The IRS is done being patient with crypto investors. In 2026, exchanges are issuing Form 1099-DA for the first time, per-wallet cost tracking is mandatory, and the digital asset checkbox on your Form 1040 now cross-references broker-reported data. The grace period for vague crypto tax reporting is over.

Whether you traded one Bitcoin or one thousand tokens, you need to understand the rules, because the IRS already has your data.

Disclaimer: This guide is for informational purposes only. Cryptocurrency regulations are rapidly evolving. Always consult a qualified CPA regarding your specific situation.

Find Yourself: Which Crypto Taxpayer Are You?

For wallet-specific reporting quirks, browse our guides by wallet, by exchange, and by coin.

The Casual Holder

You bought some BTC or ETH on Coinbase, held it, and haven’t sold.

Good news: you might not owe anything yet. Jump to Taxable Events →The Active Trader

You swap tokens frequently across multiple exchanges with a messy transaction history.

You need the new per-wallet rules and cost basis methods. Jump to Per-Wallet Tracking →The Yield Farmer

You earn daily staking rewards, lending interest, or LP yields from DeFi protocols.

Your situation is complex and income-heavy. Jump to Crypto Income Tax →The Loss Harvester

Your portfolio took a hit and you want to use those losses to lower your tax bill.

You can use this to your advantage. Jump to Tax-Loss Harvesting →The Panic Searcher

You got an IRS letter or your 1099-DA looks wildly wrong and you’re terrified.

Don’t panic. Here’s exactly how to respond. Jump to IRS Audits →How Does the IRS Classify Cryptocurrency?

Cryptocurrency is classified as property by the IRS. As of 2026, every time you sell, trade, or spend digital assets, you trigger a taxable event subject to capital gains tax according to IRS Notice 2014-21.

This means crypto is treated like stocks or real estate, not like dollars in your bank account. The classification has been in effect since 2014, and it determines everything about how you’re taxed.

The Digital Asset Question on Form 1040

Every US taxpayer must answer the digital asset question on page one of Form 1040: “At any time during 2025, did you receive, sell, send, exchange, or otherwise acquire any interest in digital assets?”

If you owned crypto at any point, even if you only held, you must check “Yes.” The IRS uses this as a compliance trigger.

Want the full breakdown? Read our deep dive: How Is Crypto Taxed in the US? (2026 Guide).

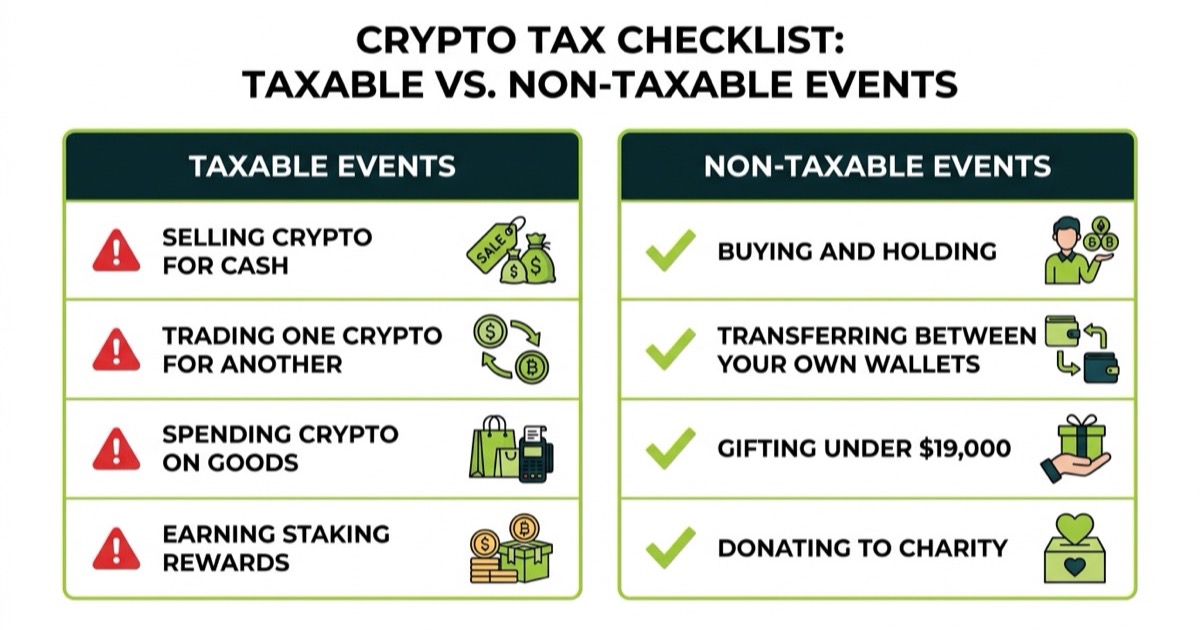

Taxable vs. Non-Taxable Crypto Events

Here’s the thing: not everything you do with crypto triggers taxes. Understanding the difference saves you from over-reporting and unnecessary panic.

What Triggers a Taxable Event?

- Selling crypto for USD (or any fiat currency)

- Trading one crypto for another (e.g., BTC → ETH)

- Spending crypto on goods or services

- Earning crypto (staking, mining, airdrops, wages)

What is NOT Taxable?

Transferring cryptocurrency between your own wallets is not a taxable event. As of 2026, moving assets from Coinbase to a Ledger hardware wallet does not trigger capital gains, provided you retain ownership of both.

