term holders of art-like inscriptions should plan for 28% as the ceiling. If your position only works at 20%, it does not work.

- Take a documented position. Whichever treatment you file, note the reasoning and apply it consistently across years. Inconsistency is worse than either answer.

- Watch for guidance. A final rule could arrive any year and reshape holding decisions for six-figure collections. This is squarely a question worth twenty minutes with a crypto tax specialist if the dollars are meaningful.

Creator Income: Royalties, Mints, and the Business Line

Ordinals creators earn in two ways, and both are ordinary income, not capital gains.

Primary sales. Revenue from minting out a collection is income at fair market value when received, whether collected in BTC or anything else. This is payment for creating, the same as any artist selling work.

Royalties. Ongoing percentages of secondary sales, where marketplaces honor them, are ordinary income at the value of each payment when it arrives. Each BTC royalty payment also establishes a new basis lot for the BTC received, which you will need when that BTC is eventually spent or sold.

The classification question is hobby versus business. A creator who ships collections regularly, markets them, and operates for profit is running a trade or business: income goes on Schedule C, self-employment tax of 15.3% applies, and expenses become deductible (inscription fees, design tools, commissioned art, marketplace costs). A one-off experiment stays hobby income: reportable, no self-employment tax, and no deductions. The dividing line follows the same factors we cover for miners in our Bitcoin mining tax guide, where the hobby-business distinction does the same heavy lifting. Creators earning real money should settle the classification with a crypto tax specialist before filing season, because the answer changes the forms, the tax, and the deductions all at once.

Valuing Illiquid Inscriptions

Fungible tokens have price feeds. A 1-of-1 inscription in a thin collection does not, and valuation questions show up at three moments: when you receive one as income, when you trade one for another, and when you claim a loss.

The hierarchy of evidence, best to weakest:

- Your actual transaction price. An arm’s length sale is the definition of fair market value. Most events price themselves.

- Collection floor price at the relevant time, for pieces near the floor. Screenshot it; marketplaces do not archive floors for you.

- Recent comparable sales of similar pieces (same collection, similar traits), adjusted with judgment.

- Documented good-faith estimate for genuinely unique pieces, built from whatever evidence exists: offers received, trait rarity, creator sales history.

Consistency and documentation carry more weight than precision. What fails is opportunism: valuing a piece high when claiming income basis and low when reporting a trade. Use one method, keep the evidence, and apply it the same way every time.

Spam Inscriptions and Dust

Ordinals inherited crypto’s spam problem with a Bitcoin twist. Unsolicited inscriptions and dust-level sats arrive in active wallets, and the analysis mirrors spam tokens elsewhere: worthless junk pushed to your wallet is not meaningful income. Fair market value of nothing is nothing.

The Bitcoin-specific danger is operational, not tax: careless wallet management can accidentally spend inscribed sats as fees or change, destroying an artifact or merging it into an exchange deposit. Use ordinals-aware wallets that isolate inscribed UTXOs, and never sweep a collector wallet with a standard Bitcoin wallet tool. If a pushed inscription turns out to carry real value, the conservative position is income at that value once you exercise control, the same dominion and control logic that governs airdrops.

