Kraken reports your transactions. It does not know your entire crypto history. That gap is where almost every Kraken tax problem begins. Starting with the 2025 tax year, Kraken users are receiving Form 1099-DA, and many are opening it to find enormous gross proceeds with little or no cost basis. A trader who actually made a modest profit can see hundreds of thousands of dollars in reported proceeds and panic, assuming that is what they owe tax on. It is not.

This is the definitive Kraken Taxes guide for 2026. Kraken is a centralized exchange, not a self-custody wallet, so the tax picture is different from MetaMask, Phantom, or Coinbase Wallet. We cover the 1099-DA reality, the gross-proceeds-versus-gains confusion, missing cost basis, staking, margin trading, futures, the Kraken Tax Center, multi-exchange reconciliation, common mistakes, and an audit-ready checklist.

Disclaimer: This guide is for informational purposes only and is not tax or legal advice. Cryptocurrency rules are evolving quickly, and several positions discussed here (futures, margin, funding payments) are nuanced. Always consult a qualified CPA about your specific situation.

Find Yourself: Which Kraken User Are You?

Kraken users are not all the same, and your tax exposure depends on how you use the exchange. Find your profile and jump to what matters most.

The 1099-DA Shock Case

You opened your 1099-DA, saw a huge proceeds number, and assumed you owe tax on all of it.

Proceeds are not gains. Jump to Understanding 1099-DA →The Transfer-In Case

You bought elsewhere, moved crypto into Kraken, and sold, and now your basis is missing.

This is the core problem. Jump to Cost Basis Problems →The Active Trader

High-volume spot, margin, and futures activity across the year.

Margin and futures have special rules. Jump to Margin Taxes →The Staker

You earn staking rewards on ETH, SOL, DOT, or ADA through Kraken.

Rewards are income then gains. Jump to Staking Taxes →The Multi-Platform User

Kraken plus Coinbase, Binance, MetaMask, Ledger, and more.

You need full reconciliation. Jump to the Audit Checklist →What Is Kraken?

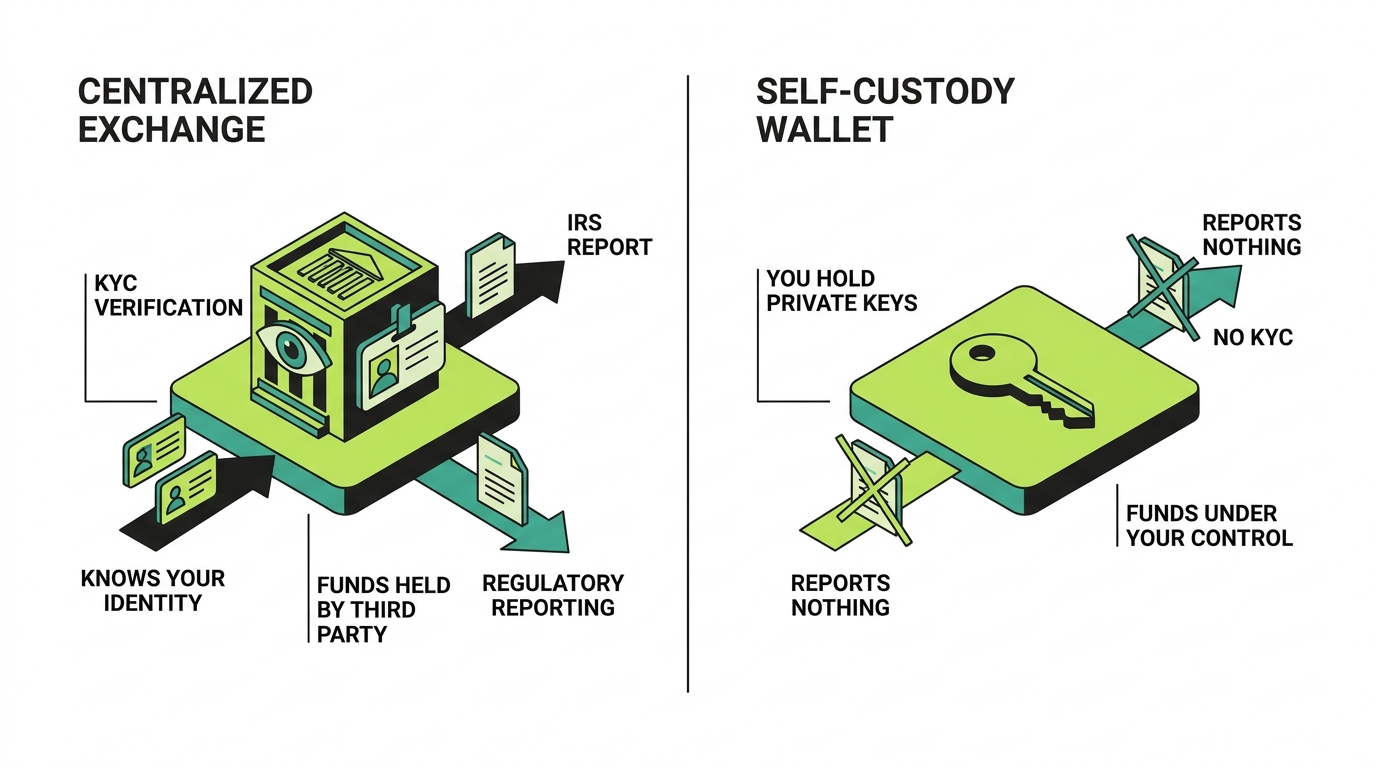

Kraken is one of the largest centralized cryptocurrency exchanges, where you buy, sell, and trade crypto, earn staking rewards, and access advanced products like margin and futures. Because it is centralized and custodial, the tax situation is fundamentally different from a self-custody wallet, and understanding that difference is the foundation of getting your Kraken taxes right.

How Kraken Works

On Kraken you fund your account, buy crypto with dollars, trade pairs on the spot market, and optionally use margin and futures. Kraken holds your crypto in custody, runs KYC to verify your identity, and keeps a record of the trades that happen on its platform. Because it is a broker, it reports certain activity to the IRS and provides tax documents through its Tax Center. This is the opposite of a self-custody wallet, where no company keeps your books.

Kraken vs Self-Custody Wallets

A self-custody wallet like MetaMask or Coinbase Wallet reports nothing and leaves all recordkeeping to you. Kraken is the other model: it knows your identity, it tracks the trades on its platform, and it reports to the IRS. The catch is that Kraken only knows what happened on Kraken. The moment crypto enters from another platform or leaves to a wallet, Kraken’s view of your basis breaks, which is the source of most reconciliation problems.

Why Taxes Are Different On Exchanges

On an exchange, the tax story is shaped by broker reporting. You receive forms, the IRS receives matching reports, and your return is checked against them. That makes accuracy and reconciliation more important, not less, because a mismatch between the proceeds Kraken reports and what you file can trigger a notice. The exchange gives you a starting point, but it is gross proceeds, not a finished tax answer.

An exchange like Kraken hands you a 1099-DA full of proceeds. It is the opening line of your tax story, not the conclusion.

Do You Owe Taxes On Kraken?

Yes, if you had taxable events. Buying and holding is not taxable, but selling, trading, spending, and earning crypto are.