Other non-taxable events:

- Buying crypto with fiat and holding

- Gifting crypto under the $19,000 annual exclusion

- Donating crypto to a qualified 501(c)(3) charity

Is Buying Crypto Taxable?

No, unless you’re buying one crypto with another crypto. Purchasing Bitcoin with USD is not a taxable event. But swapping ETH for a memecoin is.

Need the complete list? See our Taxable vs Non-Taxable Crypto Events cheat sheet.

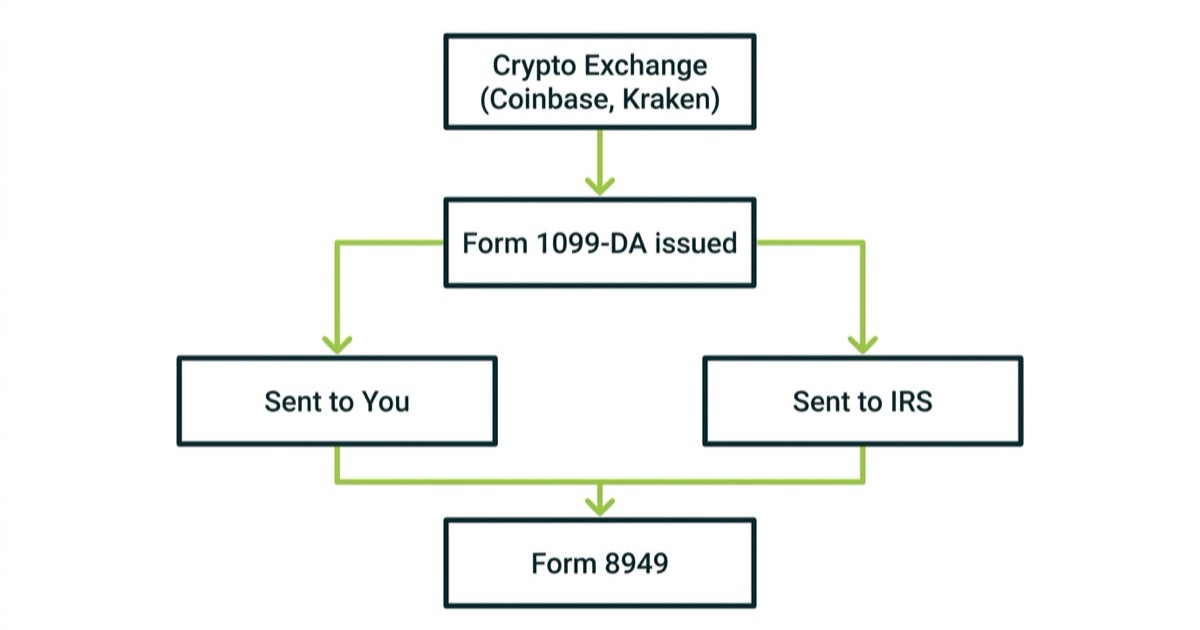

The Big Change for 2026: Form 1099-DA

Form 1099-DA is a tax reporting document for digital assets. Starting in the 2025 tax year and filed in 2026, centralized exchanges must issue Form 1099-DA to report your crypto proceeds to both you and the IRS.

This is the single biggest compliance change in crypto tax history. The IRS now receives the same transaction data you do.

Why Your 1099-DA Cost Basis Might Be Wrong

Here’s where it gets interesting. When you transfer crypto from one exchange to another, the receiving exchange often doesn’t know your original purchase price. They may report a $0 cost basis, making your entire sale look like pure profit.

While Form 1099-DA rules take effect for the 2025 tax year (filed in 2026), the IRS frequently updates reporting timelines, so always verify the latest broker requirements before filing.

How to Reconcile Missing Data

You are responsible for maintaining accurate cost basis records. If your 1099-DA shows incorrect basis, you must reconcile it using your own records, crypto tax software, or a crypto tax specialist.

Want to reconcile your 1099-DA step by step? Read Form 1099-DA Explained: What It Is and How to Reconcile It.

Understanding Crypto Capital Gains Tax

When you sell crypto for more than you paid, the profit is a capital gain. The tax rate depends on how long you held the asset.

Short-Term vs. Long-Term Capital Gains

- Short-term (held ≤ 365 days): Taxed at your ordinary income rate (10% to 37%)

- Long-term (held > 365 days): Taxed at preferential rates (0%, 15%, or 20%)

Long-term capital gains apply to crypto held for more than one year. In 2026, these long-term gains are taxed at preferential rates of 0%, 15%, or 20%, depending on your overall taxable income.

2026 Capital Gains Tax Brackets

For single filers (2026):

- 0% on taxable income up to ~$48,350

- 15% on income from ~$48,351 to ~$533,400

- 20% on income above ~$533,400

Real Example: Calculating Your Tax Bill

Now, let’s look at a real example:

You buy 1 BTC at $30,000 in March 2025. You sell it for $90,000 in May 2026 (held > 1 year).

- Gain: $90,000 - $30,000 = $60,000

- Single filer making $80,000 salary: Falls in the 15% long-term bracket → $9,000 federal tax

- Single filer making $550,000 salary: Falls in the 20% bracket → $12,000 federal tax (plus 3.8% NIIT)

For detailed bracket tables and calculations at every income level, see 2026 Crypto Capital Gains Tax Brackets.

