How are Bitcoin ETFs taxed? Spot Bitcoin ETFs like IBIT, FBTC, ARKB, and GBTC are grantor trusts, which means the tax law looks straight through the fund and treats you as owning a fractional pile of Bitcoin. Selling shares is a normal capital gain or loss. But the look-through cuts both ways: when the trust sells Bitcoin to pay its own fees, you are treated as the seller, and those phantom “expense sales” land on your 1099-B every year whether you traded or not.

The spot ETFs launched in January 2024 and became the default Bitcoin exposure for brokerage accounts, IRAs, and advisors almost overnight. IBIT alone became one of the fastest-growing ETFs in history. Millions of investors now hold Bitcoin through a ticker symbol, and most of them assume the tax treatment is identical to a stock fund. It is close, and the differences are exactly where returns go wrong: expense sales nobody computes basis for, wash sale rules that apply to shares but not to coins, a GBTC basis history stretching back a decade, and a futures fund (BITO) taxed under an entirely different regime.

This guide covers Bitcoin ETF taxes end to end for 2026: how grantor trust treatment actually works, the expense-sale mechanics and the tax letters that decode them, ETF versus direct Bitcoin as a tax matter, wash sales, retirement accounts, the GBTC conversion and Mini Trust spin-off, and how futures ETFs differ. It is one piece of our complete Bitcoin tax guide, alongside our guides to Bitcoin mining taxes, selling Bitcoin, Ordinals and BRC-20 tokens, and wrapped Bitcoin in DeFi.

Disclaimer: This guide is for informational purposes only and is not tax or legal advice. Cryptocurrency rules change quickly. Always consult a qualified CPA about your specific situation.

The Grantor Trust: Why You Own Bitcoin Whether You Know It or Not

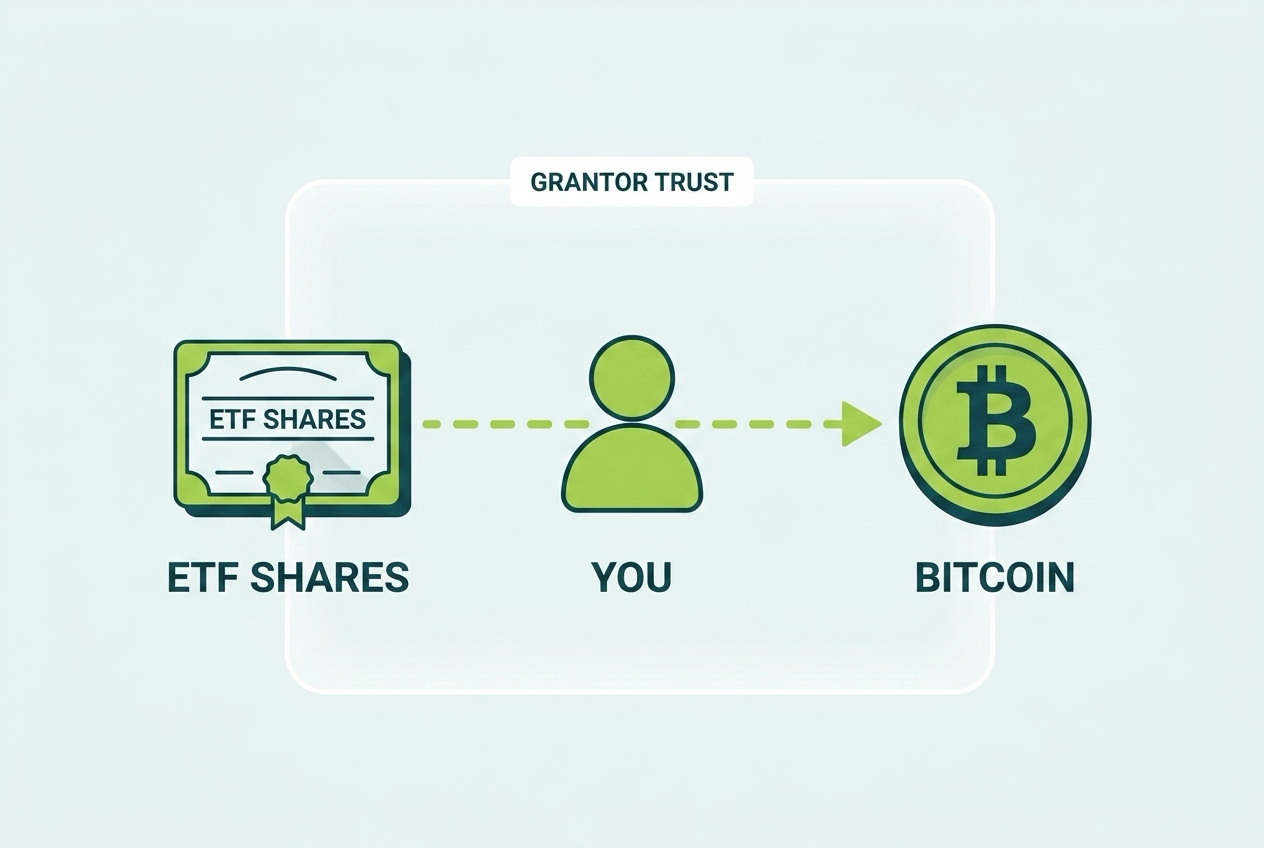

Every major spot Bitcoin ETF (IBIT, FBTC, ARKB, GBTC, BITB, HODL, and the rest) is organized as a grantor trust, not as a regulated investment company like a normal stock fund. The distinction sounds like plumbing, and it drives everything in this guide.

