Coinbase is the exchange most American crypto investors actually use, which makes it the place where the new tax-form era hits hardest. In 2026, Coinbase users are opening Form 1099-DA, seeing enormous proceeds numbers, and assuming they owe tax on all of it. They do not. This guide explains exactly what Coinbase reports, why the numbers look the way they do, and how to turn a proceeds-only form into an accurate return.

Find Yourself: Which Coinbase User Are You?

Coinbase users are not all the same, and your tax exposure depends on how you use the platform. Find your profile and jump to what matters most.

The 1099-DA Shock Case

You opened your 1099-DA, saw a huge proceeds number, and assumed you owe tax on all of it.

Proceeds are not gains. Jump to Understanding 1099-DA →The Transfer-In Case

You bought elsewhere, moved crypto into Coinbase, and sold, and now your basis is missing or noncovered.

This is the core problem. Jump to Wallet Transfers and Cost Basis →The Advanced Trader

High-volume spot and derivatives activity on Coinbase Advanced across the year.

Volume changes everything. Jump to Advanced Taxes →The Staker

You earn staking rewards on ETH, SOL, ADA, or ATOM through Coinbase.

Rewards are income then gains. Jump to Staking Taxes →The Base User

You bridge to Base and trade DeFi, memecoins, and NFTs in the Coinbase ecosystem.

On-chain activity is on you. Jump to Base Network Taxes →The Multi-Platform User

Coinbase plus Kraken, Coinbase Wallet, Ledger, MetaMask, and more.

You need full reconciliation. Jump to the Audit Checklist →What Is Coinbase?

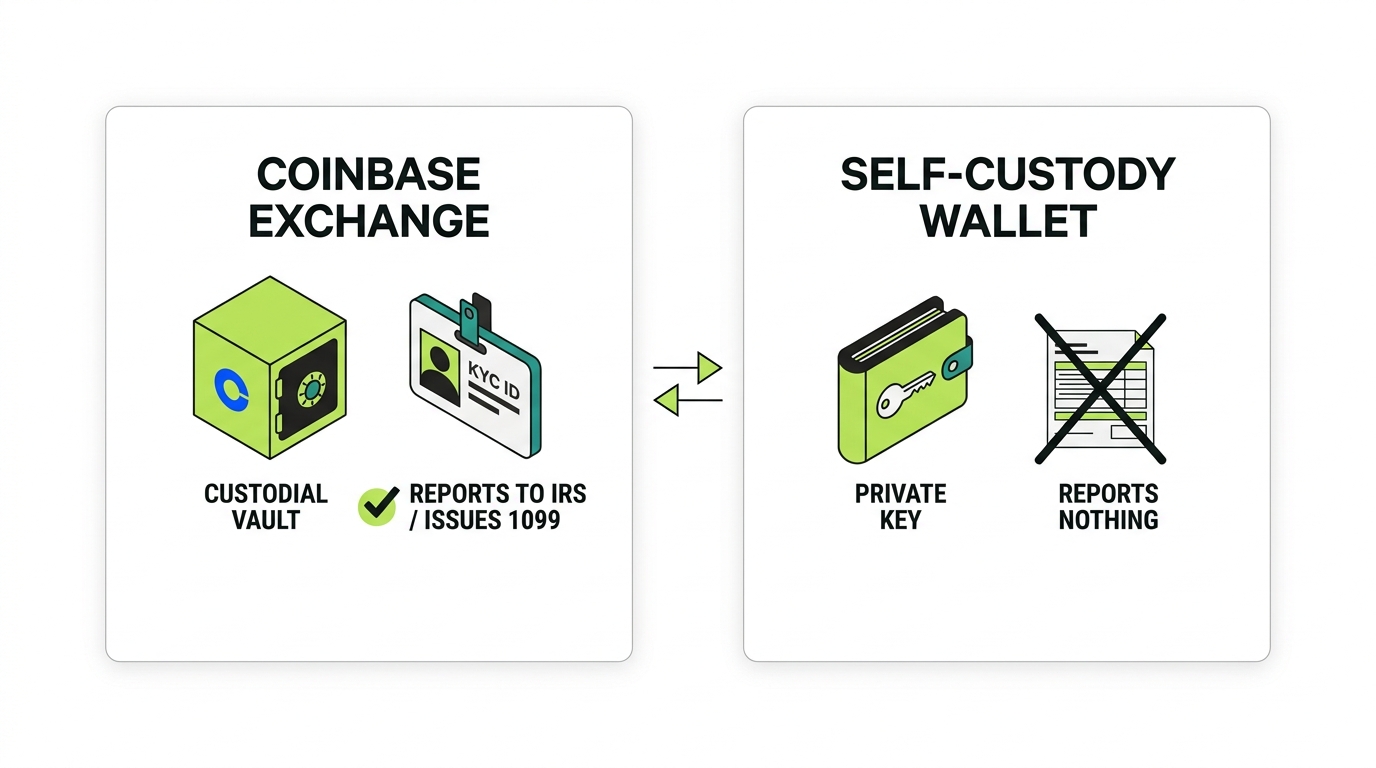

Coinbase is the largest US-based centralized cryptocurrency exchange, where you buy, sell, and trade crypto, earn staking rewards, and access advanced products like Coinbase Advanced and derivatives. Because it is centralized and custodial, the tax situation is fundamentally different from a self-custody wallet, and understanding that difference is the foundation of getting your Coinbase taxes right.

Coinbase Exchange Overview

The main Coinbase app is where most users buy crypto with dollars, sell, convert between assets, and hold balances in custody. Coinbase runs KYC to verify your identity, keeps a record of the trades that happen on its platform, and as a broker reports certain activity to the IRS and provides tax documents through its Tax Center. This is the opposite of a self-custody wallet, where no company keeps your books.

Coinbase Advanced

Coinbase Advanced is the professional trading interface with order books, maker and taker fees, and far higher trade volume. The tax rules are the same as spot, but the sheer number of disposals makes accurate reconciliation a much bigger job, which is why active Advanced traders see the largest and most confusing proceeds totals.

Coinbase Wallet

Coinbase Wallet is a separate, self-custody application. It is not the exchange. It holds your private keys, connects to DeFi and on-chain apps, and reports nothing to the IRS. For taxes, the exchange and the wallet are different worlds, and the assets moving between them must be tracked so basis follows each transfer. We cover the self-custody side in depth in our dedicated Coinbase Wallet guide.

Coinbase Prime

Coinbase Prime is the institutional platform for funds, businesses, and large holders, with custody, trading, and reporting built for scale. The same tax principles apply, but institutional users typically have additional reporting obligations and entity-level considerations that warrant professional guidance.

An exchange like Coinbase hands you a 1099-DA full of proceeds. It is the opening line of your tax story, not the conclusion.

Do You Owe Taxes On Coinbase?

Yes, if you had taxable events. Buying and holding is not taxable, but selling, trading, spending, and earning crypto are.

IRS Property Rules

The IRS treats virtual currency as property under Notice 2014-21. That classification is why every disposal can trigger a capital gain or loss and why earning crypto is ordinary income. Coinbase does not change these rules, it simply reports some of the activity that triggers them.

Capital Gains

Capital gains apply when you dispose of crypto: selling it for dollars, trading it for another token, converting it to a stablecoin, or spending it. Your gain or loss equals proceeds minus cost basis. Hold an asset one year or less and the gain is short-term, taxed at ordinary rates. Hold it longer than a year and the gain is long-term, taxed at the lower 0, 15, or 20 percent rates.

Ordinary Income

Income events apply when you earn crypto: staking rewards, learn-and-earn grants, and other reward income are ordinary income at fair market value when you gain control of them. That value also becomes your cost basis for a later sale.

Taxable Events

A taxable event is any moment you dispose of or earn crypto. Selling, trading, converting, spending, and earning all qualify. Buying with dollars, holding, and transferring between your own accounts do not. Most Coinbase tax mistakes come from misjudging which bucket an action falls into.

Does Coinbase Report To The IRS?

Yes. As a centralized, KYC-verified broker, Coinbase reports to the IRS, and that reporting is expanding.