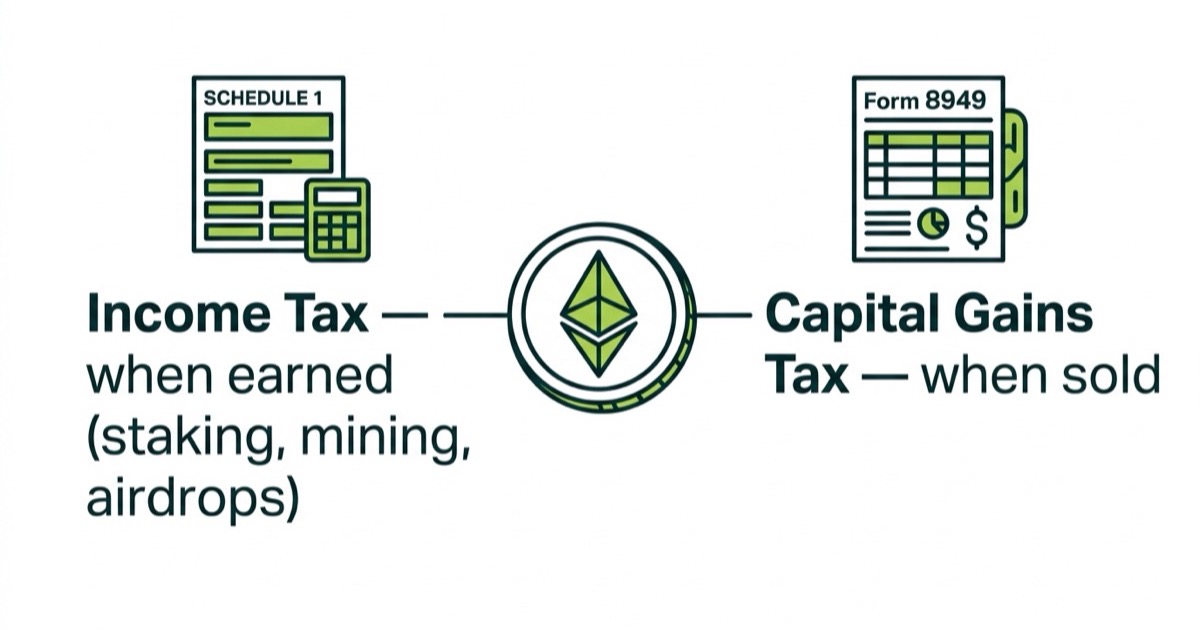

Understanding Crypto Income Tax

Not all crypto taxes come from selling. If you earn crypto, it’s taxed as ordinary income at Fair Market Value (FMV) on the day you receive it.

Staking Rewards and Mining

Staking rewards are classified as ordinary income. Under Revenue Ruling 2023-14, you must report the Fair Market Value of staking rewards as income the moment you gain dominion and control over the tokens.

Revenue Ruling 2023-14 solidifies that cash-method taxpayers must include staking rewards in gross income at their FMV when received.

Despite ongoing litigation regarding whether staking is taxable upon receipt or only upon sale, the current official IRS stance mandates taxation upon receipt.

Example: You stake $5,000 of ETH and receive 0.05 ETH when ETH is at $3,000. That’s $150 of ordinary income reported on Schedule 1. If you later sell that 0.05 ETH at $4,000/ETH ($200), you owe capital gains on the $50 profit.

Airdrops and Hard Forks

Under Revenue Ruling 2019-24, you owe ordinary income tax on the fair market value of a hard fork airdrop the exact moment you have dominion and control over the new coins.

If the airdrop is worth $0 at receipt and you sell later for $500, your cost basis is $0 and the full $500 is capital gain.

Getting Paid in Crypto

Crypto wages are subject to income tax, Social Security, and Medicare, just like a regular paycheck. Self-employed individuals report on Schedule C and owe self-employment tax (15.3%) in addition to income tax.

Staking rewards are taxed at their Fair Market Value the exact moment they hit your wallet, giving you dominion and control.

Staking, mining, airdrops, and wages each have different rules. Get the full picture in How Crypto Income Tax Works.

The New Per-Wallet Cost Tracking Rule

Per-wallet tracking is mandatory for crypto cost basis. Under IRS Revenue Procedure 2024-28, investors must transition from universal basis tracking to a strict per-wallet allocation starting January 1, 2025.

Why does this matter for 2026? If you have crypto spread across Coinbase, Kraken, and a Ledger, each wallet is now its own cost-basis bucket. You can no longer pool all your purchases into one universal lot.

Universal vs. Wallet-Level Tracking

Before (pre-2025): All your BTC purchases across all wallets formed one pool. Sell from any wallet and pick any lot.

After (Jan 1, 2025): Each wallet tracks its own lots independently. Selling 1 BTC from Coinbase can only use lots that are in Coinbase.

The IRS requires a transition to per-wallet cost tracking effective January 1, 2025, meaning legacy universal tracking methods are no longer permitted.

The Safe Harbor Deadline

The safe harbor window for allocating legacy holdings to specific wallets closed on January 1, 2025. If you missed it, you may need to reconstruct records retroactively. A CPA or specialized software can help.

![]()

For a detailed walkthrough of Rev. Proc. 2024-28, read our Per-Wallet Crypto Cost Tracking guide.

Cost Basis Methods Explained

Your cost basis method determines which units are considered sold, and that choice can mean thousands in tax savings.