A grantor trust is transparent for tax purposes. The IRS does not see a fund that owns Bitcoin and shareholders who own the fund. It sees you, directly owning a pro rata share of every satoshi in the trust, with the trust as a disregarded wrapper. Your shares are just the receipt.

Three consequences fall out of the look-through:

Selling shares is selling Bitcoin. Your gain or loss is proceeds minus basis, short-term at ordinary rates if held a year or less, long-term at 0%, 15%, or 20% if held longer, plus the 3.8% net investment income tax for high earners. Functionally identical to a stock sale, and your broker reports it on Form 1099-B with basis, since ETF shares are securities in the traditional reporting system rather than the new Form 1099-DA digital asset system.

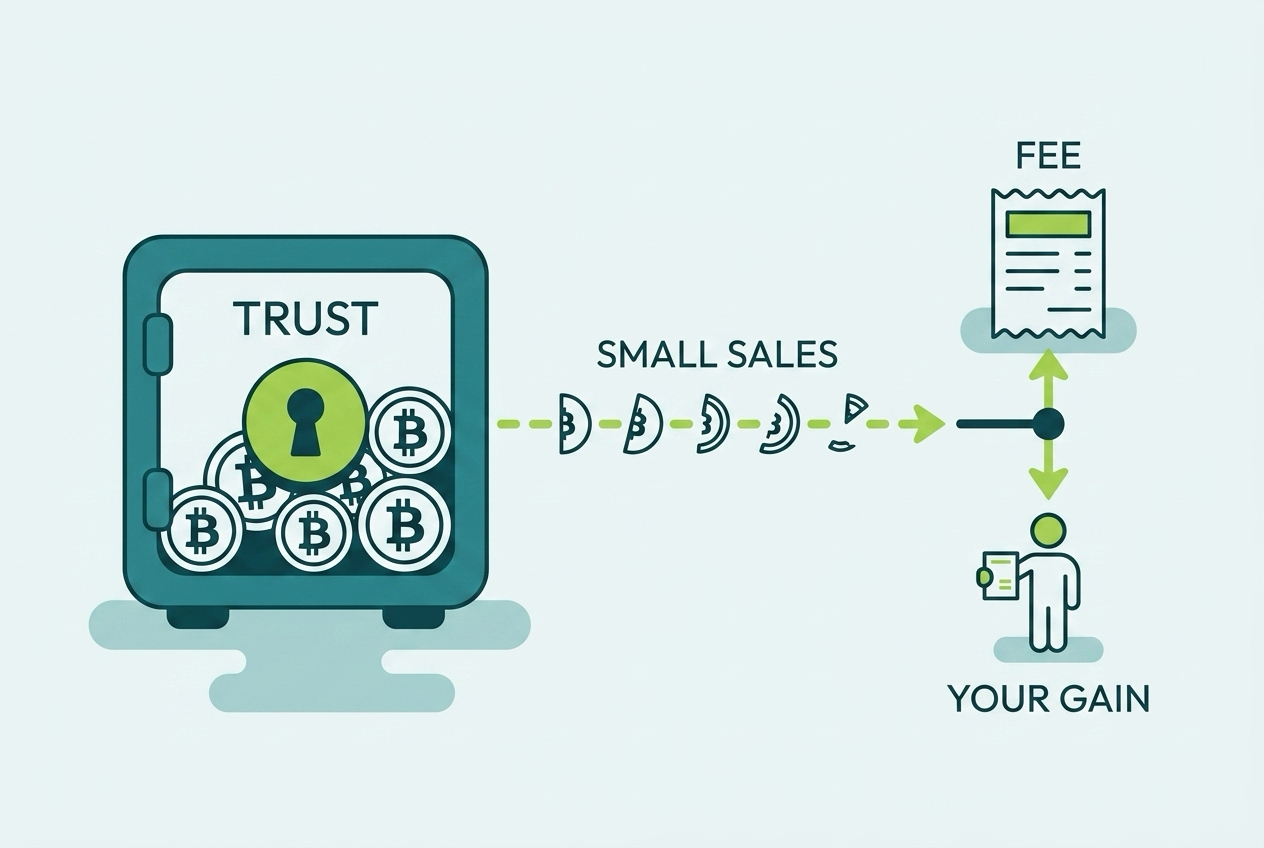

The trust’s actions are your actions. When the trust disposes of Bitcoin, each shareholder is treated as having sold their fractional slice of it. This is the source of the expense-sale phenomenon covered next.

