Coinbase helps you buy crypto. Coinbase Wallet lets you use crypto. Taxes get exponentially more complicated once you leave the exchange. If you moved assets from the Coinbase exchange into Coinbase Wallet and then started swapping on Base, collecting NFTs, staking ETH, or farming DeFi, you are generating taxable events that the wallet will never report for you. Coinbase Wallet is self-custody. It does not issue 1099s and it does not file anything on your behalf.

This is the definitive Coinbase Wallet Taxes guide for 2026, built for the one thing most articles get wrong: the difference between the custodial Coinbase exchange and the self-custody Coinbase Wallet. We cover Base network taxes, DeFi through Uniswap and Aerodrome, NFTs, staking and liquid staking, bridges, gas fees, the new Form 1099-DA reconciliation problem, wallet-level cost basis, common mistakes, and an audit-ready checklist.

Disclaimer: This guide is for informational purposes only and is not tax or legal advice. Cryptocurrency rules are evolving quickly. Always consult a qualified CPA about your specific situation.

Find Yourself: Which Coinbase Wallet User Are You?

Coinbase Wallet users are not all the same, and your tax exposure depends on how you use the wallet. Find your profile and jump to what matters most.

The Exchange Graduate

You bought on Coinbase, moved assets to Coinbase Wallet, and assume Coinbase will sort out the taxes.

It will not. Jump to Wallet vs Exchange →The Base Native

You live on Base: memecoins, Aerodrome, low fees, constant swaps.

Every Base swap is a disposal. Jump to Base Network Taxes →The DeFi Power User

You provide liquidity, lend, borrow, and farm yield across Uniswap and Aerodrome.

Your activity is income-heavy and messy. Jump to DeFi Taxes →The NFT Collector

You mint, flip, and hold NFTs across Ethereum and Base marketplaces.

Mints, sales, and royalties each have rules. Jump to NFT Taxes →The Reconciliation Case

Assets bounced between Coinbase, Coinbase Wallet, Base, and DeFi, and your 1099-DA looks wrong.

You need a clean audit trail. Jump to the Audit Checklist →What Is Coinbase Wallet?

Coinbase Wallet is a self-custody crypto wallet. You hold your own private keys, connect to decentralized apps, swap tokens, manage NFTs, and move across networks including Ethereum, Base, Polygon, and others. Coinbase the company makes the app, but it does not hold your funds inside it, and that single fact changes everything about how it is taxed.

How Coinbase Wallet Works

When you open Coinbase Wallet, you create or import a wallet secured by a private key and a recovery phrase that only you control. From there you can receive crypto, send it, swap one token for another through connected decentralized exchanges, buy and sell NFTs, bridge assets between chains, and interact with DeFi protocols like Uniswap and Aerodrome. Coinbase Wallet is the doorway to on-chain activity, not a custodian sitting between you and the blockchain.

Because you control the keys, there is no company keeping a clean internal ledger of what you paid and what you sold. The wallet shows you raw on-chain transactions, but it does not know your cost basis in dollars, your intent, or which lot you disposed of. Reconstructing that context is the work of a Coinbase Wallet tax return.

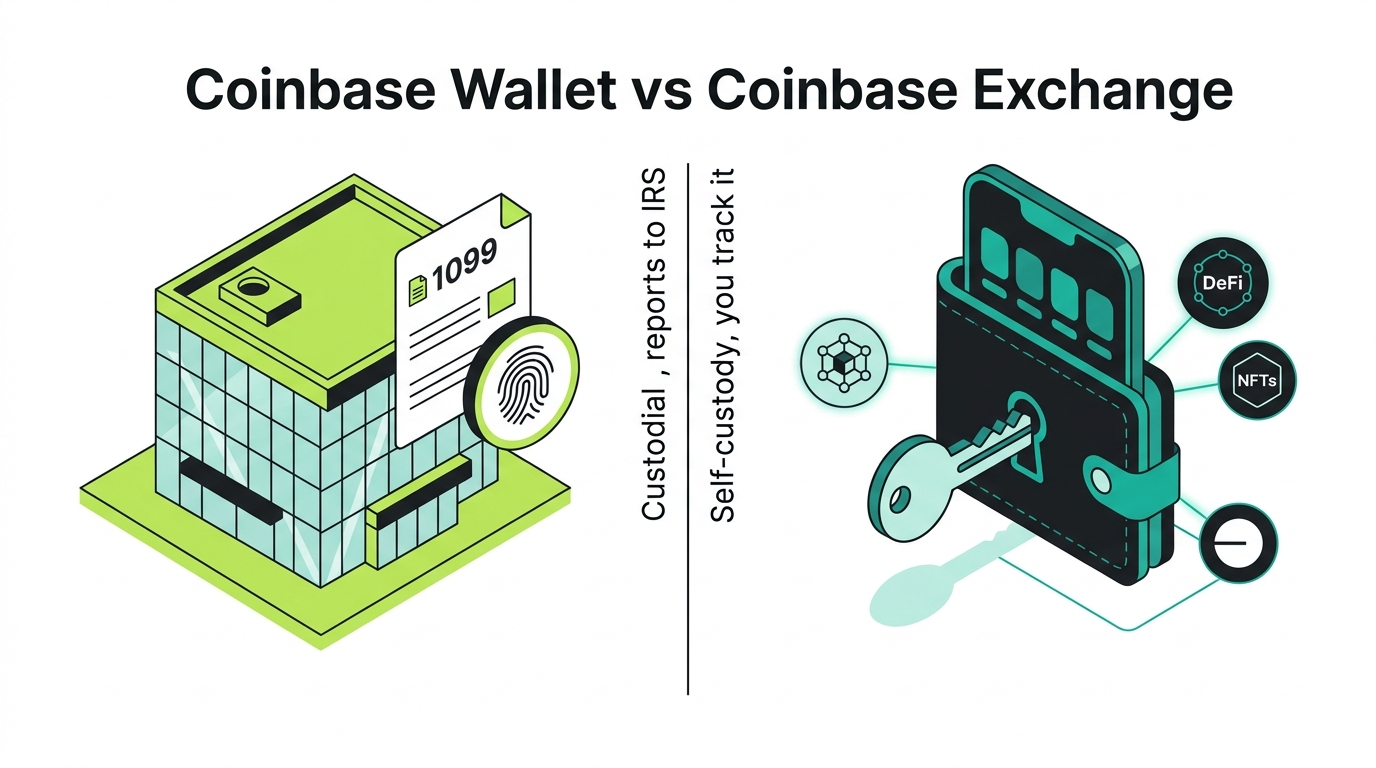

Coinbase Wallet vs Coinbase Exchange

This is the most important section in the entire guide, and it is the thing nearly every competing article fails to make clear. Coinbase and Coinbase Wallet are two different products with two completely different tax situations.

| Coinbase exchange (Coinbase.com) | Coinbase Wallet | |

|---|---|---|

| Custody | Custodial: Coinbase holds your crypto | Self-custody: you hold your keys |

| Identity | KYC verified to your identity | No KYC on the wallet itself |

| Tax documents | May issue 1099-DA and history reports | Issues nothing |

| Reporting to IRS | Yes, as a broker | No |

| Who tracks basis | Coinbase has the data for on-platform trades | You do |

| Typical activity | Buy, sell, hold | Swaps, DeFi, NFTs, Base, bridges |

The mental model that trips people up is “I use Coinbase, so Coinbase will calculate my taxes.” That is sometimes true for what you did on the exchange. It is almost never true for what you did in the wallet. The moment your crypto leaves the custodial exchange and enters self-custody, Coinbase stops keeping your books.