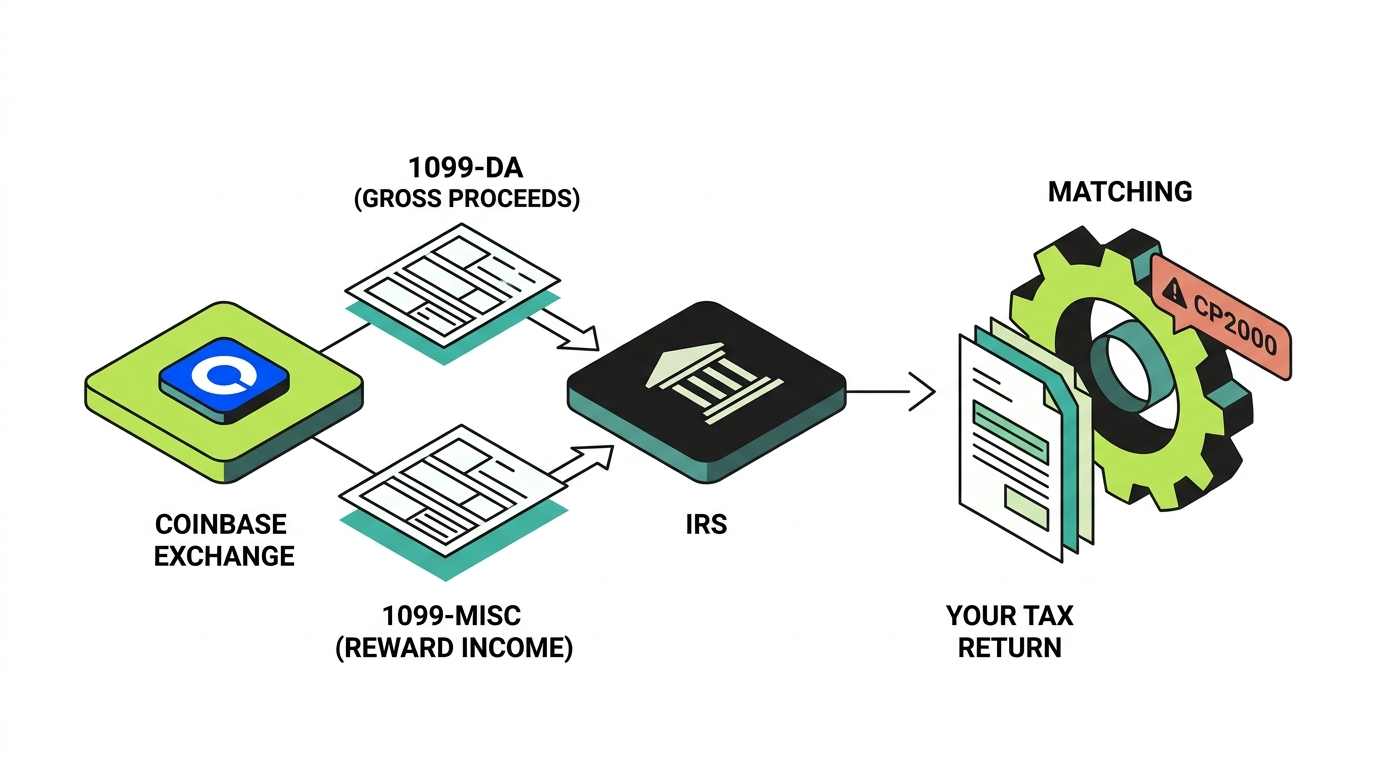

1099-DA

Form 1099-DA is the new digital asset broker reporting form. Starting with the 2025 tax year, Coinbase provides 1099-DA for reportable sales and dispositions, reporting gross proceeds. For 2025, brokers generally report proceeds while full cost basis reporting is still phasing in. This single fact, proceeds without complete basis, drives the entire reconciliation challenge covered later.

1099-MISC

Separately, Coinbase may issue Form 1099-MISC to report certain income such as rewards when reporting thresholds are met. Even without a form, reward income is taxable, so you report it from your own records regardless of whether a 1099-MISC arrives.

IRS Matching Programs

The IRS runs automated matching that compares broker-reported proceeds to what taxpayers file. If your return omits Coinbase activity or does not reconcile with the reported proceeds, that mismatch can trigger an automated notice such as a CP2000. The defense is a return that ties cleanly to the 1099-DA proceeds while reflecting your true basis.

What Coinbase Reports

Coinbase reports qualifying digital asset sales and dispositions through IRS-required tax forms including Form 1099-DA and, in some cases, Form 1099-MISC, and provides those documents through its Tax Center. The reporting is tied to your verified identity, so the IRS receives information linked directly to you. What Coinbase cannot report is the history that happened off its platform: purchases on other exchanges, self-custody and on-chain activity, and the original basis of assets you transferred in.

Understanding Coinbase 1099-DA

This is the most important section in the guide, because the 1099-DA is where Coinbase users panic, overpay, or underreport. Read it carefully.

What Is Form 1099-DA?

Form 1099-DA is the IRS form brokers use to report digital asset sales and dispositions. It tells the IRS the gross proceeds from your activity on the platform and, over time, more basis information. It is an information return, not a bill, and not a finished calculation of what you owe. We break the form down box by box in our dedicated Coinbase 1099-DA guide.

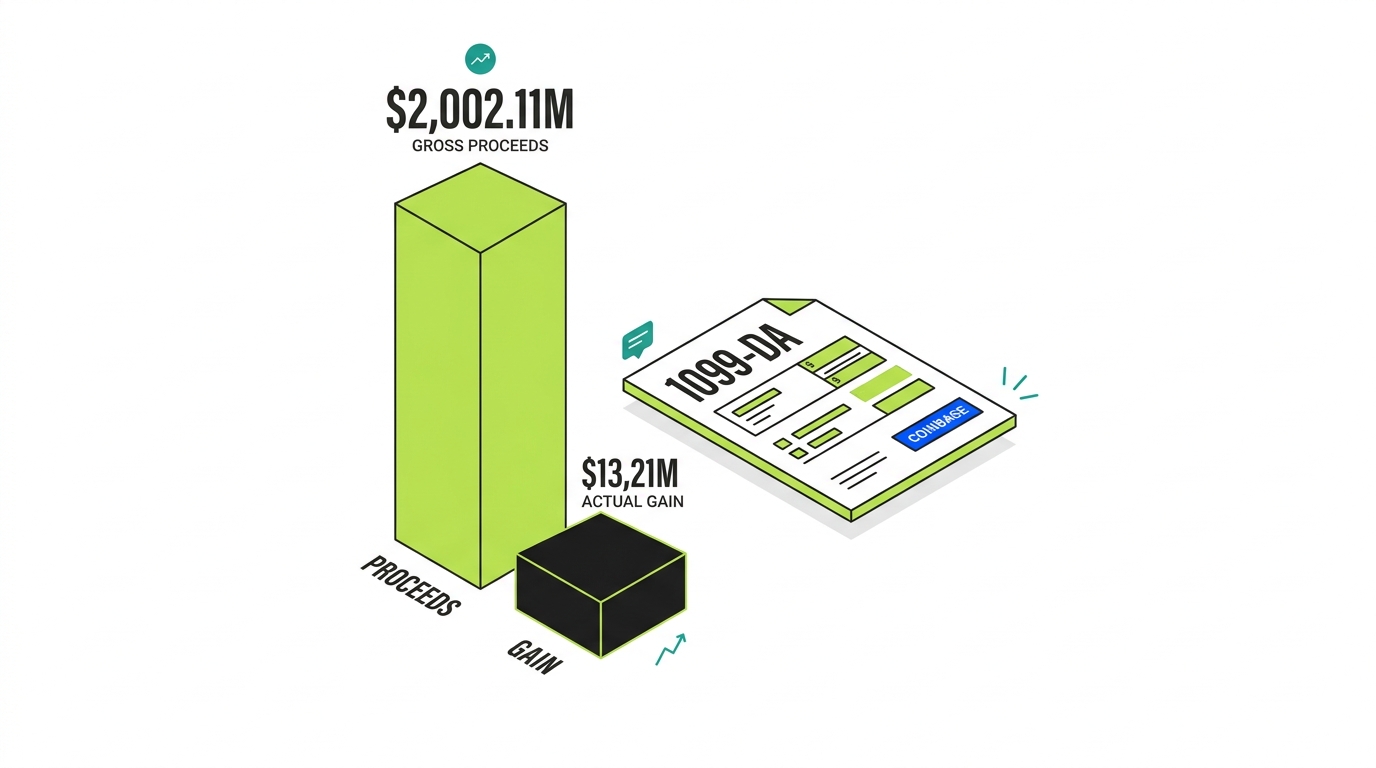

Why Proceeds Look So High

The proceeds figure is the total of everything you sold for, summed across every disposal, before subtracting what you paid. If you traded the same capital in and out many times, each trade adds its full proceeds to the total. That is how an account that netted a small profit can report enormous proceeds. The number reflects activity volume, not profit.

This matters most for Coinbase Advanced traders and anyone who used crypto-to-crypto conversions, because each leg of a round trip counts. Buy, sell, buy again, sell again, and the same dollars get reported as proceeds four times. A buy-and-hold investor who sold once sees proceeds close to their actual sale, while a frequent trader sees a proceeds total many multiples of the capital they ever put in. Neither is wrong, the form is doing exactly what it is designed to do. The mistake is reading the proceeds line as if it were the gain line.

Proceeds vs Gain Example

Why Cost Basis May Be Missing

For 2025, Coinbase generally reports proceeds, and it cannot report basis for assets you bought elsewhere and transferred in. So the form may show large proceeds paired with little or no basis. Left unreconciled, tax software or a naive reading treats the missing basis as zero, which overstates your gain dramatically and inflates your tax bill.

Covered vs Noncovered Assets

Covered assets are those for which the broker is required to track and report basis, generally tied to when the rules took effect and whether the asset was acquired on the platform. Noncovered assets are those where basis is not broker-reported, often because they came in from elsewhere. For noncovered assets, supplying the correct basis is entirely your job, and Coinbase may flag these so you know the basis figure is yours to establish.

How To Reconcile A 1099-DA

Reconciliation means pairing the proceeds Coinbase reports with your true cost basis for each disposal, accounting for transferred-in assets, removing duplication, and producing a Form 8949 that shows real gains and losses while tying to the reported proceeds total. This is the heart of exchange tax work, and it is exactly what most ranking articles skip. If your form shows blank or zero basis, start with our 1099-DA cost basis fix guide.