No distributions, no dividend tax. Spot trusts do not pay dividends; Bitcoin generates no income to distribute. Aside from expense sales, nothing happens tax-wise until you sell. That makes spot ETFs surprisingly tax-efficient for buy-and-hold investors, more so than BITO and its distribution firehose, as we cover below.

Phantom Expense Sales: The Gains You Never Ordered

Here is the part that surprises almost every spot ETF holder at tax time.

The trust has to pay its sponsor fee (0.25% annually for IBIT and FBTC, 0.21% for ARKB, 1.50% for GBTC). Bitcoin does not throw off cash, so the trust raises it the only way it can: it sells a little Bitcoin, typically in small monthly increments. Under grantor trust rules, each of those sales is attributed to you in proportion to your holdings. You are deemed to have sold a microscopic amount of Bitcoin every month, at that month’s price, against your own basis.

The practical fallout:

- Your 1099-B grows line items. Brokers report the proceeds from each expense sale, so a holder who never traded can see twelve or more small sale rows per fund. The dollar amounts are usually tiny (a fee of 0.25% means roughly a quarter of one percent of your position value flows through per year, spread across months).

- Basis is your problem. Brokers often report the proceeds with basis blank, because your allocable basis depends on when and at what price you bought. Each sponsor publishes a grantor trust tax information letter early in the year (BlackRock, Fidelity, Grayscale, and Ark all post them) with per-share tables of Bitcoin quantities sold and proceeds. You, your software, or your CPA use the tables to compute gain or loss on each expense sale.

- The amounts are small; the mismatch risk is not. Reporting nothing while your broker reported proceeds creates an automated mismatch. Reporting proceeds with zero basis overstates gain. The correct answer is a small, calculated number, and it is worth the twenty minutes.

- Your basis quietly shrinks. Each expense sale reduces both your Bitcoin-per-share and your remaining basis. Over years, the trust’s Bitcoin per share declines (this is how the fee is actually extracted), and your eventual sale computes against a slightly reduced basis. The tax letters handle this if followed consistently from your first year.

The Holder Who Never Sold

Elena buys $50,000 of IBIT in January and holds all year. The trust sells Bitcoin monthly for its 0.25% fee, so roughly $125 of proceeds flow through to her across twelve small deemed sales. Her allocable basis against those proceeds is close to, but not exactly, $125; in a year where Bitcoin rose after her purchase, she nets perhaps $20 to $40 of gain. The tax owed is trivial. The filing obligation, and the broker mismatch if she ignores it, is not.

Worth flagging while planning: expense sales in a rising market are nearly always gains, because the trust sells at prices above the basis of long-held lots. There is no election to make them go away in a taxable account. The only environments where they vanish are retirement accounts, covered below.