Why This Difference Matters For Taxes

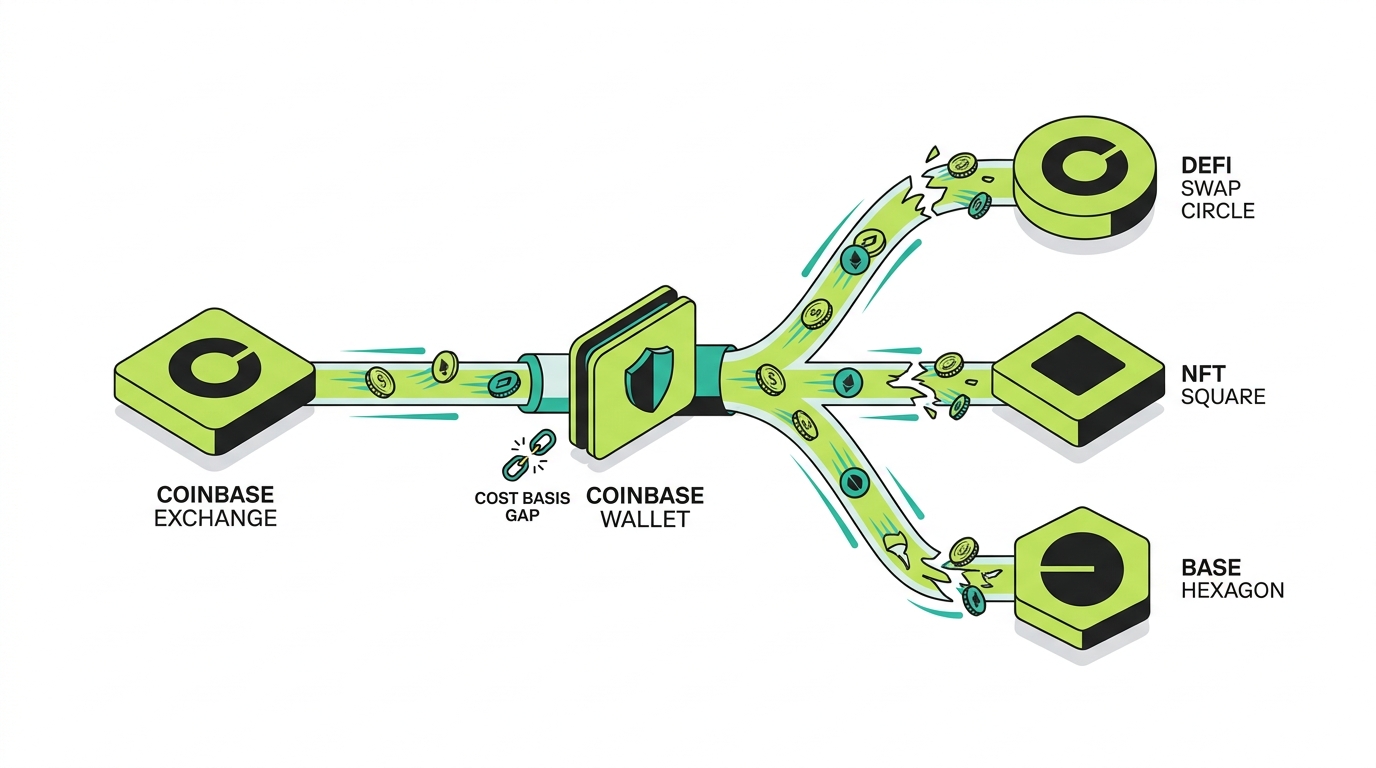

It matters because basis and reporting live in different places. Your cost basis usually originates on the Coinbase exchange, where you bought the crypto with dollars. Your taxable disposals usually happen in Coinbase Wallet, where you swap, sell into DeFi, or trade on Base. If those two halves are never connected, your tax software sees disposals with no basis and assumes you owe tax on the entire proceeds. That is how a self-custody user ends up with a wildly overstated gain.

Coinbase keeps your books while the crypto is on the exchange. The instant it lands in Coinbase Wallet, the bookkeeping becomes yours.

Do You Owe Taxes On Coinbase Wallet?

Yes, if you had taxable events. Holding crypto in the wallet is not taxable, but disposing of it or earning it is.

IRS Property Rules

The IRS treats virtual currency as property for federal tax purposes under Notice 2014-21. That classification drives the whole system: when you dispose of property you realize a capital gain or loss, and when you earn property you realize ordinary income. Coinbase Wallet does not change these rules, it just means you are the one applying them.

Capital Gains

Capital gains apply when you dispose of crypto: selling it for dollars, swapping it for another token, or spending it. Your gain or loss equals what you received in fair market value minus your cost basis. Hold the asset one year or less and the gain is short-term, taxed at ordinary rates. Hold it more than a year and the gain is long-term, taxed at the lower 0, 15, or 20 percent rates.

Ordinary Income

Ordinary income applies when you earn crypto: staking rewards, liquid staking yield, lending interest, and airdrops are taxed at their fair market value when you gain control of them. That value also becomes your cost basis for a later sale.

Does Coinbase Wallet Report To The IRS?

This is the question that drives the most search traffic, and the honest answer requires separating the two Coinbase products.

What Coinbase Reports

The Coinbase exchange is a custodial broker. It runs KYC, knows your identity, and starting with the 2025 tax year is part of the broker world that issues Form 1099-DA for digital asset sales on the platform. It can also provide gain/loss reports and transaction history for activity that happened on Coinbase.com. If you bought and sold on the exchange, expect Coinbase to report it. See our full Coinbase exchange tax guide for how the custodial platform reports to the IRS.

What Coinbase Wallet Reports

Coinbase Wallet reports nothing. As a self-custody wallet, it is not a broker holding your funds, so it does not file 1099 forms about your swaps, transfers, DeFi trades, or NFT activity. Do not wait for a form that is never coming. The reporting responsibility for wallet activity is entirely yours.

Blockchain Transparency

“Coinbase Wallet does not report” is not the same as “my activity is invisible.” Ethereum, Base, and other chains are public, permanent ledgers. The moment your wallet is linked to something that knows your identity, the chain becomes traceable back to you. The most common link is the most ironic one: you withdrew crypto from the Coinbase exchange (which has your KYC identity) directly into your Coinbase Wallet address. That single transfer ties your “anonymous” wallet to your verified identity forever.

1099-DA Reporting

Form 1099-DA is the new digital asset reporting form. Brokers like the Coinbase exchange report gross proceeds, and over time basis reporting expands. The problem for Coinbase Wallet users is the gap between what the exchange reports and what actually happened in self-custody. We cover this in depth in the dedicated 1099-DA section below, because it is one of the biggest reconciliation risks self-custody users face.

Coinbase Wallet Transactions That Are Not Taxable

Not every action is a taxable event. These generally are not taxable.

Buying Crypto

Buying crypto with US dollars is not taxable. It simply sets your cost basis, which is what you paid including fees. This is the basis that must follow your crypto when it moves into Coinbase Wallet.

Holding Crypto

Holding crypto, tokens, or NFTs in Coinbase Wallet is never taxable, no matter how much the value changes. Unrealized gains are not taxed until you dispose of the asset.

Transfers Between Your Own Wallets

Moving crypto between wallets you own and control is not a taxable event. Your basis carries with the asset. The small network fee you pay can be a tiny taxable disposal of the asset used to pay it, but the transfer itself is not a sale.

Moving Assets To Coinbase Wallet

Sending crypto from the Coinbase exchange into Coinbase Wallet is a transfer between your own accounts, not a sale, so it is not taxable. The critical caveat is basis: the original purchase price must travel with the asset, or your records will show a zero-basis disposal later.

