Gemini reports your transactions. It does not know your complete crypto history. That gap is where almost every Gemini tax problem begins. Starting with the 2025 tax year, Gemini users are receiving Form 1099-DA, and many are opening it to find enormous gross proceeds with little or no cost basis. An investor who actually made a modest profit can see hundreds of thousands of dollars in reported proceeds and panic, assuming that is what they owe tax on. It is not.

This is the definitive Gemini Taxes guide for 2026. Gemini is a US-regulated, security-first centralized exchange with a strong institutional and high-net-worth user base, so the tax picture differs from a self-custody wallet like MetaMask or Phantom. We cover the 1099-DA reality, the gross-proceeds-versus-gains confusion, OTC block-trade taxes, missing cost basis, staking, transfers, the Gemini Tax Center, multi-exchange reconciliation, common mistakes, and an audit-ready checklist.

If you take one idea from this guide, make it this: the form Gemini sends you and the IRS reports what you sold for, not what you owe. The distance between those two numbers is your cost basis, and on a Gemini account that basis is frequently incomplete, scattered across other platforms, or missing entirely on assets you transferred in. Closing that gap accurately is the entire job. Everything below is in service of doing it correctly, whether you file with software, a CPA, or a reconciliation specialist.

Disclaimer: This guide is for informational purposes only and is not tax or legal advice. Cryptocurrency rules are evolving quickly, and several positions discussed here (OTC trades, institutional structures) are nuanced. Always consult a qualified CPA about your specific situation.

What Is Gemini?

Gemini is a centralized cryptocurrency exchange founded in 2014 by Cameron and Tyler Winklevoss. It built its reputation on regulatory compliance and security, positioning itself as the exchange for users who prioritize trust, including institutions, family offices, and high-net-worth individuals.

That positioning attracted a particular kind of user: people and entities moving serious money who wanted a regulated, US-based counterparty rather than an offshore venue. Over the years, Gemini layered on products aimed at that audience, from advanced trading to a dedicated OTC desk to institutional custody. The result is a user base whose tax situations are, on average, more complex and higher-stakes than those of a typical retail app. Understanding the exchange’s character helps explain why its tax guidance has to go deeper than buy, sell, and report.

Gemini Exchange Overview

Gemini operates as a New York trust company and has leaned into a security-first, compliance-forward identity since its early days. It is a US-regulated exchange, it runs full KYC on its users, and it has historically targeted serious investors and institutional clients rather than purely retail speculation. That institutional focus matters for taxes, because the accounts tend to be larger, the trades tend to be bigger, and the reporting stakes are higher.

The compliance-first identity is not just branding. It shapes how Gemini handles reporting. A platform that markets itself to regulators, institutions, and cautious high-net-worth clients is going to lean into broker reporting, not away from it. For users, that means you should assume every reportable disposal on Gemini is visible to the IRS, tied to your verified identity, and documented on a form the agency can match against your return. The upside of that transparency is that a well-reconciled Gemini return is easy to defend. The downside is that a sloppy one is easy to flag.

Gemini Products

Gemini is more than a simple buy-and-sell app. Its product surface creates several distinct tax situations:

- Spot Trading. Standard buying and selling of crypto for dollars or other crypto.

- ActiveTrader. A high-performance trading interface with advanced order types and lower fees for active traders, which means more transactions to reconcile.

- OTC Trading. A private, over-the-counter desk for large block trades, used heavily by institutions and high-net-worth clients.

- Staking. Earning rewards on certain assets, which generates ordinary income.

- Institutional Services. Custody and trading services for entities, trusts, and funds.

Why Gemini Taxes Are Different

Gemini crypto taxes work differently from a self-custody wallet because Gemini is a centralized exchange and a broker, so it handles Gemini tax reporting to the IRS and provides tax documents through its Tax Center. Three things make Gemini taxes distinct: its strong OTC and institutional activity creates large, basis-sensitive trades; its users frequently hold multiple account types and move assets across platforms; and its high-net-worth and entity clients often have complex, multi-source histories that no single form captures.

The difference shows up most clearly in the dollar amounts. A retail user on a simple buy-and-hold app might have a 1099-DA with a few thousand dollars of proceeds and basis that mostly lines up. A typical Gemini user is more likely to be selling a position built over several years, often through the OTC desk, with the original purchases scattered across other platforms and wallets. When the trade is large and the basis is somewhere else, the gap between the reported proceeds and the real gain is not a rounding error. It can be hundreds of thousands of dollars. That is why Gemini taxes reward careful reconciliation more than almost any other exchange.

There is also a transition-year effect. The 2025 tax year is the first year Form 1099-DA is in force, which means many Gemini users are seeing broker-reported proceeds for the first time. The forms are new, the basis reporting is still phasing in, and the IRS matching program now has a data feed it did not have before. Investors who filed casually in prior years are suddenly facing a form the IRS can check their return against line by line.

Gemini reports transactions. It does not know your complete crypto history.

Do You Owe Taxes on Gemini?

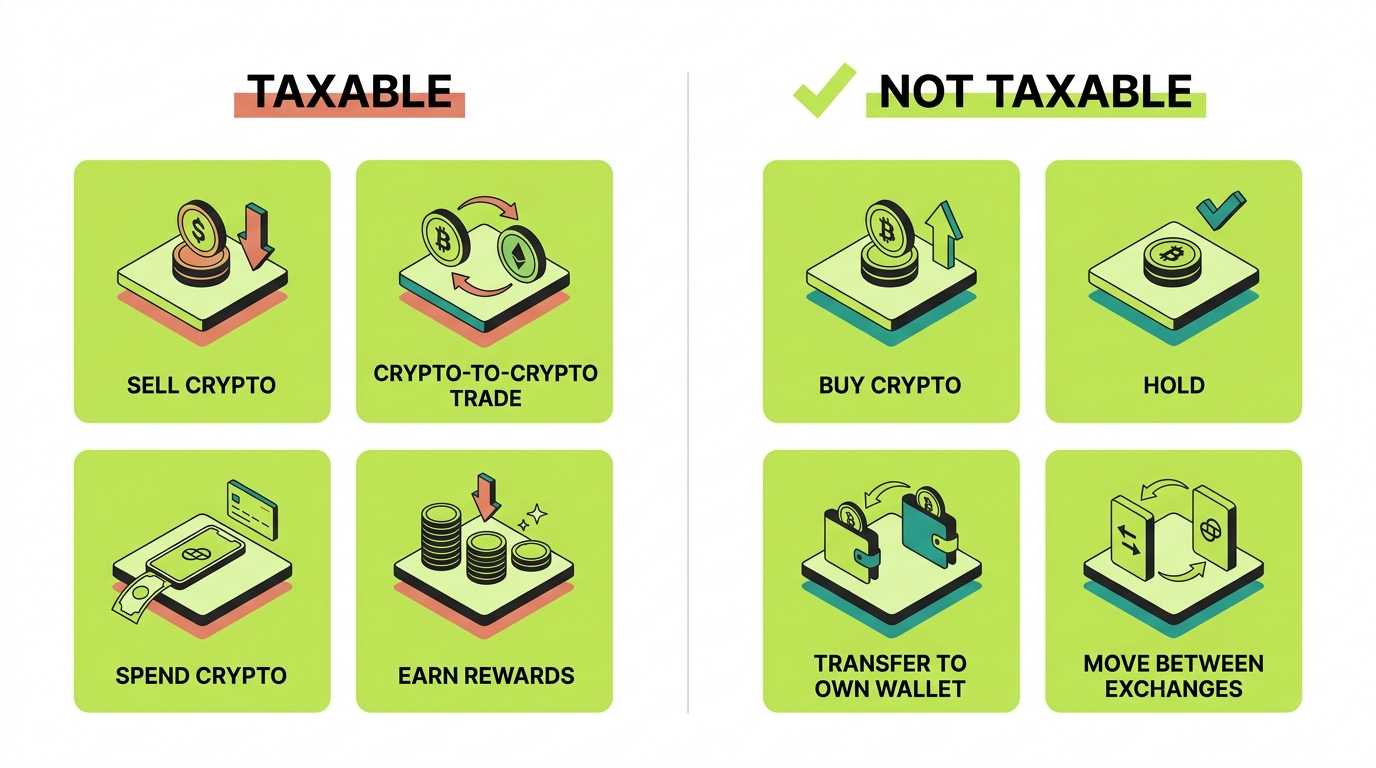

If you only ever bought crypto and held it, you likely owe nothing yet. Tax is triggered by events, not by owning crypto. Understanding which events are taxable is the foundation of everything else.

IRS Treatment of Cryptocurrency

The IRS treats cryptocurrency as property, not currency (Notice 2014-21). That single rule drives the entire system. Disposing of property triggers a capital gain or loss, and earning property as a reward triggers ordinary income. Every Gemini tax question traces back to those two ideas.

A taxable event is one where you dispose of crypto or receive new crypto as income. A non-taxable event is one where you simply acquire, hold, or move your own crypto without disposing of it.