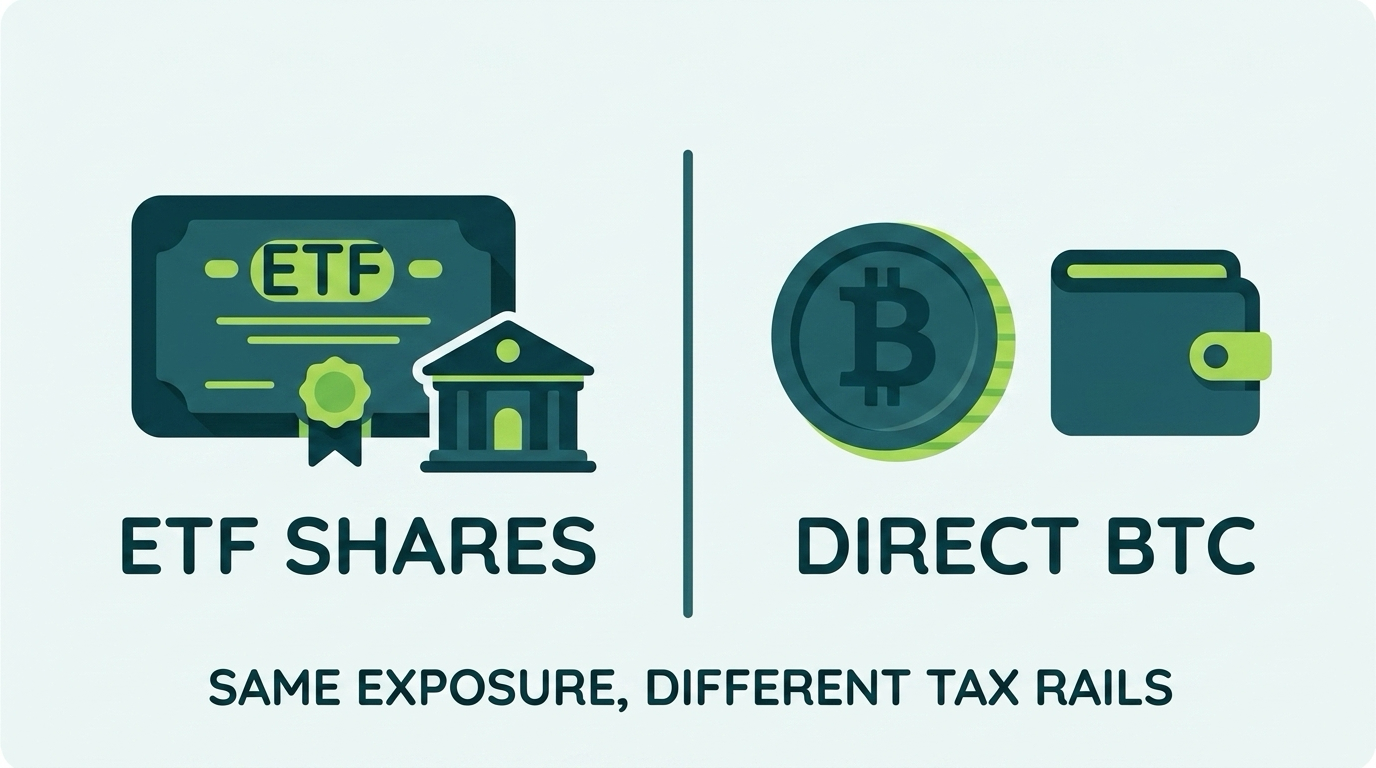

ETF vs Direct Bitcoin: The Honest Tax Comparison

Both routes give you Bitcoin price exposure. Tax-wise they live in different worlds, and the comparison is worth making explicitly.

Where the ETF wins:

- Reporting simplicity. One broker, one 1099-B, basis usually tracked for you. No wallet forensics, no wallet-by-wallet basis tracking under Rev. Proc. 2024-28, no reconciling a 1099-DA that has proceeds but no basis.

- Retirement account access. Buying spot Bitcoin in an IRA requires a specialty custodian; buying IBIT in an IRA takes one click. For tax-sheltered Bitcoin exposure, the ETF is the practical route.

- Estate and advisor logistics. Shares sit in brokerage accounts with beneficiary designations, step-up mechanics, and margin eligibility that the traditional system already handles well.

Where direct Bitcoin wins:

- No wash sale rule, for now. Directly held Bitcoin is property, not a security, so today you can sell at a loss and rebuy immediately, a harvesting flexibility we cover in depth here. ETF shares do not get that latitude.

- No fee drag or phantom sales. Self-custodied Bitcoin has no sponsor fee eroding your coin count and no deemed sales generating annual line items.

- Utility. You can spend it, collateralize it, move it across borders, and use it in DeFi through wrapped forms. Shares just sit there.

Where it is a wash: rates. Both routes produce the same short-term and long-term capital gains rates, the same NIIT exposure, and the same charitable donation and gifting opportunities (donating appreciated shares or appreciated coins both avoid the gain).

The pattern we see work in practice: long-term holdings in tax-advantaged accounts via ETF, self-custodied coins for utility and loss-harvesting flexibility in taxable accounts, and a deliberate decision (rather than an accident) about which lane new money goes into. If your holdings straddle both worlds, a crypto tax specialist can map the cleanest structure for your bracket and state.

Wash Sales: The Rule That Applies to Shares but Not Coins

The wash sale rule disallows a loss when you sell a security and buy a substantially identical one within 30 days before or after the sale. Its application to Bitcoin exposure splits cleanly down the middle:

Direct Bitcoin: no. The statute covers stock and securities. The IRS classifies Bitcoin as property, and under current law wash sales do not reach it. Congress has proposed closing this repeatedly, so the window deserves monitoring, but it remains open today. Our crypto wash sale guide tracks the state of play.

ETF shares: yes, treat it as applying. ETF shares are securities traded on national exchanges, and brokers apply wash sale tracking to them mechanically. Sell IBIT at a loss, rebuy IBIT within the window, and the loss defers into the replacement shares’ basis. There is a theoretical argument that the grantor trust look-through changes the analysis, and it is not an argument to bet a filing position on: assume the rule applies.

The interesting question is the middle case: sell IBIT at a loss, buy FBTC the same day. Different issuers, different fees, same underlying asset. “Substantially identical” has never been crisply defined, and two trusts holding nothing but Bitcoin sit closer to identical than two S&P 500 funds from different sponsors, which the industry has long treated as safe. Positions run the spectrum:

- Aggressive: different issuer means different security; swap freely.

- Moderate: fund-to-fund swaps are defensible today given no direct guidance, but document the differences (fee, custodian, structure details) and keep sizes reasonable.

- Conservative: wait 31 days, or harvest the ETF loss and hold direct Bitcoin during the window (an asymmetry the property classification makes possible in that direction).

Bitcoin ETFs in IRAs and 401(k)s: Where the Complexity Dies

Everything difficult in the first half of this guide evaporates inside a retirement account, which is precisely why ETFs became the standard way to hold Bitcoin in one.

