Where you live can change what you owe on crypto by tens of thousands of dollars. The IRS treats cryptocurrency as property at the federal level, but each state adds its own layer of taxation (or none at all). In 2026, the difference between holding crypto in Texas versus California can mean the difference between keeping your gains and handing over more than 13% of them to the state.

This guide covers every state. We start with deep dives on the four states people ask about most (Texas, Florida, California, and New York), then walk through all 50 states plus Washington, DC, a full comparison table, and the best states for crypto mining in 2026. State rates below reflect Tax Foundation data as of January 1, 2026, cross-checked against state revenue departments.

Federal vs. State Crypto Taxes: A Quick Overview

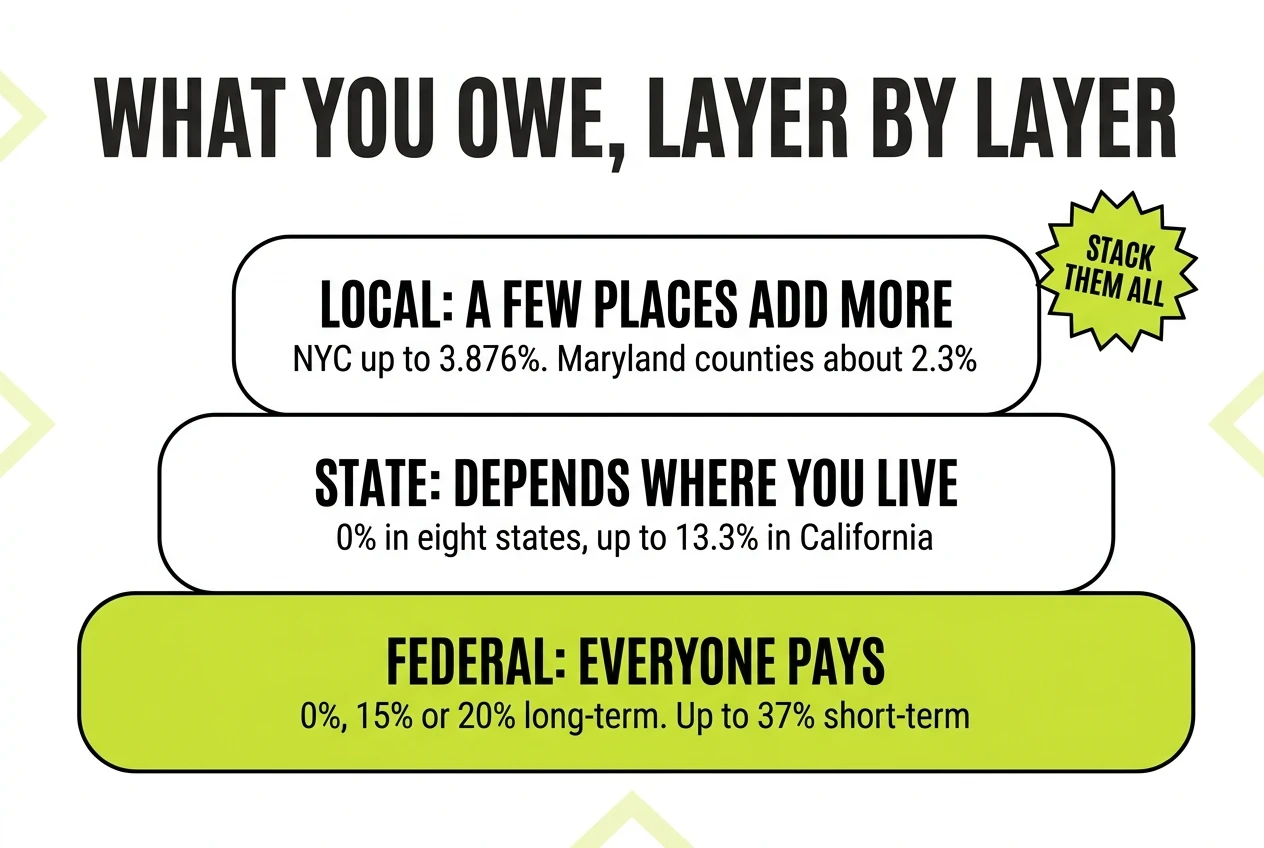

Before comparing states, it helps to understand the two layers of crypto taxation every U.S. investor faces.

Federal taxes apply uniformly. The IRS taxes crypto disposals (sales, trades, spending) as capital gains. Short-term gains (assets held under one year) are taxed at ordinary income rates up to 37%. Long-term gains (assets held over one year) are taxed at 0%, 15%, or 20% depending on your income. Crypto received as income (mining, staking, airdrops) is taxed as ordinary income. For a deeper look at how these rules work, see our guide on how crypto is taxed in the U.S.