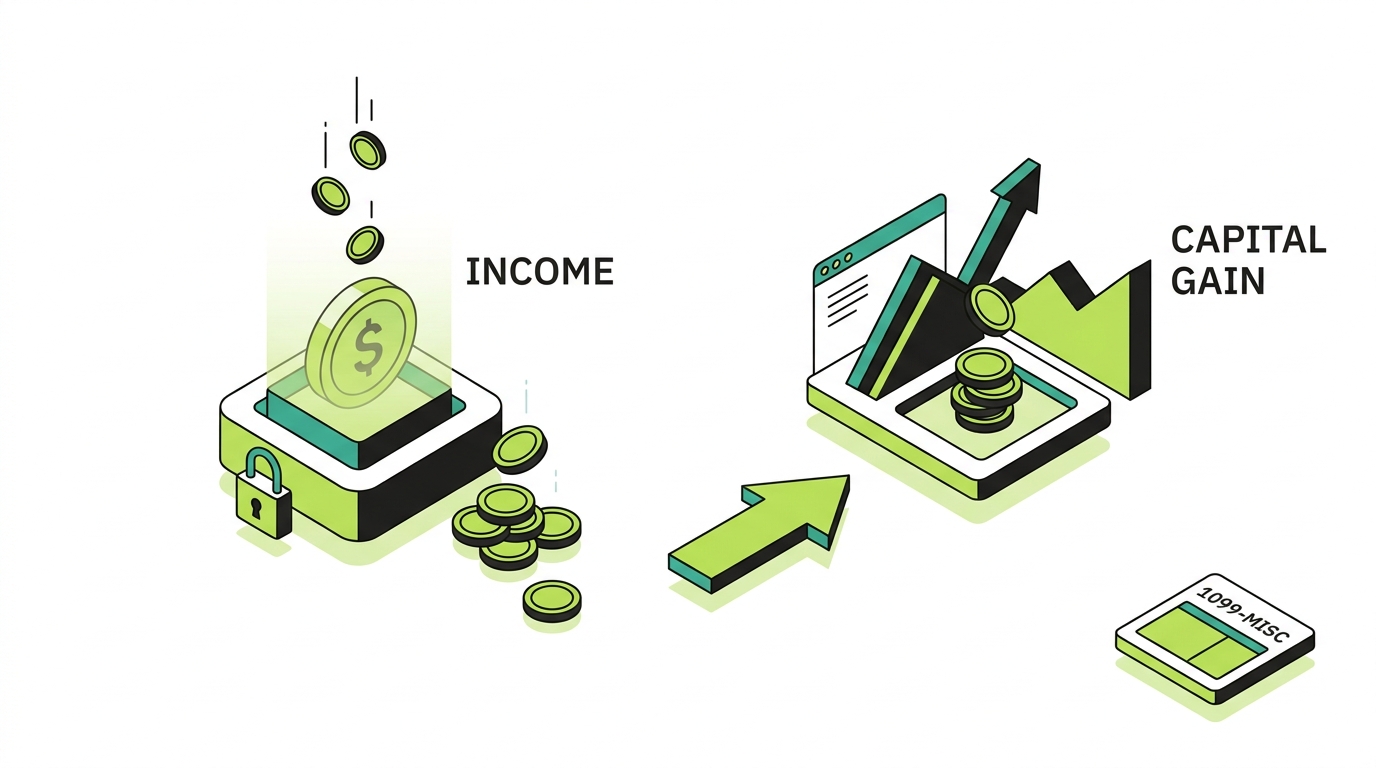

Capital Gains

Capital gains apply when you dispose of crypto: selling it for dollars, trading it for another token, converting it to a stablecoin, or spending it. Your gain or loss equals proceeds minus cost basis. Hold an asset one year or less and the gain is short-term, taxed at ordinary rates. Hold it longer than a year and the gain is long-term, taxed at the lower 0, 15, or 20 percent rates.

Income Events

Income events apply when you earn crypto: staking rewards and other reward income are ordinary income at fair market value when you gain control of them. That value also becomes your cost basis for a later sale.

IRS Property Rules

The IRS treats virtual currency as property under Notice 2014-21. That classification is why every disposal can trigger a capital gain or loss and why earning crypto is ordinary income. Kraken does not change these rules, it simply reports some of the activity that triggers them.

Does Kraken Report To The IRS?

Yes. As a centralized, KYC-verified broker, Kraken reports to the IRS, and that reporting is expanding.

What Kraken Reports

Kraken reports digital asset sales and dispositions on the relevant 1099 forms and provides those documents through its Tax Center. The reporting is tied to your verified identity, so the IRS receives information linked directly to you. What Kraken cannot report is the history that happened off its platform: purchases on other exchanges, self-custody activity, and the original basis of assets you transferred in.