In a traditional IRA or 401(k), there are no taxable events while the money stays in the account. Expense sales happen and nobody computes them. Trades between funds trigger nothing. Wash sales are irrelevant. Tax arrives only at withdrawal, as ordinary income on the full distribution, which is the standard traditional-account trade: deferral now, ordinary rates later, and the loss of the long-term capital gains rate you would have had in a taxable account.

In a Roth IRA or Roth 401(k), qualified withdrawals are entirely tax-free, making it the most powerful wrapper available for an asset you expect to appreciate dramatically. Every dollar of Bitcoin upside inside a Roth escapes tax permanently.

Spot Bitcoin ETFs cleared the path that direct coins never quite did: IRAs cannot easily hold self-custodied Bitcoin (custody requirements make personal wallet custody of IRA assets a prohibited-transaction minefield, and specialty crypto IRA custodians charge for the privilege). ETF shares are ordinary securities every brokerage IRA can hold. Note that the collectibles prohibition that keeps some assets out of IRAs does not block these trusts; Bitcoin is not a collectible under Section 408(m).

Two planning notes worth the words:

- Asset location matters more with Bitcoin than most assets. High expected growth belongs in a Roth if you have one, because the wrapper converts the largest gains to zero tax. Bonds-in-IRA, growth-in-Roth logic applies to Bitcoin with the dial turned up.

- Traditional accounts convert capital gains into ordinary income. A massive Bitcoin gain in a traditional IRA eventually comes out at ordinary rates, potentially higher than the 15 to 20% long-term rate a taxable account would have paid. For very long horizons the deferral usually still wins, but it is a real trade-off, not a free lunch, and worth modeling with a crypto tax specialist if the numbers are large.

GBTC: A Decade of Basis History in One Ticker

GBTC deserves its own section because its holders carry the most complicated basis stories in the ETF complex.

Grayscale Bitcoin Trust launched in 2013 as a private placement, traded over the counter for years at wild premiums and discounts to its Bitcoin value, and finally uplisted to NYSE Arca as a spot ETF on January 11, 2024 after Grayscale’s court victory over the SEC. The conversion changed where shares trade, not what the trust is: it was a grantor trust before and after, and the conversion was not a taxable event. Holders kept their original basis and holding periods, some dating to 2015.

That continuity has consequences:

- Legacy holders sit on enormous unrealized gains. Shares accumulated at Bitcoin-equivalent prices in the hundreds or low thousands of dollars carry basis to match. Switching to a cheaper fund like IBIT means realizing the entire gain. GBTC’s 1.50% fee is painful, and for many long-term holders it is still cheaper than the tax bill a switch would trigger; that math is worth running per lot rather than assuming.

- The Mini Trust spin-off added a wrinkle. In July 2024, Grayscale moved a slice of GBTC’s Bitcoin into the new Bitcoin Mini Trust (ticker BTC, 0.15% fee) and distributed Mini Trust shares to GBTC holders. The distribution was structured as non-taxable, and holders were required to allocate their GBTC basis between the two positions based on relative fair market values at the distribution. If you held GBTC in July 2024 and your records show full original basis still sitting on the GBTC lots, every subsequent sale of either ticker is being computed wrong.

- Discount-era buyers have unusual lots. Investors who bought GBTC at its steep 2022-2023 discount to net asset value acquired basis in the shares (not the underlying Bitcoin), and the discount’s collapse after conversion produced share-price gains that outran Bitcoin itself. Those are ordinary capital gains, just larger than the coin chart implies.

The GBTC conversion moved billions of dollars of Bitcoin exposure into the ETF era without a single taxable event. The basis histories it carried along are another matter, and they are still generating amended returns two years later.

If your GBTC story includes OTC-era purchases, the discount trade, or the Mini Trust spin-off, the position deserves a lot-by-lot review with a crypto tax specialist before your next sale, not after.