Your 1099-DA tells the IRS what you sold for. Your job is to tell the IRS what you actually made.

Coinbase Transactions That Are Taxable

These are the events that create a tax bill.

Selling Crypto

Selling crypto for dollars or stablecoins is a taxable disposal. Gain or loss equals proceeds minus cost basis.

Crypto-to-Crypto Trades

Trading or converting one cryptocurrency for another is a taxable disposal of the crypto you gave up, even though no dollars change hands. Coinbase makes conversions easy with one tap, which is exactly why these are the most commonly overlooked taxable events.

Stablecoin Transactions

Converting crypto into a stablecoin like USDC or USDT is a disposal of the crypto you converted, so it is taxable. Stablecoins are still property, and moving into them does not make the underlying sale tax free.

Spending Crypto

Spending crypto on goods or services, including through a Coinbase card, is treated as a sale of that crypto at fair market value, triggering a gain or loss.

Advanced Trades

Every disposal on Coinbase Advanced is taxable just like spot, but the volume is far higher. Each trade is a separate gain or loss event that must be captured and reconciled.

Derivative Transactions

Settlement and closing of derivatives positions produces realized profit or loss that is a taxable result of the activity. We cover the nuances in the derivatives section.

Coinbase Transactions That Are Not Taxable

Not every action is a taxable event. These generally are not.

Buying Crypto

Buying crypto with US dollars is not taxable. It sets your cost basis, which is what you paid including fees.

Holding Crypto

Holding crypto on Coinbase is never taxable, no matter how much the value changes. Unrealized gains are not taxed until you dispose of the asset.

Transfers Between Wallets

Withdrawing crypto from Coinbase to a wallet you own, including Coinbase Wallet, is a transfer, not a sale, so it is not taxable. Your basis must follow the asset, because once it leaves Coinbase the exchange stops tracking it.

Moving Assets To Coinbase

Moving crypto into Coinbase from another exchange or wallet you control is a transfer, not a sale, so it is not taxable. The risk is purely about basis following the asset, because Coinbase will not know what you originally paid.

Coinbase Staking Taxes

Staking is a common source of ordinary income for Coinbase users across ETH, SOL, ADA, ATOM, and more.

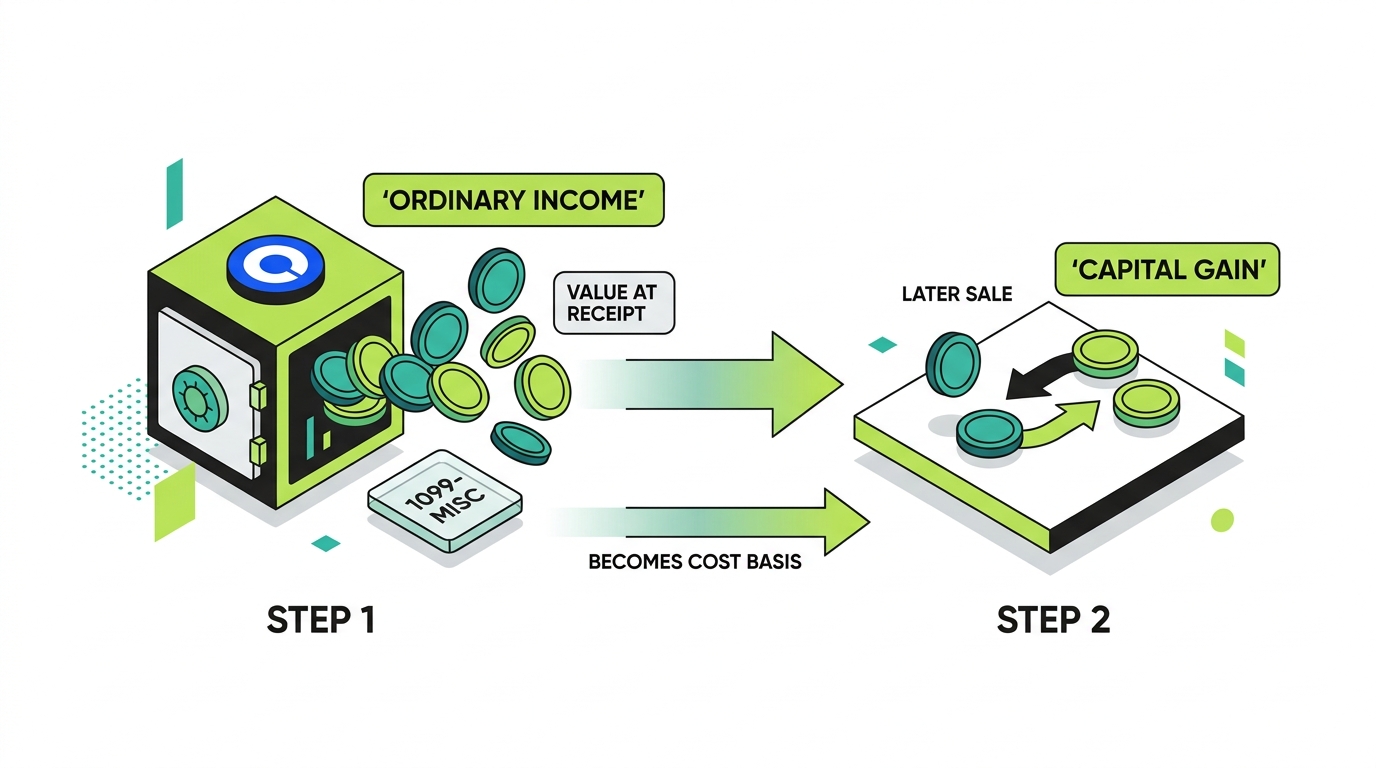

Reward Income

Staking rewards are ordinary income at fair market value when you gain control of them, consistent with IRS guidance in Revenue Ruling 2023-14. Tracking the value at each reward point across the year is tedious but necessary.

1099-MISC Reporting

Coinbase may report reward income on Form 1099-MISC. Whether or not you receive one, the income is taxable and you report it from your records.

Basis Treatment

The amount you report as income becomes your cost basis in the reward assets. Report rewards once as income when received, then again as a capital gain or loss when sold, not twice as income.

Selling Reward Assets

When you later sell or trade your staking rewards, you report a separate capital gain or loss equal to the sale value minus the basis you established when you earned them.

Staking Example

Coinbase Advanced Taxes

Coinbase Advanced is where high-volume traders generate the most complexity, and it is a major content gap that most ranking pages ignore.

Trading Fees

Maker and taker fees are part of your cost of acquiring or disposing of crypto. Fees generally increase your basis when buying and reduce your proceeds when selling, which lowers your gain. Capturing fees correctly across thousands of trades is one reason software reconciliation beats manual calculation.

High-Frequency Trading

High-frequency activity can generate thousands of taxable disposals in a year. The only practical path is to export the complete trade history and run it through crypto tax software, because manual calculation is not realistic at that volume.

Short-Term Gains

Most Advanced trading produces short-term gains, taxed at ordinary income rates, because positions are held briefly. Separating short-term from long-term lots correctly is essential, since the rate difference is significant.

Recordkeeping

The defining challenge of Advanced trading is recordkeeping. Export everything, reconcile the proceeds to the 1099-DA, and keep the transaction-level detail, because a summary number alone cannot be defended in an audit.