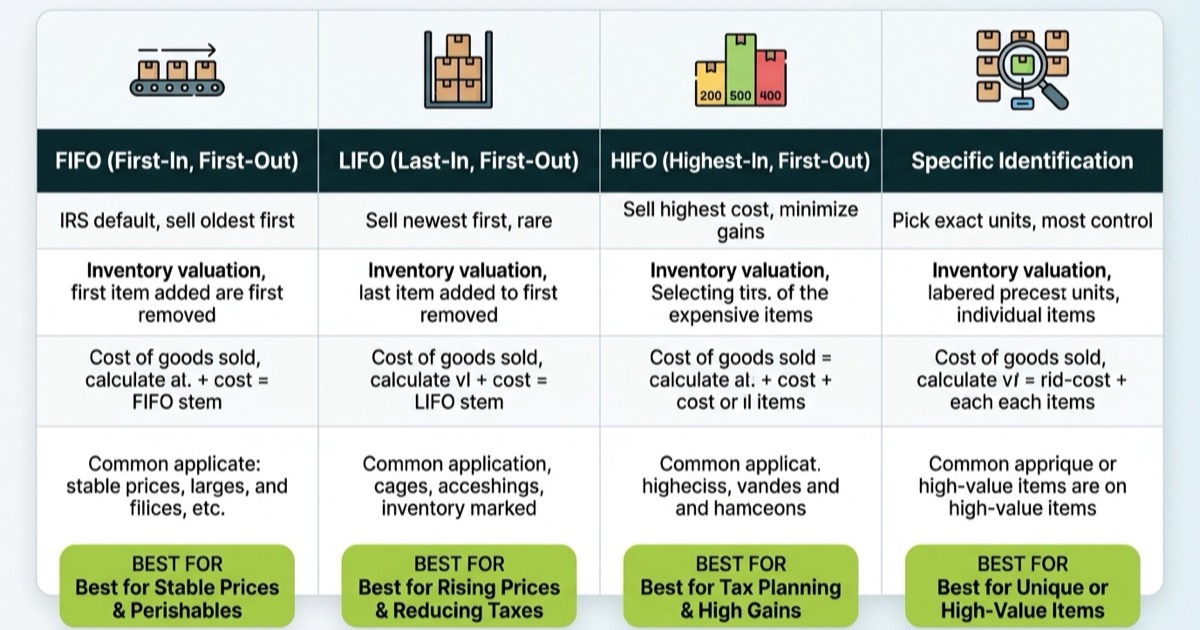

FIFO (First-In, First-Out)

FIFO is the IRS default. Your oldest purchased units are sold first. In a long-running bull market, FIFO often produces the highest gains because your oldest lots have the lowest cost.

HIFO (Highest-In, First-Out)

HIFO sells your most expensive lots first, minimizing your taxable gain. It’s a strategy within Specific Identification and is fully IRS-compliant with proper documentation.

Specific Identification

Spec ID gives you the most control: you pick exactly which lots to sell. It requires detailed record-keeping (date, amount, price, wallet) for every acquisition.

Real Example: FIFO vs. HIFO

You bought 1 ETH at $2,000, then 1 ETH at $3,500. You sell 1 ETH at $4,000.

Sells Oldest Lot First

$4,000 - $2,000 = $2,000 gain. FIFO picks the oldest (cheapest) lot.

Sells Most Expensive Lot First

$4,000 - $3,500 = $500 gain. HIFO picks the highest-cost lot, minimizing the gain.

See real math comparing all three methods in FIFO vs HIFO vs Spec ID for Crypto Taxes.

NFTs, DeFi, and Complex Taxes

Are NFTs Taxed Differently?

The IRS has not explicitly categorized all NFTs as collectibles, but art-based NFTs may be subject to the higher 28% collectible capital gains rate upon sale.

For non-art NFTs (gaming items, domain names, membership passes), the standard capital gains rates apply. The IRS is still developing guidance here, but you still owe taxes when you sell.