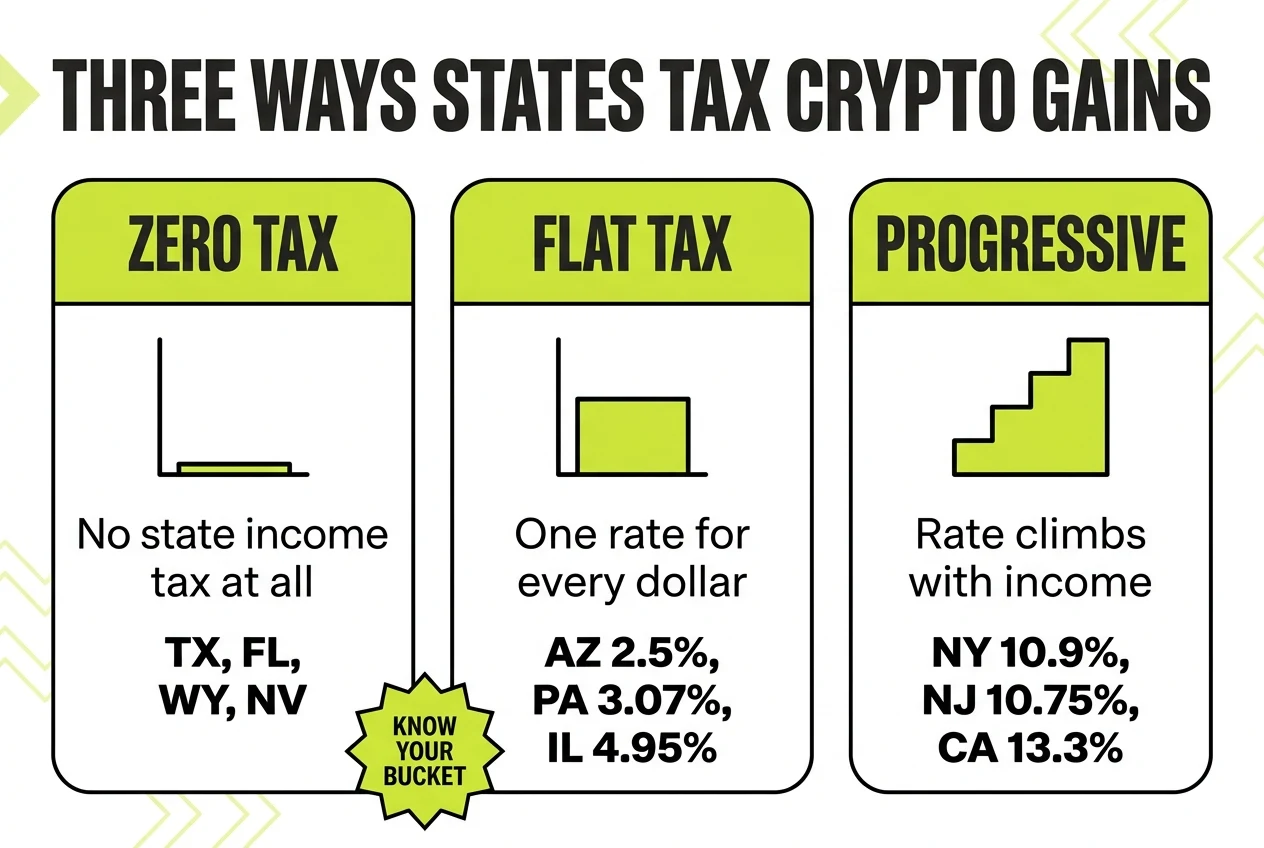

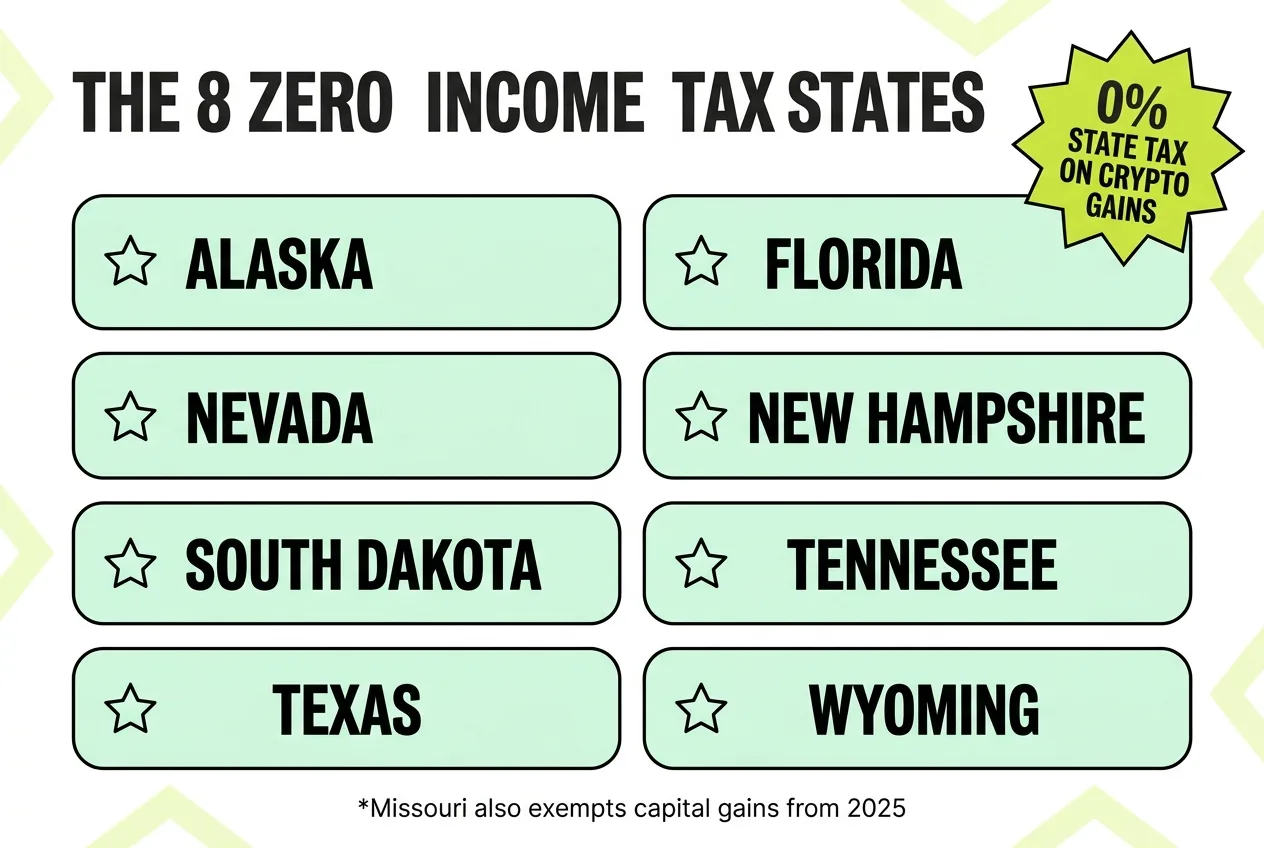

State taxes vary dramatically. Most states piggyback on federal rules and apply their own income tax rates on top, usually with no discount for long-term gains. Eight states have no income tax at all. A handful sit in between: they tax income but exclude part (or all) of your capital gains, which quietly makes them some of the friendliest places in the country to sell crypto.

Texas: No State Income Tax

Texas is one of eight states with no personal income tax. This makes it one of the most tax-friendly states for crypto investors.

What this means for you:

- Zero state tax on crypto capital gains (short-term or long-term).

- Zero state tax on crypto income from mining, staking, or airdrops.

- You still owe federal taxes on all taxable crypto events.

Texas also has no state-level capital gains tax of any kind. The state funds itself primarily through property taxes and sales taxes, neither of which apply to crypto holdings.