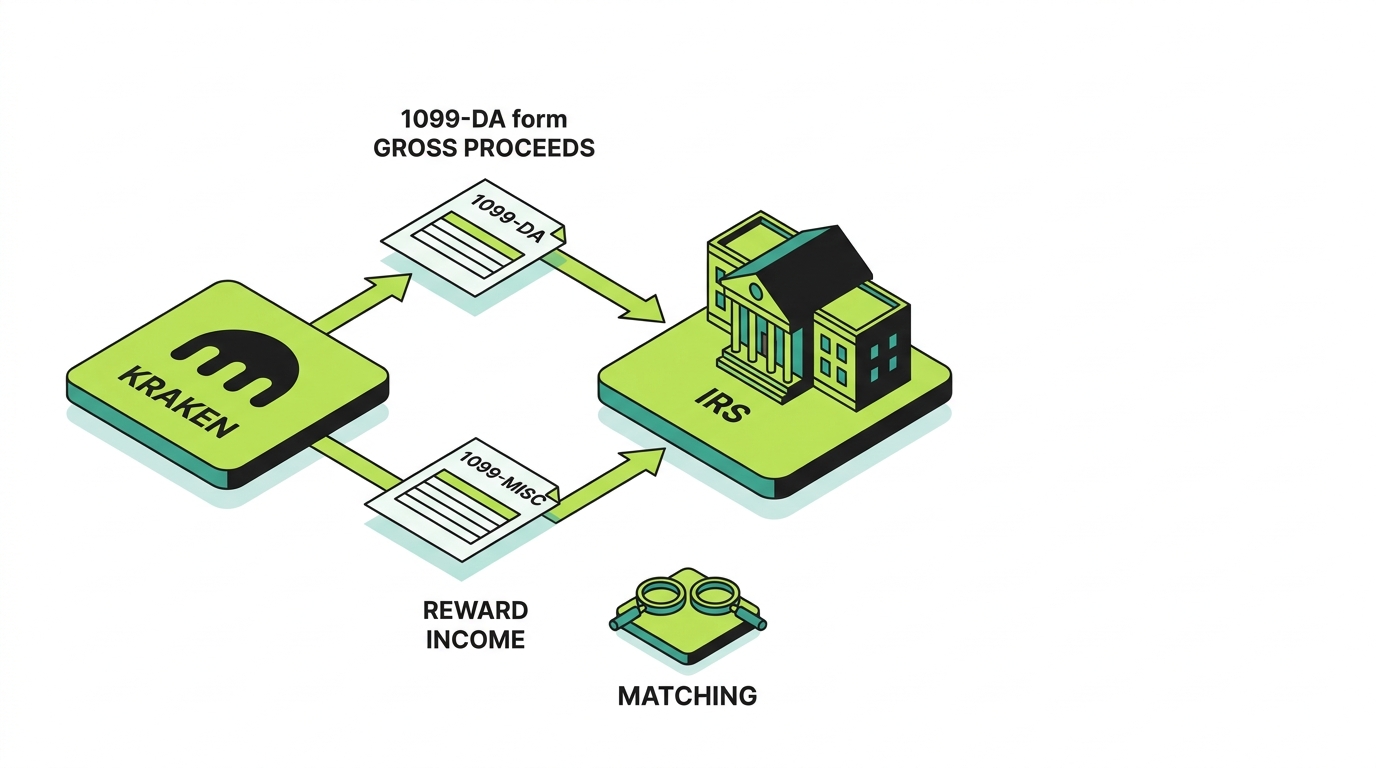

1099-DA Reporting

Form 1099-DA is the new digital asset broker reporting form. Starting with the 2025 tax year, Kraken provides 1099-DA for reportable sales and dispositions, reporting gross proceeds. For 2025, brokers generally report proceeds while full cost basis reporting is still phasing in. This single fact, proceeds without complete basis, drives the entire reconciliation challenge covered later. For a dedicated walkthrough of the form itself, what Kraken reports, why basis is often missing, and how to fix it before filing, see our Kraken 1099-DA guide.

1099-MISC Reporting

Separately, Kraken may issue Form 1099-MISC to report certain income such as rewards when reporting thresholds are met. Even without a form, reward income is taxable, so you report it from your own records regardless of whether a 1099-MISC arrives.

IRS Matching Programs

The IRS runs automated matching that compares broker-reported proceeds to what taxpayers file. If your return omits Kraken activity or does not reconcile with the reported proceeds, that mismatch can trigger an automated notice. The defense is a return that ties cleanly to the 1099-DA proceeds while reflecting your true basis.

Understanding Kraken 1099-DA

This is the most important section in the guide, because the 1099-DA is where Kraken users panic, overpay, or underreport. Read it carefully.

What Is Form 1099-DA?

Form 1099-DA is the IRS form brokers use to report digital asset sales and dispositions. It tells the IRS the gross proceeds from your activity on the platform and, over time, more basis information. It is an information return, not a bill, and not a finished calculation of what you owe.

Why Proceeds Look Too High

The proceeds figure is the total of everything you sold for, summed across every disposal, before subtracting what you paid. If you traded the same capital in and out many times, each trade adds its full proceeds to the total. That is how an account that netted a small profit can report enormous proceeds. The number reflects activity volume, not profit.

This matters most for active traders and anyone who used crypto-to-crypto trades, because each leg of a round trip counts. Buy, sell, buy again, sell again, and the same dollars get reported as proceeds four times. A buy-and-hold investor who sold once sees proceeds close to their actual sale, while a frequent trader sees a proceeds total many multiples of the capital they ever put in. Neither is wrong, the form is doing exactly what it is designed to do. The mistake is reading the proceeds line as if it were the gain line.

Proceeds vs Gain Example

Missing Cost Basis

For 2025, Kraken generally reports proceeds, and it cannot report basis for assets you bought elsewhere and transferred in. So the form may show large proceeds paired with little or no basis. Left unreconciled, tax software or a naive reading treats the missing basis as zero, which overstates your gain dramatically and inflates your tax bill.

Covered vs Non-Covered Assets

Covered assets are those for which the broker is required to track and report basis, generally tied to when the rules took effect and whether the asset was acquired on the platform. Non-covered assets are those where basis is not broker-reported, often because they came in from elsewhere. For non-covered assets, supplying the correct basis is entirely your job.

How To Reconcile Your 1099-DA

Reconciliation means pairing the proceeds Kraken reports with your true cost basis for each disposal, accounting for transferred-in assets, removing duplication, and producing a Form 8949 that shows real gains and losses while tying to the reported proceeds total. This is the heart of exchange tax work, and it is exactly what most ranking articles skip.

Your 1099-DA tells the IRS what you sold for. Your job is to tell the IRS what you actually made.

Kraken Transactions That Are Taxable

These are the events that create a tax bill.

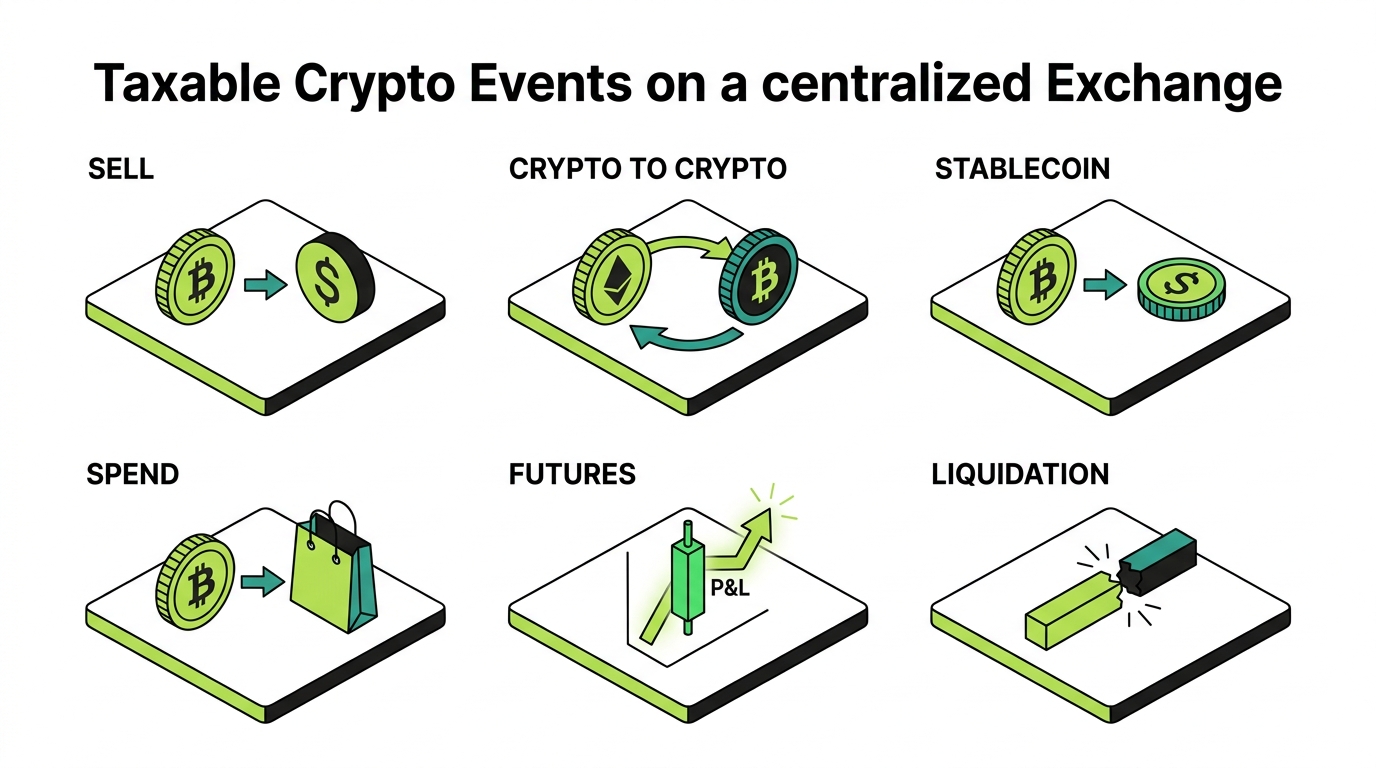

Selling Crypto

Selling crypto for dollars or stablecoins is a taxable disposal. Gain or loss equals proceeds minus cost basis.