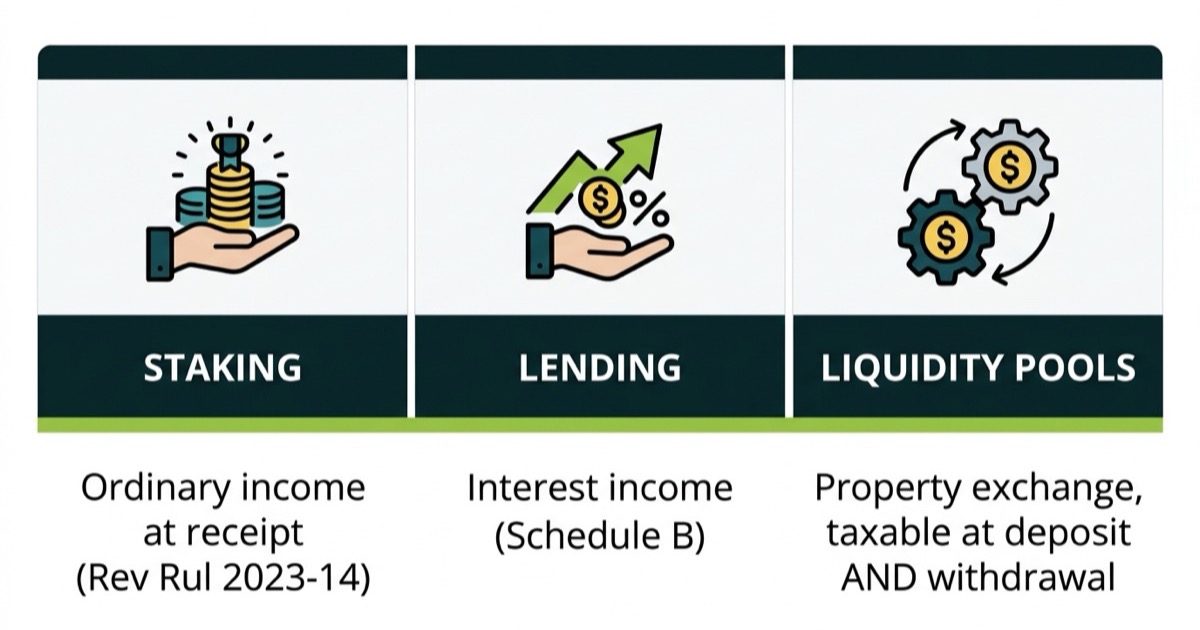

Liquidity Pools, Staking, and Lending

But here’s where it gets interesting for DeFi users. Each activity has different tax treatment:

- Staking: Ordinary income at receipt (Rev. Rul. 2023-14)

- Lending: Interest income reported on Schedule B

- Liquidity Pools: Depositing tokens is likely a taxable property exchange. Impermanent loss doesn’t reduce your tax bill until you withdraw.

Trading crypto within a self-directed IRA is generally tax-advantaged, but certain margin trades or complex DeFi yield farming can trigger Unrelated Business Taxable Income (UBTI) taxes.

LPs, wrapped tokens, and the 28% collectible risk: read NFT and DeFi Taxes: Liquidity Pools, Staking, Lending.

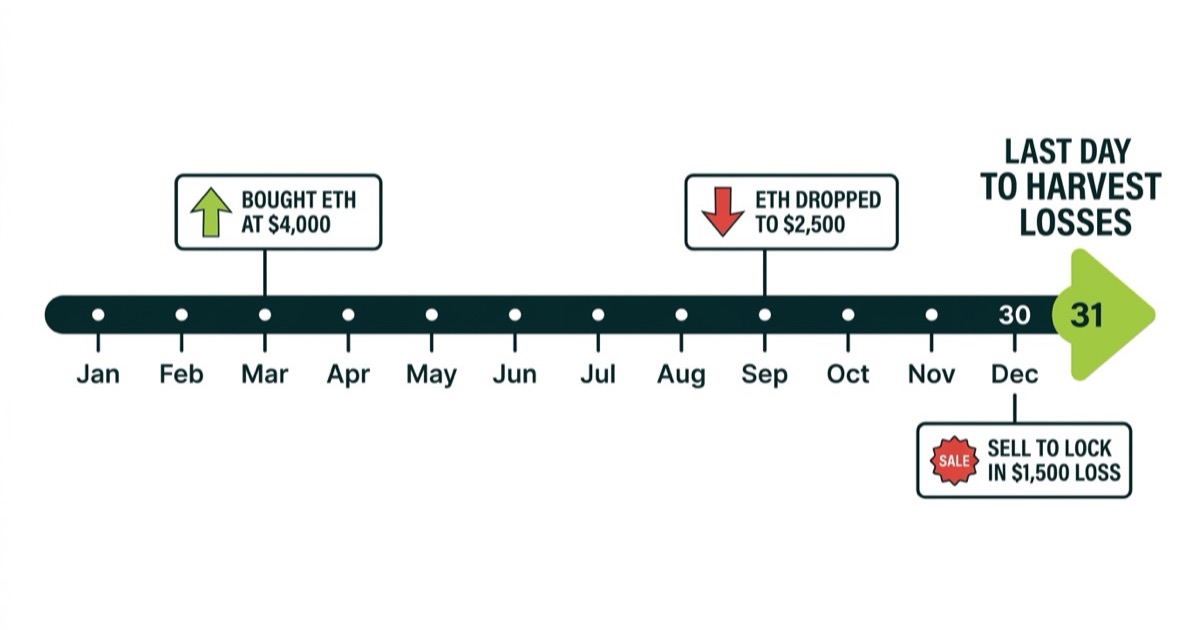

Crypto Tax-Loss Harvesting

If your portfolio is down, you can turn those paper losses into real tax savings by selling before year-end.

How to Offset Your Gains

Sell losing positions to realize capital losses. These losses directly offset your capital gains dollar-for-dollar. If your losses exceed gains, you get an additional deduction.

The maximum net capital loss deduction is strictly limited. As of 2026, you can deduct a maximum of $3,000 in crypto losses against your ordinary income, carrying over any remaining balance to future tax years.

The $3,000 Ordinary Income Deduction

After netting against gains, excess losses offset up to $3,000 of W-2 or other ordinary income per year. Remaining losses carry forward indefinitely.

Does the Wash Sale Rule Apply to Crypto in 2026?

The bottom line? Currently, the wash sale rule applies to “stocks and securities,” exempting cryptocurrency. You can sell at a loss and immediately repurchase the same token.

Currently, the wash sale rule applies to ‘stocks and securities’, exempting cryptocurrency, but Congress has proposed closing this loophole. Consult a CPA before harvesting massive, rapid losses.

For the full strategy, wash-sale status, and step-by-step instructions, read Crypto Tax-Loss Harvesting: 2026 Rules and Wash-Sale Status.