Capital Gains Taxes

When you dispose of crypto for more than your cost basis, you have a capital gain. Hold the asset one year or less and the gain is short-term, taxed at ordinary income rates. Hold it longer than a year and the gain is long-term, taxed at preferential rates (0, 15, or 20 percent for most taxpayers). For Gemini’s longer-term holders, especially those selling large positions through OTC, the long-term rate can be the difference between a manageable bill and a painful one.

The holding period is measured per lot, from the day after you acquired each batch of coins to the day you dispose of it. This is where careful records pay off directly. If you have lots that are just short of the one-year mark, waiting a few extra days before selling can move that gain from short-term to long-term and cut the rate roughly in half for many taxpayers. On a large OTC position, that timing decision alone can be worth a substantial amount, but it only works if you know exactly which lots you hold and when you bought them. Without lot-level records, you cannot make the call with confidence, and you may default to a less favorable treatment by accident.

Ordinary Income Taxes

Some Gemini activity is taxed as ordinary income at the moment you receive it, valued at fair market value:

- Staking rewards earned on supported assets.

- Promotional rewards and incentives.

- Referral rewards for bringing in new users.

Ordinary income is taxed at your regular marginal rate, which for most investors is higher than the long-term capital gains rate. The key distinction is timing and character. Capital gains arise when you dispose of something you already owned, and the rate depends on how long you held it. Ordinary income arises when new value lands in your hands, and it is taxed immediately at full rates regardless of holding period. Crypto rewards are income the moment you control them. Only afterward, when you sell those reward coins, does the capital gains system take over for any change in value since receipt.

Common Taxable Events

The most common taxable events on Gemini are selling crypto for dollars, trading one crypto for another, spending crypto, and receiving rewards. Each of those is a moment where the IRS expects you to measure a gain, a loss, or income. The mental model worth internalizing is simple: you owe something whenever crypto leaves your hands in a disposal, or whenever new crypto arrives as income. Acquiring and holding are free. Disposing and earning are taxable. Almost every Gemini tax question can be answered by asking which of those two things just happened.

Does Gemini Report to the IRS?

Yes. Gemini is a US-regulated broker, and as a broker it has reporting obligations to the IRS that are expanding under the digital asset rules taking effect for the 2025 tax year.

What Gemini Reports

Gemini IRS reporting covers qualifying digital asset sales and dispositions through IRS-required Gemini tax forms, and the reporting is tied to your verified identity through KYC. The IRS receives information linked directly to you. What Gemini cannot report is the history that happened off its platform: purchases on other exchanges, self-custody and on-chain activity, and the original basis of assets you transferred in.

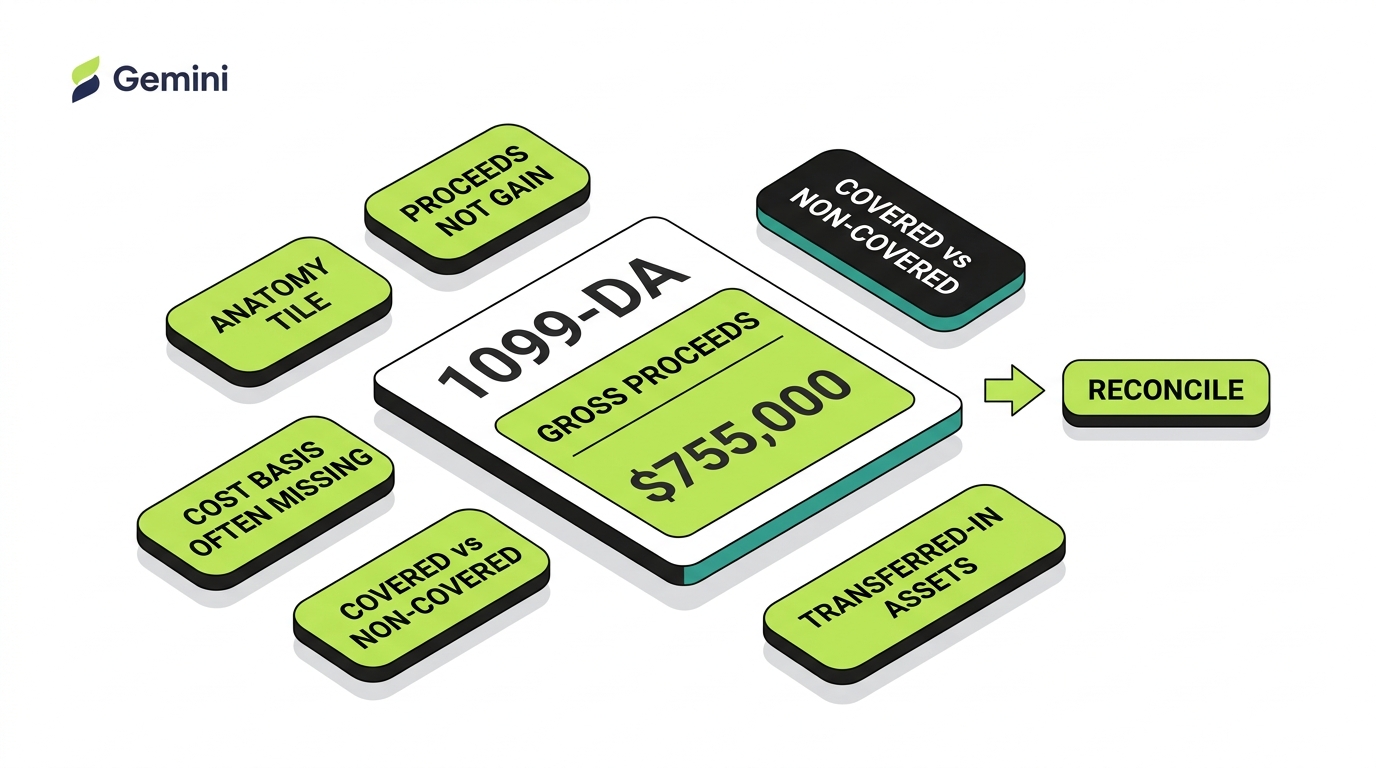

Form 1099-DA

Form 1099-DA is the new broker reporting form for digital assets, and it anchors Gemini tax forms 2026 filers will work with. It reports the gross proceeds from your reportable sales and dispositions on Gemini. If you sold or exchanged digital assets on Gemini during the tax year, you should expect to receive one through the Tax Center. The single most important fact about this form is that the number it reports is proceeds, not gain.

Form 1099-MISC

If you earned a certain threshold of reward or incentive income (such as staking rewards) on Gemini, you may also receive Form 1099-MISC reporting that income. Even if the amount is below the reporting threshold and no form is issued, the income is still taxable and you are responsible for reporting it.

IRS Matching Programs

The IRS runs automated matching programs that compare the proceeds brokers report against what taxpayers file. If your return omits Gemini activity or does not reconcile with the reported proceeds, the mismatch can generate an automated notice such as a CP2000. Filing a return that ties cleanly to your 1099-DA proceeds is the best way to avoid one.

It helps to understand how the matching actually works, because it explains why reconciliation matters so much. The system does not evaluate whether your gain calculation is correct. It checks whether the proceeds total you reported lines up with the proceeds total the broker reported. If Gemini tells the IRS you had 500,000 dollars in proceeds and your return only accounts for 200,000, the computer flags the gap automatically, often a year or more after you filed. A CP2000 notice then proposes additional tax as if the unexplained proceeds were pure gain. Responding means proving your real basis after the fact, under a deadline, which is far harder than simply reporting it correctly the first time. The lesson is to make sure your return reflects the full proceeds figure from every 1099-DA, with the correct basis subtracted, so the totals reconcile and nothing trips the match.

Understanding Gemini’s 1099-DA

This is the section that resolves the most panic, so it is worth reading slowly. The 1099-DA is not wrong when it looks enormous. It is doing exactly what it is designed to do.

What Is Form 1099-DA?

Form 1099-DA (“Digital Asset Proceeds From Broker Transactions”) is the IRS form brokers use to report your crypto sales and dispositions. For the 2025 tax year and beyond, exchanges like Gemini issue it to report the gross proceeds of your reportable transactions. The IRS gets a copy, which is why your return needs to reconcile to it.

The form exists because the digital asset reporting rules finally pulled crypto brokers into the same framework that has long applied to stock brokers. For years, the IRS received almost no third-party reporting on crypto sales, which made enforcement difficult and left honest taxpayers guessing. The 1099-DA changes that. Now the agency has a direct, account-level report of what you sold and what you received for it. The catch is that the form was designed around proceeds first, with full cost basis reporting phasing in over time, so the early versions tell only half the story: what you sold for, not what you paid.

Why Your Proceeds May Look Extremely High

Gross proceeds are the sum of everything you sold for, before subtracting what you paid. Every sale and every crypto-to-crypto trade adds its full sale value to the total. An active account, or one that sold a large position, can show a proceeds figure that dwarfs the actual profit.

