Are you leaving money on the table every time you sell crypto? Most investors default to FIFO and never think twice, but the cost basis method you choose can mean the difference between a four-figure tax bill and a three-figure one.

Here’s the thing: the IRS doesn’t pick your method for you. You get to choose. And that choice has real dollar consequences.

What Is Cost Basis and Why Does It Matter?

Cost basis is the original value of a crypto asset for tax purposes, typically the purchase price plus any fees. When you sell, swap, or spend crypto, the IRS calculates your taxable gain or loss as proceeds minus cost basis.

A simple example: You bought 1 ETH at $2,000 in January and another 1 ETH at $3,500 in March. You sell 1 ETH in December for $4,000.

Sell the $2,000 ETH

$4,000 - $2,000 = $2,000 gain. FIFO always picks your oldest lot first.

Sell the $3,500 ETH

$4,000 - $3,500 = $500 gain. HIFO picks the most expensive lot, minimizing the gain.

This is why cost basis optimization is the single most impactful lever in your crypto tax strategy. And it’s why the IRS requires you to report it on Form 8949 for every single disposal.

FIFO: The IRS Default

First-In, First-Out means the earliest-acquired units are sold first. It’s the method the IRS uses if you don’t specify anything else.

When FIFO works in your favor:

- You bought most of your holdings during a bull market (high basis)

- You’re selling during a downturn (lower proceeds)

- Your oldest lots already have favorable long-term capital gains treatment

When FIFO hurts:

- Your earliest purchases were at low prices (early adopter problem)

- Markets have appreciated significantly since you started buying

- You’re triggering large short-term gains unnecessarily

Most crypto tax software defaults to FIFO. That’s fine. It’s the safest choice. But “safe” and “optimal” are not the same thing.

Switching from FIFO to HIFO can result in significant tax savings because HIFO allows you to sell the highest-cost assets first, which generally reduces your taxable capital gains.

HIFO: Minimize Your Tax Bill

Highest-In, First-Out means the most expensive lots are sold first. This minimizes your gain (or maximizes your loss) on every disposal.

HIFO is powerful because:

- It defers gains by always selling the highest-cost units first

- It’s fully compliant with IRS rules (as part of Specific Identification)

- It can dramatically reduce your current-year tax liability

But here’s where it gets interesting. HIFO isn’t a standalone IRS-recognized method. It’s a strategy within Specific Identification. You need to be able to identify exactly which lot you’re selling at the time of the sale.

How to Properly Elect HIFO

- Maintain detailed records of every lot (date, amount, price, fees)

- Identify the specific lot before or at the time of sale

- Document your selection: your crypto tax reconciliation report should show lot-level detail

- Keep broker confirmations or on-chain transaction records as backup

Specific Identification: Maximum Control

Specific Identification (Spec ID) lets you cherry-pick exactly which lots to sell for each transaction. It’s the most flexible method, and the most demanding.

With Spec ID, you can:

- Choose HIFO lots to minimize gains during profitable sales

- Choose LIFO (last-in, first-out) lots to reduce taxable gains or increase losses

- Optimize for long-term vs. short-term capital gains treatment

- Combine strategies across different assets in your portfolio

If you elect to use the specific identification method, you must identify the specific units of property that were sold, exchanged, or otherwise disposed of.

The Documentation Requirement

The IRS is clear: Spec ID requires adequate identification. You must specify the particular units being sold and receive confirmation from your broker or exchange. For crypto, this means:

- Centralized exchanges: Some (like Coinbase) now support lot selection. Check your exchange’s tax settings.

- DeFi transactions: On-chain activity doesn’t have a “lot selector.” You’ll need to reconstruct lot identification using transaction hashes, timestamps, and wallet records.

- Cross-chain transfers: Moving assets between wallets doesn’t change your basis, but you need to track the chain of custody.

