The wash sale rule does not apply to cryptocurrency in 2026. IRC Section 1091 covers stocks and securities, and the IRS classifies crypto as property under Notice 2014-21. That means you can sell a coin at a loss, buy it back the same day, and still claim the loss on your taxes. There are real caveats, though, and one exception that catches people every year: crypto ETFs.

What is the wash sale rule?

The wash sale rule stops investors from manufacturing tax losses without really changing their position. Under IRC Section 1091, if you sell a stock or security at a loss and buy the same or a substantially identical one within 30 days before or after the sale, the loss is disallowed for that year. Instead, the disallowed loss gets added to the cost basis of the replacement shares.

The window is 61 days in total: 30 days before the sale, the day of the sale, and 30 days after. Inside that window, a repurchase “washes” the loss.

That is the rule for securities. The entire question for crypto investors is whether digital assets count as securities for this purpose. They do not.

Why crypto is exempt from the wash sale rule

The IRS answered the classification question back in Notice 2014-21: cryptocurrency is property for federal tax purposes. Section 1091 applies to “shares of stock or securities.” Property that is not a stock or security sits outside the rule entirely.

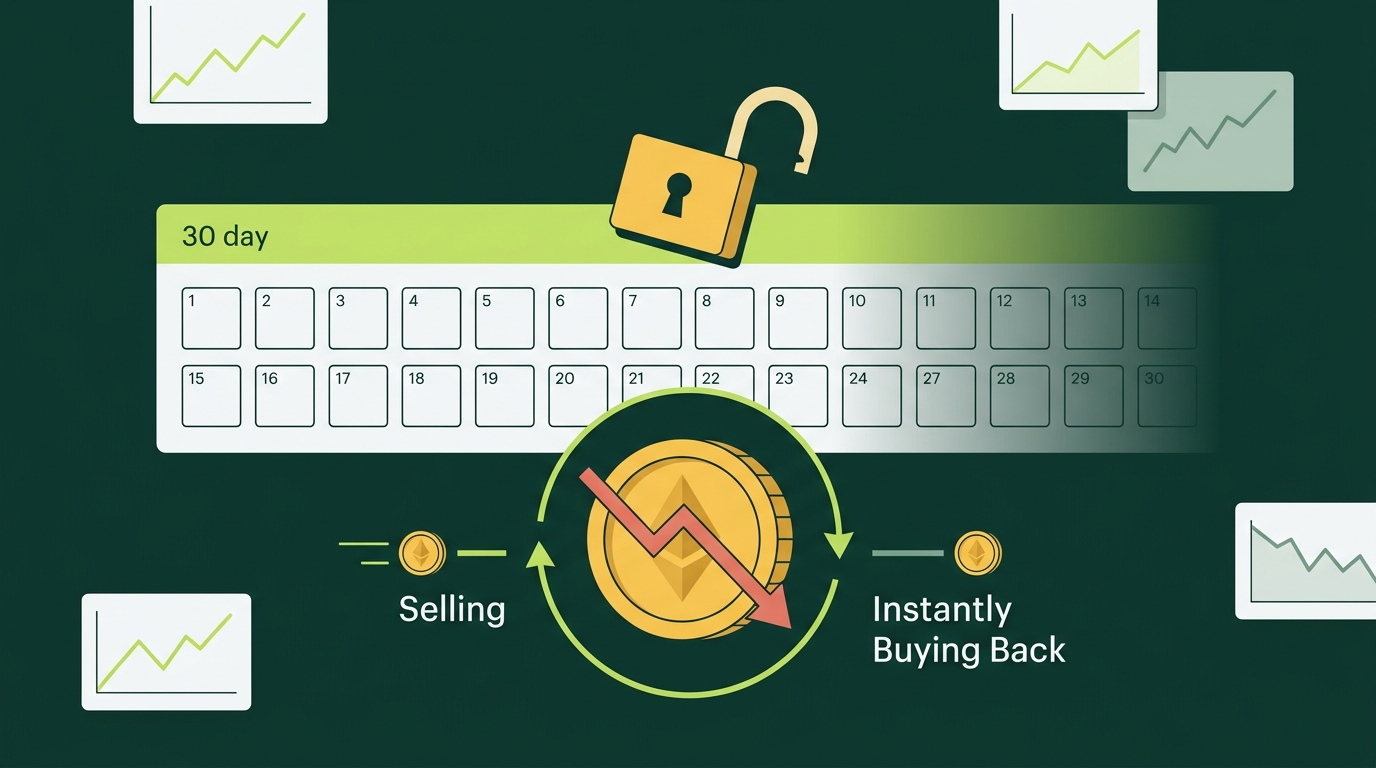

The practical effect is simple. If you sell Bitcoin at a loss today and buy the same amount back five minutes later, the loss is still deductible. There is no 30 day clock to run out. This applies to every directly held crypto asset: Bitcoin, Ethereum, Solana, XRP, memecoins, and stablecoins alike.

How the crypto tax-loss loophole works

Because the rule does not apply, crypto investors can harvest losses aggressively without giving up their position. Here is what that looks like in real dollars.