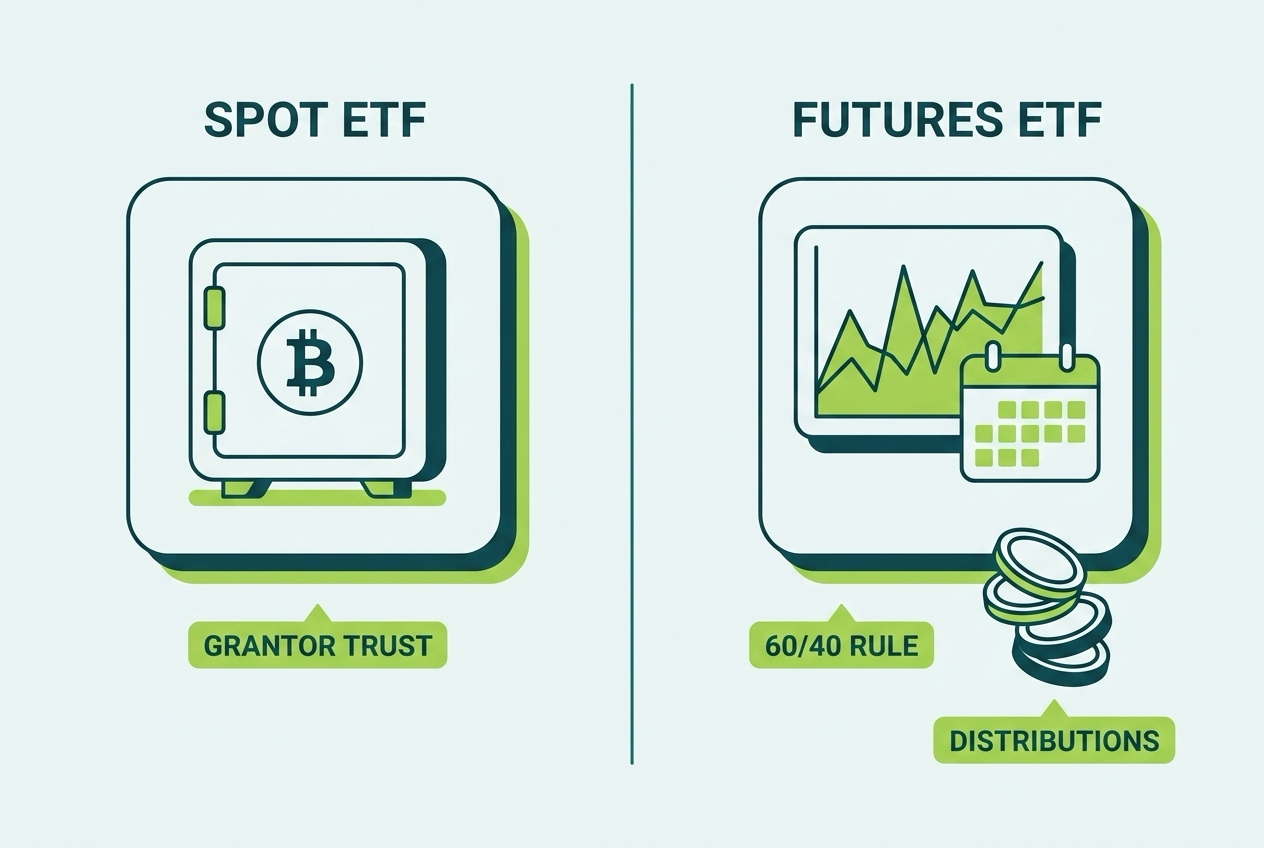

Futures ETFs: BITO and the Section 1256 Track

Before the spot funds existed there was BITO (ProShares Bitcoin Strategy ETF, launched October 2021), and it is still trading, still popular for its enormous distributions, and taxed on a completely different track from everything above.

BITO holds no Bitcoin. It holds CME Bitcoin futures, and it is organized as a regulated investment company (RIC), not a grantor trust. The tax mechanics stack up like this:

- Inside the fund, Section 1256 rules apply. Regulated futures contracts are marked to market at year-end, with gains and losses treated as 60% long-term and 40% short-term regardless of holding period. That blended character exists at the fund level.

- The fund distributes, and you are taxed on distributions. As a RIC, BITO pushes out its income and gains each year, reported to you on a 1099-DIV. BITO’s distributions have frequently been very large relative to its price (rolling futures in volatile markets generates a lot of recognized gain), and substantial portions have been taxed as ordinary income. Holders in taxable accounts get an annual tax bill whether or not they sell.

- Your own shares are just shares. Selling BITO produces normal short-term or long-term capital gain based on your holding period. The 60/40 treatment does not apply to your share sale; it shaped the character of what the fund distributed.

- Performance drag is structural. Rolling futures month after month in a market that usually prices later contracts higher (contango) bleeds returns against spot. No tax treatment repairs that; it is a reason the spot funds displaced BITO for buy-and-hold money within months of launching.

For completeness: investors who trade CME Bitcoin futures directly (not through a fund) get Section 1256 treatment personally, with 60/40 character, mark-to-market at year-end, and a three-year loss carryback election. Active traders sometimes prefer that regime to property treatment on spot coins. It is a specialist’s game, and the wash sale rule does not apply to 1256 contracts, one more wrinkle in an already wrinkled map.

The practical guidance is blunt: for long-term Bitcoin exposure in a taxable account, spot funds dominate BITO on both fee drag and tax deferral. BITO’s niche is income-seeking strategies and options traders, and its holders should expect heavy 1099-DIV activity every single year.

Reporting Bitcoin ETF Activity: Step by Step

Here is the full filing pipeline for a taxable account holding spot Bitcoin ETFs.

- Collect your 1099-B from each broker. Share sales you initiated appear with basis in most cases. Expense-sale proceeds appear as many small rows, often with basis blank.

- Download each fund’s grantor trust tax letter from the sponsor’s website (iShares for IBIT, Fidelity for FBTC, Grayscale for GBTC and the Mini Trust, Ark/21Shares for ARKB).