For crypto investors with large portfolios, Texas offers a straightforward advantage. There is no additional state paperwork, no state-level crypto reporting, and no extra tax bill. Texas is also the largest bitcoin mining hub in the country, which we cover in the mining section below.

If you want help getting your Texas crypto activity CPA-ready, see our Texas crypto tax services.

Florida: No State Income Tax

Florida mirrors Texas in one critical way: it has no state income tax. The Florida Constitution actually prohibits a state income tax, making this protection more durable than in most other states.

What this means for you:

- Zero state tax on crypto capital gains.

- Zero state tax on crypto income.

- Federal taxes still apply in full.

Florida also has no state estate tax. This can matter for crypto investors thinking about gifting or estate planning with digital assets.

The combination of no income tax and no estate tax makes Florida a popular destination for high-net-worth crypto investors looking to minimize their overall tax exposure.

If you want help getting your Florida crypto activity CPA-ready, see our Florida crypto tax services.

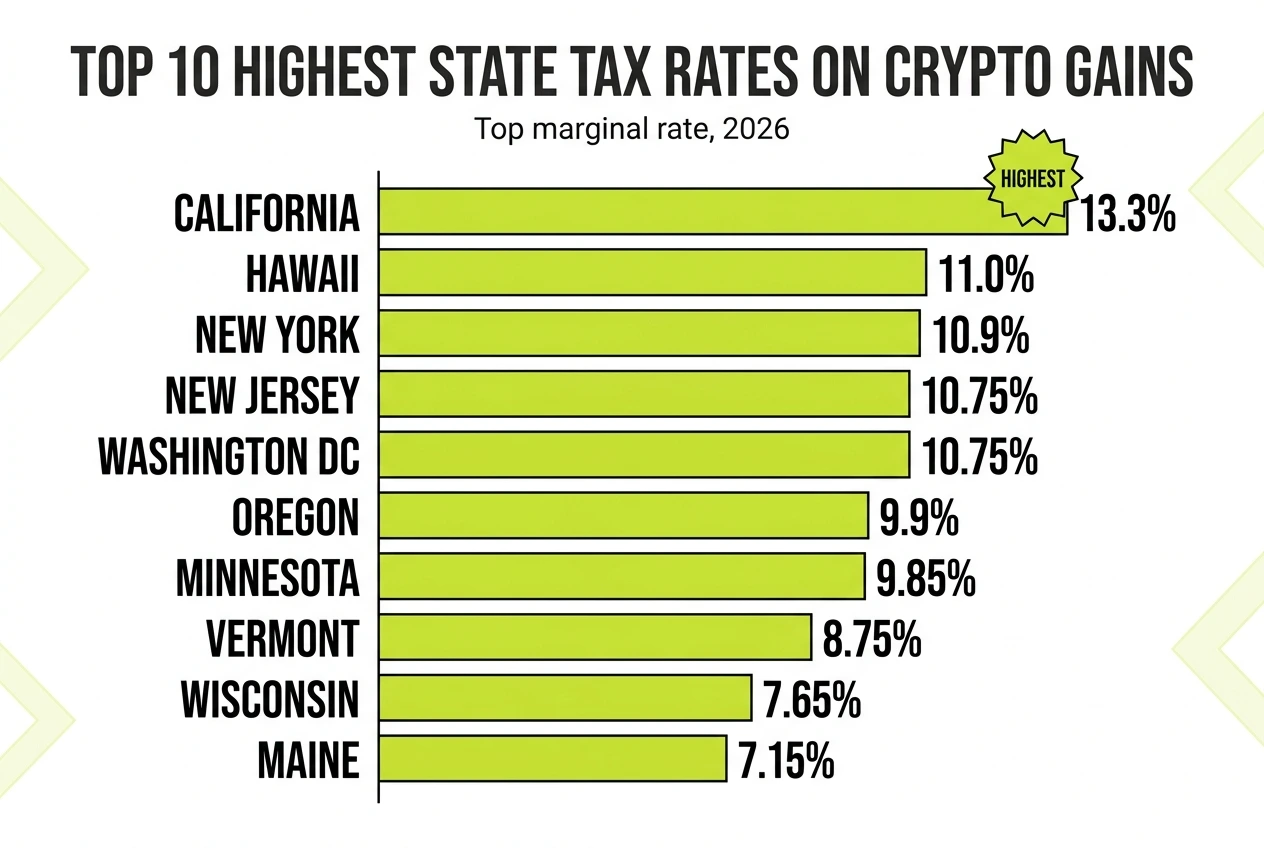

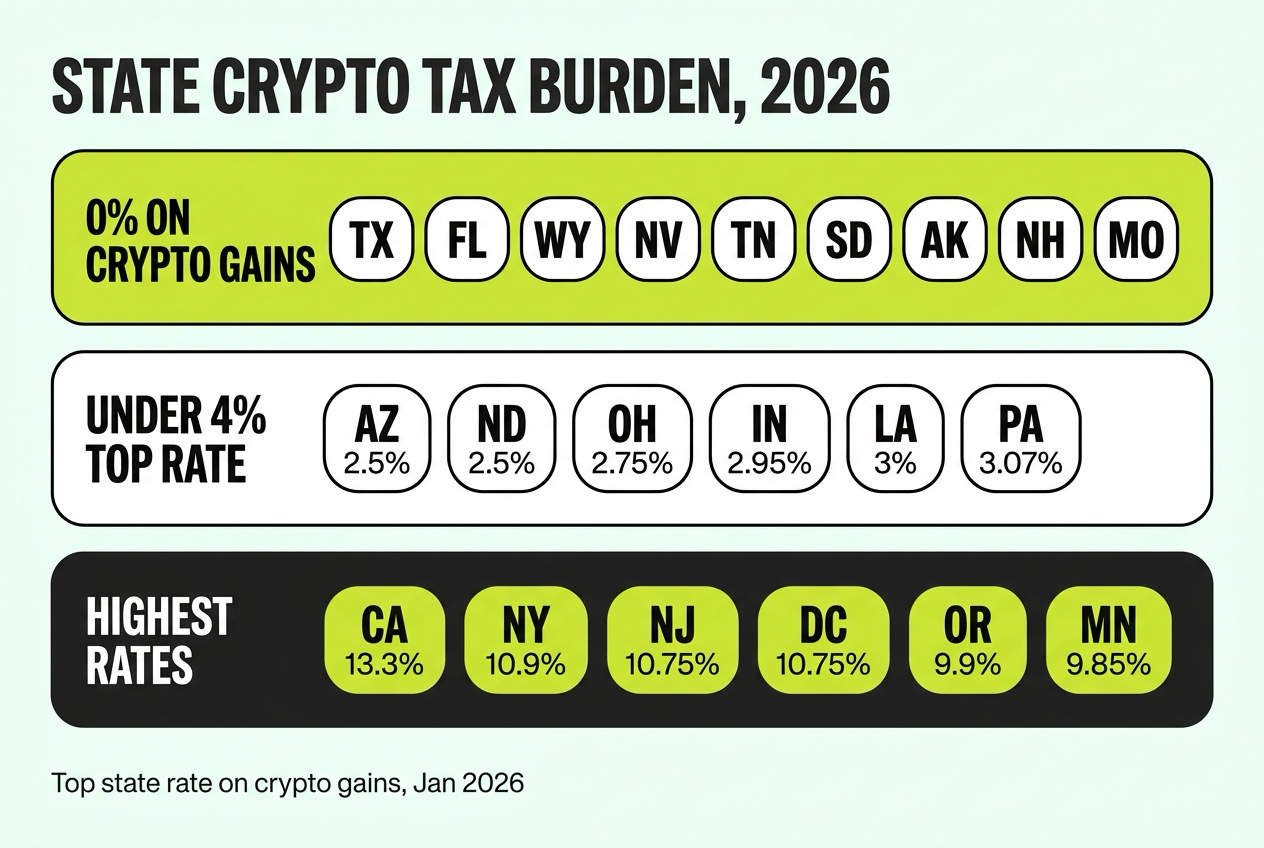

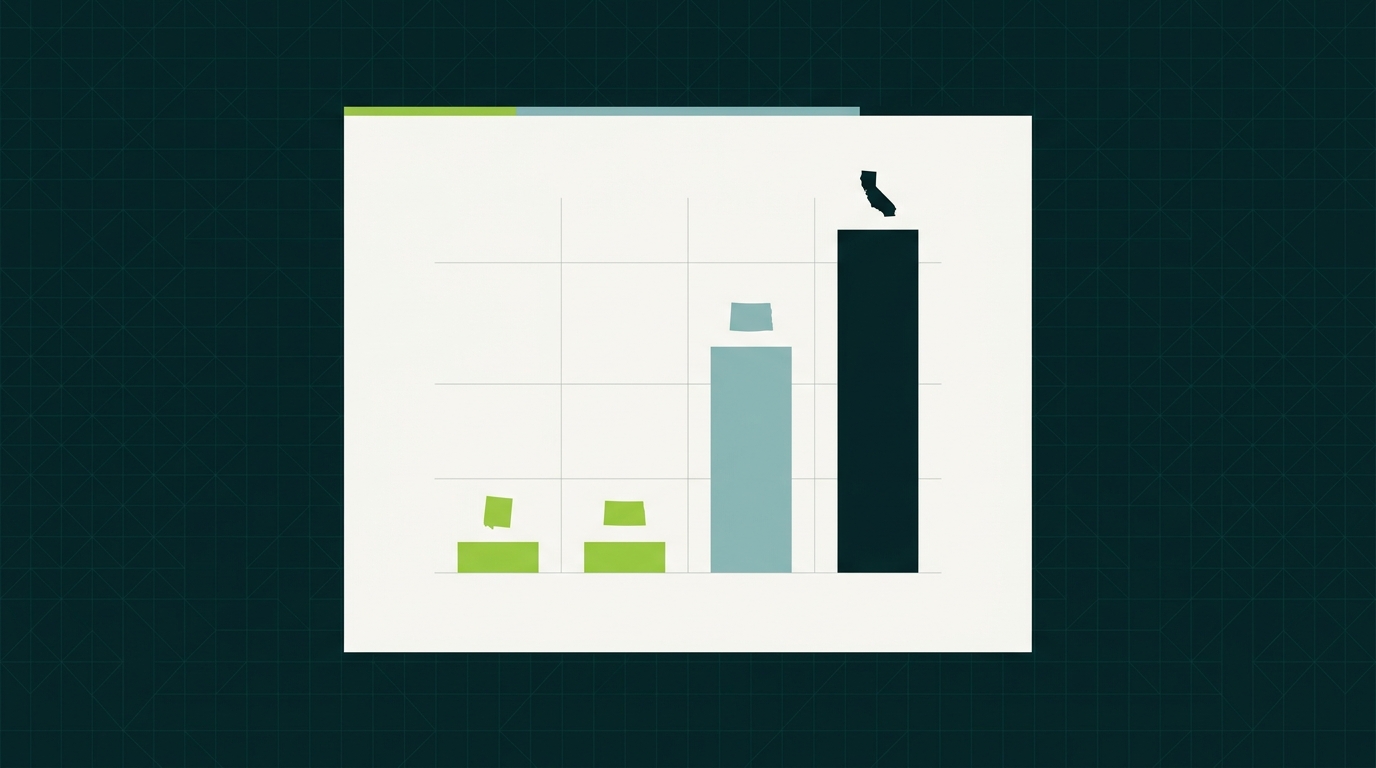

California: Up to 13.3% on Crypto Gains

California sits at the opposite end of the spectrum. The state conforms closely to federal tax treatment of cryptocurrency, meaning crypto gains are taxed as income. The problem for investors is that California has the highest marginal income tax rate in the country.

California’s tax brackets for crypto gains (2026):

- 1% on the first $11,079 of taxable income (single filer)

- Rates increase through nine brackets

- 12.3% on income over $742,953

- An additional 1% Mental Health Services Tax on income over $1 million (bringing the effective top rate to 13.3%)

Key details:

- California does not offer a preferential long-term capital gains rate. All crypto gains are taxed as ordinary income at the state level.

- The Franchise Tax Board (FTB) has been increasingly active in crypto enforcement.

- California follows federal rules for determining cost basis and holding periods.

- The state’s 1.1% payroll tax on wages does not apply to capital gains, so 13.3% remains the ceiling for crypto disposals.