Posting Collateral

Depositing crypto as collateral in a lending protocol, where you retain ownership and can withdraw it, is generally treated as a non-taxable transfer rather than a disposal. The treatment can shift if the protocol takes ownership or if your collateral is liquidated, which we cover in the DeFi section.

Coinbase Wallet Transactions That Are Taxable

These are the events that create a tax bill.

Selling Crypto

Selling crypto for dollars or stablecoins is a taxable disposal. Gain or loss equals proceeds minus cost basis.

Swapping Tokens

Swapping one token for another, including through Uniswap, Aerodrome, or any connected DEX, is a taxable disposal of the token you gave up, even though no dollars are involved. This is the single most common taxable event Coinbase Wallet users overlook.

Spending Crypto

Spending crypto on goods or services is treated as a sale of that crypto at its fair market value, triggering a capital gain or loss.

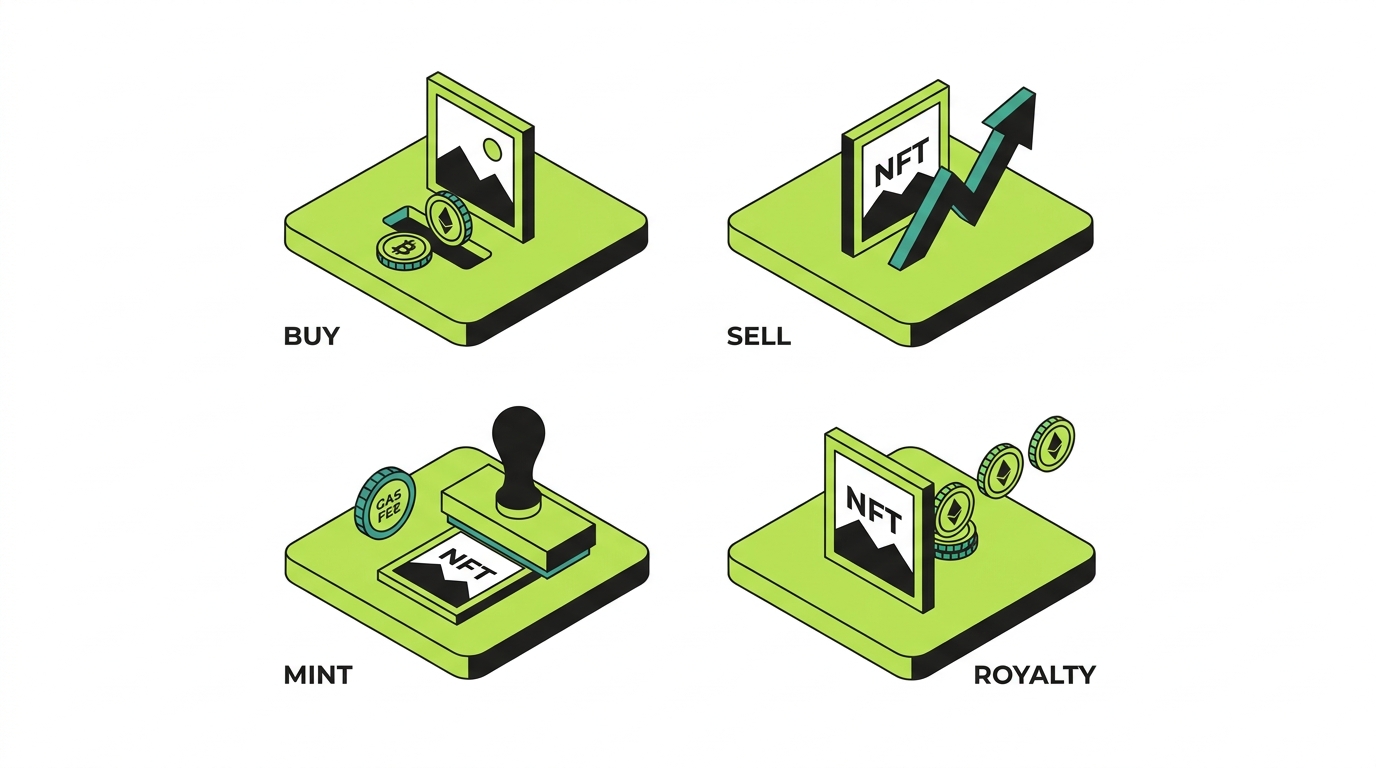

NFT Sales

Selling an NFT is a taxable disposal. Buying an NFT with crypto also disposes of that crypto, so a single NFT purchase can create two events.

Token Redemptions

Redeeming, unwrapping, or burning a token for another asset is generally a disposal of the token you gave up. Wrapping and unwrapping the same asset one-for-one is a gray area often treated as non-taxable, but redemptions that change what you hold are usually taxable.

Coinbase Wallet and Base Network Taxes

This is the biggest SEO and content gap in the entire Coinbase Wallet tax landscape, and it is where this guide goes where competitors do not. Coinbase Wallet adoption is heavily tied to Base, the Ethereum Layer 2 network incubated by Coinbase. If you use Coinbase Wallet, there is a strong chance most of your on-chain activity actually happens on Base.

What Is Base

Base is a low-fee Ethereum Layer 2 built on the OP Stack and closely associated with Coinbase. It hosts a fast-growing ecosystem of DeFi protocols, memecoins, NFT marketplaces, and consumer apps. From a tax standpoint, the key point is simple: Base activity is taxed exactly like Ethereum activity. The IRS taxes crypto as property regardless of the network, so Base does not get special treatment, and “it was just on Base” is not a defense for not reporting.

Base DeFi

Base DeFi runs through protocols like Aerodrome, Uniswap, and others. Every swap is a taxable disposal, providing liquidity can be a disposal of the tokens you deposit, and yield and rewards are ordinary income. Low Base fees encourage high transaction counts, which means a single active month can produce hundreds of taxable events that automated imports often mislabel.

Base Memecoins

Base has become a major memecoin venue, and memecoins are a tax minefield because of volume. Every swap of SOL-style velocity, where you flip in and out of tokens constantly, is a separate taxable disposal. Hundreds of trades means hundreds of events, almost all short-term. The upside is that the losses are just as real as the gains, and capturing every loss is how active traders avoid overpaying.

Base NFTs

Base hosts active NFT marketplaces. Buying an NFT with ETH on Base disposes of that ETH, selling an NFT is a taxable disposal, minting uses crypto and sets the NFT’s basis, and royalties are ordinary income. The same rules as Ethereum NFTs apply, just on a cheaper, faster chain that encourages more activity.