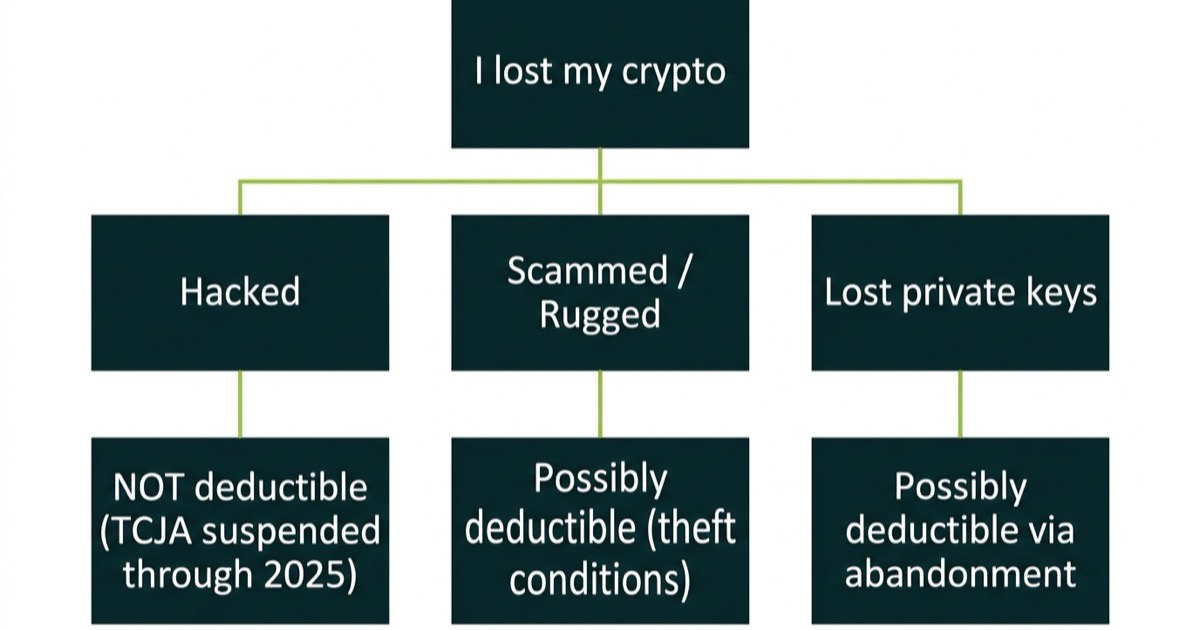

What Happens to Lost, Stolen, or Rugged Crypto?

Hacks vs. Scams

The Tax Cuts and Jobs Act (TCJA) suspended personal casualty losses through 2025, meaning stolen or hacked crypto is generally not deductible as a theft loss, though abandonment strategies may apply.

- Hacks: NOT deductible as a casualty loss under current law

- Scams/Rug pulls: Potentially deductible as a theft loss if you can prove fraudulent intent, but TCJA still blocks most claims through 2025

- Worthless tokens: May qualify for a capital loss via “abandonment” if the token has zero value and no market

Lost Keys and Worthless Tokens

If you’ve permanently lost access to your wallet, you may be able to claim a worthlessness deduction. Document the inaccessibility thoroughly. The IRS requires evidence that the asset has zero recovery potential.

Hacks, rug pulls, and worthless tokens each have different rules. Read Lost or Stolen Crypto: Are Losses Deductible in 2026?

Crypto Gambling, Sweepstakes, and Prediction Markets

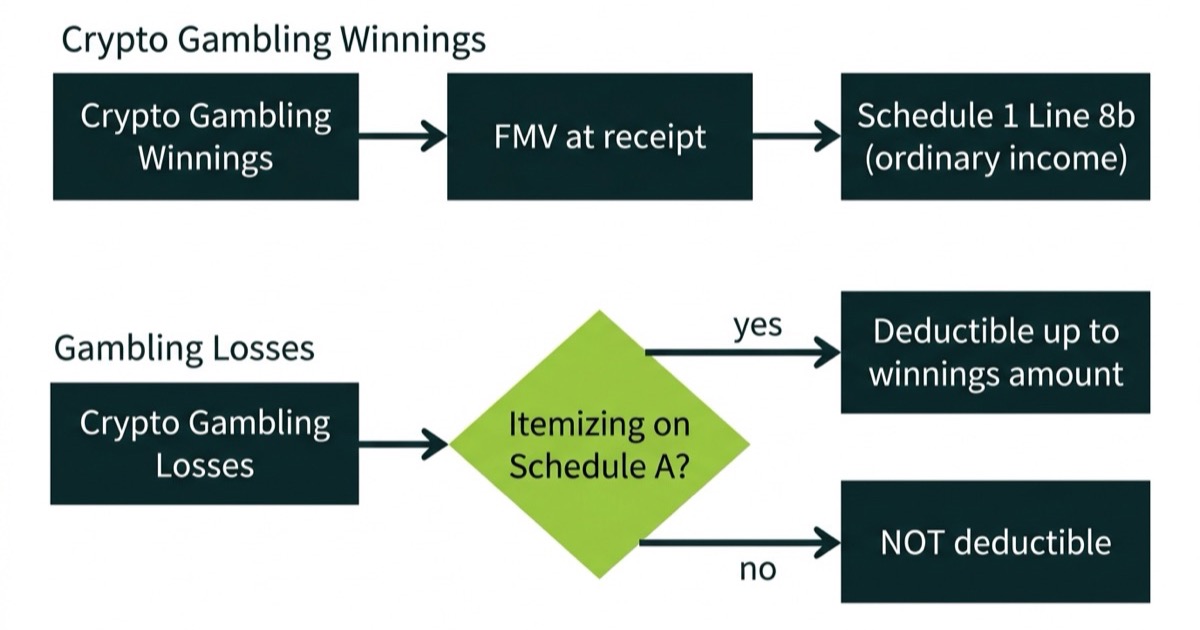

How Are Crypto Gambling Winnings Taxed?