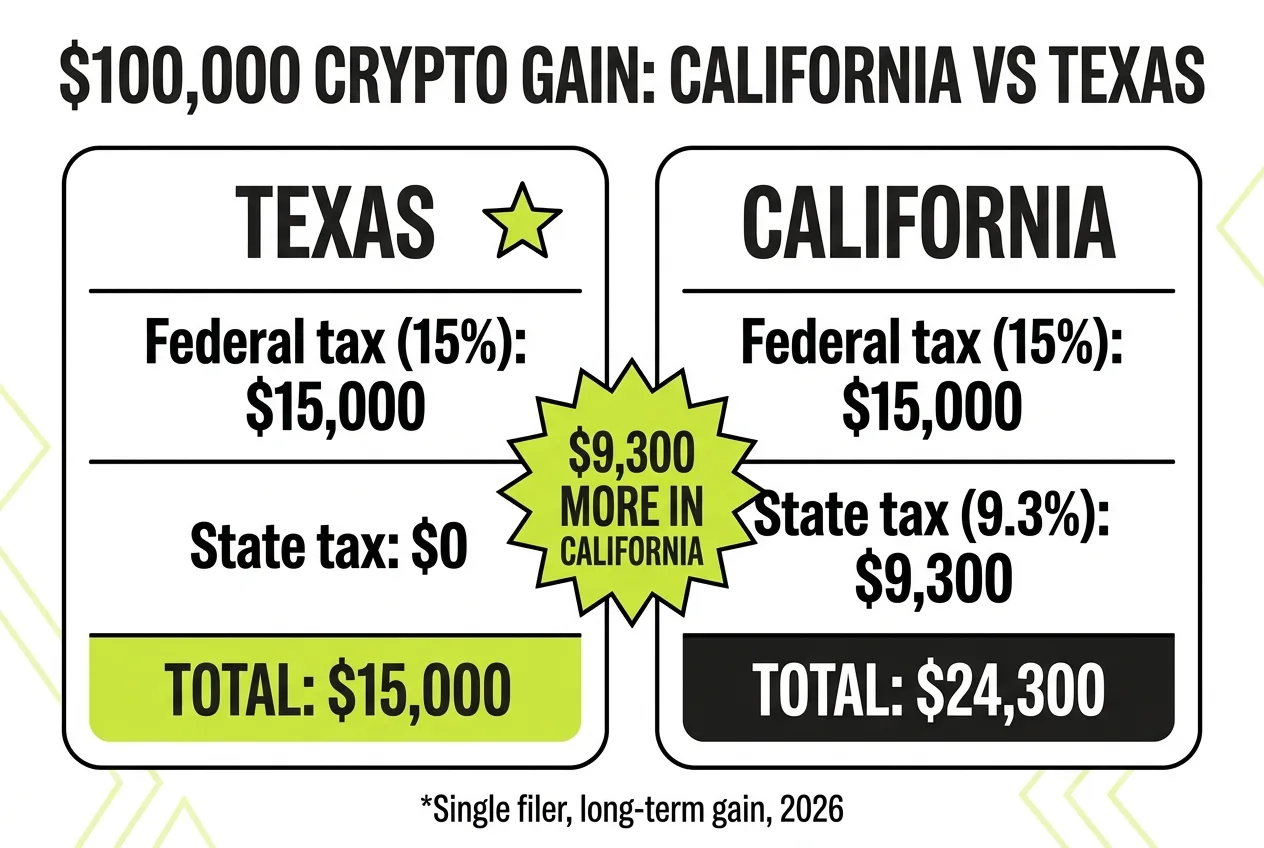

Real Dollar Example: $100,000 Crypto Gain in California vs. Texas

Single filer with $100,000 in W-2 income realizes a $100,000 long-term crypto gain. At this income level, the gain stays in the federal 15% long-term capital gains bracket and falls inside California’s 9.3% marginal state income tax bracket.

No State Income Tax

Federal tax at the 15% LTCG rate: $15,000. State tax: $0. Texas has no personal income tax.

9.3% State Tax in This Example

Federal tax at 15%: $15,000. California state tax on the crypto gain: ~$9,300. California does not offer a preferential long-term rate at the state level.

Over several years of active trading, the cumulative difference can be substantial.

If you want help getting your California crypto activity CPA-ready, see our California crypto tax services.