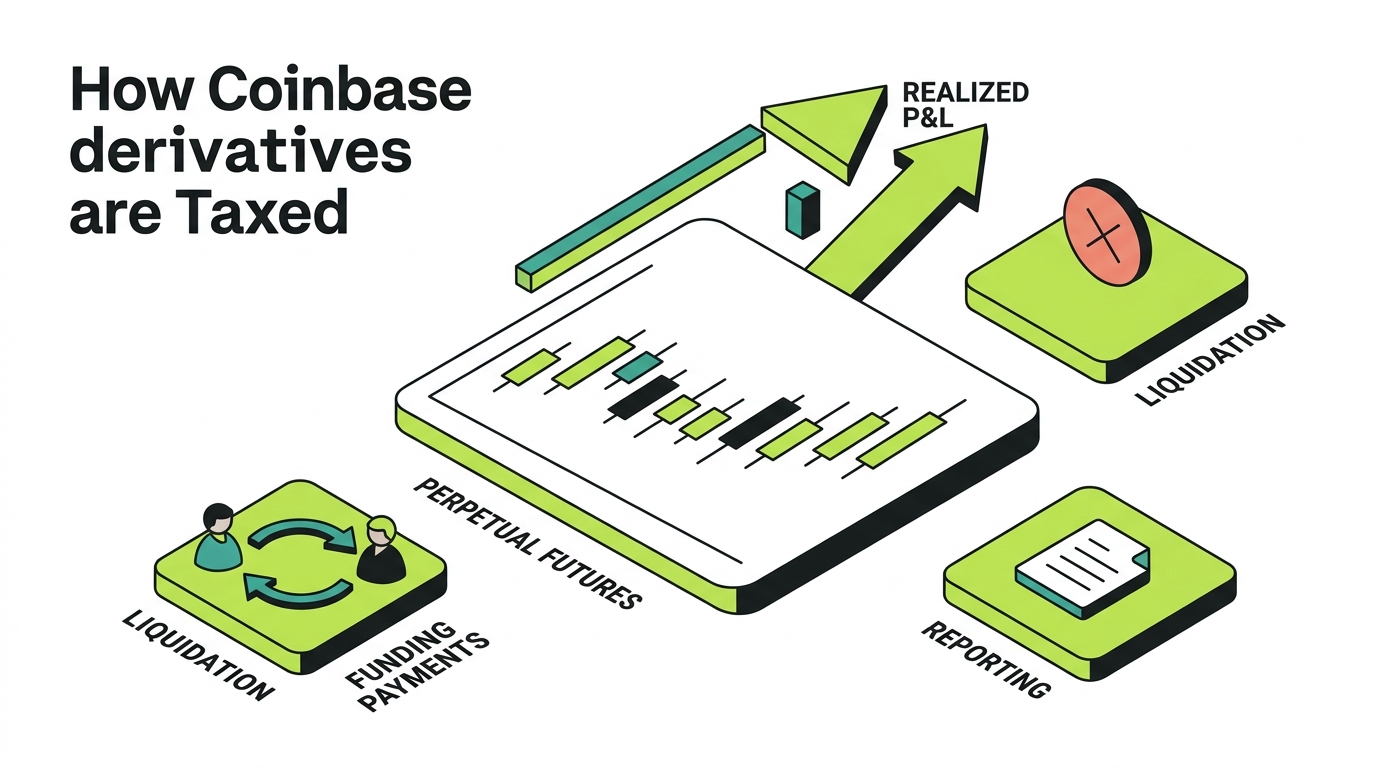

Coinbase Derivatives Taxes

Coinbase derivatives are a major content gap that almost nobody covers well, yet they create some of the most complex reporting.

Perpetual Futures

Perpetual futures let you take leveraged positions without an expiry date. The borrowed exposure itself is not income, but the closing and settlement of positions produces realized gains and losses that are taxable.

Realized P&L

Your taxable result from derivatives is the realized profit and loss across your positions, including the effect of funding payments over the life of each position. Document every open, close, and settlement so the realized result is accurate.

Liquidations

A liquidation is a forced close of a position, so it is a taxable event with a gain or loss, often at an unfavorable price. Liquidations frequently produce losses, which are still deductible, so capture them rather than ignoring the position.

Reporting Considerations

The exact federal treatment of crypto derivatives can be complex and depends on the product and your situation. Track every position, funding payment, and liquidation, and have a professional confirm the correct characterization rather than guessing.

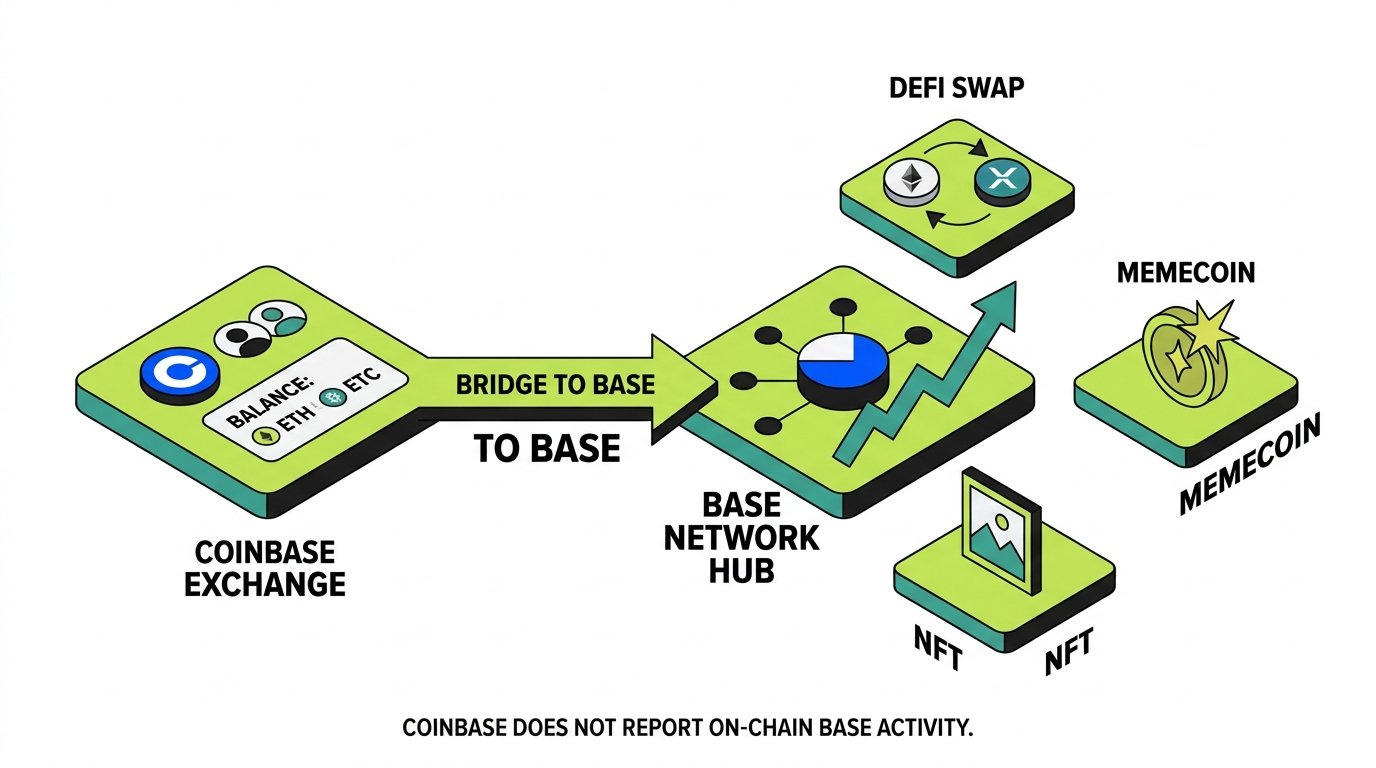

Base Network Taxes

Base is perhaps the biggest future tax opportunity tied to Coinbase, because Coinbase built Base and most guides ignore it entirely.

What Is Base?

Base is an Ethereum layer-2 network incubated by Coinbase. It is on-chain, so activity on Base happens in self-custody wallets and decentralized apps, and Coinbase does not report it for you. Everything you do on Base is your responsibility to track and report.

Bridging To Base

Bridging crypto from Coinbase or Ethereum to Base is generally a transfer of your own assets, not a sale, so the bridge itself is usually not taxable. The critical part is that basis must follow the asset across the bridge, or a later sale on Base will show as zero basis.

Base DeFi

Swaps, liquidity provision, lending, and yield on Base apps like Aerodrome are taxable events. A token swap is a disposal, liquidity and yield can create income and disposals, and each must be captured from on-chain data.

Base NFTs

Buying, selling, and minting NFTs on Base are taxable like any other crypto disposal or acquisition. Selling an NFT is a capital gain or loss, and royalties or mint rewards can be income.

Base Memecoins

Base memecoin trading generates a taxable disposal on every swap. High-volume memecoin activity can create a large number of taxable events with messy basis, making reconciliation essential.

Coinbase Wallet Transfers and Cost Basis

This is the core problem for most Coinbase users, because crypto rarely stays in one place.

Coinbase to Wallet

When you move crypto from Coinbase to a wallet you control, the basis must travel with it. Coinbase stops tracking the asset once it leaves, so a later disposal elsewhere depends on you carrying the original basis forward.

Wallet to Coinbase

When you move crypto into Coinbase from a wallet, Coinbase does not know what you originally paid. If you then sell, the 1099-DA may show proceeds with missing or noncovered basis, which is the classic source of an overstated gain.