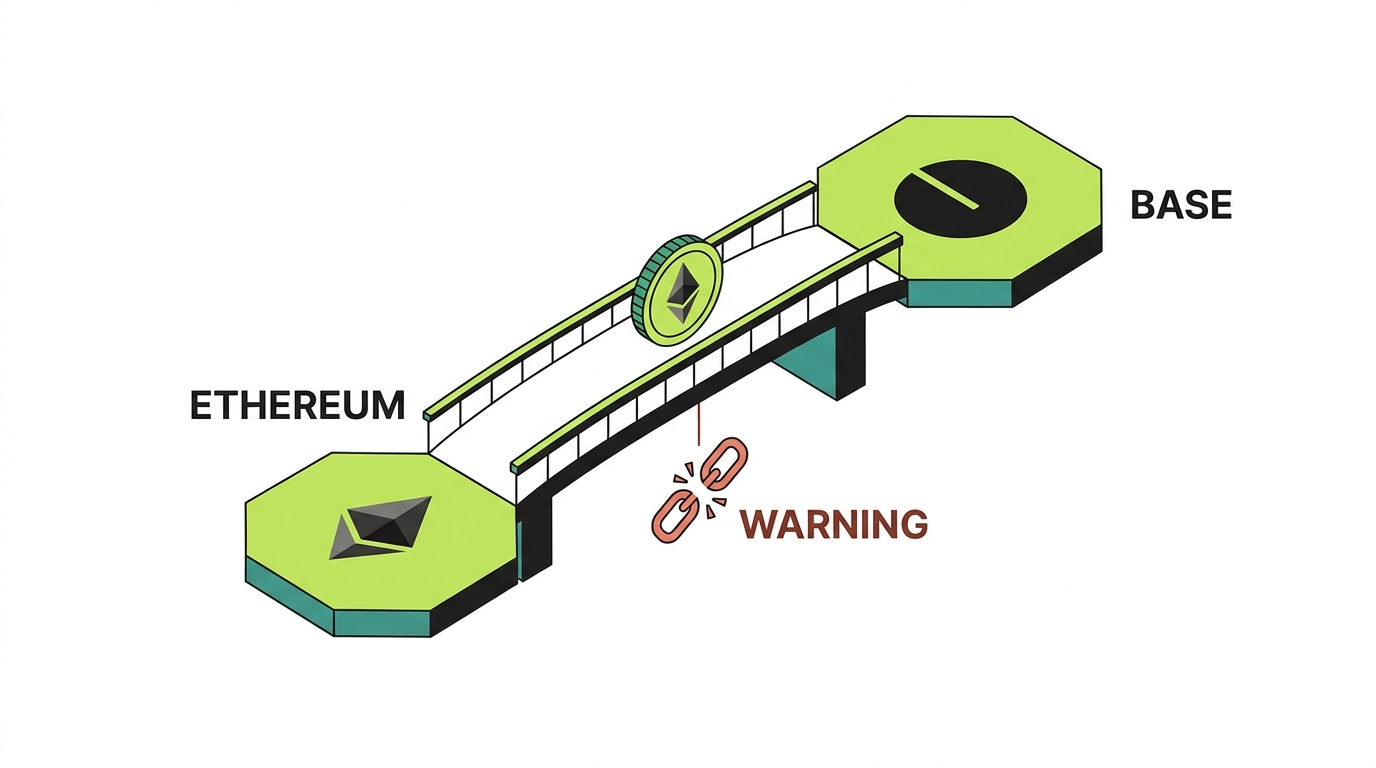

Base Bridges

Getting assets onto and off of Base usually involves a bridge, and bridging is a genuinely unsettled area. Moving the same asset across the official bridge while keeping ownership is often treated as a non-taxable transfer. But if the bridge wraps or swaps your token into a different asset, it may be a taxable disposal. The bigger practical risk is lost basis, because bridges frequently break the chain of cost-basis tracking that software relies on.

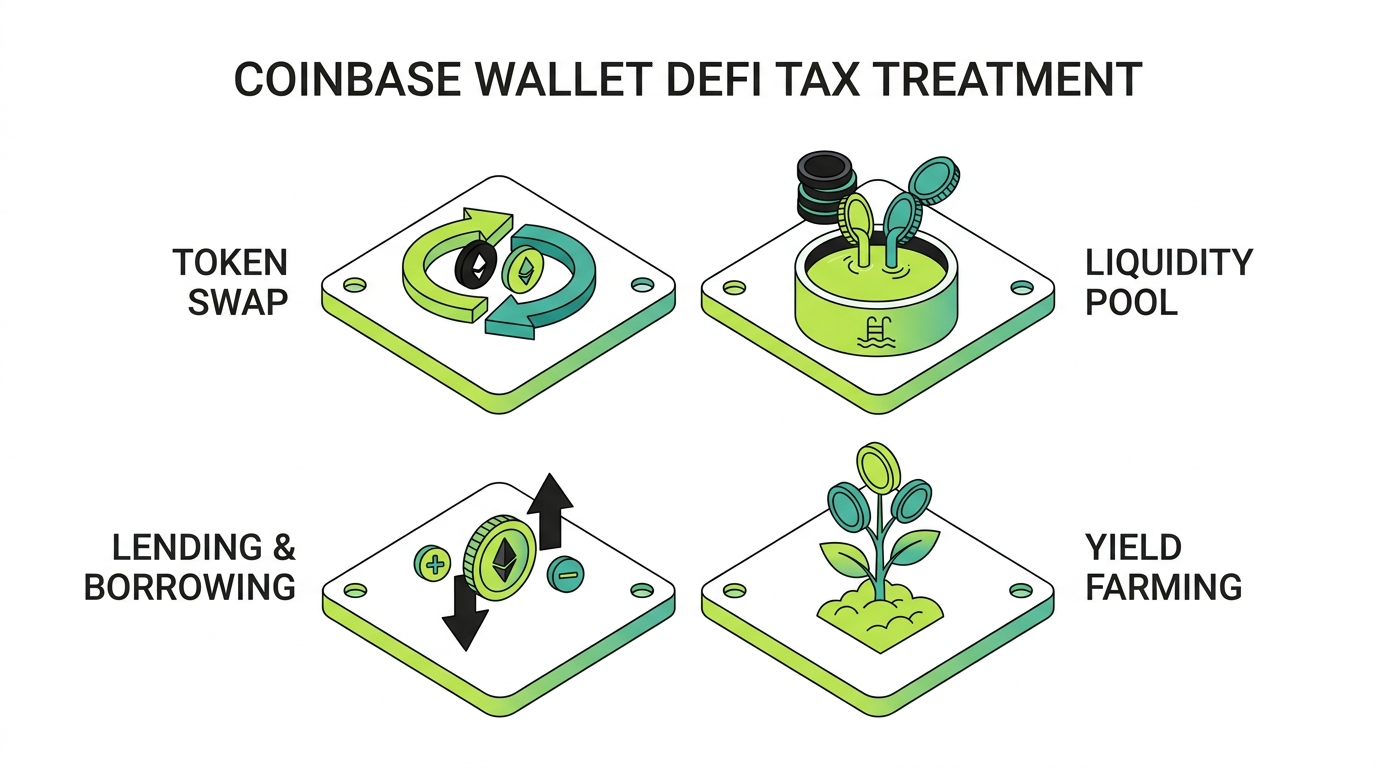

Coinbase Wallet DeFi Taxes

DeFi is where Coinbase Wallet power users carry the most risk, and it is one of the most under-explained topics in existing content. Coinbase Wallet connects to protocols on Ethereum and Base, and each interaction has a tax consequence.

Uniswap

Uniswap swaps are taxable disposals of the token you give up. Providing liquidity to a Uniswap pool can be a disposal of the deposited tokens depending on how LP tokens are issued, and the LP token itself can carry its own basis and disposal events when you redeem it.

Aerodrome

Aerodrome is a leading DeFi protocol on Base. Swaps, liquidity provision, and reward emissions all have tax consequences: swaps are disposals, and the reward tokens you earn (often the protocol token) are ordinary income at fair market value when received.

Liquidity Pools

Depositing into a liquidity pool, receiving an LP token, having it rebalance, and redeeming it can read as a chain of swaps with unclear basis. Whether the initial deposit is taxable depends on the protocol’s mechanics, which is exactly the kind of judgment call that software gets wrong.

Yield Farming

Yield farming rewards are ordinary income at fair market value when you gain control of them. That value becomes the cost basis of the reward tokens, so selling them later is a separate capital gain or loss.

Lending

Supplying assets to a lending protocol and earning interest produces ordinary income on the interest. Whether the deposit itself is a disposal depends on whether you receive a receipt token that changes what you hold.