Crypto-to-Crypto Trades

Trading one cryptocurrency for another is a taxable disposal of the crypto you gave up, even though no dollars change hands. These trades are the most commonly overlooked taxable events on exchanges.

Stablecoin Trades

Converting crypto into a stablecoin like USDT or USDC is a disposal of the crypto you converted, so it is taxable. Stablecoins are still property, and moving into them does not make the underlying sale tax free.

Spending Crypto

Spending crypto on goods or services is treated as a sale of that crypto at fair market value, triggering a gain or loss.

Futures Settlement

Settlement of futures positions produces realized profit or loss that is a taxable result of the activity. We cover the nuances in the futures section.

Margin Liquidations

A margin liquidation is a forced disposal of the position or collateral that was closed out, so it is a taxable event with a gain or loss, often at an unfavorable price.

Kraken Transactions That Are Not Taxable

Not every action is a taxable event. These generally are not.

Buying Crypto

Buying crypto with US dollars is not taxable. It sets your cost basis, which is what you paid including fees.

Holding Crypto

Holding crypto on Kraken is never taxable, no matter how much the value changes. Unrealized gains are not taxed until you dispose of the asset.

Moving Assets Between Wallets

Withdrawing crypto from Kraken to a wallet you own is a transfer, not a sale, so it is not taxable. Your basis must follow the asset, because once it leaves Kraken the exchange stops tracking it.

Transfers Between Exchanges

Moving crypto between exchanges you control, such as from Coinbase, Gemini, or Binance.US to Kraken, is a transfer, not a sale, so it is not taxable. The risk is purely about basis following the asset.

Kraken Staking Taxes

Staking is a common source of ordinary income for Kraken users across ETH, SOL, DOT, ADA, and more.

Reward Income

Staking rewards are ordinary income at fair market value when you gain control of them. Tracking the value at each reward point across the year is tedious but necessary.

1099-MISC Treatment

Kraken may report reward income on Form 1099-MISC. Whether or not you receive one, the income is taxable and you report it from your records.

Basis Tracking

The amount you report as income becomes your cost basis in the reward assets. Report rewards once as income when received, then again as a capital gain or loss when sold, not twice as income.

Selling Reward Assets

When you later sell or trade your staking rewards, you report a separate capital gain or loss equal to the sale value minus the basis you established when you earned them.

Staking Example

Kraken Margin Trading Taxes

Margin trading is a major content gap that most ranking pages ignore, and Kraken has long attracted sophisticated traders, so it matters.

Borrowed Funds

Borrowing funds to trade on margin is not income, because a loan is not income. The tax consequences come from what you do with the borrowed capital and how the positions close. When you open a margin position you are using borrowed capital to take a larger exposure than your own funds would allow, and the borrowed amount itself does not create a taxable event when you receive it. What creates the tax is the disposal: when the position is closed, sold, or liquidated, you realize a gain or loss just as you would on any other sale.

Interest Costs

Interest and borrowing costs on margin are expenses associated with the trading. Whether and how they are deductible depends on your tax situation and whether you are an investor or a trader, so document every cost.

Liquidations

A liquidation is a forced disposal of the position or collateral, a taxable event with a gain or loss measured against basis. Liquidations often occur at bad prices and can create real losses, which are deductible, so capture them.

Gain/Loss Calculations

Margin gains and losses are reported as capital gains and losses on the positions you close. Because margin records are complex and span borrowing, interest, and forced closes, reconcile the full history rather than trusting a single summary number.

The practical difficulty is that margin trading generates a dense web of related entries: the borrow, the trades made with borrowed funds, interest accruals, partial closes, and any liquidations. Tax software frequently imports these as a confusing mix of transfers and trades, and it can double-count or misclassify the borrow as a disposal. The reliable approach is to reconstruct each position from open to close, confirm the realized gain or loss, treat the borrow correctly as a non-event, and account for interest separately. For high-volume margin traders, this is where professional reconciliation saves both money and audit risk.

Kraken Futures Taxes

Kraken futures is another major opportunity that almost no tax guide covers well. The treatment is nuanced, so this section flags the issues and points you to professional confirmation.

Perpetual Futures

Perpetual futures have no expiry and are kept aligned to spot through funding payments. Your taxable result is driven by the realized profit and loss on your positions plus the effect of funding.

Funding Payments

Funding payments are periodic transfers between long and short traders. Their characterization can be nuanced and forms part of the overall profit and loss of your futures activity, so track them rather than ignoring them.

Liquidation Events

Liquidations in futures close your position by force and crystallize a realized result, which is part of your taxable profit and loss for the activity.

Tax Reporting Challenges

Crypto derivatives sit in an area where the rules are still developing, and product mechanics vary. The practical takeaway is to maintain meticulous records of every position, funding payment, and liquidation, and to have a professional confirm the correct characterization for your specific products and situation.

The core challenge is that crypto futures do not map cleanly onto either simple spot trades or traditional regulated futures contracts. Treatment can hinge on the specific product, how it settles, and your own facts, and crypto tax software is rarely built to model perpetual funding and liquidation mechanics accurately. As a result, futures activity is one of the few areas where pulling the raw data and working through it deliberately, rather than trusting an automated import, is essential. If futures are a meaningful part of your year, this is the single most important section to bring to a professional.