Proceeds vs gain

Your Gemini 1099-DA shows 500,000 dollars in gross proceeds, and your stomach drops. But across those sales your cost basis was 460,000 dollars. Your actual taxable gain is 40,000 dollars, not 500,000. The proceeds figure is the headline number the IRS sees. The gain is what you actually owe tax on.

Proceeds vs Taxable Income

Proceeds are gross. Taxable income is net. The entire job of an accurate crypto return is converting that gross proceeds figure into a real gain by subtracting the right cost basis for every disposal. When the basis is correct, the scary proceeds number becomes a manageable gain.

Why Cost Basis May Be Missing

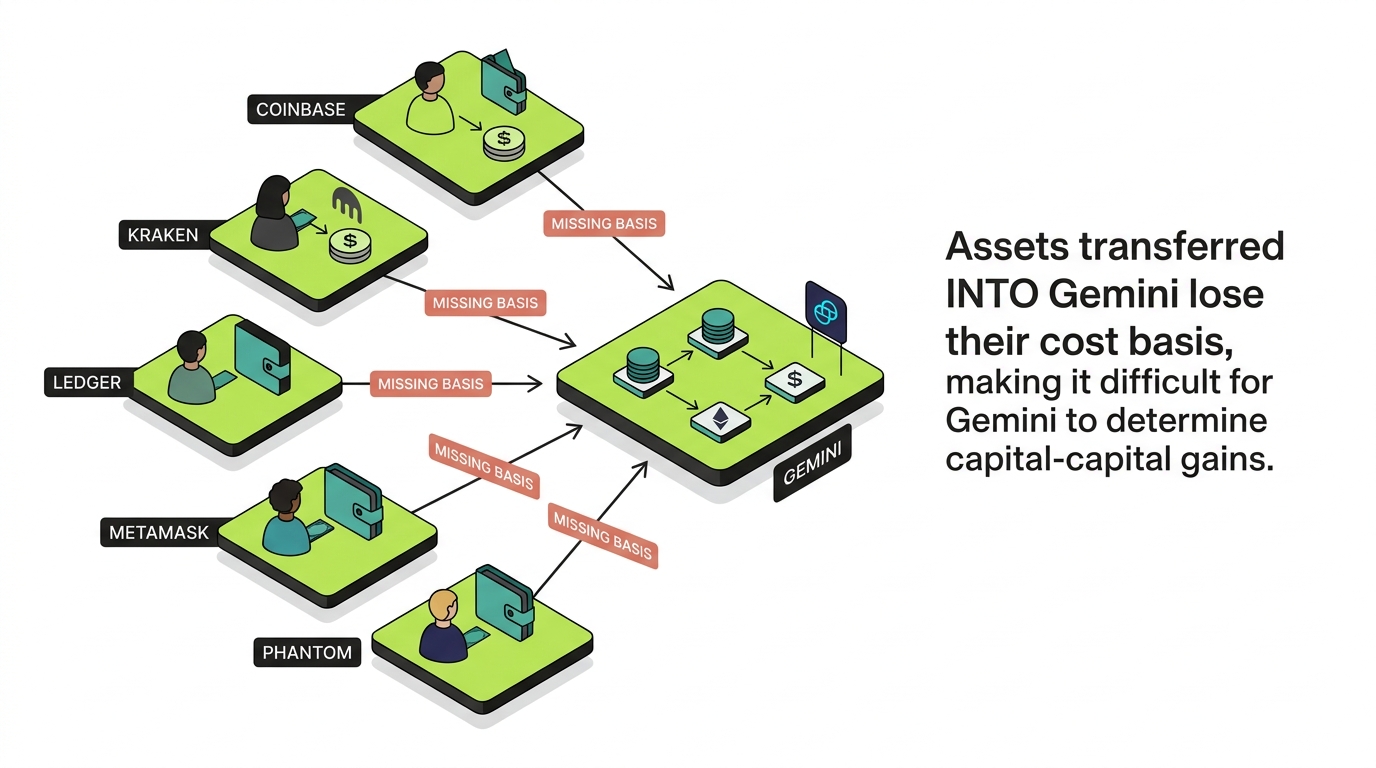

For the 2025 tax year, brokers generally report gross proceeds while full cost basis reporting is still phasing in. More importantly, Gemini simply cannot know the basis for crypto you bought somewhere else and moved in. If you bought Bitcoin on another exchange years ago, transferred it to Gemini, and sold it, Gemini sees only the deposit and the sale, not the original purchase price.

Covered vs Non-Covered Assets

A covered asset is one the broker is required to track basis for, generally tied to when reporting rules took effect and whether the asset was acquired on the platform. A non-covered asset is one where basis is not broker-reported, usually because it was transferred in. For non-covered assets, supplying the correct basis is entirely your responsibility, and most large Gemini tax problems live here.

Assets Transferred into Gemini

Any asset you transferred into Gemini from another exchange or a wallet is a prime candidate for missing basis. The deposit arrives without its purchase history attached. Unless you reconstruct and attach that basis, a later sale can look like nearly pure gain.

Common 1099-DA Misunderstandings

The most common mistakes are assuming proceeds equal gains, assuming a high number is an error, and filing directly off the form without reconciling basis. None of these are correct. The form is a starting point, not a finished tax calculation.

How to Reconcile a Gemini 1099-DA

Working out your true Gemini gains and losses means matching the proceeds Gemini reports to your own cost basis for each disposal, accounting for transferred-in assets, removing duplication, and producing a Form 8949 that shows real gains and losses while still tying to the reported proceeds total. That is the work that turns a frightening form into an accurate return.

Basis treated as zero

Your Gemini 1099-DA shows 80,000 dollars in proceeds on an asset you transferred in, with no basis attached. Tax software treats the basis as zero, so the entire 80,000 dollars looks like gain and your tax bill is dramatically overstated.

Real basis traced to the asset

The original 55,000 dollar purchase from another exchange is traced to the asset, and the transfer into Gemini is matched rather than double counted. Your Form 8949 ties to the 1099-DA proceeds while showing the real 25,000 dollar gain.

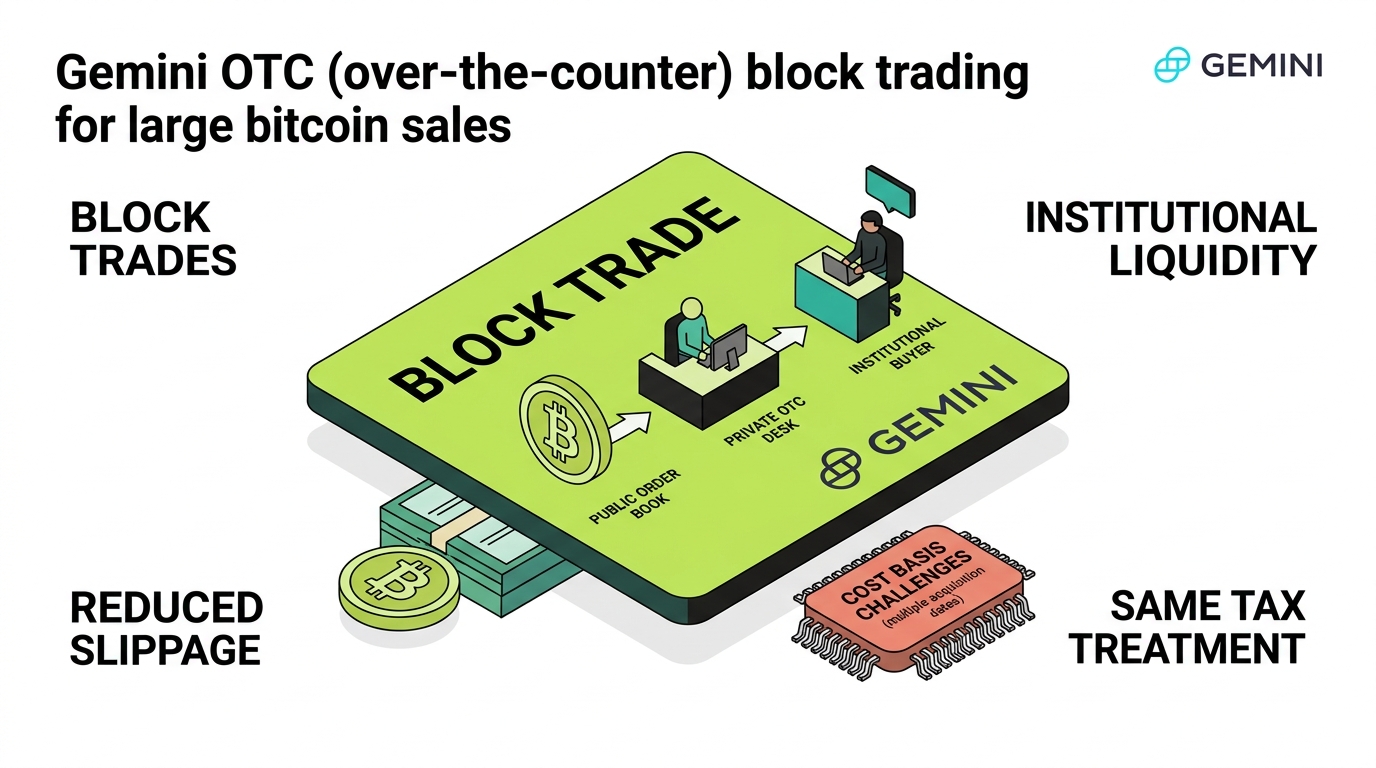

Gemini OTC Trading Taxes

This is where Gemini taxes get genuinely different from most exchanges. Gemini’s OTC desk is used heavily by institutions and high-net-worth clients, and the trades are large enough that a basis mistake can be a six- or seven-figure error.