Crypto gambling winnings are ordinary income taxed at Fair Market Value (FMV) at the time of receipt. Report them on Schedule 1, Line 8b (“Gambling winnings”).

The standard W-2G thresholds apply when the platform is a US-licensed payer: $1,200 for slots/bingo, $5,000 for poker tournaments, and $600 at 300:1 odds for other wagers. Offshore crypto casinos (Stake.com, BC.Game, Rollbit) generally don’t issue W-2Gs, but the income is still fully taxable.

What about prediction markets? The IRS has not formally classified payouts from platforms like Polymarket or Kalshi. Current best practice: treat prediction-market winnings as gambling income unless a specific ruling says otherwise.

Can I Deduct Crypto Gambling Losses?

Yes, but only against winnings, only if you itemize on Schedule A, and only up to the amount of winnings reported.

Real example: You won $5,000 in crypto gambling and lost $4,000. Your net taxable gambling income is $1,000, and you claim a $4,000 deduction on Schedule A (only available if you itemize). For non-itemizers (most filers post-TCJA), gambling losses cannot offset winnings at all.

Professional gamblers filing on Schedule C follow different rules and can deduct business expenses, but this is rare and triggers significant audit risk.

What Records Do You Need?

Keep detailed records: date, platform, deposit/withdrawal transaction hashes, and the USD amount at FMV at the time of each session. Offshore platforms may also trigger FBAR (FinCEN Form 114) or Form 8938 reporting if account balances cross reporting thresholds.

Prediction markets, W-2G thresholds, and offshore FBAR traps: see Crypto Gambling and Sweepstakes: 2026 Tax Rules.

Hidden Traps: FBAR, Gifts, and State Taxes

FBAR and Form 8938 for Foreign Exchanges

Holding crypto on foreign exchanges like Binance or KuCoin triggers FBAR reporting if your aggregate foreign accounts exceed $10,000 at any point in the year.

Form 8938 has higher thresholds ($50,000 for domestic filers, $200,000 for expats) but applies to the same foreign crypto holdings.

2026 Gift Tax Thresholds

The annual gift tax exclusion applies to cryptocurrency. For the 2026 tax year, you can gift up to $19,000 worth of digital assets to any individual without triggering gift tax reporting requirements.

For 2026, the annual gift tax exclusion is $19,000 per recipient, and the lifetime estate exemption sits at $15 million before taxes apply.

Example: You gift your sibling 0.5 BTC worth $20,000. The first $19,000 is excluded. The remaining $1,000 counts against your lifetime exemption. No tax owed, but you must file Form 709.

State Tax Nuances

Federal taxes apply to everyone, but state taxes vary wildly; states like Texas, Florida, and Washington have no state income tax, while New York strictly regulates activity via the BitLicense.

- TX, FL, WA, NV: No state income tax on crypto gains

- CA: Conforms to federal rules. Expect state tax of 9.3% to 13.3% on top

- NY: BitLicense reporting rules add a compliance layer for exchanges operating in the state

Deep dives on each topic: FBAR and Form 8938 for Crypto | Crypto Gift Tax 2026 | Crypto Taxes by State

Step-by-Step: How to File Your Crypto Taxes

Step 1: Gather Your Data

Export transaction histories from every exchange and wallet. Use crypto tax software (Koinly, CoinTracker, CoinLedger) or spreadsheets if your volume is low. For complex portfolios, work with a crypto tax specialist.

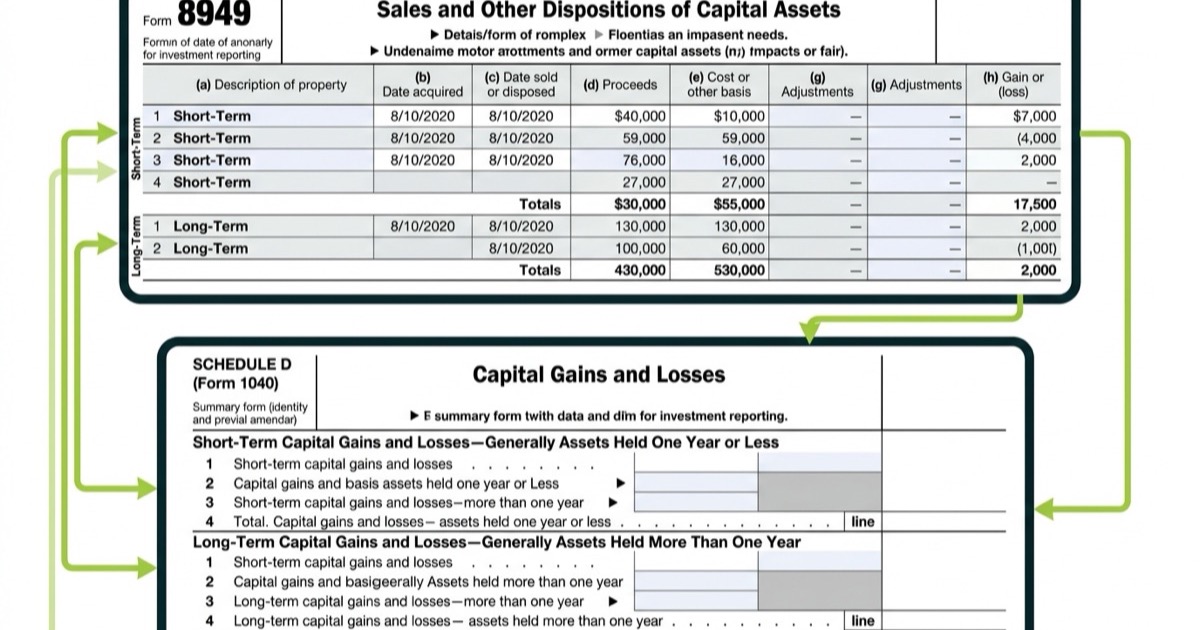

Step 2: Form 8949 (Individual Transactions)

List each disposal on Form 8949: date acquired, date sold, proceeds, cost basis, gain or loss. Short-term transactions go in Part I; long-term in Part II.