Borrowing

Taking a loan against your crypto collateral is generally not a taxable event when you receive the borrowed funds, because a loan is not income. The tax appears if your collateral is liquidated, which is a taxable disposal of the collateral that was sold to cover the loan.

Leveraged Positions

Leveraged and perpetual positions add complexity: opening, closing, funding payments, and liquidations can each have tax consequences, and gains are typically short-term. Document every position, because these are among the hardest items for software to reconstruct.

Coinbase Wallet Staking Taxes

Staking is a common source of ordinary income for Coinbase Wallet users, especially around ETH.

ETH Staking

Native ETH staking rewards are ordinary income at fair market value when you gain dominion and control over them. That value becomes your cost basis in the reward ETH, so a later sale is a separate capital gain or loss.

Liquid Staking

Liquid staking through tokens like a staked-ETH receipt token adds a wrinkle. You receive a token whose value grows against ETH rather than discrete payouts. Whether the initial conversion is a taxable swap is unsettled: the conservative view records a disposal at conversion, while the more aggressive view defers until you redeem. The value accrual is generally realized when you swap or unstake.

Reward Income

All staking rewards, native or liquid, are income when received. Tracking the value at each accrual point across a year is tedious but necessary, and per-reward valuations are an area to spot-check because small timing differences add up.

Cost Basis Treatment

The amount you report as income becomes your basis in the reward tokens. Report rewards once as income when received, and again as a capital gain or loss when sold, not twice as income.

ETH Staking Example

Coinbase Wallet NFT Taxes

Coinbase Wallet users frequently interact with NFTs across Ethereum and Base, and each action has its own treatment.

Buying NFTs

Buying an NFT with crypto disposes of the crypto you spent, which is a taxable event measured from your basis in that crypto. The amount you pay, including fees, becomes the NFT’s cost basis.

Selling NFTs

Selling an NFT is a taxable disposal. Gain or loss equals proceeds minus your cost basis, including mint and marketplace fees. Some collectibles may face a higher long-term capital gains rate, an evolving area worth flagging for high-value long-term sales.

Minting NFTs

Minting uses crypto, which disposes of that crypto, and your total mint cost including gas becomes the NFT’s basis.

Royalties

Creator royalties you earn are ordinary income at fair market value when received.

Airdrops

NFT and token airdrops you claim and control are ordinary income at fair market value on receipt, which becomes your basis. Unsolicited scam NFTs and spam tokens are a known gray area and should be reviewed rather than auto-booked as income.

NFT With ETH Example

Bridge Transactions and Coinbase Wallet

Bridging is common for Coinbase Wallet users moving between Ethereum and Base, and it is a major content gap because the treatment is genuinely unsettled.

Ethereum to Base

Moving ETH from Ethereum to Base through the official bridge, where you hold the same asset on the other side, is often treated as a non-taxable transfer of your own property. Keep records so basis carries across.

Base to Ethereum

The same logic applies in reverse. Bridging back is generally a non-taxable transfer when the asset is unchanged, but the basis must follow.

Cross-Chain Bridges

Third-party cross-chain bridges that swap or wrap your asset into a different token are more likely to be taxable disposals, because what you hold afterward is not the same asset you started with.

Wrapped Assets

Wrapping ETH to WETH one-for-one is commonly treated as non-taxable, but bridged or wrapped variants that represent a different asset can be disposals. The treatment depends on the mechanics, so document each one.

Bridge Failures

Failed or stuck bridge transactions still cost gas and can leave assets in limbo. Document failures, because a lost or unrecoverable asset may eventually support a loss claim, and the gas spent has its own treatment.

Gas Fees and Coinbase Wallet Taxes

Gas fees are unavoidable on-chain, and they affect your taxes more than most people realize.

Network Fees

For investors, gas paid to acquire an asset generally adds to its cost basis, and gas paid to dispose of an asset generally reduces your proceeds. Gas on a purely personal transfer is usually not separately deductible.

Swap Fees

Fees paid during a swap are part of the cost of that transaction and factor into the gain or loss on the disposal.

NFT Mint Fees

Gas paid to mint an NFT is added to the NFT’s cost basis, increasing what you can later deduct against the sale price.

Failed Transactions

Failed transactions are common, especially during congestion, and they still cost gas. The treatment of gas on a failed transaction is unsettled and fact-specific, so document it and ask a professional rather than guessing.

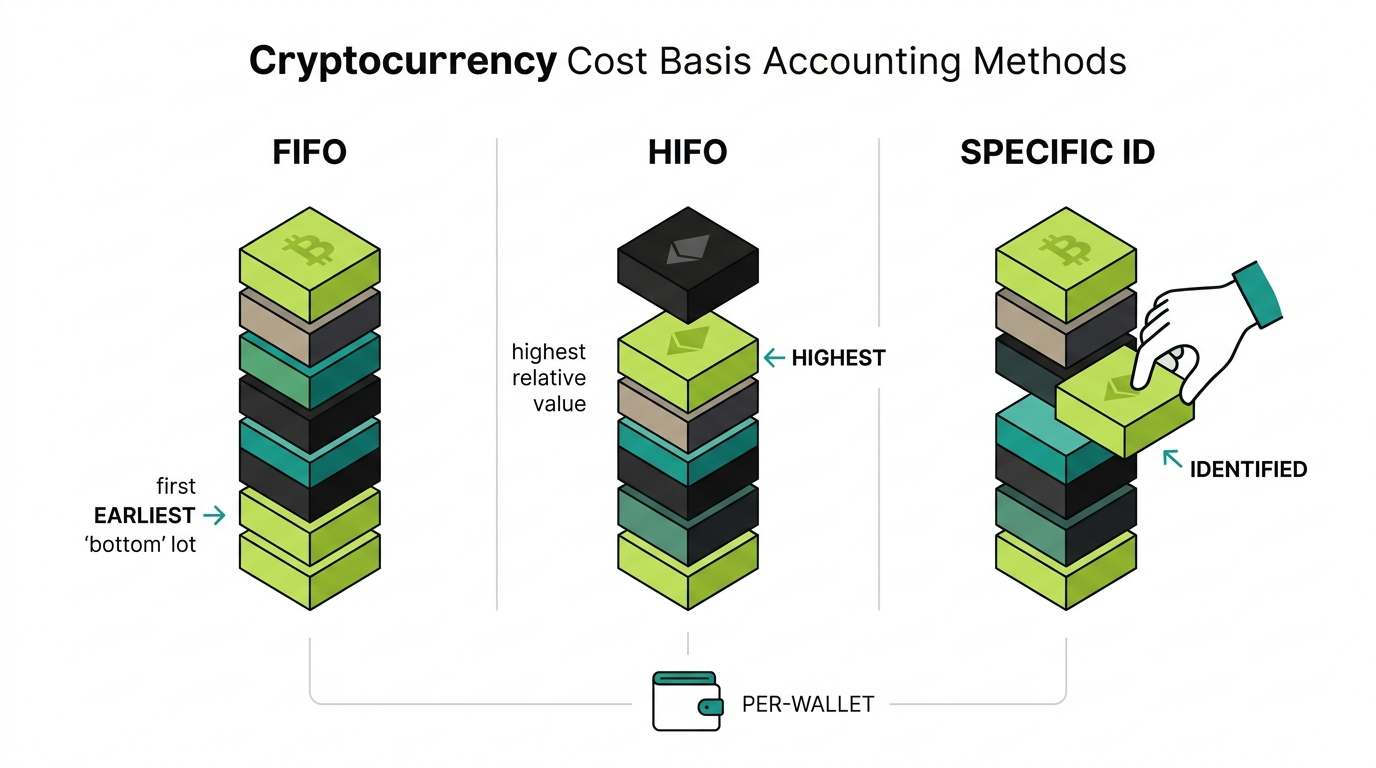

How To Calculate Coinbase Wallet Cost Basis

Cost basis is what you paid for an asset, and it determines your gain or loss when you dispose of it. You can use one of several methods, applied consistently.