What Is Gemini OTC?

OTC stands for over-the-counter. Instead of executing on the public order book, an OTC trade is negotiated privately as a block trade, often for very large amounts. The appeal is institutional liquidity and reduced slippage: you can move a large position without moving the market price against yourself. It is the preferred path for selling millions of dollars of Bitcoin in a single transaction.

Are OTC Trades Taxable?

Yes. OTC trades generally receive the same tax treatment as ordinary exchange trades. Selling crypto through the OTC desk is a disposal, so it produces a capital gain or loss measured by proceeds minus cost basis. The private, negotiated nature of the trade does not change the underlying rule that a disposal is a taxable event.

This surprises some people, because an OTC trade feels different from clicking sell on an app. It is negotiated, it settles privately, and it often involves a relationship with a desk rather than an order book. But from the IRS’s perspective, none of that is relevant. You disposed of property and received value for it. The mechanics of execution do not change the character of the event. A 10 million dollar OTC Bitcoin sale is taxed on exactly the same principle as a 100 dollar sale on the spot market: proceeds minus basis equals gain. The only thing that scales with the trade size is the cost of getting the basis wrong.

How OTC Bitcoin Sales Are Taxed

An OTC Bitcoin sale is taxed as a capital gain or loss. You take the proceeds and subtract your cost basis, which is what you originally paid including fees. If you held longer than a year, the gain is long-term and taxed at lower rates. The arithmetic is simple. The difficulty is establishing the basis on Bitcoin that may have been bought years ago across several sources.

Why OTC Creates Cost Basis Challenges

OTC sellers almost always have complicated acquisition histories. The Bitcoin being sold might have come from multiple acquisition dates, multiple exchanges, self-custody wallets, and historical purchases going back years. Pulling all of that into one accurate basis figure is the hard part, and it is exactly what the 1099-DA cannot do for you.

Picture a typical OTC seller. They started buying Bitcoin in 2017 on one exchange, added more in 2020 on another, received some from a business deal into a hardware wallet, and dollar-cost-averaged through a third platform. Years later they consolidate everything into Gemini and sell it all in one block trade. Gemini reports the full sale as proceeds, but the basis lives in four different places, some of which may no longer even exist as accessible accounts. Reconstructing that basis means gathering records from every source, matching each tranche of Bitcoin to its original purchase, and assembling a defensible cost figure for a sale that might be worth millions. This is not a data-entry task. It is forensic accounting, and it is the single most valuable piece of work on an OTC seller’s return.

OTC Trades and Form 1099-DA

Reportable OTC dispositions can flow onto your 1099-DA as gross proceeds, which is how a single OTC sale can make your proceeds total explode. With basis frequently missing on those large positions, the gap between reported proceeds and real gain is widest precisely where the dollars are biggest.

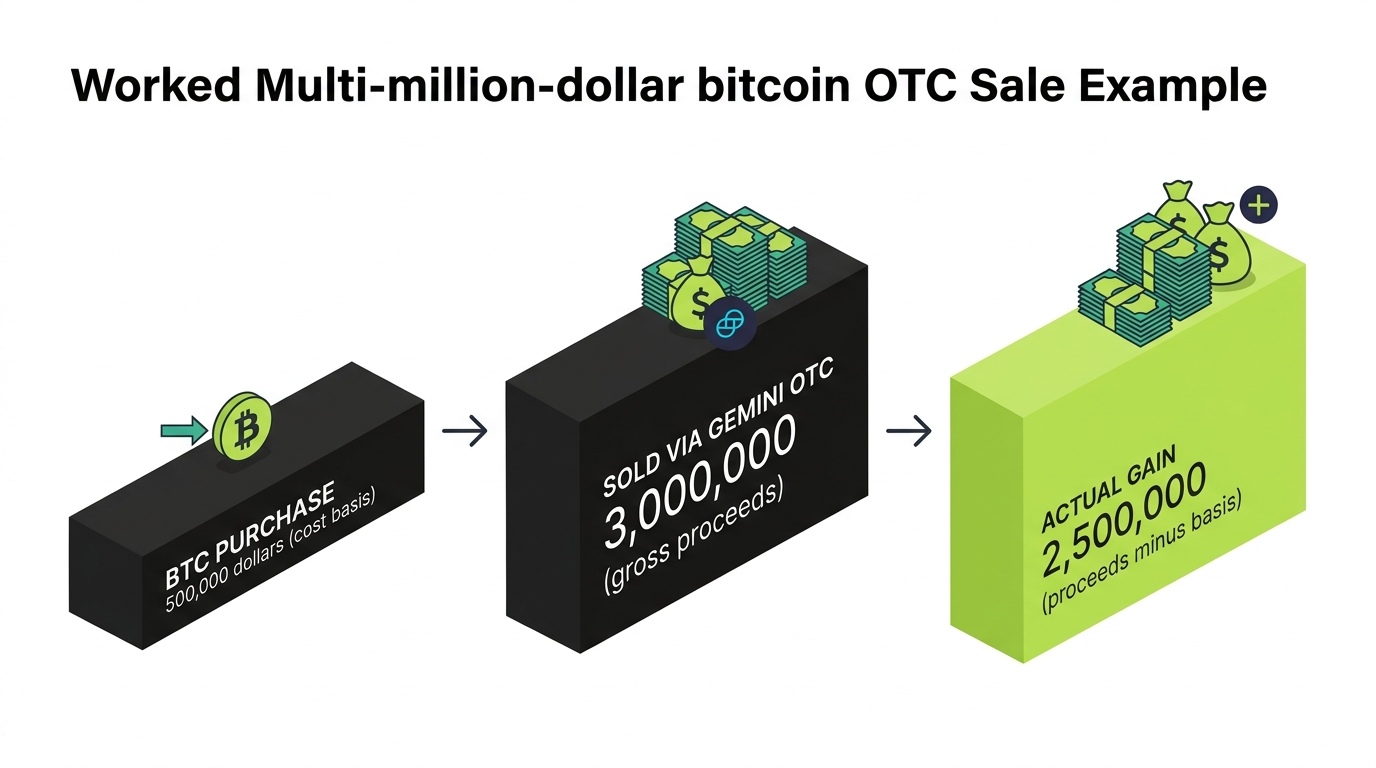

Multi-Million Dollar Bitcoin Sale Example

Consider a classic Gemini OTC scenario: a long-term holder selling a large Bitcoin position through the desk.

| Event | Amount |

|---|---|

| BTC Purchase (cost basis) | $500,000 |

| BTC Sale via Gemini OTC (proceeds) | $3,000,000 |

| Actual Gain (proceeds minus basis) | $2,500,000 |

Family Office and Institutional Considerations

OTC sellers are frequently entities, not individuals. Trusts, LLCs, and other entities each have their own filing requirements. Multi-signature wallets and third-party custody providers add layers to the recordkeeping. The tax rules underneath are the same, but the reconciliation has to tie together exchange activity, custody records, and entity structure into one defensible picture, which is rarely something software handles alone.

Gemini Transactions That Are Taxable

Here is the full list of Gemini activity that triggers tax, with the reason each one counts.

Selling Cryptocurrency

Selling crypto for US dollars is a disposal and a taxable event. You report the gain or loss as proceeds minus basis.

Crypto-to-Crypto Trades

Trading one crypto for another (for example BTC for ETH) is a taxable disposal of the crypto you gave up, even though no dollars change hands. This is the single most overlooked taxable event on every exchange. People intuitively understand that selling for dollars is taxable, but a crypto-to-crypto swap feels like a wash because no cash hit their bank account. The IRS sees it differently: you disposed of one piece of property and acquired another, so you measure a gain or loss on the asset you let go of, using its fair market value at the moment of the trade. On an active ActiveTrader account, these swaps can number in the hundreds, and each one is its own taxable line.

Stablecoin Trades

Converting crypto into a stablecoin like GUSD, USDC, or USDT is a disposal of the crypto you converted. Stablecoins are still property, so moving into them is a taxable event measured against your basis.

Spending Cryptocurrency

Using crypto to pay for goods or services is a disposal at the moment of spending, with a gain or loss based on the value at that time versus your basis.

Conversions

Any in-app conversion between assets is a disposal of the asset you converted away from, taxed like a crypto-to-crypto trade.