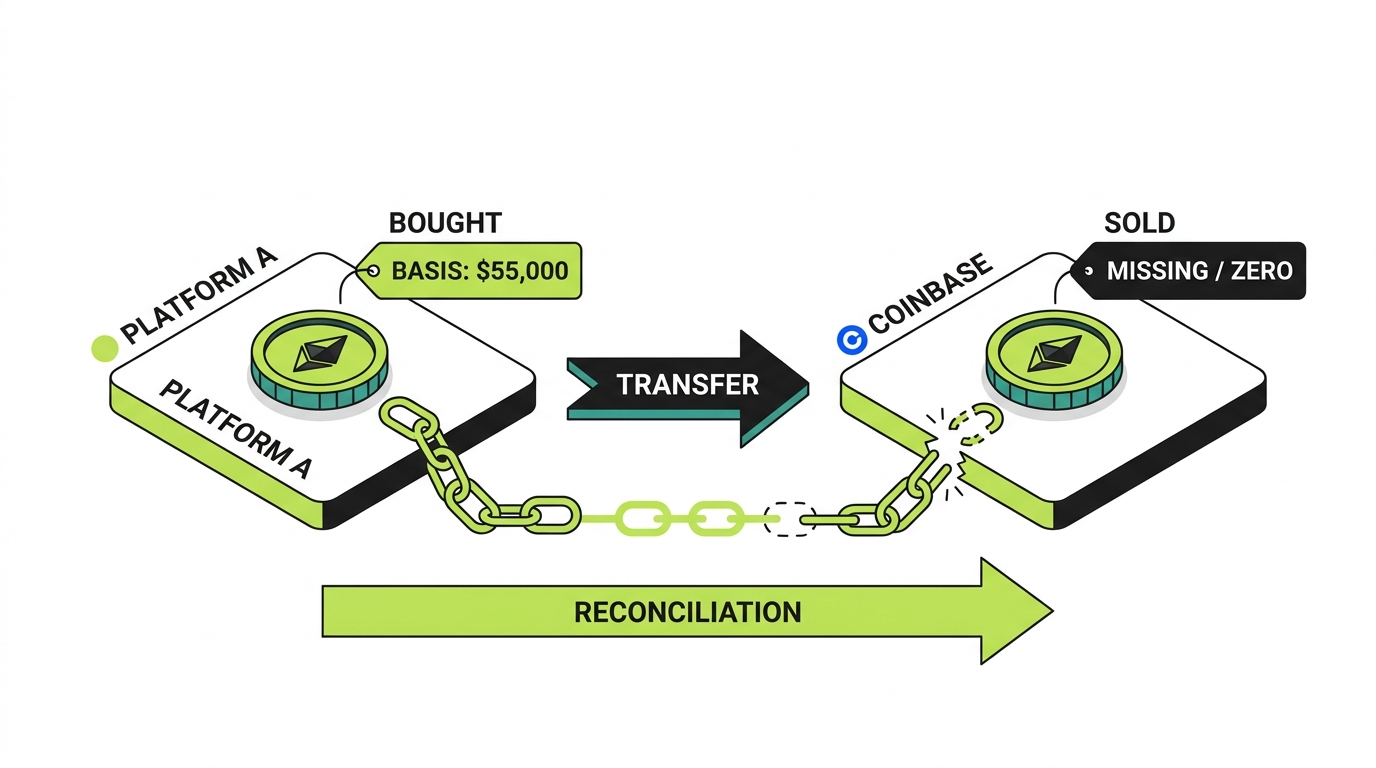

External Exchanges

Crypto bought on Kraken, Gemini, Binance.US, or another exchange and then sold on Coinbase has its basis on the original platform and its disposal on Coinbase. Only by combining both histories do you get an accurate gain.

Missing Acquisition Records

For assets bought years ago or across platforms that no longer have your records, you must reconstruct the original acquisition price. Without it, the basis defaults toward zero and the gain is overstated. Reconstructing and documenting that basis is a central part of reconciliation.

Basis treated as zero

The Coinbase 1099-DA shows 80,000 dollars in proceeds with missing basis. Tax software treats the basis as zero, so the entire 80,000 dollars looks like gain and the tax bill is dramatically overstated.

Real basis traced to the asset

The original 55,000 dollar basis from Kraken is traced to the asset and the transfer into Coinbase is matched, not double counted. The Form 8949 ties to the 1099-DA proceeds while showing the real 25,000 dollar gain.

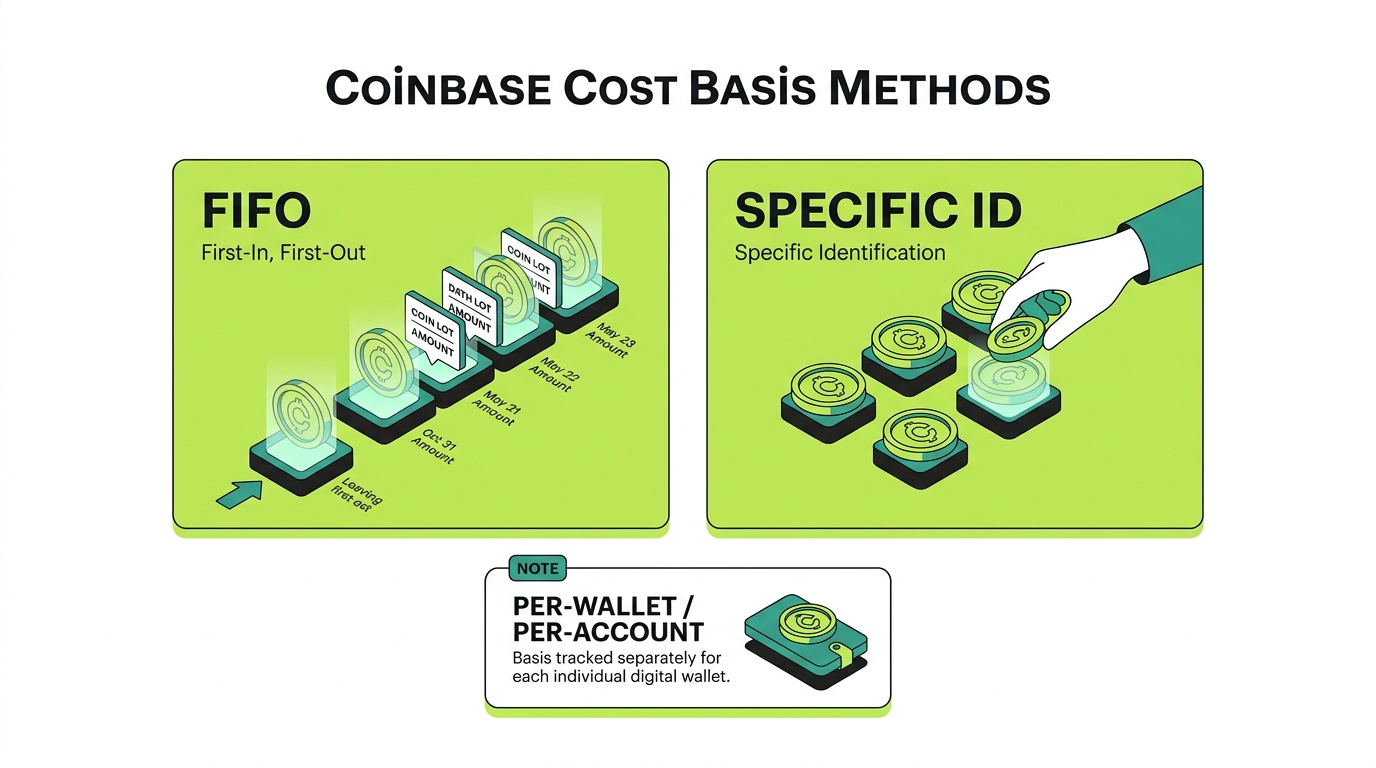

How To Calculate Coinbase Cost Basis

Cost basis is what you paid for an asset including fees, and it is the number that turns proceeds into a real gain.

FIFO

First In, First Out assumes the earliest coins you bought are the first ones sold. It is the common default and is simple, but in a rising market it often produces larger taxable gains than other methods.

Specific Identification

Specific Identification lets you choose which lots you sell, if your records support it, which can minimize gains by selling higher-basis lots first. It requires detailed, contemporaneous records to hold up.

Wallet-Level Tracking

Under Revenue Procedure 2024-28, taxpayers track basis on a per-wallet and per-account basis rather than universally across all holdings, effective starting January 1, 2025. This makes where each asset lives, and the basis attached to it, more important than ever.

Transfer Reconciliation

The hardest part is reconciling transfers so basis follows each asset across exchanges and wallets. This is the step that connects everything into an accurate gain, and it is the foundation of digital asset reconciliation.

How To Download Coinbase Tax Reports

Coinbase provides tax documents and reports through its Tax Center, and pulling the right data is the first practical step.

Tax Center

The Tax Center provides a tax summary of your activity, access to any 1099 forms, and downloadable reports. It is the starting point, but the summary alone is not enough for accurate reconciliation. Here is how to get into it.

On desktop:

- Sign in to your account at Coinbase.com.

- Click your profile icon in the top right corner.

- Select “Taxes” from the dropdown menu (or go directly to the Coinbase Taxes section).

- Open the “Documents” tab. This is where your 1099 forms, gain/loss summaries, and report generators live.

On the mobile app:

- Open the Coinbase app and tap the menu (the three lines).

- Tap “Taxes,” then “Documents.”

- From here you can view your forms and generate reports.

Note: the Tax Center reflects activity on Coinbase.com only. It does not include Coinbase Wallet (self-custody) or the deprecated Coinbase Pro. Those need to be pulled separately and reconciled in.

Transaction Reports

Download the complete transaction history, not just the summary. Transaction-level data is what software imports rely on, and it is essential for reconciling transferred-in assets and noncovered basis.

To download it:

- From the Tax Center, open the “Documents” tab.

- Find the “Transaction History” or raw transaction report option (this is separate from the gain/loss summary).

- Choose the tax year you need, then set a custom date range of January 1 to December 31 for that year to capture everything.

- Click “Generate Report” and download the CSV file.

- Save the raw CSV. This is the file you hand to tax software or a reconciliation specialist, because it contains the line-by-line buys, sells, conversions, transfers, and rewards.

ProTip: generate the report for the full calendar year even if you think you only traded for part of it. Transfers and rewards often land in months you forget about, and a partial-year export is how line items go missing.

Gain/Loss Reports

Coinbase offers gain and loss reports that estimate your results, but they reflect only what Coinbase knows. For assets with off-platform basis, these reports can be inaccurate until reconciled with your full history.

To download one:

- From the Tax Center “Documents” tab, locate the “Gain/Loss” report.

- Select the tax year.

- Download the report (CSV or PDF, depending on what Coinbase offers for your account).