- Compute expense-sale gain or loss per lot using the letter’s per-share factors and your purchase dates and prices. Tax software with grantor trust support, or your CPA, does this mechanically.

- Report everything on Form 8949 and Schedule D. Your own sales and the expense sales both land there, in the covered or noncovered sections matching the 1099-B. Our Form 8949 guide walks the form itself.

- Check the wash sale column. Brokers flag same-account, same-ticker wash sales, but cross-account and cross-broker repurchases are on you to catch.

- Adjust ongoing basis. Carry the expense-sale basis reductions forward so next year’s calculation starts from the right number.

- Answer the digital asset question correctly. Current form instructions do not require a yes for positions held through ETFs alone; owning IBIT is owning a security. If you also touched actual crypto, answer for that activity on its own merits.

- Roth and IRA holders: skip all of the above. Nothing to report until distributions.

One reconciliation note: if you hold both ETFs and direct Bitcoin, keep the two ledgers clearly separate. The ETF lives in the 1099-B securities world; the coins live in the 1099-DA and wallet-tracking world. Mixing them in one spreadsheet is how basis errors metastasize, and untangling exactly that mess is a large share of what a crypto tax specialist does in the spring.

Common Bitcoin ETF Tax Mistakes

The recurring errors, roughly ordered by frequency:

Ignoring the Expense Sales

The 1099-B shows small proceeds, the taxpayer reports nothing, and the automated matching system notices. The dollars are small; the notice is not fun. Report them with computed basis.

Reporting Expense Sales With Zero Basis

The opposite overcorrection: proceeds reported, basis skipped, tiny sales taxed as 100% gain. The tax letters exist precisely so you do not do this.

Missing the Mini Trust Basis Allocation

GBTC holders from July 2024 selling either GBTC or BTC (Mini Trust) with unallocated basis. Every such sale misstates gain until the allocation is done.

Washing a Loss Through Another Account

Harvesting an IBIT loss in the brokerage account while an automatic investment buys IBIT in the IRA the same week. The loss is disallowed, and in the IRA-repurchase case, permanently destroyed.

Assuming Coin Rules Apply to Shares

Selling ETF shares at a loss and rebuying next day because “crypto has no wash sale rule.” The coins have that latitude; the shares do not.

Holding BITO for the Long Haul by Accident

Buy-and-hold investors sitting in a futures fund, paying ordinary rates on large annual distributions and eating roll drag, when a spot fund matched their intent. Reviewing which wrapper you actually own takes one minute.

Forgetting NIIT

High earners layering ETF gains on top of other investment income and missing the extra 3.8% in their estimates.

Your Bitcoin ETF Tax Checklist

- Inventory every fund and account: spot vs futures, taxable vs retirement.

- Pull the grantor trust tax letter for each spot fund you held during the year.

- Compute expense-sale gains per lot; do not report zero basis or skip them.

- Report sales and expense sales on Form 8949 and Schedule D.

- Sweep all accounts for wash sales before harvesting any ETF loss, IRAs included.

- Allocate GBTC basis to the Mini Trust if you held GBTC in July 2024.

- Confirm BITO holders expect a 1099-DIV with heavily ordinary income distributions.

- Locate new Bitcoin exposure deliberately: Roth for maximum growth shelter, taxable for harvesting flexibility.

- Keep ETF and direct-coin records in separate ledgers with basis tracked in each.

- Run the NIIT math if your income clears the thresholds.

Bottom Line

Bitcoin ETF taxes are stock taxes with three asterisks. The grantor trust look-through makes you a direct Bitcoin owner, which mostly just means capital gains treatment on your sales, and occasionally means computing your share of the trust’s fee-funding Bitcoin sales from a tax letter. Wash sale rules follow the shares even though they do not follow the coins. And the account wrapper matters more than fund selection: inside a Roth, every complexity in this guide disappears along with the tax itself. Where ETFs end and self-custodied coins begin, the full Bitcoin tax picture takes over, with its own set of rules.

If your situation includes unexplained 1099-B line items, a GBTC position with a decade of history, an unallocated Mini Trust spin-off, or a portfolio split between shares and self-custodied coins, the reconciliation is very fixable, and much cheaper to fix before a mismatch notice than after. Count On Sheep handles ETF expense-sale calculations, basis reconstructions, and combined coin-plus-ETF reporting every season. Book 20 minutes with a crypto tax specialist to size your situation, or reach out to our team for a full review.

Not sure your crypto taxes are right?

Talk to a Count On Sheep specialist. We will spot the costly errors before you file. No obligation.

Book My Free Review- Reviewed by Former Big 4 Accountants

- Keep your CPA

- No pressure, no sales pitch

Related Reading

- Bitcoin Mining Taxes: Hobby vs Business & Deductions

- Selling Bitcoin: Capital Gains, Lots & Reporting

- Bitcoin Ordinals & BRC-20 Taxes

- Wrapped Bitcoin & DeFi Taxes

- The Crypto Wash Sale Rule in 2026

- Crypto Tax-Loss Harvesting

- Form 1099-DA Explained

Frequently Asked Questions

How are spot Bitcoin ETFs like IBIT and FBTC taxed?