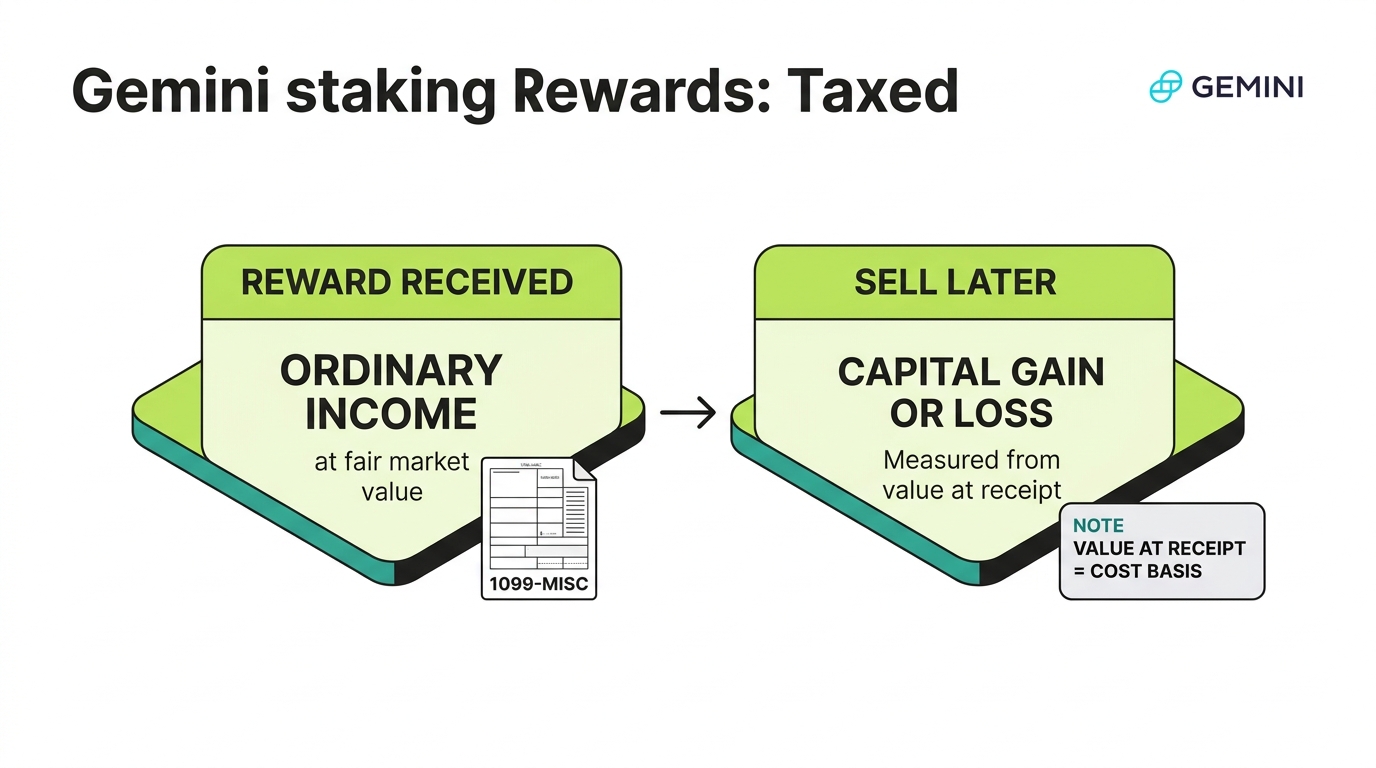

Staking Rewards

Receiving staking rewards is ordinary income at fair market value when you gain control of them. This is income first, before any later capital gain on the reward tokens. The amount you report as income is locked in at the value on the day you received it, even if the token’s price later falls. That is why keeping a dated record of every reward and its value at receipt matters: it sets both your income for the year and your basis for the eventual sale.

Promotional Rewards

Promotional and incentive rewards are generally ordinary income at their value when received.

Gemini Transactions That Are Not Taxable

Just as important is knowing what is not taxable, so you do not over-report.

Buying Cryptocurrency

Buying crypto with US dollars is not taxable. It only sets your cost basis for later.

Holding Cryptocurrency

Holding crypto, no matter how much it appreciates on paper, is not a taxable event. Tax applies only when you dispose of it.

Transfers Between Your Own Wallets

Moving crypto from Gemini to your own wallet, or vice versa, is a transfer, not a sale. It is not taxable. Your basis must follow the asset. The mistake to avoid is letting a tax tool misread the withdrawal as a sale, which would invent a taxable disposal that never happened. Label transfers as transfers, and make sure the basis is carried to wherever the asset lands so the eventual real sale is calculated correctly.

Transfers Between Exchanges

Moving crypto between exchanges you control, such as Gemini to Coinbase, Kraken, or Binance.US, is also a non-taxable transfer. The only risk is losing track of basis.

Internal Account Movements

Moving assets between your own Gemini account types or sub-accounts is not a disposal and is not taxable.

Gemini Staking Taxes

Staking is the clearest example of crypto being taxed twice in two different ways, and getting it wrong is common.

How Staking Rewards Are Taxed

Staking rewards are ordinary income at their fair market value on the date you gain control of them. That is the first taxable moment.

When Rewards Become Taxable

The income event is when you gain dominion and control over the reward, typically when it is credited to your account and you can move or sell it. You measure the dollar value at that moment.

Form 1099-MISC Reporting

Gemini may report staking rewards on Form 1099-MISC if they meet the threshold. Whether or not you receive the form, you must report the income.

Cost Basis of Reward Assets

The income amount you reported becomes your cost basis in the reward tokens. This is the link that prevents double taxation later.

Selling Staking Rewards

When you later sell or trade the reward tokens, you report a separate capital gain or loss measured from that cost basis to the sale price. The income tax and the capital gains tax are two distinct events on the same coins.

Common Staking Mistakes

The usual errors are forgetting to report the income at receipt, failing to set the reward’s cost basis, and then double-paying tax on the full sale value later because the basis was never recorded. The fix is a simple discipline: every time a reward lands, note the date and its dollar value. That single record does double duty, fixing your income for the year and your basis for the future sale, and it closes the gap that causes the double-tax mistake.

How to Calculate Gemini Cost Basis

Cost basis is what you paid for an asset including fees, and it is the number that turns proceeds into a real gain.

What Is Cost Basis?

Cost basis is your total cost to acquire an asset, including the purchase price and any fees. When you sell, your gain or loss is the proceeds minus this basis.

Why Cost Basis Matters

Basis is the entire game. With accurate basis, a large proceeds figure becomes a modest gain. With missing basis defaulting to zero, the same sale looks like nearly pure profit and the tax is massively overstated. The asymmetry is brutal: a missing basis never works in your favor. It can only inflate your gain and your tax. Every dollar of basis you fail to document is a dollar of phantom gain you pay tax on. That is why, for a Gemini user, hunting down and proving cost basis is not bookkeeping busywork. It is the highest-return tax task you can do, often worth far more per hour than anything else on the return.

FIFO Method

FIFO (First In, First Out) assumes the first coins you bought are the first ones you sold. It is the common default and is straightforward, though it can produce larger gains in a rising market.

Specific Identification

Specific Identification lets you choose exactly which lots you are selling, which can minimize gains if you have good records. It requires detailed documentation of each lot’s acquisition date and price. Done well, it is a powerful tool: by selling your highest-basis lots first, you can reduce the gain on a sale and keep your lower-basis coins for a future long-term sale at preferential rates. The trade-off is recordkeeping. Specific Identification only holds up if you can show, at the time of the sale, exactly which lot you intended to sell. For a Gemini OTC seller liquidating a large position, choosing the right lots can shift the tax bill substantially, which is another reason accurate, lot-level basis records are worth the effort.

Wallet-Level Tracking

Current IRS guidance points toward tracking basis on a per-account, per-wallet basis rather than universally pooling it. That makes keeping each platform’s records clean even more important.

Multi-Exchange Tracking

Because crypto moves between platforms, basis has to be tracked across all of them as one connected history. A coin bought on Coinbase, moved to Gemini, and sold there carries its Coinbase basis with it.

Missing Cost Basis Scenarios

Missing basis almost always traces to assets bought elsewhere and transferred in, old purchases with lost records, or rewards whose receipt value was never recorded. Each of these is reconstructable, but only with deliberate effort.

Gemini Transfers and Missing Cost Basis

This is one of the highest-value sections for accuracy, because transfers are where basis most often disappears.

Coinbase to Gemini

Transferred crypto is the heart of the basis problem. Crypto bought on Coinbase and moved to Gemini keeps its Coinbase basis, but Gemini does not see it. You reconcile the two so the Gemini sale reflects the real Coinbase purchase price.

Kraken to Gemini

Same pattern with Kraken: the basis lives on Kraken, the disposal lives on Gemini, and only by combining the histories do you get an accurate gain.

Ledger to Gemini

Crypto sent from a Ledger hardware wallet into Gemini arrives without purchase history. You supply the original acquisition cost yourself.

MetaMask to Gemini

On-chain assets moved from MetaMask into Gemini carry basis that must be reconstructed from the original on-chain purchases and any DeFi activity along the way.