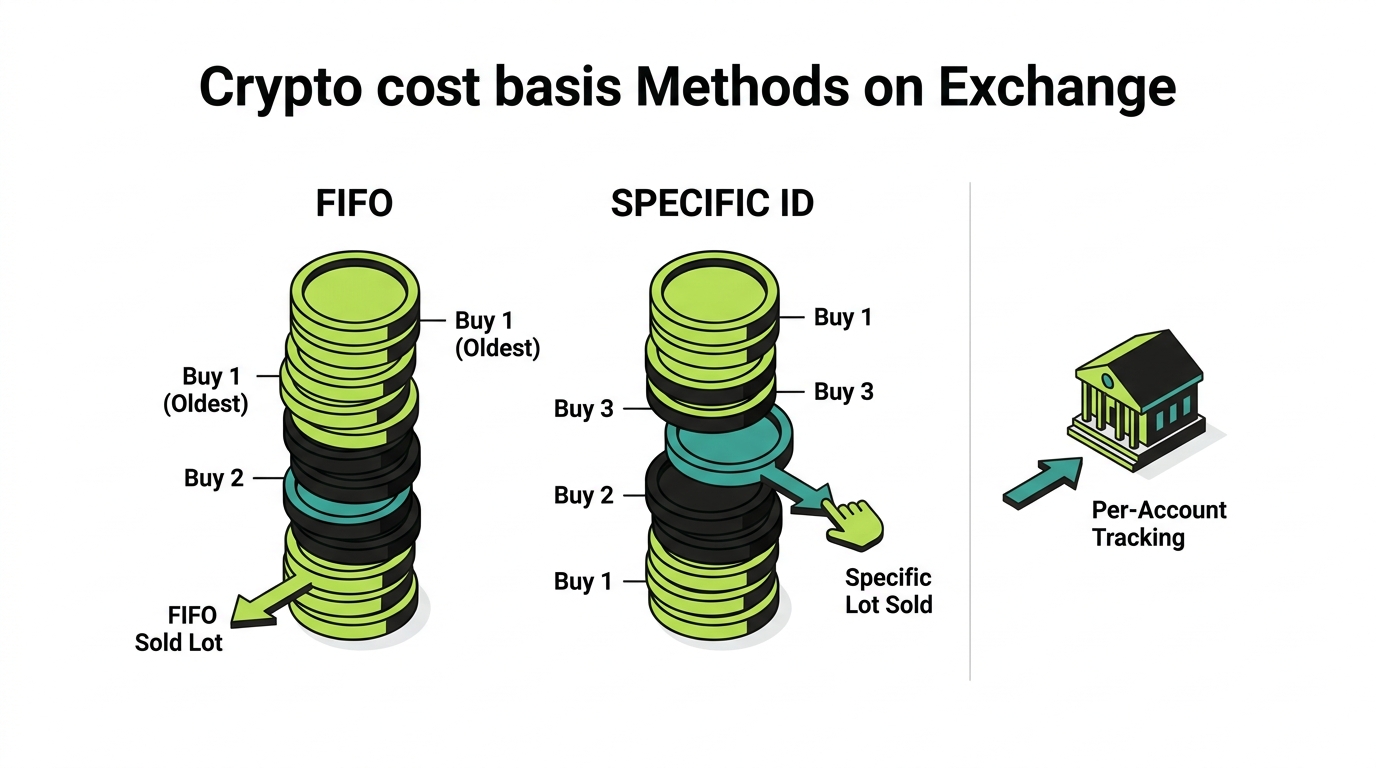

How To Calculate Kraken Cost Basis

Cost basis is what you paid for an asset, and it determines your gain or loss on disposal. You choose a method and apply it consistently.

FIFO

First In, First Out is the IRS default. It assumes the first units you acquired are the first you dispose of. It is simple but in a rising market it tends to produce larger gains.

Specific Identification

Specific Identification lets you choose exactly which lot you are disposing of, giving the most control over gains and losses. It requires strong recordkeeping, because if you cannot prove which lot you sold you fall back to FIFO.

Wallet-Level Tracking

Under IRS Revenue Procedure 2024-28, effective January 1, 2025, cost basis must be tracked per account or wallet rather than pooled universally. Your Kraken account is its own bucket, separate from other exchanges and wallets. Transfers between them are not taxable, but the basis must carry with the asset.

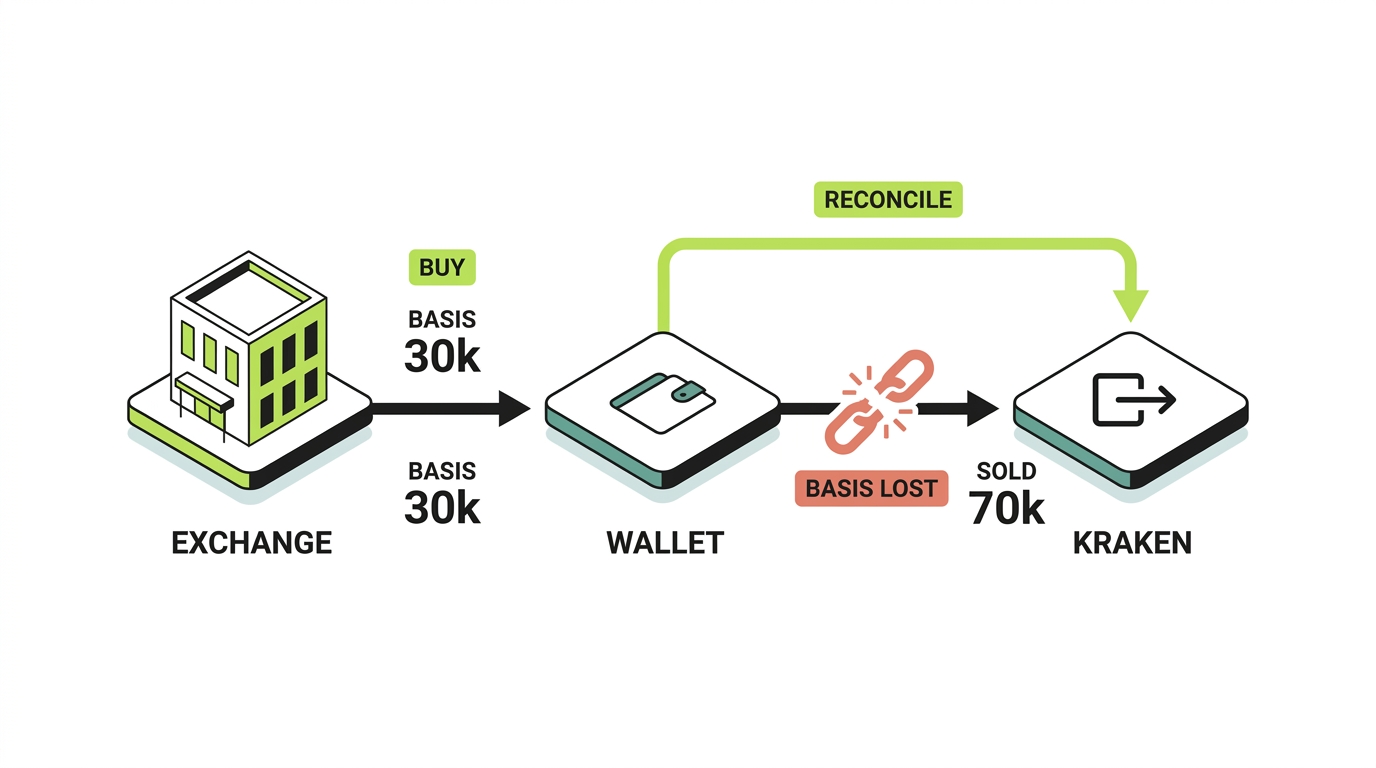

Exchange Transfers

Exchange transfers are where basis lives or dies. When you move an asset into Kraken, the original basis from the source platform must follow it, or the later sale on Kraken will appear to have a zero basis. Documenting transfers is the single highest-value recordkeeping habit for exchange users.

Kraken and 1099-DA Cost Basis Problems

This section deserves extra detail, because transferred-in assets are where the worst Kraken tax surprises happen.

External Wallet Deposits

When you deposit crypto from an external wallet into Kraken, Kraken sees the deposit but not what you originally paid. The basis is in your wallet and source records, not on Kraken, so you must supply it.

Transferred Assets

Assets transferred in from another exchange carry the same problem. Kraken can report the eventual sale proceeds but not the purchase price that happened elsewhere, leaving a basis gap on the 1099-DA.