FIFO

First In, First Out is the IRS default. It assumes the first units you acquired are the first you dispose of. It is simple but in a rising market it tends to produce larger gains.

HIFO

Highest In, First Out assumes you dispose of your highest-cost units first, which usually minimizes gains in a heavy-trading year. It demands clean records to defend.

Specific Identification

Specific Identification lets you choose exactly which lot you are disposing of, giving the most control over gains and losses. It requires the strongest recordkeeping, because if you cannot prove which lot you sold, you fall back to FIFO.

Wallet-Level Tracking

Beyond the method, Coinbase Wallet users face a structural rule. Under IRS Revenue Procedure 2024-28, effective January 1, 2025, cost basis must be tracked per wallet or account. Universal pooling across all wallets is no longer allowed. Your Coinbase Wallet is its own bucket, the Coinbase exchange is another, and any other wallet is another. Transfers between them are not taxable, but the basis must carry with the asset.

How To Export Coinbase Wallet Transaction History

Coinbase Wallet does not produce a finished report, so exporting is about getting your raw history into a tool that can.

Wallet Address Method

Your public wallet address is the master key to your history. Copy it, and any addresses you used on other networks like Base, and provide them to your tax software, which reads the chain directly. Because Coinbase Wallet is multi-chain, capture every address on every network you touched.

Block Explorer Method

A block explorer for Ethereum or Base lets you view and export the raw transaction list for your address. This is useful for verifying or filling gaps, though raw explorer data still needs to be priced and categorized.

Tax Software Imports

The practical path is to import your wallet addresses into crypto tax software, then separately import your Coinbase exchange history via CSV or API so transfers reconcile and basis follows the asset. Reconcile wallet by wallet, because each address is its own ledger under the per-wallet rule.

Best Coinbase Wallet Tax Software

No tool fully automates messy self-custody history, but the right one does most of the heavy lifting. The best choice depends on your volume and how much DeFi, NFT, and Base activity you have.

CoinTracker

CoinTracker is a widely used option that Coinbase has partnered with, which makes the Coinbase and Coinbase Wallet import path relatively smooth. Strong for portfolio tracking and mainstream activity.

CoinLedger

CoinLedger is popular for its clean Form 8949 generation and straightforward import flow, and it handles common DeFi and NFT activity well.

Koinly

Koinly supports a very large number of chains and exchanges, which helps for multi-chain Coinbase Wallet users who touch Base, Ethereum, and beyond.

TokenTax

TokenTax pairs software with optional professional services, useful when your history is complex enough to want hands-on help.

ZenLedger

ZenLedger is another established option with broad integration support and tax-loss harvesting tools.

Summ

Summ is a newer entrant focused on streamlined crypto tax reporting, sometimes surfaced through wallet partner pages.

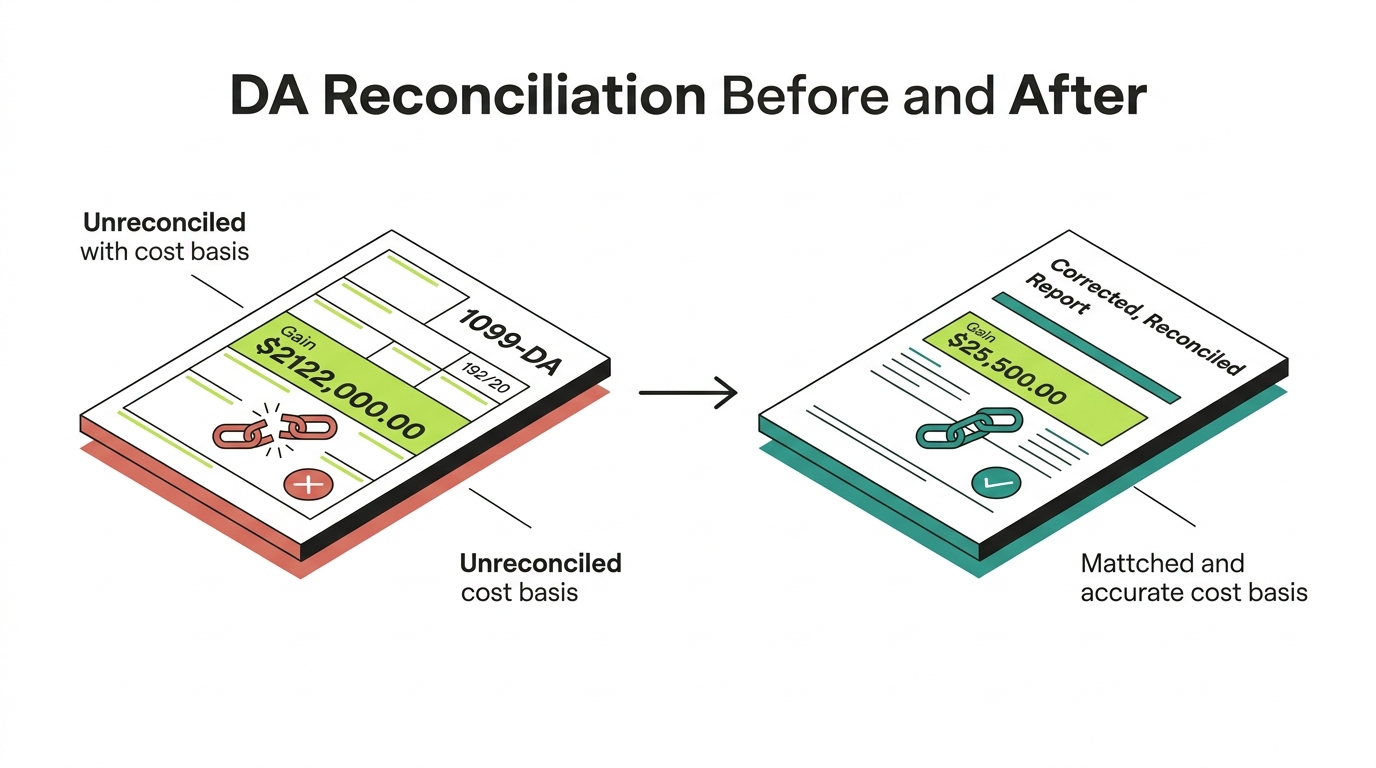

Coinbase Wallet and 1099-DA

Form 1099-DA deserves its own section because it is the reconciliation problem that will define Coinbase Wallet taxes through 2026 and beyond.

Broker reporting. The Coinbase exchange is a broker and reports digital asset sales on Form 1099-DA, starting with gross proceeds and expanding over time. This covers what you did on the custodial platform.

Self-custody implications. Coinbase Wallet is not a broker and reports nothing. So your 1099-DA reflects only the exchange side, never your wallet swaps, DeFi, or Base activity. You still owe tax on the wallet side regardless.

Missing basis. The core trap is that when you moved assets from the exchange into Coinbase Wallet and later sold elsewhere, or sold back on the exchange, the form may show proceeds with little or no basis. Without reconciliation, the IRS sees a much larger gain than you actually had.

Reconciliation challenges. Matching the exchange’s 1099-DA to your true cost basis requires connecting both Coinbase data and full wallet history, then proving the transfers between them. This is the heart of self-custody tax work.