Phantom to Gemini

Solana assets moved from Phantom into Gemini have the same issue: the basis is set by the original Phantom-side acquisition, not by the Gemini deposit.

Self-Custody Wallet Transfers

Any transfer from a wallet you control into Gemini is non-taxable, but it severs the visible basis trail unless you reconnect it.

Historical Crypto Purchases

Old purchases, sometimes years before the transfer, are the hardest to document and the most valuable to recover, because they often carry the lowest basis and therefore the largest unrealized gain.

How Cost Basis Gets Lost

Basis is lost when assets cross platforms without their purchase records, when records were never kept, or when a tax tool imports only the Gemini side of the story. The deposit shows up; the history does not.

How to Reconstruct Cost Basis

Reconstruction means going back to the source platform’s records, matching each transferred asset to its original purchase, and attaching that basis to the eventual Gemini disposal. This is the core of professional reconciliation. In practice it draws on whatever evidence exists: old exchange CSV exports, on-chain transaction records tied to your wallet addresses, bank or card statements showing the original fiat purchase, and historical price data to value any rewards or swaps. Each asset is traced backward from the Gemini sale to its true origin, and the basis is rebuilt from the documentation rather than guessed. When the original records are genuinely gone, defensible estimation methods exist, but they should be applied carefully and documented, because the IRS expects a reasonable, supportable basis rather than a convenient one.

Gemini Tax Center Explained

Your Gemini tax documents and reports live in the Tax Center, and pulling the right data is the first practical step toward an accurate return.

Accessing the Tax Center

Sign in to your Gemini account and open the tax or documents area (on the web, through your account settings; in the mobile app, through the account menu). This is where your forms, statements, and report generators live. Note that the Tax Center reflects activity on Gemini only, not assets while they lived on other platforms or in your own wallets.

A practical sequence looks like this:

- Sign in to Gemini on the web at the account level.

- Open your account settings or profile menu and find the tax documents or statements section.

- Select the tax year you are filing for.

- Download every available form for that year (1099-DA, and 1099-MISC if issued).

- Generate and download the full transaction history as a CSV, using a January 1 to December 31 date range.

- Download any gain/loss statement Gemini provides, but treat it as an estimate to be verified.

Downloading Tax Forms

Download every 1099 Gemini issues you, including any 1099-DA (gross proceeds) and 1099-MISC (reward income). These are the forms the IRS already has, so your return must reconcile to them, and keeping copies is part of your audit defense.

Downloading Transaction History

Download the complete transaction history, not just the summary. The raw, transaction-level CSV is what tax software imports rely on, and it is essential for reconciling transferred-in assets and OTC trades. Generate it for the full calendar year (January 1 to December 31) so nothing is missed.

Gain/Loss Statements

Gemini may offer a gain/loss statement that estimates your results, but it reflects only what Gemini knows. For assets with off-platform basis, those numbers can be inaccurate until reconciled with your full history. Treat the statement as an estimate, not a filing-ready figure.

Reviewing Tax Documents

Review every document against your own records before filing. Confirm that proceeds match your expectations, flag any disposal with missing basis, and identify transferred-in assets that need basis reconstruction. This review is where most reconciliation work is scoped: once you can see which disposals have clean basis and which do not, you know exactly how much reconstruction the return actually requires before it is safe to file.

Common Reporting Errors

The most common errors are relying on the summary instead of the raw history, missing transferred-in basis, and failing to capture OTC and staking activity correctly. Each is avoidable with a full export and careful reconciliation.

How to Report Gemini Taxes

Once your data is reconciled, reporting follows a defined set of IRS forms.

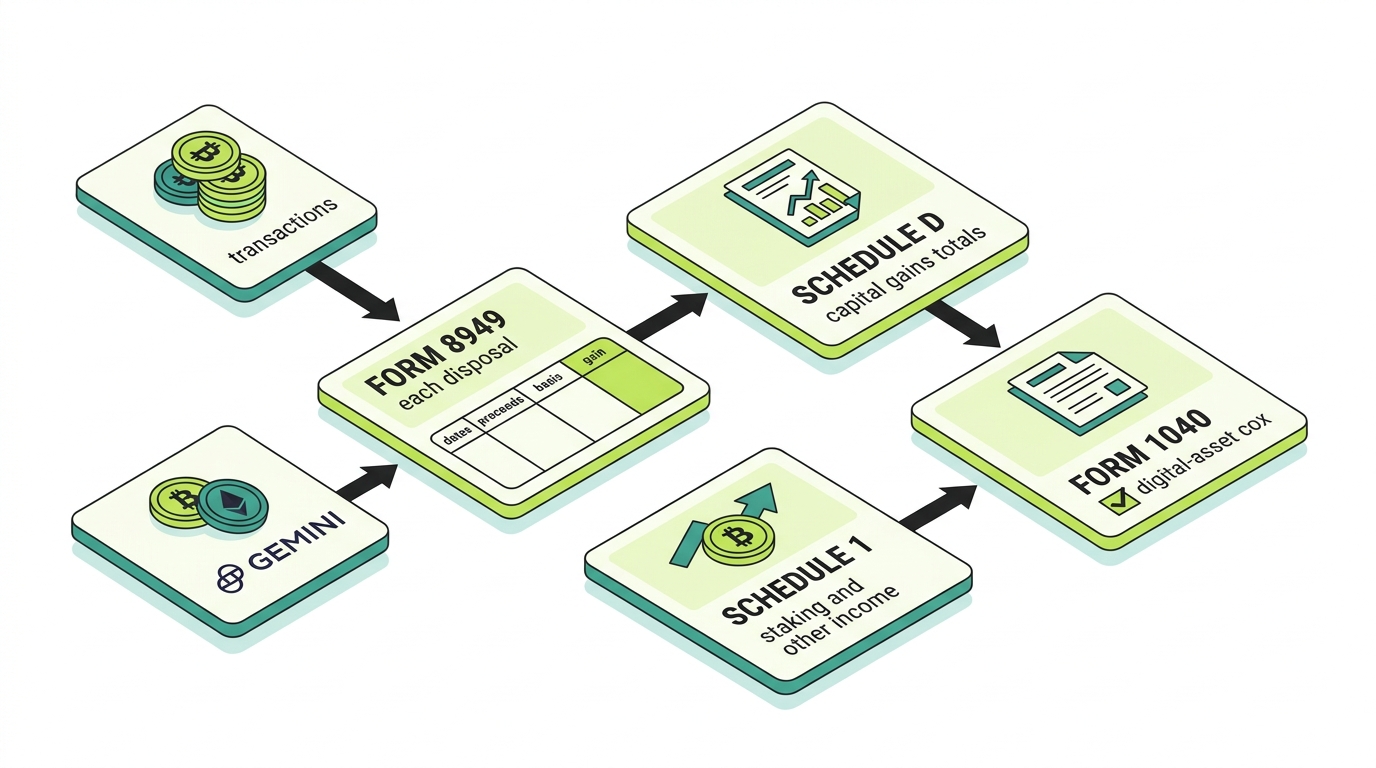

Form 8949

Report each taxable disposal on Form 8949 with the acquisition and sale dates, proceeds, cost basis, and resulting gain or loss. This is where reconciled basis does its work. Each disposal gets its own line, split between short-term and long-term sections based on holding period, and assets with broker-reported basis are separated from those where you supply the basis yourself. For a busy account, this form can run to many pages, which is exactly why a clean import and accurate basis matter: every line has to be right, and the totals have to tie back to the proceeds the IRS already received.

Schedule D

Carry the totals from Form 8949 to Schedule D, which summarizes your short-term and long-term capital gains and losses.

Schedule 1

Report staking and other crypto income as ordinary income, generally on Schedule 1 (or Schedule C if it rises to the level of a trade or business).

Staking Income Reporting

Staking income goes in as ordinary income at its receipt value, separate from the capital gains you report when you later sell the reward tokens.

Reconciling Gemini with Other Exchanges

If you used other exchanges, combine all of their histories so transfers are matched and basis follows each asset. Your Form 8949 should reflect the complete, connected picture, not just the Gemini slice.

Reconciling Gemini with Wallets

Add your self-custody wallet activity to the same reconciliation so on-chain purchases, DeFi, and transfers are tied to the exchange disposals. This is what produces a return that actually reflects reality.

Best Gemini Tax Software

Software is a powerful first pass, but on a complex Gemini history it is a starting point, not a finish line.

CoinTracker

A widely used tool with broad exchange and wallet support and strong reconciliation features.

Koinly

Popular for its clean interface and multi-country support, with good handling of transfers and many exchanges.

CoinLedger

Known for a straightforward import-and-export flow that generates a Form 8949.

TokenTax

Geared toward more complex situations and offers professional services alongside the software.

ZenLedger

Another full-featured option with exchange and wallet integrations and tax-form output.

Summ

A newer reconciliation-focused tool aimed at cleaning up messy multi-source histories.

When Software Alone Isn’t Enough

No tool fully automates a messy, multi-platform history. On Gemini accounts with OTC trades, transferred-in assets, missing basis, staking, and entity structures, plan to review every import for zero-basis disposals, unmatched transfers, and mislabeled income. That review is exactly where reconciliation specialists earn their fee.