- Treat the numbers as an estimate, not a filing-ready figure. Any asset you transferred into Coinbase from another exchange or wallet may show a missing or zero cost basis, which inflates the gain.

Note: starting with the 2025 tax year, Form 8949 is no longer available directly through the Coinbase retail Tax Center. If you need a completed 8949, you will either reconcile through tax software or work with a specialist who produces it from your transaction history.

1099 Downloads

Download every 1099-DA and 1099-MISC Coinbase issues. These are the forms the IRS already has, so your return must reconcile to them, and keeping copies is part of your audit defense.

To download them:

- Go to the Tax Center “Documents” tab.

- Any 1099 forms issued to you for the tax year appear here. Coinbase typically posts 1099-MISC by mid-February.

- Download each form (1099-DA for gross proceeds from sales and dispositions, 1099-MISC for $600 or more in reward and incentive income).

- Save a copy of every form alongside your transaction history. If a form will not download, enable pop-up downloads in your browser and retry.

Warning: the 1099-DA reports gross proceeds, not your gain, and for 2025 it may not include cost basis on assets you transferred in. The number looking large is normal. Your job is to reconcile to it, not to ignore it.

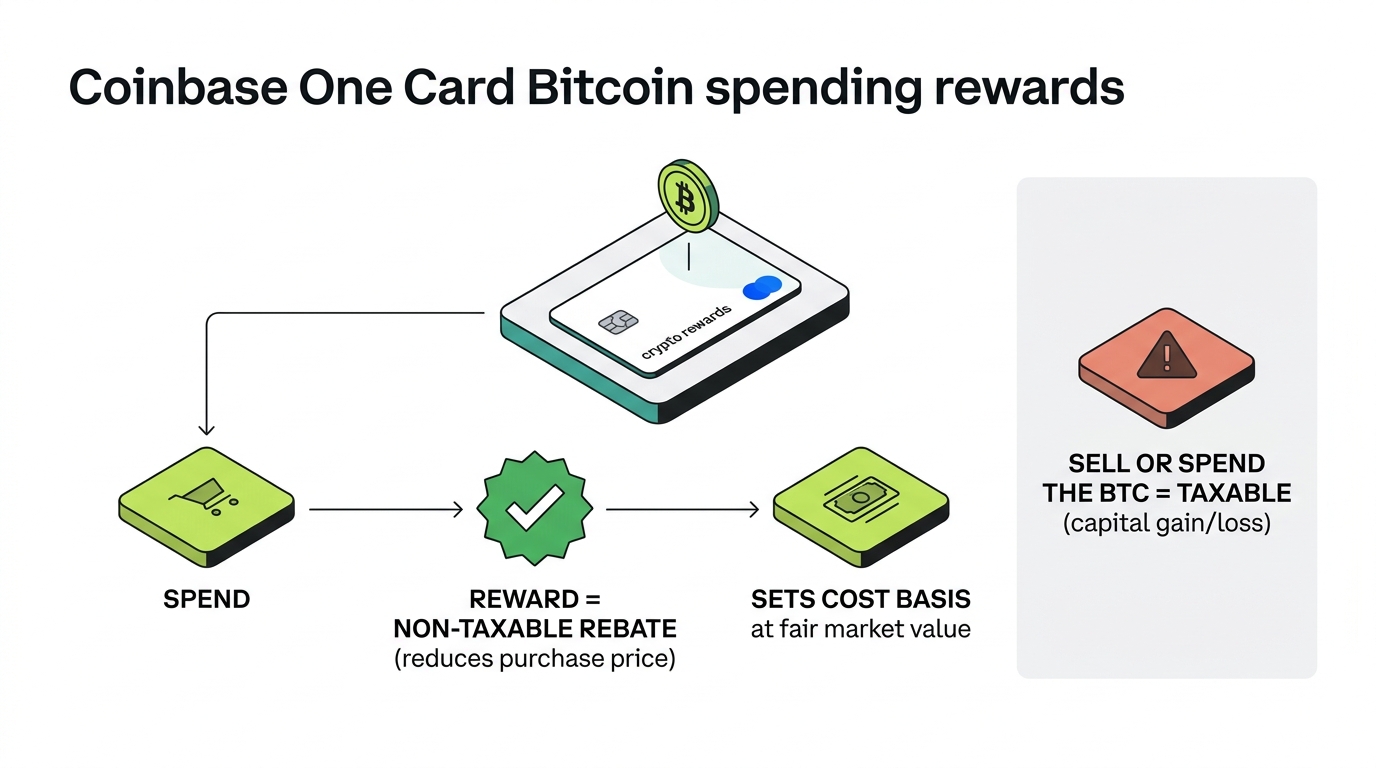

Coinbase One Card Bitcoin Rewards And Taxes

The Coinbase One Card pays bitcoin rewards on your spending, and the most common question is whether those rewards are taxable income. For everyday spend-based rewards, the answer is generally no, and the reason is worth understanding.

Why Spend-Based Rewards Are Not Income

The IRS has long treated credit and debit card rewards earned on spending the same way it treats cash back, points, and airline miles: as a rebate, not income. A rebate is considered a reduction in the purchase price of what you bought, not money you earned. Getting bitcoin back for spending follows that same logic, so you do not report the receipt of those rewards as ordinary income.

The Catch: Receiving Bitcoin Sets A Cost Basis

Here is the part people miss. The reward is not taxed when you receive it, but you are receiving an actual crypto asset, and that asset gets a cost basis equal to its fair market value in dollars on the day it lands in your account. That basis matters later.

When you eventually sell, convert, or spend that reward bitcoin, that is a disposal, and a disposal is a taxable event. You report a capital gain or loss measured from the value when you received it to the value when you disposed of it. So the reward itself is not income, but the bitcoin it gave you is still property the IRS tracks.

Reward earned, then sold

You spend through the year and earn 100 dollars worth of bitcoin in card rewards. You owe nothing on that 100 dollars when you receive it, because it is a rebate. Your cost basis in that bitcoin is 100 dollars. Months later you sell it for 120 dollars. You now report a 20 dollar capital gain, measured from your 100 dollar basis to the 120 dollar sale price.

When Card-Related Rewards Are Taxable

The rebate treatment applies to rewards tied to spending. Rewards that are not tied to spending are a different story. A sign-up bonus you get just for opening an account, or a referral bonus for bringing in a friend, is generally treated as ordinary income because you did not have to spend to earn it. If those incentives total $600 or more, Coinbase may report them on a 1099-MISC, and you owe income tax on them whether or not you receive the form.

Best Coinbase Tax Software

Software helps import and calculate, but no tool fully solves missing basis and cross-platform reconciliation on its own. These are the common options.

CoinTracker

CoinTracker integrates closely with Coinbase and is a popular choice for importing activity and generating tax reports. It handles standard activity well but still needs accurate transfer reconciliation.

Koinly

Koinly supports a wide range of exchanges and wallets and is strong at consolidating multi-platform histories. It is a frequent pick for users with activity across many venues.

CoinLedger

CoinLedger focuses on straightforward imports and report generation, with a clean workflow for filing-ready output once your data is clean.

TokenTax

TokenTax pairs software with professional services, which can help users with complex situations who want more hands-on support.

ZenLedger

ZenLedger covers exchange and DeFi activity and is used by individuals and professionals for consolidating crypto tax data.

Summ

Summ is built for the reconciliation-first approach, aimed at producing a clean, accurate picture of complete crypto history before filing rather than trusting a single exchange export.

Common Coinbase Tax Mistakes

These are the errors that cost Coinbase users the most money and the most audit risk.

Trusting 1099-DA Alone

Treating the 1099-DA proceeds as your gain is the single biggest mistake. Proceeds are not profit, and filing off the raw number either overstates your tax or, if misread, underreports it.

Missing Cost Basis

Letting transferred-in assets default to zero basis overstates gains dramatically. Establishing the real basis for every asset is the core of accurate Coinbase reporting.

Ignoring Wallet Activity

Forgetting that crypto moved to Coinbase Wallet, MetaMask, or Ledger is part of the same tax picture leads to broken basis chains and inaccurate gains.

Ignoring Staking Rewards

Failing to report staking and reward income as ordinary income when received, or double counting it later, are both common and both wrong.

Ignoring Base Transactions

Assuming Coinbase reports your Base activity. It does not. On-chain Base swaps, NFTs, and memecoins are taxable and entirely your responsibility.

Duplicate Imports

Importing the same activity twice, often by combining a 1099 with a transaction export, double counts proceeds and creates phantom gains. Clean deduplication is part of reconciliation.

How To Prepare For A Coinbase Tax Audit

If the IRS questions your return, documentation is everything. This is a major content gap, and it is where reconciliation pays off.

Exchange Records

Keep complete Coinbase transaction histories and every 1099 form. These tie your return to what the IRS already received and are the first thing an examiner will check.

Wallet Records

Maintain records of every wallet you control and the on-chain activity in them, including Coinbase Wallet and any Base addresses. Self-custody activity is invisible to Coinbase but still part of your tax picture.

Transfer Documentation

Document every transfer in and out of Coinbase with the basis that traveled with each asset. Transfers are where basis breaks, so transfer records are the backbone of an audit defense.

Cost Basis Support

Keep the original purchase records for assets bought elsewhere, so you can prove the basis you used. For noncovered assets, this documentation is the only thing standing between you and a zero-basis assessment.