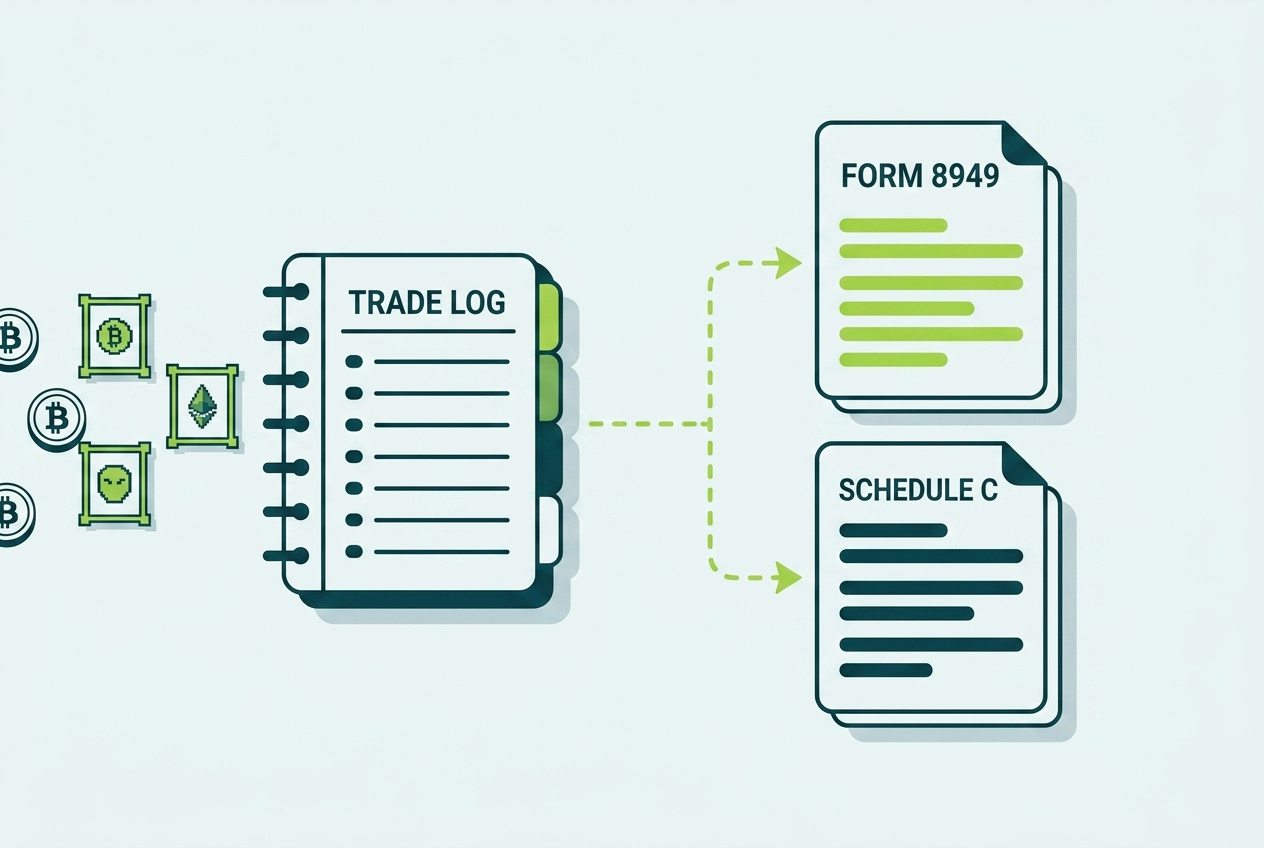

Reporting and Record-Keeping: You Are the Infrastructure

Here is the uncomfortable structural fact about Ordinals taxes: almost nothing reports for you.

Form 1099-DA now covers custodial brokers, and basis reporting is phasing in for assets bought and sold on the same platform starting in 2026. But most Ordinals volume runs through non-custodial marketplaces, and reporting rules for non-custodial and DeFi platforms were rolled back in 2025 pending a rework. Meanwhile mainstream tax software, which handles exchange trades well, still struggles to parse inscription transfers, BRC-20 operations, and sat-level provenance out of raw Bitcoin transactions.

No reporting does not mean no visibility. Every inscription trade is a Bitcoin transaction, permanent and public, and the moment proceeds touch an exchange the 1099-DA system sees BTC arriving with no origin story. The gap between what the IRS can see (everything, eventually) and what gets reported to it automatically (nothing) is exactly the shape of a future audit problem.

The fix is a discipline, not a tool:

- Keep a trade log as you go: inscription ID, date, counterpart BTC amount and dollar value, fees, marketplace.