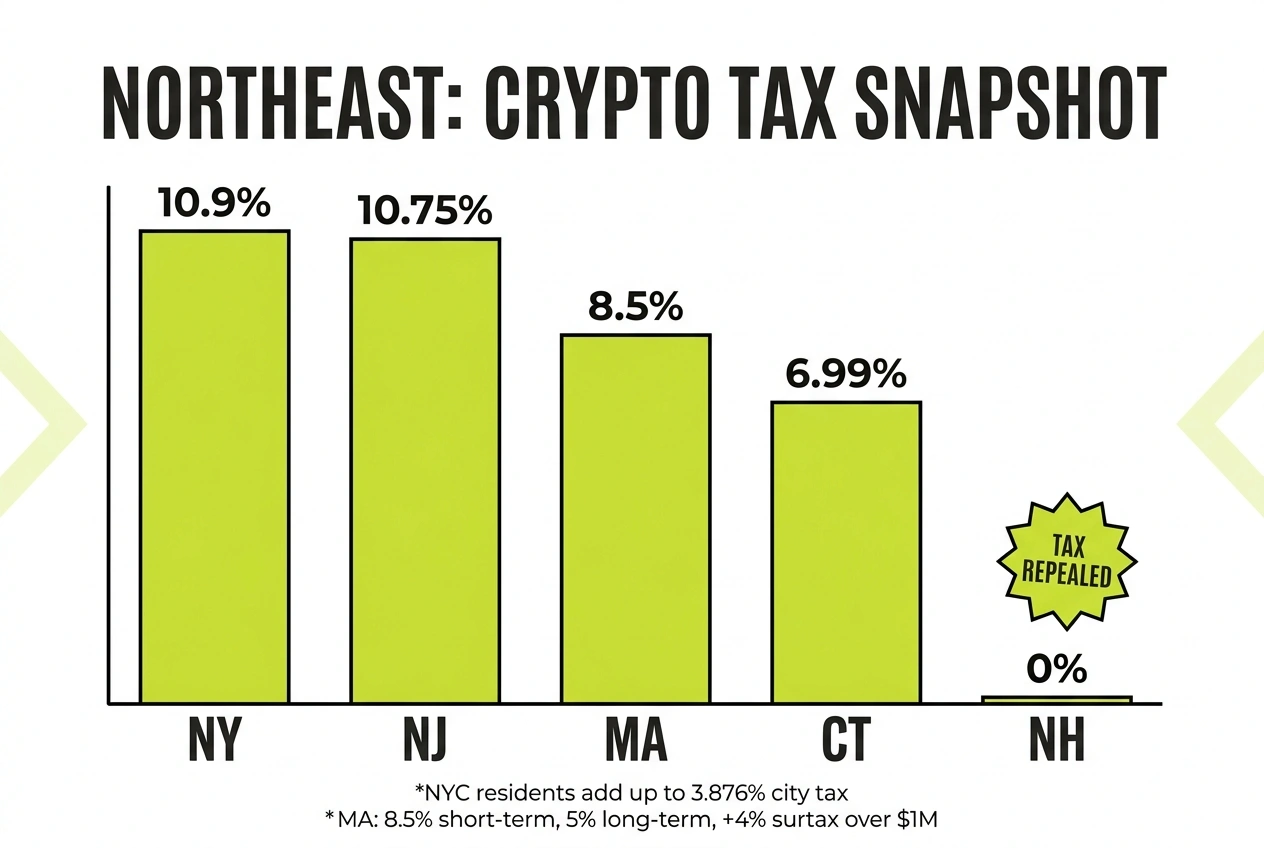

New York: Up to 10.9% Plus BitLicense Rules

New York presents a double challenge for crypto participants. Individual investors face state income tax rates up to 10.9%, and crypto businesses must comply with the state’s BitLicense framework.

State income tax on crypto:

- New York taxes crypto gains as ordinary income.

- State rates range from 3.9% to 10.9% in 2026.

- New York City residents face an additional city income tax of 3.078% to 3.876%, pushing the combined state and city rate above 14% for top earners.

The BitLicense: New York’s Department of Financial Services (NYDFS) requires any business engaged in virtual currency activity to obtain a BitLicense. This applies to exchanges, custodians, and certain other crypto service providers operating in the state. Individual investors do not need a BitLicense, but the regulation has caused some crypto platforms to restrict services for New York residents.

If you want help getting your New York crypto activity CPA-ready, see our New York crypto tax services.

Other Notable States

A few states deserve a callout before the full list.

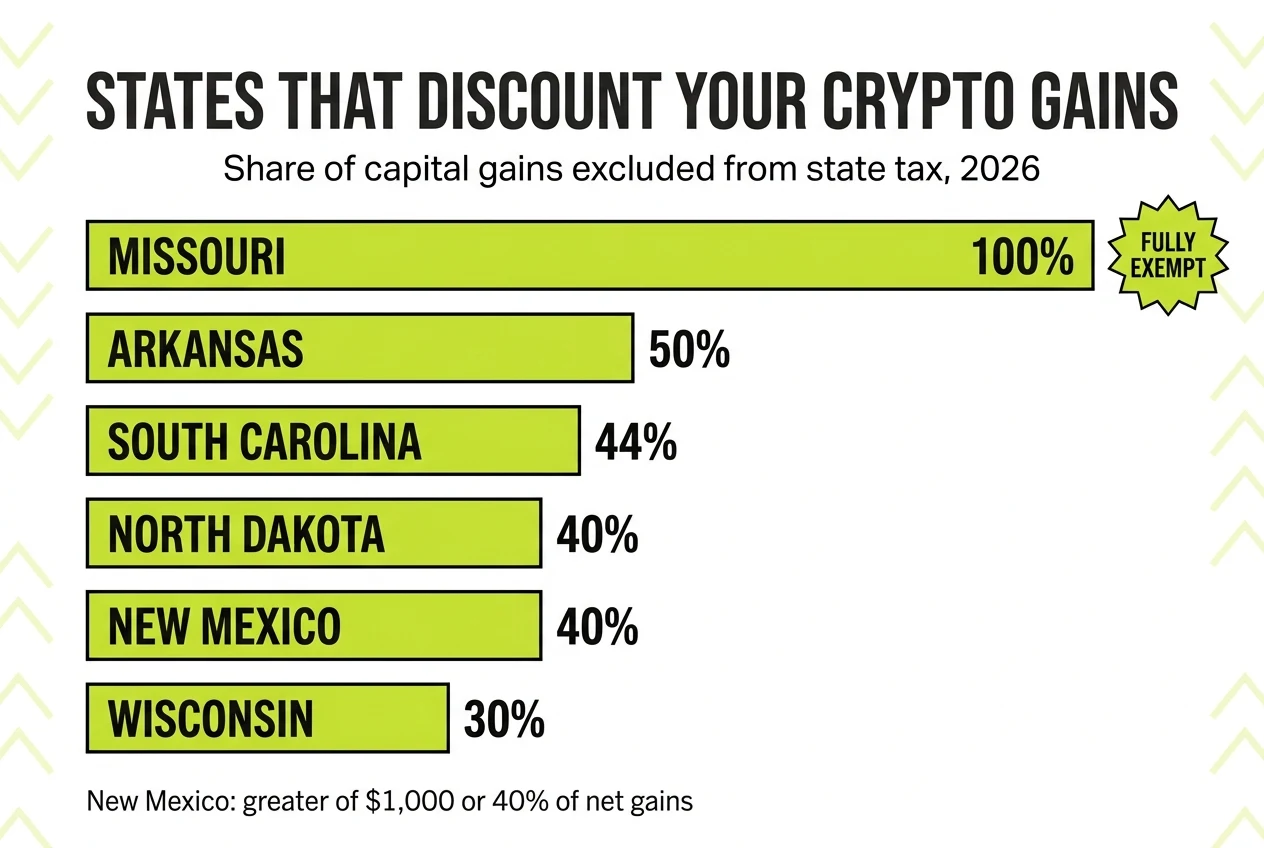

Missouri became the first state to exempt capital gains from its individual income tax. HB 594, signed in July 2025, lets individuals deduct 100% of capital gains starting with tax year 2025. Sell crypto as a Missouri resident and the state takes nothing, though mining and staking income is still taxed as ordinary income.

Washington has no income tax but does impose a capital gains excise tax: 7% on long-term gains above a standard deduction of $278,000 (2025 figure, adjusted annually), plus a 2.9% surcharge on gains above $1 million. Oddly, short-term gains are not covered at all.