Form 8949 Reconciliation

Be able to show a Form 8949 that reconciles your real gains and losses to the proceeds Coinbase reported. A return that ties cleanly to the 1099-DA, with documented basis, is the strongest position in an audit.

An audit is won or lost on records. Reconciliation is not just about paying the right tax, it is about being able to prove it.

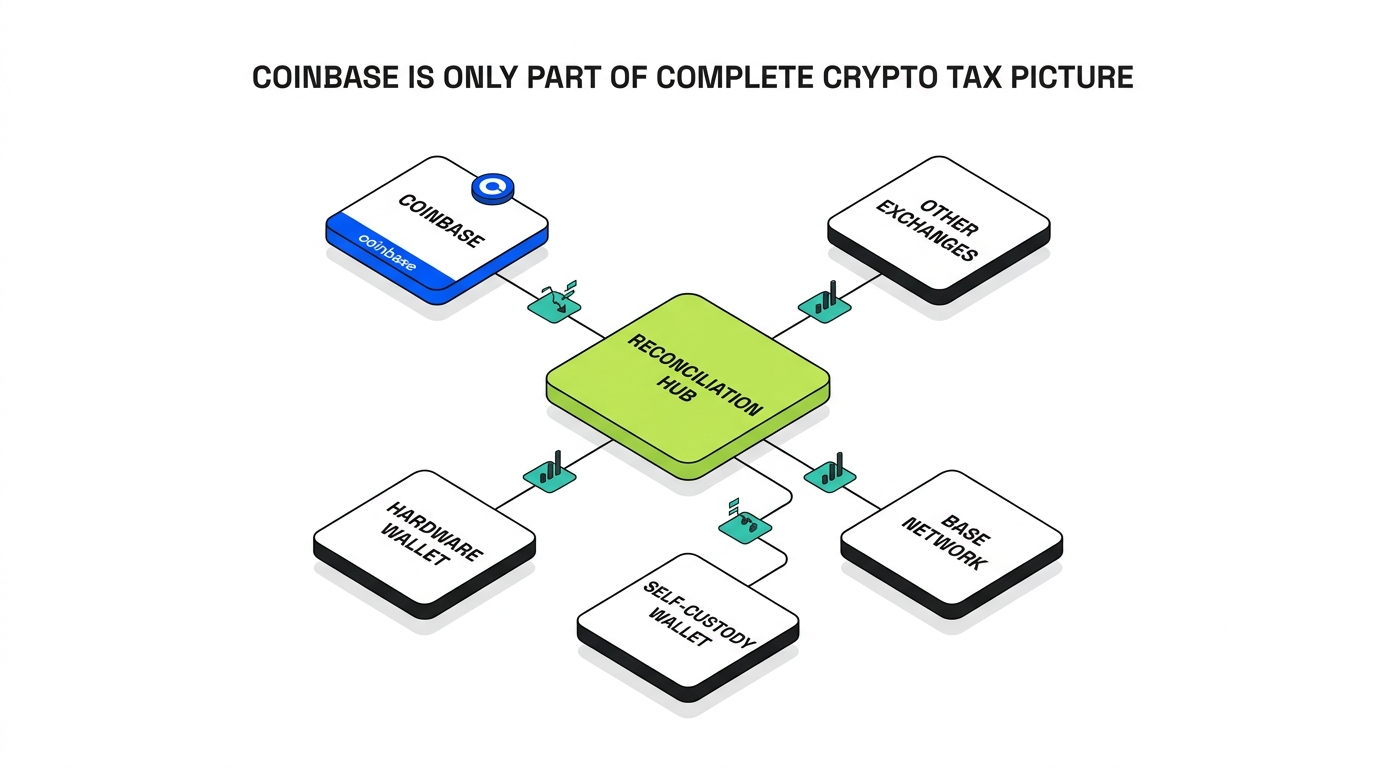

Where Count On Sheep Fits

Coinbase reports your transactions. It does not know your complete crypto history. That gap, between what an exchange reports and what actually happened across every platform you used, is exactly the problem Count On Sheep solves.

Count On Sheep provides CPA-ready Digital Asset Reconciliation for Coinbase users:

- We connect your Coinbase activity with every other exchange, wallet, and on-chain network you have used, including Base.

- We trace cost basis across transfers so noncovered assets get their real basis instead of defaulting to zero.

- We deduplicate and reconcile so your Form 8949 ties to the proceeds on your 1099-DA.

- We produce a clean, accurate, defensible picture of your complete crypto history before your return is prepared.

Count On Sheep is the reconciliation layer that sits underneath filing. We are not a tax filing service and we do not replace your CPA, we make sure the numbers your CPA files are right.

Not sure your crypto taxes are right?

Talk to a Count On Sheep specialist. We will spot the costly errors before you file. No obligation.

Book My Free Review- Reviewed by Former Big 4 Accountants

- Keep your CPA

- No pressure, no sales pitch

Coinbase Tax FAQ

The questions below cover the most common Coinbase tax situations. For your specific circumstances, talk to a professional who can review your complete history.

Related Reading

- Kraken Tax Guide (2026)

- Gemini Tax Guide (2026)

- Binance.US Tax Guide (2026)

- Coinbase Wallet Tax Guide (2026)

- MetaMask Tax Guide (2026)

- Phantom Wallet Tax Guide (2026)

- How Is Crypto Taxed in the US (2026)

- Form 1099-DA Explained (2026)

- How to File Crypto Taxes with Form 8949 and Schedule D

- Per-Wallet Crypto Cost Basis and Rev. Proc. 2024-28

- Crypto Income Tax: Staking, Mining and Airdrops (2026)

- FIFO vs HIFO vs Specific ID for Crypto Taxes

- Crypto Tax Loss Harvesting and the Wash Sale Rule (2026)

- NFT and DeFi Taxes: Liquidity Pools, Staking and Lending

Official IRS Resources

For the primary source rules behind this guide, see the IRS directly:

- IRS: Digital Assets

- IRS Notice 2014-21 (crypto treated as property)

- IRS: About Form 8949

- IRS: About Schedule D (Form 1040)

- IRS: About Form 1099-DA

Frequently Asked Questions

Does Coinbase report to the IRS?

Yes. Coinbase is a centralized exchange and a broker for tax purposes, so it reports certain digital asset activity to the IRS. Starting with the 2025 tax year, Coinbase provides Form 1099-DA for reportable digital asset sales and dispositions, and it may also issue Form 1099-MISC for certain income such as rewards. Your identity is tied to your account through KYC, so the IRS receives reporting linked directly to you.

Will Coinbase send a 1099-DA?

If you had reportable digital asset sales or dispositions on Coinbase, yes, you should expect a Form 1099-DA through the Coinbase Tax Center for the 2025 tax year and beyond. The form reports gross proceeds from your dispositions. Always download and reconcile it against your own records, because the proceeds figure is not your taxable gain.

Why is my Coinbase 1099-DA so high?

Because the 1099-DA reports gross proceeds, not gain. Every sale and crypto-to-crypto trade adds its full proceeds to the total, so an account that traded actively can show hundreds of thousands in proceeds while the actual taxable gain is a small fraction of that. The proceeds number is the sum of what you sold for, before subtracting what you paid. It is not what you owe tax on.

Why is my Coinbase cost basis missing?

For the 2025 tax year, brokers like Coinbase generally report gross proceeds while cost basis reporting is still phasing in, and Coinbase cannot know the basis for crypto you bought somewhere else and transferred in. If you moved assets from another exchange or a wallet into Coinbase before selling, Coinbase often has no record of your original purchase price, so basis shows as missing, zero, or as a noncovered asset.

Does Coinbase report staking rewards?

Coinbase may report certain reward income on Form 1099-MISC. Regardless of whether a form is issued, staking rewards are taxable as ordinary income at their fair market value when you gain control of them, and that value becomes your cost basis when you later sell the reward assets.

How do I report Coinbase Advanced trades?

Coinbase Advanced trades are reported as capital gains and losses on each disposal, just like spot trades, but the volume is usually far higher. Export your full Advanced trade history, account for maker and taker fees in your basis and proceeds, separate short-term from long-term, and reconcile the totals so your Form 8949 ties to the proceeds Coinbase reports.

How do I report Base transactions?

Base activity happens on-chain, so Coinbase does not report it for you. You report Base transactions the same way you report any crypto: trades, swaps, and sales are taxable disposals, and earning tokens is income. Pull your Base wallet history, reconcile bridges in and out, and combine it with your Coinbase exchange activity so basis follows each asset across the bridge.

Can the IRS see my Coinbase account?

Yes. Coinbase is KYC verified to your identity and reports to the IRS, and the IRS runs matching programs that compare reported proceeds to what you file. If your return does not reconcile with the proceeds on your 1099-DA, that mismatch can trigger a notice such as a CP2000. Treat all Coinbase activity as visible and reportable.

What if my Coinbase 1099-DA is wrong?

First understand that a high proceeds number is usually not an error, it is gross proceeds by design. If there is a genuine factual error, contact Coinbase support to review it. In most cases the fix is not correcting the form but reconciling it: pairing the reported proceeds with your true cost basis so your Form 8949 shows the real gain or loss rather than the raw proceeds.

How do I reconcile Coinbase with Kraken?