- Track the BTC legs separately. Every purchase spends a lot; every sale creates one. These flow into your normal Bitcoin basis tracking under the per-wallet rules.

- Screenshot valuations (floors, comps) at trade time for anything illiquid.

- Report disposals on Form 8949 and Schedule D, inscriptions and token trades alike, and creator income on Schedule 1 or Schedule C as classification dictates. Our Form 8949 walkthrough covers the mechanics.

- Answer the digital asset question yes.

Ordinals run on the most transparent ledger ever built, through marketplaces that tell the IRS nothing. The chain remembers every trade forever. The only question is whether your records or an examiner’s subpoena reconstructs them first.

Common Ordinals Tax Mistakes

The recurring failures, from cheapest to most expensive.

Ignoring the BTC Leg of Every Trade

Tracking inscription profits while the appreciated BTC funding the trades realizes unreported gains on every purchase. Usually the largest number in the cleanup.

Treating Mints as Free

Minted tokens sold for real money with no basis records and no thought about whether the mint itself was income. Profitable mint seasons deserve professional review, not silence.

No Valuation Evidence

Trades and losses reported at values that cannot be reconstructed because nobody screenshotted a floor price that no longer exists anywhere.

Royalties Accumulating Unlogged

A creator wallet with two years of small BTC payments, each one income at a different price, none recorded. Reconstructing this is possible and miserable.

Assuming No Form Means No Tax

The marketplace sent nothing, so the trader filed nothing. The blockchain preserved everything, and exchange deposits eventually connect the wallets to a name.

Accidentally Spending the Inventory

Not a tax mistake until it is: inscribed sats swept as change, then a claimed loss with no disposal documentation. Wallet hygiene is record hygiene.

Your Ordinals Tax Checklist

- Log every trade with inscription ID, dates, BTC amounts, dollar values, and fees.

- Track the BTC disposal on every purchase, fee, and mint.

- Record basis at creation for everything you inscribe: fees plus inscribed sat basis.

- Classify creator activity as hobby or business, and file Schedule C if it is a business.

- Log each royalty payment at its receipt-date value.

- Screenshot floors and comps for illiquid valuations at trade time.

- Decide your collectibles position for long-term art-like holdings, and document the reasoning.

- Preserve rare sat lineage from original acquisition through extraction to sale.

- Sell, do not abandon, worthless inscriptions when harvesting losses.

- Report all disposals on Form 8949 and answer the digital asset question yes.

Bottom Line

Ordinals taxes are ordinary property taxes applied to an ecosystem with no reporting rails. Every inscription trade is two events, every mint and fee is a micro-disposal, creator earnings are ordinary income, and the 28% collectibles question hangs unresolved over long-term art holdings. None of it is exotic law. All of it is invisible to the systems that normally do taxpayers’ record-keeping for them, which is why Ordinals traders are so consistently unprepared at filing time.

If you traded through the BRC-20 mania, minted Runes, or built an inscription collection with nothing but a wallet full of transactions to show for it, the reconstruction is very doable: the chain kept perfect records even if nobody else did. Count On Sheep untangles inscription trades, values the illiquid pieces, sorts creator income from capital gains, and delivers CPA-ready numbers, all grounded in the same framework as our complete Bitcoin tax guide. A 15-minute call with a crypto tax specialist will size the project quickly, or reach out to our team for a full Ordinals review.

Not sure your crypto taxes are right?

Talk to a Count On Sheep specialist. We will spot the costly errors before you file. No obligation.

Book My Free Review- Reviewed by Former Big 4 Accountants

- Keep your CPA

- No pressure, no sales pitch

Related Reading

- Selling Bitcoin Taxes: Rates, Basis & Reporting

- Bitcoin Mining Taxes: Hobby vs Business

- Bitcoin ETF Taxes: IBIT, FBTC & Grantor Trusts

- Wrapped Bitcoin & BTC DeFi Taxes

- NFT & DeFi Taxes: Liquidity Pools, Staking & Lending

- Form 1099-DA Explained

- How to File Crypto Taxes: Form 8949 & Schedule D

Frequently Asked Questions

Are Bitcoin Ordinals taxable?