Wyoming pairs zero income tax with the most developed crypto legal framework in the country, including DAO LLCs and special-purpose crypto banks.

Illinois investors: we published a dedicated breakdown of Illinois crypto taxes, covering the flat 4.95% rate and what it means for your gains.

We cover every state: browse all 50 on our crypto tax services by state hub.

Crypto Taxes in All 50 States (2026)

Here is how every state (plus Washington, DC) taxes crypto in 2026. Unless noted, states tax crypto gains as ordinary income with no long-term discount, and crypto income from mining, staking, and airdrops follows the same ordinary rates. Top rates come from the Tax Foundation’s 2026 state individual income tax data (as of January 1, 2026).

Alabama

Alabama taxes crypto gains as ordinary income with a top rate of 5%, which kicks in at just $3,000 of taxable income. The state lets you deduct federal income taxes paid, which softens the real burden. Some cities levy occupational taxes on wages, but those do not touch capital gains. If you want your Alabama crypto activity reconciled before filing, see our Alabama crypto tax services.

Alaska

No state income tax and no statewide sales tax. Crypto gains, mining income, and staking rewards all escape state tax entirely. The tradeoff for miners is electricity, which costs well above the national average in most of the state. We offer crypto tax help for Alaska investors.

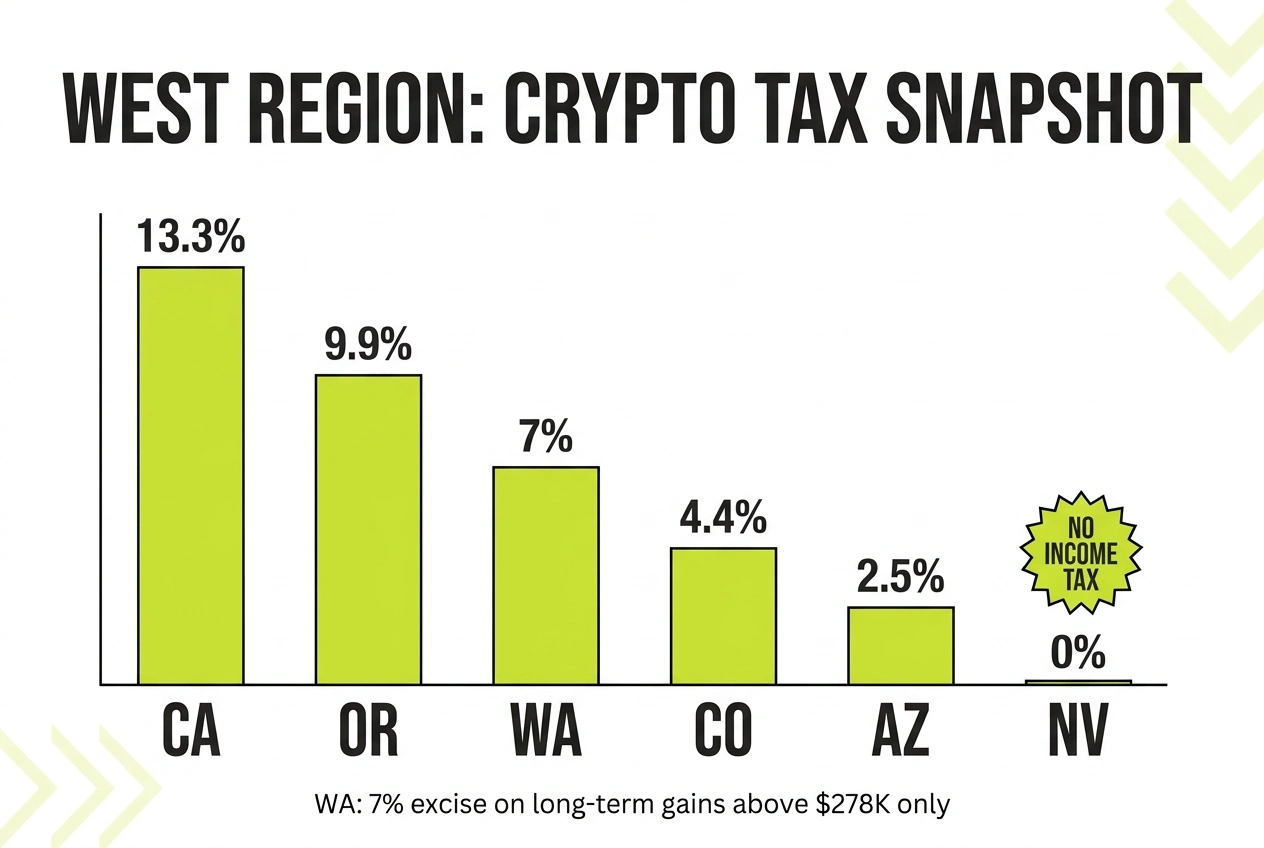

Arizona

Arizona has a flat 2.5% income tax, the lowest flat rate in the country. Crypto gains and crypto income are both taxed at that single rate. For a state that actually taxes income, it is about as painless as it gets. Our Arizona crypto tax services page explains how we get messy records filing-ready.

Arkansas

The top rate is 3.9%, but Arkansas excludes 50% of net capital gains from taxable income, so the effective top rate on crypto gains is roughly 1.95%. Any net capital gains above $10 million in a single year are fully exempt. The state also passed the Arkansas Data Centers Act in 2023, which protects crypto miners from discriminatory utility rates. For done-for-you reconciliation, see our crypto tax services in Arkansas.

California

The highest state tax on crypto in the country: gains are taxed as ordinary income at up to 13.3%, with no long-term discount. See the full California breakdown above for brackets and a worked example. Our California crypto tax page covers how we help investors there.

Colorado

Colorado has a flat 4.4% income tax that applies to crypto gains and income alike. The state has accepted crypto for state tax payments since 2022, a first in the country. Need help with your records? Start with our Colorado crypto tax services.

Connecticut

Connecticut’s graduated rates top out at 6.99% on income over $1 million (joint filers). Crypto gains are taxed as ordinary income with no capital gains preference. If you want your Connecticut crypto activity reconciled before filing, see our Connecticut crypto tax services.

Delaware

Delaware’s top rate is 6.6% on income over $60,000. There is no state sales tax, and the state is popular for business formation, but individual crypto investors get no special break. We offer crypto tax help for Delaware investors.