IRS matching. Because the exchange reports under your KYC identity and your wallet links back to it through transfers, the IRS can increasingly spot mismatches between what was reported and what you filed. Clean reconciliation is your defense.

Your 1099-DA tells the exchange’s half of the story. The IRS sees that half. Your job is to file the whole story so the two halves reconcile.

Common Coinbase Wallet Tax Mistakes

Assuming Coinbase Handles Everything

The number one mistake. Coinbase reports your exchange activity, not your self-custody wallet. Treating them as one is how people underreport without realizing it.

Missing Cost Basis

When assets move from the exchange or another wallet and the basis does not follow, software assumes zero and overstates your gain. This is the most expensive common error.

Ignoring Base Transactions

Many users forget that Base activity is fully taxable, or assume their software captured it. Base is often the single largest source of unreported events for Coinbase Wallet users.

Ignoring NFTs

NFT buys, sells, mints, and the hidden crypto disposal behind each purchase are frequently left out entirely.

Ignoring DeFi

Liquidity, lending, farming, and reward income on Uniswap and Aerodrome are routinely missed or mislabeled.

Missing Wallets

Under the per-wallet rule, leaving out an address breaks the basis chain. Every wallet and every chain has to be included.

Duplicate Transactions

Importing the same activity from both a wallet connection and a CSV can double-count events, inflating gains. De-duplication is part of a clean reconciliation.

How To Prepare For A Coinbase Wallet Tax Audit

This is a major content gap, and audit readiness is exactly where a reconciliation mindset pays off.

Recordkeeping

Keep a complete record of every wallet address, every exchange account, every transfer, and the dollar value and date of each taxable event. Your records are your defense.

Wallet Hygiene

Use clear, consistent wallets and label them. Avoid mixing personal, trading, and experimental activity in ways that make history impossible to reconstruct later.

Transfer Documentation

Document every transfer between the Coinbase exchange, Coinbase Wallet, and any other wallet, with the date, asset, amount, and the basis that traveled with it. Transfers are where basis dies, so they are where audits focus.

DeFi Documentation

For DeFi positions, record what you deposited, what receipt tokens you got, what rewards you earned and when, and what you redeemed. Reconstructing this after the fact is the hardest part of a self-custody return.

Audit Trail Maintenance

Maintain a clean, dated audit trail that ties each reported number back to source data. The goal is that any line on your Form 8949 can be traced to a real transaction with a defensible basis.

Assets bounced between Coinbase, Coinbase Wallet, Base, and DeFi?

That is exactly the history DIY tools get wrong. We reconcile your full Coinbase Wallet and exchange activity into defensible, CPA-ready numbers.

See how it worksWhere Count On Sheep Fits

Coinbase gives you an easy on-ramp. Coinbase Wallet gives you self-custody and access to DeFi, NFTs, staking, and Base. The cost is that the reconciliation layer is missing, and that is the exact problem we solve. The exchange issues a 1099-DA that only tells half the story, the wallet reports nothing, software imports are imperfect, and Base and DeFi activity often needs manual review while wallet-level cost basis raises the bar for clean records.

Count On Sheep prepares CPA-ready Digital Asset Reconciliation for Coinbase and Coinbase Wallet users: we connect the exchange and every wallet, match transfers so basis follows the asset, handle the Base, DeFi, and NFT edge cases, reconcile against your 1099-DA, and produce a defensible Form 8949 and income report you can actually file behind. We are a crypto tax reconciliation service, not a CPA firm, and we work alongside your tax preparer.

Not sure your crypto taxes are right?

Talk to a Count On Sheep specialist. We will spot the costly errors before you file. No obligation.

Book My Free Review- Reviewed by Former Big 4 Accountants

- Keep your CPA

- No pressure, no sales pitch

Related Reading

- Ultimate MetaMask Tax Guide 2026

- Ultimate Phantom Wallet Tax Guide 2026

- Crypto Tax Guide 2026: IRS Rules, Forms and Rates

- Form 1099-DA Explained for 2026

- How to File Crypto Taxes With Form 8949 and Schedule D

- Per-Wallet Crypto Cost Basis: Rev. Proc. 2024-28

This guide is educational and not tax or legal advice. Digital asset rules change frequently, and several positions discussed here (bridging, wrapping, liquid staking, DeFi deposits) are unsettled. Consult a qualified CPA about your specific Coinbase Wallet and Base activity.

Frequently Asked Questions

Does Coinbase Wallet report to the IRS?

Coinbase Wallet is a self-custody wallet, so it does not file 1099 forms or report your wallet activity to the IRS the way the Coinbase exchange does. This is the single biggest point of confusion: the Coinbase exchange (Coinbase.com) is a custodial broker that can issue tax documents, while Coinbase Wallet is a separate self-custody app where you control the keys and you are responsible for tracking and reporting. Your on-chain activity is still public and traceable, and you still owe tax on every taxable event.

Is Coinbase Wallet the same as Coinbase?

No. Coinbase (the exchange at Coinbase.com) is a custodial platform that holds your crypto, runs KYC, and can issue tax forms. Coinbase Wallet is a separate self-custody wallet app where you hold your own private keys and connect to DeFi, NFTs, and networks like Base. They have completely different tax reporting situations, and assuming they are the same is the most common Coinbase Wallet tax mistake.

Does Coinbase Wallet issue 1099 forms?

No. As a self-custody wallet, Coinbase Wallet does not issue Form 1099-DA or any other 1099 for your wallet swaps, transfers, or DeFi activity. The Coinbase exchange may issue 1099-DA for assets you sold through the custodial platform starting with the 2025 tax year. You reconcile any exchange 1099-DA against your own Coinbase Wallet records, because the wallet itself is not the form issuer.

Do I pay taxes on Coinbase Wallet transfers?

Moving your own crypto between your own wallets, including from the Coinbase exchange to Coinbase Wallet or from Coinbase Wallet into a DeFi protocol you control, is generally not a taxable event. The catch is that your cost basis must travel with the asset. If the basis is lost in transit, your tax software may assume a zero basis and overstate your gain when you later sell.

Are Base transactions taxable?

Yes. Activity on the Base network is taxed exactly like activity on Ethereum or any other chain, because the IRS taxes crypto as property regardless of which network it lives on. Base swaps, memecoin trades, NFT sales, and DeFi disposals are all taxable events, and Base staking, yield, and airdrops are ordinary income at fair market value when received.

Are Coinbase Wallet swaps taxable?

Yes. Swapping one token for another inside Coinbase Wallet, including through Uniswap, Aerodrome, or any connected DEX, is a taxable disposal of the token you gave up. You calculate a capital gain or loss based on the fair market value at the moment of the swap minus your cost basis, even when no US dollars are involved.

How do I calculate gains in Coinbase Wallet?

Your gain or loss on each disposal equals the fair market value you received minus your cost basis in the asset you gave up. Cost basis is what you originally paid, including fees. Because Coinbase Wallet is self-custody and assets often arrive from the Coinbase exchange or other wallets, the work is connecting every source so the original basis follows the asset into the wallet and out again.

What tax forms do I need for Coinbase Wallet?

Most Coinbase Wallet users report capital gains and losses on Form 8949 and Schedule D, and report crypto income such as staking, rewards, and airdrops on Schedule 1 or Schedule C depending on the activity. You also answer the digital asset question on Form 1040. If you sold through the Coinbase exchange, reconcile any Form 1099-DA against your own records.

Does Coinbase Wallet give you tax documents?

No finished tax documents. Coinbase Wallet does not produce a filing-ready report. It lets you export or view your transaction history, and it integrates with tax software, but turning that history into a Form 8949 is on you or your tax software. The Coinbase exchange is the side of the business that issues tax documents, not the self-custody wallet.