Spot Bitcoin ETFs are structured as grantor trusts, so the tax law treats you as owning your pro rata slice of the trust's Bitcoin directly. Selling shares is a capital gain or loss, short-term or long-term based on your holding period, exactly like selling a stock. The twist is that the trust's own Bitcoin sales to pay its sponsor fee flow through to you as tiny taxable events even when you sell nothing.

Why does my 1099-B show sales from a Bitcoin ETF I never sold?

Those are the trust's expense sales. Every month the trust sells a small amount of Bitcoin to pay its sponsor fee, and as a grantor trust owner you are treated as having sold your fractional share of that Bitcoin. Your broker reports the proceeds, often as a dozen or more small line items. You compute the gain or loss on each using the fund's grantor trust tax letter, and the amounts are usually tiny.

Do I really have to calculate the expense sale amounts myself?

Often, yes. Brokers report gross proceeds from the trust's expense sales but frequently leave basis blank because the calculation depends on your purchase dates and prices. Each fund publishes a year-end tax information letter with per-share proceeds and Bitcoin quantities that lets you (or your software or CPA) compute your allocable basis. Skipping the calculation and reporting zero basis overstates your gain.

Is the wash sale rule different for Bitcoin ETFs versus actual Bitcoin?

Yes, and it cuts against the ETF. Spot Bitcoin held directly is property, not a security, so the wash sale statute does not currently apply to it. ETF shares trade as securities on a national exchange, and the practical, conservative treatment brokers apply is that wash sale rules do apply to them. Sell IBIT at a loss and rebuy IBIT within 30 days and you should expect the loss to be disallowed.

Can I harvest a loss in IBIT and buy FBTC the same day?

This is a genuine gray area. The wash sale rule blocks repurchasing substantially identical securities, and two grantor trusts holding nothing but Bitcoin are uncomfortably similar even though they are different issuers with different fees. Many advisors treat fund-to-fund swaps as defensible today; conservative ones wait 31 days or switch exposure types. Get advice before doing it in size.

Are Bitcoin ETFs better than direct Bitcoin for taxes?

They trade different problems. ETFs give you clean 1099-B reporting, easy IRA eligibility, and no wallet-level basis tracking, but bring expense-sale phantom gains, wash sale exposure, and fee drag. Direct Bitcoin has no wash sale rule (currently) and full control, but requires wallet-by-wallet basis tracking under Rev. Proc. 2024-28 and lands you in the 1099-DA reporting system. Neither is categorically better; the right answer depends on account type and how actively you trade.

How are Bitcoin ETFs taxed inside an IRA or 401(k)?

They are not, until money comes out. Traditional accounts defer everything: no capital gains on sales, no expense-sale line items to compute, and withdrawals taxed as ordinary income later. Roth accounts eliminate the tax entirely for qualified withdrawals. The grantor trust flow-through and wash sale issues that complicate taxable accounts simply do not exist inside a retirement account, which is why ETFs are the standard way to hold Bitcoin exposure in one.

Was the GBTC conversion to an ETF a taxable event?

No. When GBTC uplisted to NYSE Arca as a spot ETF in January 2024, the trust's legal and tax structure did not change; it remained a grantor trust. Long-time holders kept their original basis and holding period. That is exactly why many early GBTC investors sit on large unrealized gains and face real tax if they switch to a cheaper fund.

What about the Grayscale Mini Trust spin-off?

In July 2024 Grayscale spun off part of GBTC's Bitcoin into the Bitcoin Mini Trust (ticker BTC) and distributed Mini Trust shares to GBTC holders. The distribution was structured as non-taxable, with holders allocating a portion of their GBTC basis to the new shares based on relative values at the spin-off. If you held GBTC then, your basis records need that allocation or every later sale is computed wrong.

How is BITO taxed differently from spot ETFs?

BITO holds Bitcoin futures rather than Bitcoin, and it is a regulated investment company rather than a grantor trust. Inside the fund, futures are Section 1256 contracts, marked to market with 60/40 long-term/short-term treatment. The fund pushes income out as distributions, which have often been large and heavily ordinary income. Your own sale of BITO shares is a normal capital gain or loss, and futures roll costs create performance drag no tax treatment fixes.

Do Bitcoin ETFs show up on Form 1099-DA?

No. ETF shares are traditional securities, so sales are reported on Form 1099-B like any stock, generally with basis tracked by your broker. Form 1099-DA covers direct digital asset sales through crypto brokers. This is one of the ETF route's quiet advantages: you stay inside the mature securities reporting system instead of the new digital asset one.

Does the 3.8% net investment income tax apply to Bitcoin ETF gains?

Yes. Capital gains from ETF shares, the flow-through expense-sale gains, and BITO distributions are all investment income for NIIT purposes. Filers above $200,000 (single) or $250,000 (married filing jointly) modified AGI pay the extra 3.8% on top of capital gains rates.