Harvesting a Bitcoin loss and rebuying same day

You bought 1 BTC at $60,000. The price drops to $40,000. You sell, realize a $20,000 capital loss, and buy 1 BTC back the same afternoon at roughly the same price. You still hold 1 BTC, your new cost basis is $40,000, and the $20,000 loss is available to offset gains.

That harvested loss offsets capital gains from any asset class dollar for dollar. If losses exceed your gains, up to $3,000 per year also offsets ordinary income like salary, and everything left carries forward indefinitely to future years.

One important side effect: rebuying at the lower price resets your cost basis lower and restarts your holding period. If the coin recovers, your future gain is larger, and it starts as short-term. Harvesting defers tax more than it erases tax. For most investors that trade is still clearly worth it, especially against short-term gains taxed at ordinary rates.

For the full playbook on timing, lot selection, and year-end execution, see our guide to crypto tax-loss harvesting in 2026.

The economic substance caveat

The IRS has a general anti-abuse backstop called the economic substance doctrine. A transaction can be disregarded if it exists only on paper and changes nothing about your economic position. A same-second sell and rebuy at an identical price, done purely to book a loss, is the kind of pattern that could theoretically draw that argument.

In practice, clean habits remove most of the risk:

-

Let real market exposure exist between the sale and the repurchase, even a short one.

-

Trade on the open market rather than selling to yourself or a related party.

-

Keep records showing prices moved between the two trades.

-

Consider rotating into a correlated but different asset for a period instead of an instant identical rebuy.

None of this is required by a wash sale statute, because there is none for crypto. It is defensive documentation that makes your loss hard to challenge.

The exception: crypto ETFs are securities

Here is the nuance that trips up investors who hold both coins and funds. Spot Bitcoin and Ethereum ETFs, like IBIT, FBTC, and ETHA, are securities. The wash sale rule fully applies to them.

Sell IBIT at a loss and rebuy it within 30 days, and the loss is disallowed. The same economic trade done in spot Bitcoin would have been fine. Mixing the two can also get murky: swapping between a coin and an ETF that tracks it raises substantially identical questions that the IRS has not clearly answered. If you harvest losses in ETF positions, respect the full 61 day window just as you would with any stock.

If you do trigger a wash sale in a security, the loss is not gone forever. It is added to the basis of the replacement shares, so you recover it when you eventually sell for good.

Does this apply to XRP, Solana, or my specific coin?

Yes, the exemption covers all of them. The wash sale rule currently applies to no cryptocurrency held directly. XRP gets asked about often because of its long-running securities litigation, but for tax loss purposes it is treated like any other digital asset: property, outside Section 1091. The same goes for Solana, Dogecoin, and every other token in your wallet.

How to report harvested crypto losses

Selling at a loss is a disposal like any other, so it goes on your return the standard way:

-

Each loss sale is one line on Form 8949, with dates, proceeds, cost basis, and the loss.

-

Totals flow to Schedule D, where losses net against gains.

-

Up to $3,000 of excess loss offsets ordinary income, and the rest carries forward.

Getting the cost basis right on every lot is what makes the loss stick. Your cost basis method determines which lot you sold and how big the loss actually is, and since the per-wallet rules took effect, lots are tracked wallet by wallet. If you are unsure which of your transactions even count as taxable, start with our breakdown of taxable vs non-taxable crypto events.

Bottom line

Crypto’s wash sale exemption is one of the few tax rules that genuinely favors digital asset investors, and it will not necessarily last. Sell at a loss, rebuy if you want the position, document the trades, report every disposal on Form 8949, and keep ETF positions on the securities side of your brain where the 30 day rule still lives.

If your trading history is spread across exchanges and wallets and you are not sure your losses are provable, that is exactly the reconstruction work we do. The loss only saves you money if the records behind it hold up.

Frequently Asked Questions

Do wash sale rules apply to cryptocurrencies?

No. The wash sale rule under IRC Section 1091 applies to stocks and securities. The IRS classifies cryptocurrency as property, not a security, so you can sell crypto at a loss, repurchase it immediately, and still claim the loss. Congress has proposed changing this, but no change is law as of 2026.

Does the 30 day rule apply to crypto?

Not currently. The 30 day window before and after a sale only matters for securities covered by the wash sale rule. Crypto is classified as property, so there is no required waiting period before rebuying. Many advisors still suggest a short gap or documentation to strengthen your position.

Does the wash sale rule apply to XRP?

No. XRP is treated the same as other cryptocurrencies for this purpose. The wash sale rule does not apply to any crypto asset held directly, including XRP, Bitcoin, Ethereum, and stablecoins.

Do wash sales apply to crypto ETFs?

Yes. Spot Bitcoin and Ethereum ETFs like IBIT and ETHA are securities, so the wash sale rule fully applies to them. Selling an ETF at a loss and rebuying it within 30 days disallows the loss, even though the same trade in the underlying coin would be fine.

What happens if I accidentally trigger a wash sale?

For securities, the disallowed loss is added to the cost basis of the replacement shares, so the loss is deferred rather than destroyed. For directly held crypto there is nothing to trigger in 2026, because the rule does not apply.

What happens if you sell crypto at a loss?

You realize a capital loss. Losses offset capital gains dollar for dollar, then up to $3,000 of ordinary income per year, and any remainder carries forward indefinitely. Every disposal, including loss sales, gets reported on Form 8949.