How do I report Coinbase Wallet NFTs?

Selling an NFT held in Coinbase Wallet is a taxable disposal reported on Form 8949, with gain or loss equal to proceeds minus your cost basis including mint and marketplace fees. Buying an NFT with crypto also disposes of that crypto, which is a separate event. Royalties you earn are ordinary income, and a genuinely worthless NFT may support a capital loss if you can document it.

How do I report Coinbase Wallet staking rewards?

Report the fair market value of staking and liquid staking rewards as ordinary income for the year you gain control of them, typically on Schedule 1 for an investor. That value becomes your cost basis in the reward tokens, so when you later sell or swap them you report a separate capital gain or loss on Form 8949.

Can the IRS see Coinbase Wallet activity?

Potentially yes. Coinbase Wallet does not report to the IRS, but Ethereum, Base, and other chains are public and permanent. The moment your wallet is linked to a KYC source, such as a withdrawal from the Coinbase exchange into your Coinbase Wallet address, blockchain analysis can connect that wallet to your identity. Treat your activity as reportable and traceable.

What happens if I don't report Coinbase Wallet taxes?

Failing to report taxable crypto activity can lead to back taxes, penalties, and interest, and in serious cases more severe consequences. Because the Coinbase exchange issues 1099-DA and your wallet activity links back to that exchange, the IRS has a growing ability to spot mismatches. If you are behind, the safest move is to reconcile your full history and file accurately, ideally with professional help.

Is Coinbase Wallet self-custody?

Yes. Coinbase Wallet is a self-custody wallet, meaning you hold your own private keys and Coinbase does not control your funds. This is the defining feature that separates it from the custodial Coinbase exchange and the reason the tax recordkeeping is your responsibility rather than the platform's.

Do I owe taxes if I only hold crypto in Coinbase Wallet?

No. Simply holding crypto, NFTs, or tokens in Coinbase Wallet is not a taxable event. You only owe tax when you trigger a taxable event such as selling, swapping, spending, or earning crypto. Unrealized gains on assets you continue to hold are not taxed.

Are Coinbase Wallet gas fees deductible?

It depends on context. For investors, network fees paid to acquire an asset generally add to its cost basis, and fees paid to dispose of an asset generally reduce your proceeds. Fees on purely personal transfers or failed transactions are usually not separately deductible. Treatment differs for traders and businesses, so document every fee and ask a professional how it applies to you.

How do I export Coinbase Wallet transaction history?

Take your public wallet address, and any addresses on other networks you used such as Base, and import them into crypto tax software like CoinTracker, CoinLedger, or Koinly, which pulls your on-chain history. You can also pull data from a block explorer. Because Coinbase Wallet is multi-chain, capture every address on every network you touched, and import your Coinbase exchange history separately so transfers reconcile.

What is the best Coinbase Wallet tax software?

Strong options for Coinbase Wallet and Base activity include CoinTracker (which Coinbase has partnered with), CoinLedger, Koinly, TokenTax, and ZenLedger. The best choice depends on your transaction volume and how much DeFi, NFT, and Base activity you have. No tool fully automates messy self-custody history, so plan on reviewing the import for missing basis and mislabeled DeFi transactions.

How do I handle a 1099-DA from Coinbase with my wallet activity?

The 1099-DA from the Coinbase exchange reports activity on the custodial platform, not your self-custody Coinbase Wallet. Problems arise when assets moved between the two and basis did not follow, because the form can show proceeds with little or no basis, inflating your apparent gain. You reconcile the form against your own complete records so the gain you report reflects reality, not the form's gap.

Do I have to track each Coinbase Wallet separately?

Yes. Under IRS Revenue Procedure 2024-28, effective January 1, 2025, cost basis must be tracked per wallet or account rather than pooled universally. Your Coinbase Wallet is its own bucket, and transfers between your own wallets are not taxable but the basis must carry with the asset.

Are airdrops in Coinbase Wallet taxable?

Generally yes, when you have dominion and control over the tokens and they have a fair market value, which is ordinary income at receipt and becomes your cost basis. Be careful with unsolicited spam or scam tokens that appear in your wallet, which are a known gray area and should be reviewed rather than automatically booked as income.

Are Coinbase Wallet DeFi transactions taxable?

Yes. DeFi swaps on Uniswap, Aerodrome, or any connected protocol are taxable disposals, and yield, farming rewards, and lending interest are ordinary income at fair market value when received. Providing liquidity can be a disposal of the deposited tokens depending on the protocol. DeFi is one of the most under-reported areas of Coinbase Wallet activity because software frequently mislabels it.

How are Coinbase Wallet bridge transactions taxed?

Moving the same asset across the official Base bridge while keeping ownership is usually a non-taxable transfer, but if a bridge wraps or swaps your token into a different asset it can be a taxable disposal. The bigger practical risk is lost cost basis, because bridges often break the chain of basis tracking that tax software relies on.

Are Base memecoins taxable?

Yes. Every Base memecoin swap is a taxable disposal of the token you gave up, almost always short-term and taxed at ordinary rates. High trade volume on Base means hundreds of taxable events, but the losses are just as deductible as the gains, so capturing every trade is how active traders avoid overpaying.

Does Coinbase Wallet work with TurboTax?

Not directly as a finished report. The usual path is to run your Coinbase Wallet history through crypto tax software like CoinTracker, CoinLedger, or Koinly, which generates a Form 8949 you can then import into TurboTax or hand to your preparer. Coinbase Wallet itself does not produce a TurboTax-ready file.

What records should I keep for Coinbase Wallet taxes?

Keep every wallet address, every exchange account, the date and dollar value of each taxable event, and documentation of every transfer between the Coinbase exchange, Coinbase Wallet, and other wallets so basis follows the asset. For DeFi, record deposits, receipt tokens, rewards, and redemptions. These records are your defense if you are ever audited.

Do I owe taxes when I move crypto from Coinbase to Coinbase Wallet?

No. Sending crypto from the Coinbase exchange to your own Coinbase Wallet is a transfer between your own accounts, not a sale, so it is not taxable. The important part is that the cost basis from your original purchase must travel with the asset, or a later sale may show a zero basis and an overstated gain.

How do I report Coinbase Wallet on my tax return?

Report each taxable disposal on Form 8949 with dates, proceeds, cost basis, and gain or loss, then carry the totals to Schedule D. Report crypto income like staking and airdrops on Schedule 1 or Schedule C, and answer the digital asset question on Form 1040. Crypto tax software can generate the 8949 from your imported wallet history.

Are Coinbase Wallet to Coinbase Wallet transfers taxable?

No. Moving assets between two wallets you own and control is not a taxable event. Your basis carries with the asset. The small network fee used to pay for the transfer can be a tiny taxable disposal of the asset spent on gas, but the transfer itself is not a sale.

What is the biggest Coinbase Wallet tax mistake?

Assuming Coinbase handles everything. The Coinbase exchange reports your on-platform activity, but Coinbase Wallet is self-custody and reports nothing. Treating the two as one leads people to underreport their wallet swaps, Base activity, DeFi, and NFTs without realizing it. The fix is reconciling the exchange and the wallet together.

Can Count On Sheep help with Coinbase Wallet taxes?

Yes. Count On Sheep provides CPA-ready Digital Asset Reconciliation for Coinbase and Coinbase Wallet users: connecting the exchange and every wallet, matching transfers so basis follows the asset, handling Base, DeFi, and NFT edge cases, reconciling against your 1099-DA, and producing a defensible Form 8949 and income report. We are a reconciliation service that works alongside your tax preparer.