The failure mode is predictable. You connect Gemini and a couple of other accounts, the software ingests everything, and it produces a Form 8949 that looks complete. But under the hood, transferred-in assets defaulted to zero basis, a transfer between two of your own accounts got booked as a sale, and a batch of staking rewards landed as both income and a zero-basis disposal. The output is a clean-looking document built on dirty data. For a small, single-exchange history that might be fine. For a Gemini account with a seven-figure OTC sale and assets that lived on three other platforms first, those quiet errors can swing the tax bill by six figures in either direction. Software is the right first pass. It is rarely the right last word.

Common Gemini Tax Mistakes

These are the recurring errors that create overpayment, IRS notices, or both.

Trusting 1099-DA Alone

The form shows gross proceeds, not gains, and it often lacks basis. Filing straight from it is the number-one mistake.

Missing Cost Basis

Letting transferred-in assets default to zero basis overstates gains, sometimes dramatically on large OTC positions.

Ignoring Transfers

Treating a transfer as a sale (or losing its basis) corrupts the whole calculation.

Ignoring Wallet Activity

Leaving self-custody and on-chain activity out means the exchange disposals lack their true basis.

Ignoring Staking Income

Forgetting to report rewards at receipt, or failing to set their basis, causes both under-reporting and later double taxation.

Duplicate Transactions

Importing the same activity from overlapping sources can double count proceeds and inflate the return.

Missing Historical Records

Old purchases with lost documentation are where the largest unrecorded basis hides.

Failing to Reconcile OTC Activity

Large OTC sales with unreconciled basis produce the biggest single-line errors on any Gemini return.

Assuming Proceeds Equal Gains

The root misconception behind most Gemini tax panic. Proceeds are gross; gains are net.

How to Prepare for a Gemini Tax Audit

Because Gemini reports to the IRS and serves large accounts, audit readiness is not paranoia, it is good hygiene.

Keeping Exchange Records

Keep your full Gemini transaction history and every issued form. These are your primary records.

Maintaining Wallet Records

Keep records of every self-custody wallet address you used, so on-chain activity can be tied to your exchange activity.

Tracking Transfers

Document every transfer in and out, including the basis that traveled with each asset, so no disposal shows an unexplained zero basis. A transfer record should connect the dots: this asset left this account on this date with this basis, and arrived in Gemini on this date. When that chain is documented, an auditor can follow the basis from original purchase to final sale without gaps. When it is missing, every transferred-in disposal becomes a question you have to answer under pressure rather than evidence you can simply hand over.

Supporting Cost Basis

Keep the original purchase records for assets bought elsewhere. This is the documentation that defends your reported basis.

Reconciling Tax Forms

Make sure your return ties to your 1099-DA and 1099-MISC. A clean reconciliation is the best answer to an IRS matching notice.

Audit Documentation Checklist

Keep these ready before you ever need them:

When Tax Software Isn’t Enough

There is a clear line where a do-it-yourself import stops being safe, and Gemini accounts cross it more often than most.

Signs You Need Professional Reconciliation

Get professional help when you see any of these: missing cost basis, multiple exchanges, self-custody wallets, OTC trading, large portfolios, staking, or DeFi activity. Each one multiplies the chance that software alone produces a wrong, and usually overstated, return.

The pattern to watch for is compounding complexity. Any one of these factors on its own might be manageable with good software and patience. The trouble is that Gemini users rarely have just one. A single account can easily combine a large OTC sale, assets transferred in from two other exchanges and a hardware wallet, a year of staking rewards, and some DeFi activity that ran through a self-custody wallet. Each factor interacts with the others, and the errors multiply rather than add. When two or more of these are present, the cost of getting it wrong almost always exceeds the cost of getting it reconciled properly.

What Is Digital Asset Reconciliation (DAR)?

Digital Asset Reconciliation (DAR) is the process of connecting every exchange, wallet, and custody source you used, matching transfers so basis follows each asset, handling income and OTC events correctly, and producing a defensible Form 8949 and income report that ties to your 1099 forms. It is the missing layer between raw exchange data and an accurate filing.

Think of DAR as the step that happens before tax preparation, not as a replacement for it. Your CPA or tax software takes finished numbers and puts them on the right forms. DAR is what produces those finished numbers in the first place, by turning a pile of disconnected exports, wallet addresses, and 1099s into a single, reconciled, defensible history. For simple situations, the tax software does enough of this on its own. For Gemini users with the complexity described above, DAR is the difference between a return that merely looks complete and one that is actually correct and audit-ready.

Why DAR Matters for Gemini Users

Gemini users skew toward exactly the profile where DAR matters most: larger balances, OTC and institutional activity, multiple platforms, and assets with long, transferred-in histories. The 1099-DA gives you proceeds. DAR gives you the truth behind them.

Think about where the average Gemini user’s crypto actually lives. Some was bought on Coinbase in 2020. Some came off a Ledger that has been sitting in a drawer. Some moved through MetaMask and a few DeFi protocols. Some was earned as staking rewards. And a large chunk was sold in a single OTC block trade last year. Gemini issued a 1099-DA for the sale, but it has no idea about any of the history that led up to it. The proceeds are real and reported. The basis is scattered across five places Gemini cannot see.

That is the precise problem DAR solves. Reconciliation pulls every source into one timeline, matches each transfer so basis follows the asset across every hop, classifies income and disposals correctly, removes duplicates created by overlapping imports, and outputs a Form 8949 and income summary that tie cleanly to the 1099 forms the IRS already holds. The result is a return that is both accurate and defensible, which is what matters if a notice or audit ever arrives.

Count On Sheep is the reconciliation layer that sits underneath filing. We are not a tax filing service and we do not replace your CPA. We make sure the numbers your CPA files are right. For Gemini users with OTC activity, multiple platforms, or large transferred-in positions, that reconciliation is usually the difference between a return built on guesses and one built on evidence.

Not sure your crypto taxes are right?

Talk to a Count On Sheep specialist. We will spot the costly errors before you file. No obligation.

Book My Free Review- Reviewed by Former Big 4 Accountants

- Keep your CPA

- No pressure, no sales pitch

Related Reading

- Coinbase Tax Guide (2026)

- Kraken Tax Guide (2026)

- Binance.US Tax Guide (2026)

- MetaMask Tax Guide (2026)

- Phantom Wallet Tax Guide (2026)

- How Is Crypto Taxed in the US (2026)

- Form 1099-DA Explained (2026)

- How to File Crypto Taxes with Form 8949 and Schedule D

- Per-Wallet Crypto Cost Basis and Rev. Proc. 2024-28

- Crypto Income Tax: Staking, Mining and Airdrops (2026)

- FIFO vs HIFO vs Specific ID for Crypto Taxes

- Crypto Tax Loss Harvesting and the Wash Sale Rule (2026)

- NFT and DeFi Taxes: Liquidity Pools, Staking and Lending

Official IRS Resources

For the primary source rules behind this guide, see the IRS directly:

- IRS: Digital Assets

- IRS Notice 2014-21 (crypto treated as property)

- IRS: About Form 8949

- IRS: About Schedule D (Form 1040)

- IRS: About Form 1099-DA

Gemini Tax FAQ

Frequently Asked Questions

Does Gemini report to the IRS?

Yes. Gemini is a centralized, US-regulated exchange and a broker for tax purposes, so it reports certain digital asset activity to the IRS. Starting with the 2025 tax year, Gemini provides Form 1099-DA for reportable digital asset sales and dispositions, and it may also issue Form 1099-MISC for certain income such as staking rewards. Your identity is tied to your account through KYC, so the IRS receives reporting linked to you.

Does Gemini issue Form 1099-DA?

If you had reportable digital asset sales or dispositions on Gemini, yes, you should expect a Form 1099-DA through the Gemini Tax Center for the 2025 tax year and beyond. The form reports gross proceeds from your dispositions. Always download and reconcile it against your own records, because the proceeds figure is not your taxable gain.

Why is my Gemini 1099-DA so high?

Because the 1099-DA reports gross proceeds, not gain. Every sale and crypto-to-crypto trade adds its full proceeds to the total, so an account that traded actively can show hundreds of thousands or even millions in proceeds while the actual taxable gain is a small fraction of that. The proceeds number is the sum of what you sold for, before subtracting what you paid. It is not what you owe tax on.

Why is my Gemini cost basis missing?

For the 2025 tax year, brokers like Gemini generally report gross proceeds while cost basis reporting is not yet fully required, and Gemini cannot know the basis for crypto you bought somewhere else and transferred in. If you moved assets from another exchange or a wallet into Gemini before selling, Gemini often has no record of your original purchase price, so basis shows as missing or zero.

Does Gemini report staking rewards?

Gemini may report certain reward income on Form 1099-MISC. Regardless of whether a form is issued, staking rewards are taxable as ordinary income at their fair market value when you gain control of them, and that value becomes your cost basis when you later sell the reward assets.

Are Gemini OTC trades taxable?