Missing Purchase Records

If you no longer have the original purchase records, reconstructing basis is harder but still necessary. Historical price data and exchange exports can help rebuild it, and a reconciliation service can assemble it from the available trail.

Reconciling Historical Trades

The fix is to reconnect the full chain: original purchase, transfers, and final sale, so the gain reflects what actually happened. This is the core of Digital Asset Reconciliation and the difference between an inflated zero-basis gain and an accurate return.

Done well, reconciliation produces a return that satisfies two requirements at once. It ties to the gross proceeds Kraken reported, so the IRS matching program sees consistency, and it reflects your true cost basis, so you do not overpay on phantom gains. Getting there means importing every platform you used, matching each transfer so an outbound from one account links to the inbound on another, rebuilding basis for assets bought before you have clean records, and removing duplicates created by importing the same activity from multiple sources. It is detailed work, but it is the difference between a defensible filing and either an overpayment or an audit flag.

Missing Basis Example

Kraken Tax Center Explained

The Kraken Tax Center is your starting point for Kraken tax documents, but it is not a finished return.

Tax Summary

The Tax Center provides a tax summary of your activity. Treat it as an overview, not a filing-ready calculation, especially where transferred-in basis is involved.

Transaction Reports

You can download detailed transaction reports. These raw records are essential, because the summaries alone will not let you reconcile transfers and basis accurately.

Missing Cost Basis Alerts

Kraken surfaces cost-basis-related information and warnings where basis is incomplete. Take these seriously, because they point directly at the disposals most likely to be overstated on your return.

Downloading Tax Forms

Download your 1099-DA and any 1099-MISC from the Tax Center, along with full transaction history. Gather everything before you start, so your reconciliation has complete source data.

Best Kraken Tax Software

No tool fully automates a messy multi-platform history, but the right one does most of the heavy lifting. Your best choice depends on volume and how much margin, futures, staking, and multi-exchange activity you have.

CoinTracker

CoinTracker is a widely used option with strong portfolio tracking and broad exchange support, including a smooth Kraken import for mainstream activity.

Koinly

Koinly supports a very large number of exchanges and chains, which helps multi-platform Kraken users who also touch other exchanges and wallets.

CoinLedger

CoinLedger is popular for clean Form 8949 generation and a straightforward import flow, and it handles common exchange activity well.

TokenTax

TokenTax pairs software with optional professional services, useful when margin, futures, and multi-exchange history make your return complex.

ZenLedger

ZenLedger is an established option with broad integration support and tax-loss harvesting tools.

Summ

Summ is a newer entrant focused on streamlined crypto tax reporting, sometimes surfaced through exchange partner pages.

Common Kraken Tax Mistakes

Trusting 1099-DA Alone

The number one mistake. The 1099-DA shows gross proceeds, not gains, and often lacks basis for transferred-in assets. Filing straight from it overstates your gain.

Ignoring Wallet Transfers

Transfers in and out of Kraken are where basis is lost. Leaving them undocumented breaks the chain and inflates later gains.

Missing Cost Basis

When assets bought elsewhere arrive without basis, software assumes zero and overstates the gain. This is the most expensive common error.

Ignoring Staking Income

Staking rewards are ordinary income when received, and forgetting them underreports income even if a 1099-MISC was issued.

Ignoring Futures Activity

Futures profit and loss, funding payments, and liquidations are routinely missed or mislabeled.

Ignoring Margin Trades

Margin gains, losses, interest, and liquidations are complex and frequently left out entirely.

How To Prepare For A Kraken Tax Audit

Audit readiness is exactly where a reconciliation mindset pays off, and it is a strong, under-served topic.

Exchange Records

Keep your full Kraken transaction history, all tax forms, and detailed reports. Your records tie each reported number to a real transaction.

Wallet Records

Keep records for every wallet you used alongside Kraken, so on-chain activity and exchange activity reconcile.

Cost Basis Documentation

Document the basis for every asset, especially those transferred into Kraken, with original purchase records from the source platform.

1099 Reconciliation

Maintain a clear reconciliation between the proceeds on your 1099-DA, the income on any 1099-MISC, and the numbers on your return, so they tie out.

Form 8949 Support

Ensure every line on your Form 8949 can be traced to a real transaction with a defensible basis. That traceability is what an audit tests.

Huge proceeds on your Kraken 1099-DA, with missing cost basis?

That is exactly the history DIY tools get wrong. We reconcile your full Kraken, exchange, and wallet activity into defensible, CPA-ready numbers.

See how it worksWhere Count On Sheep Fits

Kraken gives you a powerful exchange with spot, staking, margin, and futures. What it does not give you is a finished tax answer. The 1099-DA reports gross proceeds, basis is often missing for transferred-in assets, the IRS receives those proceeds reports, and margin and futures need careful handling. The strongest way to say it is simple: Kraken reports transactions. It does not know your entire crypto history.

Count On Sheep prepares CPA-ready Digital Asset Reconciliation for Kraken users: we connect Kraken to your other exchanges and wallets, match transfers so basis follows each asset, handle staking, margin, and futures, reconcile against your 1099-DA and 1099-MISC, and produce a defensible Form 8949 and income report you can actually file behind. We are a crypto tax reconciliation service, not a CPA firm, and we work alongside your tax preparer.

Not sure your crypto taxes are right?

Talk to a Count On Sheep specialist. We will spot the costly errors before you file. No obligation.

Book My Free Review- Reviewed by Former Big 4 Accountants

- Keep your CPA

- No pressure, no sales pitch

Related Reading

- Coinbase Tax Guide (2026)

- Gemini Tax Guide (2026)

- Binance.US Tax Guide (2026)

- Coinbase Wallet Tax Guide (2026)

- MetaMask Tax Guide (2026)

- Phantom Wallet Tax Guide (2026)

- Crypto Tax Guide 2026: IRS Rules, Forms and Rates

- Form 1099-DA Explained for 2026

- How to File Crypto Taxes With Form 8949 and Schedule D

- Per-Wallet Crypto Cost Basis: Rev. Proc. 2024-28

- Crypto Income Tax: Staking, Mining and Airdrops (2026)

- FIFO vs HIFO vs Specific ID for Crypto Taxes

- Crypto Tax Loss Harvesting and the Wash Sale Rule (2026)

Official IRS Resources

For the primary source rules behind this guide, see the IRS directly:

- IRS: Digital Assets

- IRS Notice 2014-21 (crypto treated as property)

- IRS: About Form 8949

- IRS: About Schedule D (Form 1040)

- IRS: About Form 1099-DA

This guide is educational and not tax or legal advice. Digital asset rules change frequently, and several positions discussed here (futures, margin, funding payments, covered vs non-covered basis) are nuanced or unsettled. Consult a qualified CPA about your specific Kraken activity.

Frequently Asked Questions

Does Kraken report to the IRS?

Yes. Kraken is a centralized exchange and a broker for tax purposes, so it reports certain digital asset activity to the IRS. Starting with the 2025 tax year, Kraken provides Form 1099-DA for reportable digital asset sales and dispositions, and it may also issue Form 1099-MISC for certain income such as rewards. Your identity is tied to your account through KYC, so the IRS receives reporting linked to you.

Will Kraken send a 1099-DA?