Import both your Coinbase and Kraken histories into the same crypto tax software, then match the transfers between them so cost basis follows each asset. If you bought on Kraken and sold on Coinbase, the basis lives on Kraken and the disposal lives on Coinbase, and only by combining them do you get an accurate gain. Reconcile transfers carefully so nothing is double counted or shows a zero basis.

How do I reconcile Coinbase with Coinbase Wallet?

Coinbase the exchange and Coinbase Wallet the self-custody app are different systems. Add your Coinbase Wallet addresses and your Coinbase exchange history to one tax tool so on-chain activity and exchange activity live together. Crypto moved between them is a transfer, not a sale, but the basis must travel with it so a later disposal is not treated as zero basis.

What happens if I don't report Coinbase taxes?

Failing to report can lead to back taxes, penalties, and interest, and because Coinbase reports your proceeds to the IRS, an unreported or under-reported return is more likely to be flagged through matching. If you are behind, the safest path is to reconcile your complete history and file accurately, ideally with professional help, rather than ignoring a 1099-DA the IRS already has.

Do I owe taxes on Coinbase if I only bought crypto?

No. Buying crypto with US dollars on Coinbase is not a taxable event, it just sets your cost basis. You owe tax only when you trigger a taxable event such as selling, trading one crypto for another, spending crypto, or earning rewards. Simply buying and holding is not taxed.

Are crypto-to-crypto trades on Coinbase taxable?

Yes. Trading one cryptocurrency for another on Coinbase is a taxable disposal of the crypto you gave up, even though no US dollars are involved. You calculate a capital gain or loss based on the fair market value at the time of the trade minus your cost basis. These trades are the most commonly overlooked taxable events on exchanges.

Is converting crypto to a stablecoin on Coinbase taxable?

Yes. Converting crypto into a stablecoin like USDC or USDT is a disposal of the crypto you converted, so it is a taxable event with a gain or loss measured against your basis. Stablecoins are still property to the IRS, and moving into them does not make the underlying sale tax free.

Are Coinbase transfers to my own wallet taxable?

No. Withdrawing crypto from Coinbase to a wallet you own and control is a transfer, not a sale, so it is not taxable. The important part is that your cost basis must follow the asset, because once it leaves Coinbase the exchange no longer tracks it and a later sale could show a missing basis.

Does Coinbase issue a 1099-MISC?

Coinbase may issue Form 1099-MISC to report certain income such as rewards when it meets the reporting thresholds. Even if you do not receive one, reward and income events are still taxable as ordinary income, so you report them based on your own records of value at receipt.

What is the difference between gross proceeds and gains on Coinbase?

Gross proceeds are the total dollar amount you received from all your sales and dispositions, before subtracting anything. Gains are proceeds minus your cost basis. The 1099-DA reports gross proceeds, which can look alarmingly large, while your actual taxable gain is only the profit portion. Confusing the two is the single biggest source of Coinbase tax panic.

What are covered and noncovered assets on a 1099-DA?

Covered assets are those for which the broker is required to track and eventually report cost basis, generally tied to when reporting rules took effect and whether the asset was acquired on the platform. Noncovered assets are those where basis is not broker-reported, often because they were transferred in from elsewhere. For noncovered assets, supplying the correct basis is entirely your responsibility.

How do I reconcile my Coinbase 1099-DA?

Match the proceeds Coinbase reports to your own cost basis records for each disposal, account for assets transferred in from other platforms, remove any duplication, and produce a Form 8949 that shows real gains and losses. The goal is a return that ties to the 1099-DA proceeds total while reflecting your true basis, so the IRS matching program sees a consistent picture.

How is Coinbase staking taxed?

Staking rewards are ordinary income at fair market value when you gain control of them, potentially reported on a 1099-MISC. That income amount becomes your cost basis in the reward tokens, so when you later sell or trade them you report a separate capital gain or loss on the difference.

How are Coinbase derivatives taxed?

Coinbase derivatives such as perpetual futures are reported based on your realized profit and loss from the positions, including the effect of funding payments and liquidations. The federal treatment of crypto derivatives can be complex and depends on the product and your situation, so document every position, opening, closing, funding payment, and liquidation, and have a professional confirm the correct reporting.

What is a noncovered asset on Coinbase?

A noncovered asset is one where Coinbase is not reporting your cost basis, usually because you acquired it somewhere else and transferred it in, or because it predates the broker basis-reporting rules. For noncovered assets, the proceeds may be reported while the basis is left to you, so you must supply the original purchase price to calculate the real gain.

How do I report Coinbase taxes with high-frequency trading?

High-frequency activity on Coinbase Advanced can generate thousands of taxable disposals in a year. The only practical path is to export the complete trade history and run it through crypto tax software, ensuring fees are captured, short-term and long-term lots are separated, and the proceeds reconcile to the 1099-DA. Manual calculation is not realistic at that volume.

Are Coinbase rewards and learn-and-earn taxable?

Yes. Rewards, learn-and-earn token grants, and similar incentive payments are ordinary income at fair market value when you receive them. That value becomes your cost basis, and a later sale of those tokens produces a separate capital gain or loss. Coinbase may report some of this income on a 1099-MISC.

Do I owe taxes on Coinbase if I lost money?

Yes, and you usually want to report it. Reporting losses can reduce your taxable gains and, within limits, your ordinary income, and unused losses can carry forward. Because Coinbase reports your proceeds to the IRS, leaving losing trades off your return also makes it harder to reconcile, so report the full picture including losses.

How do I download my Coinbase tax forms?

Coinbase provides tax documents and downloadable reports through its Tax Center, including any 1099 forms, transaction reports, and gain/loss reports. Download the raw transaction history as well, not just the summary, because reconciliation and software imports rely on the complete transaction-level data, especially for transferred-in assets.

What records should I keep for Coinbase taxes?

Keep your full Coinbase transaction history, every 1099-DA and 1099-MISC, records of transfers in and out with the basis that traveled with each asset, and documentation of staking, Advanced trading, and derivatives activity. For assets bought elsewhere, keep the original purchase records so you can supply the missing basis. These records are your defense in an audit.

Does Coinbase report Base network activity?

No. Base is an on-chain network, and activity that happens on Base wallets and apps is not reported by Coinbase. You are responsible for pulling your Base history, reporting taxable swaps and sales, recognizing income, and reconciling bridges between Coinbase and Base so your basis stays consistent across the bridge.

What is the difference between Coinbase and Coinbase Wallet for taxes?

Coinbase is a custodial exchange that issues tax forms and reports to the IRS. Coinbase Wallet is a self-custody app that holds your keys and reports nothing. For taxes, the exchange gives you forms to reconcile, while the wallet leaves all recordkeeping to you. Most users have both, and the assets moving between them must be tracked so basis follows each transfer.

How do I report Coinbase Advanced fees?

Maker and taker fees on Coinbase Advanced are part of your cost of acquiring or disposing of crypto. Trading fees generally increase your cost basis when buying and reduce your proceeds when selling, which lowers your gain. Capturing fees correctly across high trade counts is one reason software reconciliation beats manual calculation.

Can the IRS send me a CP2000 for Coinbase?

Yes. A CP2000 is an automated underreporter notice the IRS sends when the income or proceeds reported to it do not match your return. Because Coinbase reports your proceeds, a return that does not reconcile with your 1099-DA can trigger a CP2000. The defense is accurate reconciliation that ties your Form 8949 to the reported proceeds.

How do I reconcile Coinbase with MetaMask?

Add your MetaMask wallet addresses and your Coinbase history to one tax tool so on-chain activity and exchange activity live together. Crypto bought on Coinbase, withdrawn to MetaMask, used in DeFi, and later sent back to Coinbase needs its basis traced across every hop. The reconciliation connects the exchange record to the on-chain record so the final gain is correct.

Are Coinbase to Coinbase Wallet transfers taxable?

No. Moving crypto between Coinbase and Coinbase Wallet is a transfer between accounts you control, not a sale, so it is not taxable. The risk is that the basis must follow the asset across the move, because once it is in self-custody the exchange stops tracking it and a later disposal could otherwise show as zero basis.

What is digital asset reconciliation for Coinbase?

Digital asset reconciliation is the process of connecting your entire crypto history, across Coinbase, other exchanges, wallets, and on-chain networks, so cost basis follows every asset and your reported gains and losses are accurate. For Coinbase users in the 1099-DA era, reconciliation is what turns a proceeds-only form into a correct, defensible tax return.

Do I have to report every Coinbase transaction?

You report every taxable event: sales, crypto-to-crypto trades, stablecoin conversions, spending, derivatives results, and income such as staking rewards. Non-taxable actions like buying, holding, and transferring between your own accounts are not taxed, but you still need their records so basis is correct when a later taxable event occurs.

How far back can the IRS audit my Coinbase taxes?

Generally the IRS can audit three years back, extended to six years if there is a substantial understatement of income, and there is no time limit in cases of fraud or unfiled returns. Because crypto records are easy to lose over time, keeping complete Coinbase and transfer history for many years is the safest practice.

Is Count On Sheep a tax filing service for Coinbase users?

Count On Sheep provides digital asset reconciliation that prepares a clean, CPA-ready picture of your complete crypto history, including your Coinbase activity, transfers, and on-chain transactions. It is the reconciliation layer that sits underneath filing, connecting everything so your gains and losses are accurate before a return is prepared.