Yes. Gemini OTC (over-the-counter) trades generally receive the same tax treatment as ordinary exchange trades. Selling crypto through the OTC desk is a disposal, so it is a taxable event with a capital gain or loss measured by the proceeds minus your cost basis. The private, block-trade nature of OTC does not change the underlying tax rules.

Does Gemini OTC report to the IRS?

OTC sales of digital assets executed through Gemini are subject to the same broker reporting framework as other dispositions, so reportable OTC activity can appear on your 1099-DA as gross proceeds. Because OTC trades are often large and frequently involve assets acquired years earlier or on other platforms, the missing-basis problem is especially common, which makes reconciliation essential.

How are OTC Bitcoin sales taxed?

An OTC Bitcoin sale is taxed as a capital gain or loss. You take the proceeds from the sale and subtract your cost basis, which is what you originally paid for that Bitcoin, including fees. If you held the Bitcoin for more than a year, the gain is long-term and taxed at lower rates. The challenge with OTC is establishing the correct basis when the Bitcoin was bought long ago or across multiple sources.

Are transfers between Gemini and Coinbase taxable?

No. Moving crypto between Gemini and Coinbase, both exchanges you control, is a transfer, not a sale, so it is not taxable. The risk is purely about basis: if the original purchase history does not follow the asset, the later sale can appear to have no cost basis and overstate your gain. Reconcile transfers so basis travels with each asset.

Are transfers from Ledger to Gemini taxable?

No. Sending crypto from your Ledger hardware wallet into Gemini is a transfer between things you own, not a disposal, so it is not a taxable event. But Gemini sees only the deposit, not what you paid when you first acquired the asset, so you must supply the original cost basis yourself when you later sell on Gemini.

Can the IRS see my Gemini account?

Yes. Gemini is KYC verified to your identity and reports to the IRS, and the IRS runs matching programs that compare reported proceeds to what you file. If your return does not reconcile with the proceeds on your 1099-DA, that mismatch can trigger a notice. Treat all Gemini activity as visible and reportable.

What if my Gemini 1099-DA is incorrect?

First understand that a high proceeds number is usually not an error, it is gross proceeds by design. If there is a genuine factual error, contact Gemini support to review it. In most cases the fix is not correcting the form but reconciling it: pairing the reported proceeds with your true cost basis so your Form 8949 shows the real gain or loss rather than the raw proceeds.

How do I calculate gains on Gemini?

For each disposal, take the proceeds you received and subtract your cost basis, which is what you paid for that asset including fees. The result is your capital gain or loss. Hold longer than a year and the gain is long-term, taxed at lower rates. The hard part is establishing accurate basis across all the places you bought and moved the asset, not the subtraction itself.

How do I report Gemini staking rewards?

Report staking rewards as ordinary income at their fair market value on the date you gained control of them, generally on Schedule 1 (or Schedule C if it rises to a trade or business). That value becomes your cost basis in the reward tokens, so when you later sell or trade them you report a separate capital gain or loss on Form 8949 for the difference.

How do I report Gemini OTC transactions?

Report each OTC disposal on Form 8949 with the acquisition and sale dates, the proceeds, your cost basis, and the resulting gain or loss, then carry the totals to Schedule D. Because OTC trades are large, accurate basis is critical: a missing basis on a multi-million-dollar sale can overstate your gain enormously, so reconcile the full acquisition history before filing.

How do I reconcile Gemini with Coinbase?

Import both your Gemini and Coinbase histories into the same crypto tax software, then match the transfers between them so cost basis follows each asset. If you bought on Coinbase and sold on Gemini, the basis lives on Coinbase and the disposal lives on Gemini, and only by combining them do you get an accurate gain. Reconcile transfers carefully so nothing is double counted or shows a zero basis.

How do I reconcile Gemini with Kraken?

Add both your Gemini and Kraken transaction histories to one tax tool and match the transfers between the two exchanges. Crypto bought on Kraken, moved to Gemini, and sold there needs its basis traced across the hop so the Gemini disposal reflects the true Kraken purchase price. Reconciling the two prevents a missing or zero basis from inflating your reported gain.

What happens if I don't report Gemini taxes?

Failing to report can lead to back taxes, penalties, and interest, and because Gemini reports your proceeds to the IRS, an unreported or under-reported return is more likely to be flagged through matching. If you are behind, the safest path is to reconcile your complete history and file accurately, ideally with professional help, rather than ignoring a 1099-DA the IRS already has.

What records should I keep for an audit?

Keep your full Gemini transaction history, every 1099-DA and 1099-MISC, records of transfers in and out with the basis that traveled with each asset, OTC trade confirmations, and documentation of staking activity. For assets bought elsewhere, keep the original purchase records so you can supply the missing basis. These records are your defense in an audit.

When should I hire a crypto tax professional?

Consider professional help when you have missing cost basis, activity across multiple exchanges and self-custody wallets, OTC trading, a large portfolio, staking, or DeFi activity. At that point, software alone often cannot produce a clean, defensible return, and a reconciliation specialist who connects every source and traces basis across transfers becomes worth far more than the fee.

Do I owe taxes on Gemini if I only bought crypto?

No. Buying crypto with US dollars on Gemini is not a taxable event, it just sets your cost basis. You owe tax only when you trigger a taxable event such as selling, trading one crypto for another, spending crypto, or earning rewards. Simply buying and holding is not taxed.

Are crypto-to-crypto trades on Gemini taxable?

Yes. Trading one cryptocurrency for another on Gemini is a taxable disposal of the crypto you gave up, even though no US dollars are involved. You calculate a capital gain or loss based on the fair market value at the time of the trade minus your cost basis. These trades are the most commonly overlooked taxable events on exchanges.

Is converting crypto to a stablecoin on Gemini taxable?

Yes. Converting crypto into a stablecoin like GUSD, USDC, or USDT is a disposal of the crypto you converted, so it is a taxable event with a gain or loss measured against your basis. Stablecoins are still property to the IRS, and moving into them does not make the underlying sale tax free.

What is the difference between gross proceeds and gains on Gemini?

Gross proceeds are the total dollar amount you received from all your sales and dispositions, before subtracting anything. Gains are proceeds minus your cost basis. The 1099-DA reports gross proceeds, which can look alarmingly large, while your actual taxable gain is only the profit portion. Confusing the two is the single biggest source of Gemini tax panic.

What are covered and non-covered assets on a 1099-DA?

Covered assets are those for which the broker is required to track and eventually report cost basis, generally tied to when reporting rules took effect and whether the asset was acquired on the platform. Non-covered assets are those where basis is not broker-reported, often because they were transferred in from elsewhere. For non-covered assets, supplying the correct basis is entirely your responsibility.

How do I reconcile my Gemini 1099-DA?

Match the proceeds Gemini reports to your own cost basis records for each disposal, account for assets transferred in from other platforms, remove any duplication, and produce a Form 8949 that shows real gains and losses. The goal is a return that ties to the 1099-DA proceeds total while reflecting your true basis, so the IRS matching program sees a consistent picture.

Is Gemini my entire crypto tax picture?

Almost never. Most Gemini users also use other exchanges and self-custody wallets, and crypto moves between all of them. Gemini reports only what happened on Gemini, so a complete and accurate return requires connecting Gemini to every other platform and wallet you used. Gemini reports transactions, it does not know your entire crypto history.

Does Gemini work with TurboTax?

Not as a finished return. The usual path is to export your Gemini history or connect it to crypto tax software like CoinTracker, Koinly, or CoinLedger, which generates a Form 8949 you can then import into TurboTax or give to your preparer. The Gemini Tax Center provides summaries and forms, but the reconciliation work still has to happen.

How do I get my Gemini tax documents?

Use the Gemini Tax Center, which provides tax summaries, downloadable forms such as the 1099-DA and any 1099-MISC, transaction reports, and gain/loss statements. Download everything, including raw transaction history, because the summaries alone are not enough to build an accurate, reconciled return.

How are family office or institutional Gemini accounts taxed?

The underlying tax rules are the same, but entity structures add complexity. Trusts, LLCs, and other entities have their own filing requirements, multi-signature and custody arrangements complicate the records, and large OTC positions raise the stakes on basis accuracy. These accounts almost always need professional reconciliation that ties the entity's exchange, custody, and wallet activity into one defensible picture.

What is the biggest Gemini tax mistake?

Trusting the 1099-DA alone. The form shows gross proceeds, not gains, and it often lacks basis for transferred-in assets and large OTC sales. Filing straight from the proceeds number, or ignoring the form because it looks wrong, both lead to errors. The fix is reconciliation: pairing reported proceeds with true basis across all your accounts.

Can Count On Sheep help with Gemini taxes?

Yes. Count On Sheep provides CPA-ready Digital Asset Reconciliation for Gemini users: connecting Gemini to your other exchanges and wallets, matching transfers so basis follows each asset, handling staking and OTC activity, reconciling against your 1099-DA and 1099-MISC, and producing a defensible Form 8949 and income report. We are a reconciliation service that works alongside your tax preparer.