If you had reportable digital asset sales or dispositions on Kraken, yes, you should expect a Form 1099-DA through the Kraken Tax Center for the 2025 tax year and beyond. The form reports gross proceeds from your dispositions. Always download and reconcile it against your own records, because the proceeds figure is not your taxable gain.

Why is my Kraken 1099-DA so high?

Because the 1099-DA reports gross proceeds, not gain. Every sale and crypto-to-crypto trade adds its full proceeds to the total, so an account that traded actively can show hundreds of thousands in proceeds while the actual taxable gain is a small fraction of that. The proceeds number is the sum of what you sold for, before subtracting what you paid. It is not what you owe tax on.

Why is my Kraken cost basis missing?

For the 2025 tax year, brokers like Kraken generally report gross proceeds while cost basis reporting is not yet fully required, and Kraken cannot know the basis for crypto you bought somewhere else and transferred in. If you moved assets from another exchange or a wallet into Kraken before selling, Kraken often has no record of your original purchase price, so basis shows as missing or zero.

Does Kraken report staking rewards?

Kraken may report certain reward income on Form 1099-MISC. Regardless of whether a form is issued, staking rewards are taxable as ordinary income at their fair market value when you gain control of them, and that value becomes your cost basis when you later sell the reward assets.

How do I report Kraken futures?

Kraken futures activity is reported based on your realized profit and loss from the positions, including the effect of funding payments and liquidations. The exact federal treatment of crypto futures can be complex and depends on the product and your situation, so document every position, opening, closing, funding payment, and liquidation, and have a professional confirm the correct reporting.

How do I report Kraken margin trading?

Margin gains and losses are reported as capital gains and losses on the positions you close, while borrowing itself is not income. Interest and borrowing costs and the results of any liquidations all factor in. Because margin records are complex, reconcile your full margin history rather than relying on a single summary number.

Can the IRS see my Kraken account?

Yes. Kraken is KYC verified to your identity and reports to the IRS, and the IRS runs matching programs that compare reported proceeds to what you file. If your return does not reconcile with the proceeds on your 1099-DA, that mismatch can trigger a notice. Treat all Kraken activity as visible and reportable.

What if my Kraken 1099-DA is wrong?

First understand that a high proceeds number is usually not an error, it is gross proceeds by design. If there is a genuine factual error, contact Kraken support to review it. In most cases the fix is not correcting the form but reconciling it: pairing the reported proceeds with your true cost basis so your Form 8949 shows the real gain or loss rather than the raw proceeds.

How do I reconcile Kraken with Coinbase?

Import both your Kraken and Coinbase histories into the same crypto tax software, then match the transfers between them so cost basis follows each asset. If you bought on Coinbase and sold on Kraken, the basis lives on Coinbase and the disposal lives on Kraken, and only by combining them do you get an accurate gain. Reconcile transfers carefully so nothing is double counted or shows a zero basis.

How do I reconcile Kraken with MetaMask?

Add your MetaMask wallet addresses and your Kraken history to one tax tool so on-chain activity and exchange activity live together. Crypto bought on Kraken, withdrawn to MetaMask, used in DeFi, and later sent back to Kraken needs its basis traced across every hop. The reconciliation connects the exchange record to the on-chain record so the final gain is correct.

What happens if I don't report Kraken taxes?

Failing to report can lead to back taxes, penalties, and interest, and because Kraken reports your proceeds to the IRS, an unreported or under-reported return is more likely to be flagged through matching. If you are behind, the safest path is to reconcile your complete history and file accurately, ideally with professional help, rather than ignoring a 1099-DA the IRS already has.

Do I owe taxes on Kraken if I only bought crypto?

No. Buying crypto with US dollars on Kraken is not a taxable event, it just sets your cost basis. You owe tax only when you trigger a taxable event such as selling, trading one crypto for another, spending crypto, or earning rewards. Simply buying and holding is not taxed.

Are crypto-to-crypto trades on Kraken taxable?

Yes. Trading one cryptocurrency for another on Kraken is a taxable disposal of the crypto you gave up, even though no US dollars are involved. You calculate a capital gain or loss based on the fair market value at the time of the trade minus your cost basis. These trades are the most commonly overlooked taxable events on exchanges.

Is converting crypto to a stablecoin on Kraken taxable?

Yes. Converting crypto into a stablecoin like USDT or USDC is a disposal of the crypto you converted, so it is a taxable event with a gain or loss measured against your basis. Stablecoins are still property to the IRS, and moving into them does not make the underlying sale tax free.

Are Kraken transfers to my own wallet taxable?

No. Withdrawing crypto from Kraken to a wallet you own and control is a transfer, not a sale, so it is not taxable. The important part is that your cost basis must follow the asset, because once it leaves Kraken the exchange no longer tracks it and a later sale could show a missing basis.

Does Kraken issue a 1099-MISC?

Kraken may issue Form 1099-MISC to report certain income such as rewards when it meets the reporting thresholds. Even if you do not receive one, reward and income events are still taxable as ordinary income, so you report them based on your own records of value at receipt.

What is the difference between gross proceeds and gains on Kraken?

Gross proceeds are the total dollar amount you received from all your sales and dispositions, before subtracting anything. Gains are proceeds minus your cost basis. The 1099-DA reports gross proceeds, which can look alarmingly large, while your actual taxable gain is only the profit portion. Confusing the two is the single biggest source of Kraken tax panic.

What are covered and non-covered assets on a 1099-DA?

Covered assets are those for which the broker is required to track and eventually report cost basis, generally tied to when reporting rules took effect and whether the asset was acquired on the platform. Non-covered assets are those where basis is not broker-reported, often because they were transferred in from elsewhere. For non-covered assets, supplying the correct basis is entirely your responsibility.

How do I reconcile my Kraken 1099-DA?

Match the proceeds Kraken reports to your own cost basis records for each disposal, account for assets transferred in from other platforms, remove any duplication, and produce a Form 8949 that shows real gains and losses. The goal is a return that ties to the 1099-DA proceeds total while reflecting your true basis, so the IRS matching program sees a consistent picture.

How is Kraken staking taxed?

Staking rewards are ordinary income at fair market value when you gain control of them, potentially reported on a 1099-MISC. That income amount becomes your cost basis in the reward tokens, so when you later sell or trade them you report a separate capital gain or loss on the difference.

How are Kraken margin liquidations taxed?

A margin liquidation is a forced disposal of the collateral or position that was closed out, so it is a taxable event with a gain or loss measured against your basis. Liquidations often happen at bad prices and can create losses, which are still deductible, so it is important to capture them rather than ignore the position.

How are Kraken futures funding payments taxed?

Funding payments on perpetual futures are periodic payments between long and short traders. Their tax treatment is part of the overall profit and loss of the futures activity and can be nuanced, so they should be tracked and included in the position results, with a professional confirming the correct characterization for your situation.

Do I have to report Kraken if I lost money?

Yes, and you usually want to. Reporting losses can reduce your taxable gains and, within limits, your ordinary income, and unused losses can carry forward. Because Kraken reports your proceeds to the IRS, leaving losing trades off your return also makes it harder to reconcile, so report the full picture including losses.

What records should I keep for Kraken taxes?

Keep your full Kraken transaction history, every 1099-DA and 1099-MISC, records of transfers in and out with the basis that traveled with each asset, and documentation of staking, margin, and futures activity. For assets bought elsewhere, keep the original purchase records so you can supply the missing basis. These records are your defense in an audit.