How to Model the Right Method for Your Portfolio

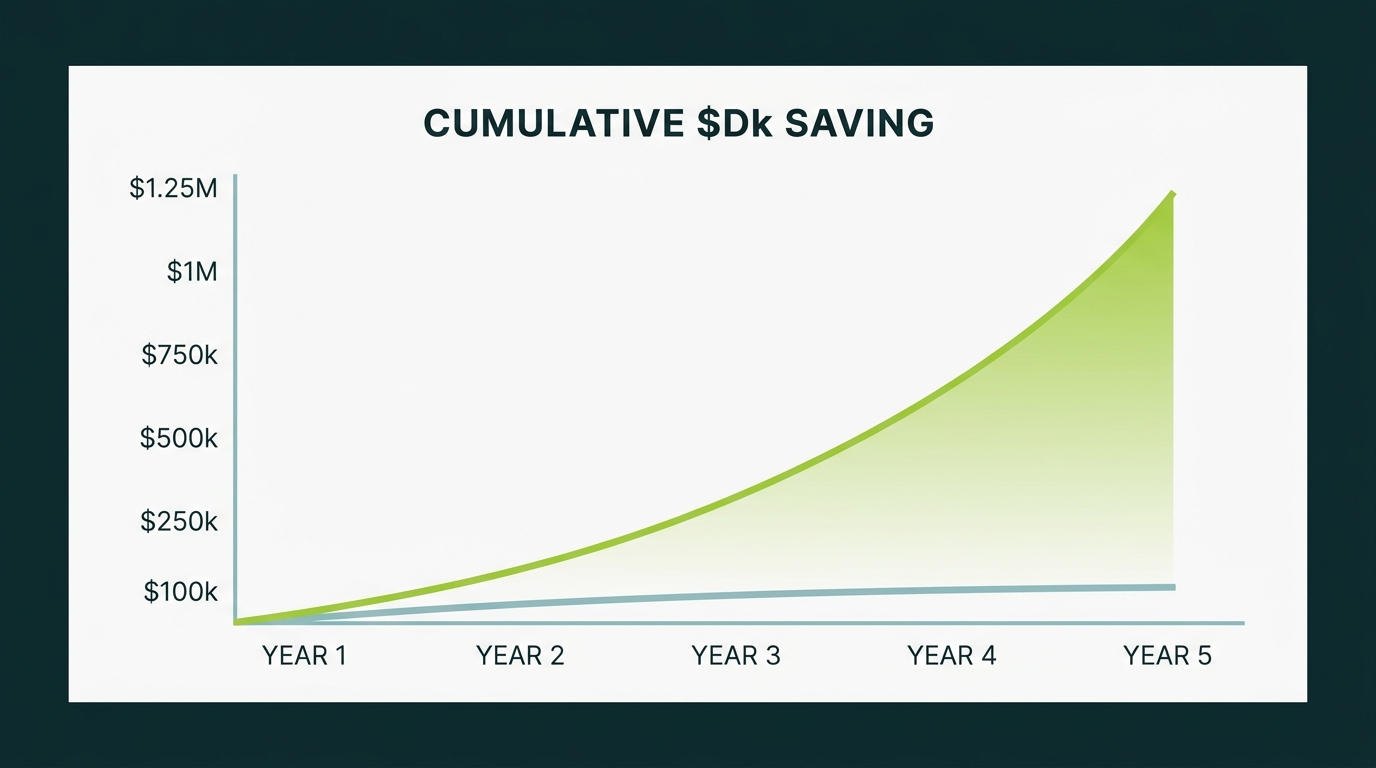

The chart below uses the same hypothetical sale modeled later in this section: $6,880 in estimated federal tax savings when Spec ID is used instead of FIFO, assuming the gain is taxed at a 32% ordinary income rate. If a similar optimization opportunity repeats each year, the cumulative savings can become meaningful without assuming unrealistic seven-figure results.

Here’s where most investors get stuck: they pick a method once and never revisit it. But your optimal method can change year to year based on market conditions and your personal tax situation.

Step 1: Export your complete transaction history from every exchange and wallet you’ve used. Include deposits, withdrawals, trades, staking rewards, and airdrops.

Step 2: Run the numbers under each method. Tools like CoinTracker and Koinly let you toggle between FIFO, LIFO, and HIFO to see the tax impact. Or hand it to a crypto tax specialist who does this daily.

Step 3: Consider your full tax picture. If you have significant stock market losses, you might want to realize more crypto gains (FIFO). If you’re already at the top marginal bracket, minimizing gains (HIFO) is critical.

Step 4: Document your election. There’s no special IRS form for choosing a method. You simply apply it consistently on Form 8949 and keep your records.

A Real-World Comparison

Here’s a hypothetical example of how different methods can impact taxable gains for the same portfolio. Assume a taxpayer had 50 Ethereum transactions across 2024 and 2025 and sold 10 ETH in Q4 2026, and the selected lots produced short-term gains taxed at a 32% federal ordinary income rate:

| Method | Taxable Gain | Estimated Federal Tax (32% ordinary rate) |

|---|---|---|

| FIFO | $28,400 | $9,088 |

| LIFO | $12,100 | $3,872 |

| HIFO | $8,300 | $2,656 |

| Spec ID | $6,900 | $2,208 |

In this example, choosing the optimal method results in approximately $6,880 in federal tax savings compared to FIFO. For larger portfolios, the tax impact can be significantly greater.

What About the New 1099-DA?

Starting in 2026, exchanges will issue Form 1099-DA reporting your digital asset transactions to the IRS. This changes the game for cost basis:

- Exchanges will report proceeds, but may not always have your complete cost basis

- Transferring crypto between exchanges or wallets can make cost basis tracking more difficult

- You’re still responsible for maintaining accurate cost basis records, especially for DeFi and cross-exchange transfers

The 1099-DA makes compliance more visible, but it doesn’t do the optimization for you. If anything, it makes proper cost basis selection more important. The IRS now has your transaction data and will compare it to your Form 8949.

Bottom Line: What to Do Next

Your crypto cost basis method is not a set-it-and-forget-it decision. It’s a strategic lever that can save you thousands of dollars annually.

Here’s your action plan:

- Audit your current method. If you’ve been defaulting to FIFO, run the numbers under HIFO and Spec ID for your latest tax year.

- Get your records in order. Complete transaction history, lot-level detail, cost basis for every acquisition. This is non-negotiable for Spec ID.

- Model before you sell. Before your next major disposal, calculate the tax impact under different methods.

- Talk to a specialist. A 15-minute crypto tax review can identify thousands in potential savings.

Don’t leave money on the table. Your cost basis method is the one thing you can control, and the difference adds up.

Frequently Asked Questions

What is FIFO for crypto taxes?

First-In, First-Out (FIFO) means the earliest-purchased crypto units are considered sold first. It is the IRS default method and often results in higher gains if your oldest coins were bought at the lowest prices.

Can I switch cost basis methods between tax years?

Yes, you can switch methods year to year as long as you have not yet filed for that tax year. However, once you file using a specific method, you cannot amend to change it retroactively for that year.

Do I need to track cost basis for every crypto transaction?

Yes. The IRS requires you to report the cost basis of every disposed crypto asset on Form 8949. Failing to track cost basis can result in the IRS assigning a $0 basis, meaning your entire sale proceeds become taxable gain.