Yes. Inscriptions are property, like other digital assets. Buying one with BTC is a disposal of the BTC you spent, selling one is a disposal of the inscription, and trading one for another is a disposal of both sides. Each event produces a capital gain or loss measured against your cost basis.

Is inscribing an ordinal a taxable event?

Creating an inscription on sats you already own is generally not income; you made property, not received it. But the BTC you spend on inscription and network fees is a disposal of that BTC at fair market value, which produces a small gain or loss. Your fees and the inscribed sats' basis form the inscription's cost basis.

How are BRC-20 mints taxed?

The dominant view treats a BRC-20 mint like creating property: the fees you paid become your basis, and no income arises at mint if you paid to create tokens with no established market. Once the token trades, selling or swapping it is a normal capital gain or loss. A minority view treats valuable mints as income at receipt; get advice if your mints were large.

Do Ordinals qualify for the 28% collectibles tax rate?

Possibly. IRS Notice 2023-27 applies a look-through analysis: an NFT is a collectible if the asset it represents is a collectible, such as a work of art. Many image inscriptions resemble digital art, so the 28% long-term rate is a live risk, but the IRS has not issued final guidance and has not addressed Ordinals specifically.

How are creator royalties on Ordinals taxed?

As ordinary income at fair market value when received, like any payment for your creative work. Consistent creator activity is generally a trade or business, reported on Schedule C with self-employment tax, but with deductions for inscription fees, tools, and other costs. Hobbyist creators report the income without the deductions.

Are rare sats taxable when I find them?

Identifying a rare sat already in your wallet is not a taxable event; nothing new was received and no disposal occurred. The sat keeps the basis of the BTC it came from. Tax hits when you sell the rare sat, and the premium a collector pays above face value is capital gain over that small basis.

How do I value an illiquid inscription?

Use the best available evidence: the actual price paid in your transaction, floor prices for the collection at the relevant time, recent comparable sales, or marketplace listings. Document the source and apply it consistently. For a genuinely unique piece with no comparables, a documented good-faith estimate is the standard.

Do Ordinals marketplaces like Magic Eden send tax forms?

Generally no, at least not yet. Most ordinals trading happens through non-custodial marketplaces that do not currently issue Form 1099-DA, and the IRS paused reporting rules for non-custodial platforms. No form does not mean no tax; every trade is still reportable, and the Bitcoin blockchain records all of it permanently.

What about spam or dust inscriptions sent to my wallet?

Unsolicited inscriptions with no real market value are generally not meaningful income, the same analysis as spam tokens on other chains. Do not pay to move or sell them, and be careful with wallet tools that could accidentally spend inscribed sats. If a pushed inscription turns out to have real value, income at that value once you control it is the conservative answer.

Are Runes taxed differently from BRC-20 tokens?

The mechanics differ but the tax logic is the same. Etching or minting Runes costs BTC fees that form basis, trading Runes is a capital gain or loss event, and receiving Runes as payment or reward is ordinary income at fair market value. The protocol change does not change the property framework.

Can I deduct a loss on an inscription that became worthless?

A realized loss requires a disposal. Selling a dead inscription for any amount, even a token sum on an open market, crystallizes the capital loss. Simply holding a worthless inscription deducts nothing, and abandonment deductions for personal investment property are severely limited under current law. Sell to harvest.

What records should I keep for Ordinals trading?

For each inscription: the inscription ID, acquisition transaction, date, BTC amount paid and its dollar value, fees, the sale transaction and proceeds, and marketplace screenshots where relevant. Ordinals tooling in mainstream tax software is immature, so a manual log maintained as you trade is the difference between a clean filing and forensic reconstruction later.