Does Kraken work with TurboTax?

Not as a finished return. The usual path is to export your Kraken history or connect it to crypto tax software like CoinTracker, Koinly, or CoinLedger, which generates a Form 8949 you can then import into TurboTax or give to your preparer. The Kraken Tax Center provides summaries and forms, but the reconciliation work still has to happen.

How do I get my Kraken tax documents?

Use the Kraken Tax Center, which provides tax summaries, downloadable forms such as the 1099-DA and any 1099-MISC, transaction reports, and cost-basis-related information. Download everything, including raw transaction history, because the summaries alone are not enough to build an accurate, reconciled return.

What is the best Kraken tax software?

Strong options include CoinTracker, Koinly, CoinLedger, TokenTax, ZenLedger, and Summ. The best choice depends on your volume and whether you have margin, futures, staking, and multi-exchange activity. No tool fully automates a messy multi-platform history, so plan to review the import for missing basis, mislabeled margin and futures entries, and unmatched transfers.

Can the IRS match my Kraken 1099-DA to my tax return?

Yes. The IRS runs automated matching that compares the proceeds brokers report to what taxpayers file. If your return omits Kraken activity or does not reconcile with the reported proceeds, the mismatch can generate an automated notice. Filing a return that ties cleanly to the 1099-DA proceeds is the best way to avoid that.

Are Kraken futures taxed differently from spot trades?

Potentially. Spot sales and crypto-to-crypto trades are straightforward capital gains events, while futures involve realized profit and loss, funding payments, and liquidations whose treatment can be more complex and product specific. Because the rules around crypto derivatives are still developing, futures activity is an area to document carefully and confirm with a professional.

Do I owe taxes when I transfer crypto between exchanges?

No. Moving crypto between exchanges you control, such as from Coinbase to Kraken, is a transfer, not a sale, so it is not taxable. The risk is purely about basis: if the original purchase history does not follow the asset, the later sale on Kraken can appear to have no cost basis and overstate your gain.

Why does my Kraken account show transfers with no cost basis?

Because the crypto was bought outside Kraken and moved in. Kraken can see the deposit and the eventual sale, but not what you originally paid on another platform, so it cannot supply the basis. You fill that gap by reconciling your records from the source platform, which is exactly where most Kraken tax problems originate.

How do I report Kraken on my tax return?

Report each taxable disposal on Form 8949 with dates, proceeds, cost basis, and gain or loss, then carry the totals to Schedule D. Report staking and other crypto income on Schedule 1 or Schedule C, and answer the digital asset question on Form 1040. Reconcile the totals against your Kraken 1099-DA so the proceeds tie out.

What is the biggest Kraken tax mistake?

Trusting the 1099-DA alone. The form shows gross proceeds, not gains, and it often lacks basis for transferred-in assets. Filing straight from the proceeds number, or ignoring the form because it looks wrong, both lead to errors. The fix is reconciliation: pairing reported proceeds with true basis across all your accounts.

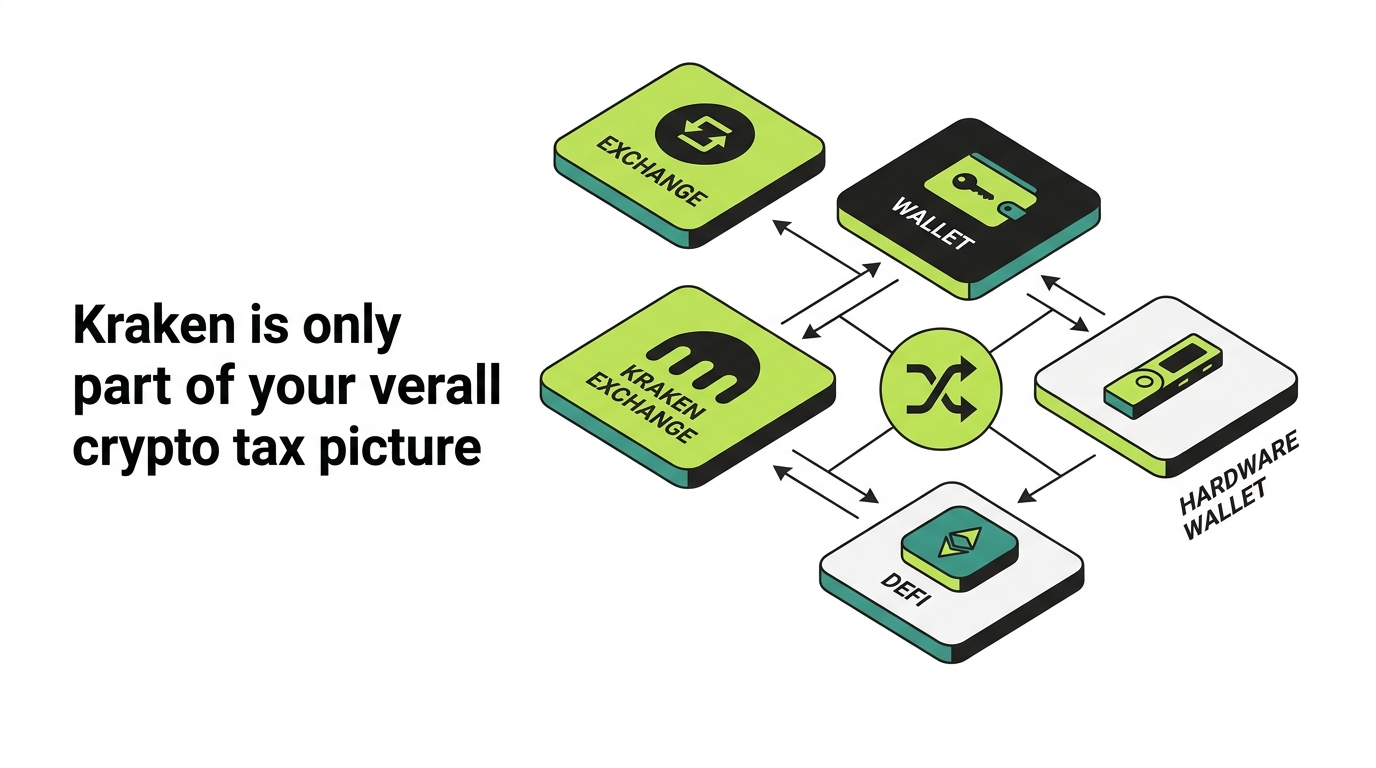

Is Kraken my entire crypto tax picture?

Almost never. Most Kraken users also use other exchanges and self-custody wallets, and crypto moves between all of them. Kraken reports only what happened on Kraken, so a complete and accurate return requires connecting Kraken to every other platform and wallet you used. Kraken reports transactions, it does not know your entire crypto history.

Can Count On Sheep help with Kraken taxes?

Yes. Count On Sheep provides CPA-ready Digital Asset Reconciliation for Kraken users: connecting Kraken to your other exchanges and wallets, matching transfers so basis follows each asset, handling staking, margin, and futures, reconciling against your 1099-DA and 1099-MISC, and producing a defensible Form 8949 and income report. We are a reconciliation service that works alongside your tax preparer.