Step 3: Schedule D (Net Gains/Losses)

Transfer totals from Form 8949 to Schedule D. This form summarizes your net short-term gain/loss and net long-term gain/loss.

Step 4: Schedule 1 or Schedule C (Income)

Report staking, mining, and airdrop income on Schedule 1 (Line 8z for misc income). Self-employed crypto earners use Schedule C with quarterly estimated payments.

Need the full walkthrough? See How to File Crypto Taxes: Form 8949 and Schedule D.

IRS Audits: What to Do If You Get a Letter

Understanding Letters 6173, 6174, and 6174-A

The IRS sends three types of crypto letters:

- Letter 6173: Requests a response, the most serious. You must reply.

- Letter 6174: Informational: acknowledges your crypto activity.

- Letter 6174-A: Soft reminder to report properly. No response required, but take it seriously.

How to Respond

If you receive Letter 6173, gather your transaction records, calculate any unreported gains, and consider filing amended returns (Form 1040-X). Don’t ignore it. Silence escalates the situation.

An IRS Letter 6174-A isn’t necessarily an audit. It’s often just the IRS telling you they know you have crypto and reminding you to report it.

Got a letter? Read exactly how to respond in IRS Letters 6173, 6174, 6174-A: What to Do.

DIY Software vs. Hiring a Crypto CPA

When Software Is Enough

If you made fewer than 100 trades on 1-2 centralized exchanges, didn’t touch DeFi, and have straightforward buy/sell activity, tax software will handle it. Our picks for the best crypto tax software in 2026 can help you choose the right one.

When to Hire Count On Sheep

You need professional help if you have:

- DeFi activity (LPs, bridges, wrapping)

- Cross-chain transactions with broken basis trails

- An IRS letter or audit notice

- High-volume trading (1,000+ transactions)

- Missing cost basis or 1099-DA discrepancies

If any of these apply, reach out to our team for a crypto tax review.

Bottom Line: What to Do Next

The IRS has your data. Exchanges are reporting. Per-wallet tracking is mandatory. The question isn’t if you owe taxes on crypto. It’s how much and how to minimize it legally.

Your action plan:

- Check your 1099-DA. Verify cost basis accuracy. Don’t assume it’s correct.

- Organize by wallet. Each wallet is its own cost-basis bucket now.

- Harvest losses before December 31. The crypto wash-sale exemption won’t last forever.

- Consider HIFO. If you’re in a bull market, selling your highest-cost lots first reduces your bill.

- File on time. Extensions give you until October 15, but estimated taxes are still due quarterly.

If your crypto tax situation is more than simple buys and sells, don’t go it alone. A 15-minute call with a crypto tax specialist can save you thousands, and a lot of stress.

Frequently Asked Questions

What is crypto taxed as?

The IRS classifies cryptocurrency as property under Notice 2014-21. This means every sale, trade, or spending event is subject to capital gains tax, similar to selling stocks or real estate.

Do I pay taxes for holding crypto?

No. Simply holding (HODLing) cryptocurrency is not a taxable event. You only owe taxes when you sell, trade, spend, or earn crypto. Unrealized gains are not taxed.

How much crypto is tax-free?

There is no blanket exemption for crypto. However, if your total income (including crypto gains) stays within the 0% long-term capital gains bracket, you may owe $0 in federal tax on long-term holdings. For 2026, single filers pay 0% on taxable income up to approximately $48,350.

Is transferring crypto taxable?

No. Transferring cryptocurrency between your own wallets (e.g., Coinbase to a Ledger) is not a taxable event, provided you retain ownership of both wallets. However, you must track cost basis accurately across wallets.

What is the wash sale rule for crypto?

Currently, the wash sale rule under IRC Section 1091 applies only to stocks and securities, not cryptocurrency. This means you can sell crypto at a loss and immediately repurchase it to harvest the tax loss. However, Congress has proposed closing this loophole, so consult a CPA before relying on it.

Can I write off hacked crypto?

Generally no. The Tax Cuts and Jobs Act (TCJA) suspended personal casualty and theft losses through 2025. For 2026, stolen or hacked crypto is typically not deductible. However, if a token becomes truly worthless, you may claim an abandonment loss.

What is Form 1099-DA?

Form 1099-DA is a tax reporting document for digital assets. Starting in the 2025 tax year (filed in 2026), centralized exchanges like Coinbase and Kraken must issue this form to report your crypto proceeds to both you and the IRS.

Does Binance report to the IRS?

Binance.US (the regulated US entity) reports to the IRS and issues 1099 forms. However, the global Binance.com platform does not directly report to the IRS. Regardless, you are still legally required to report all income and gains from any exchange, foreign or domestic.