District of Columbia

DC taxes crypto gains as ordinary income at rates from 4% up to 10.75% on income over $1 million. That top rate matches New Jersey and sits just below New York’s. Our Washington, DC crypto tax services page explains how we get messy records filing-ready.

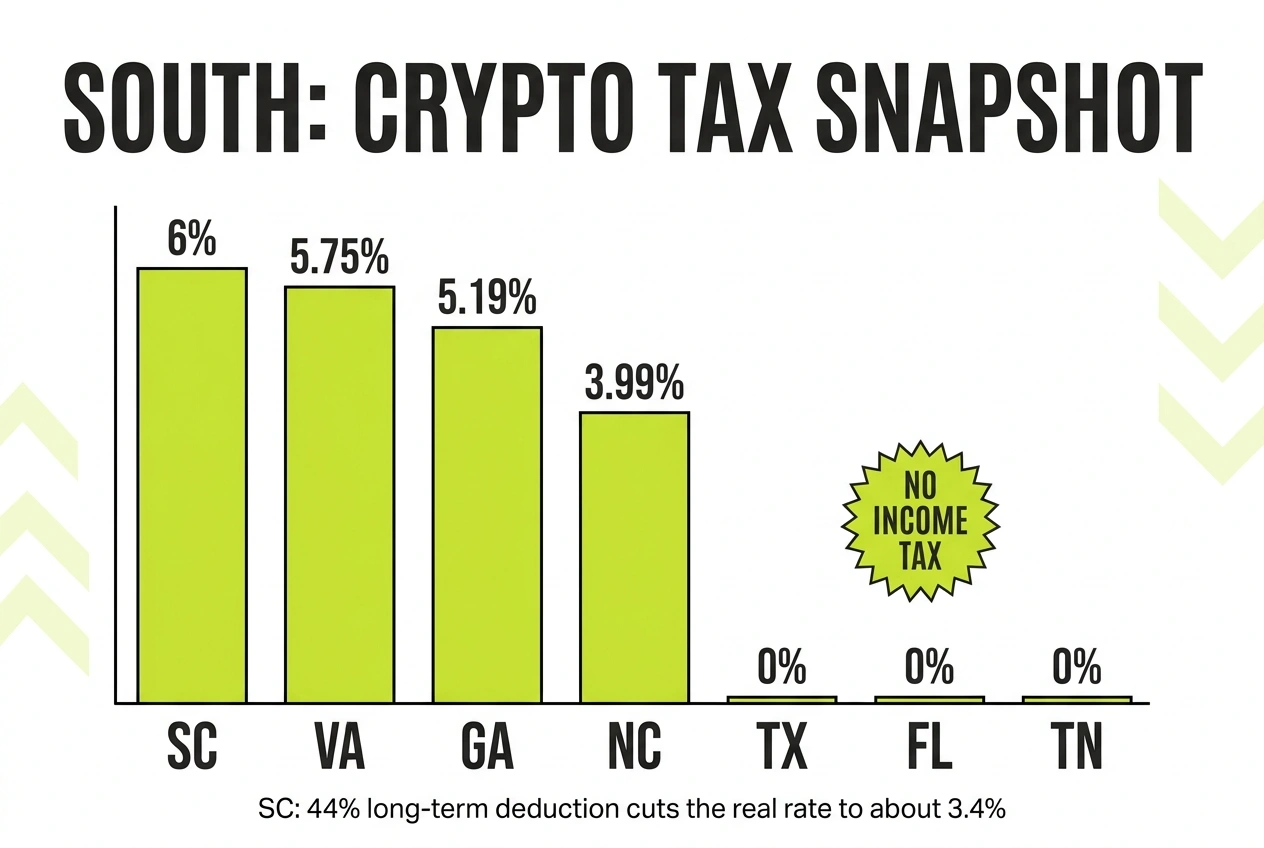

Florida

No state income tax, and the state constitution prohibits one. See the full Florida section above. For done-for-you reconciliation, see our crypto tax services in Florida.

Georgia

Georgia has a flat 5.19% income tax in 2026. Further rate cuts are scheduled if state revenue targets are met, with a long-run target of 4.99%. Our Georgia crypto tax page covers how we help investors there.

Hawaii

Hawaii’s ordinary rates run up to 11% across 12 brackets, but the state caps long-term capital gains at an alternative 7.25% rate. Short-term gains and crypto income still face the ordinary schedule. Hawaii used to be the hardest state for crypto exchanges to operate in, but it dropped its special licensing requirement for crypto companies in 2024. Need help with your records? Start with our Hawaii crypto tax services.

Idaho

Idaho taxes crypto at a flat 5.3% (after a small zero bracket). No capital gains preference for assets like crypto. If you want your Idaho crypto activity reconciled before filing, see our Idaho crypto tax services.

Illinois

Illinois has a flat 4.95% income tax on crypto gains and income. We offer crypto tax help for Illinois investors.

Indiana

Indiana’s flat rate is 2.95% in 2026 and drops to 2.9% in 2027. Every county adds its own local income tax on top, so your real rate depends on where in the state you live. Our Indiana crypto tax services page explains how we get messy records filing-ready.

Iowa

Iowa moved to a flat 3.8% income tax, a big drop from its 8.53% top rate just a few years ago. Crypto gains are taxed at that flat rate. For done-for-you reconciliation, see our crypto tax services in Iowa.

Kansas

Kansas uses two brackets with a top rate of 5.58% on income over $23,000 (single). Crypto gains are ordinary income. Our Kansas crypto tax page covers how we help investors there.

Kentucky

Kentucky’s flat rate fell to 3.5% in 2026, down from 4%. The state also exempts electricity used in commercial crypto mining from sales tax, one of the few states with a mining-specific incentive on the books. Need help with your records? Start with our Kentucky crypto tax services.

Louisiana

Louisiana moved to a flat 3% income tax in 2025, one of the lowest rates among states that tax income. Crypto gains and income are both taxed at 3%. If you want your Louisiana crypto activity reconciled before filing, see our Louisiana crypto tax services.

Maine

Maine’s graduated rates top out at 7.15% on income over $64,849 (single). No capital gains preference. We offer crypto tax help for Maine investors.

Maryland

Maryland’s top bracket is 6.5% on income over $1 million, but the bigger story for crypto investors is the new 2% surcharge on capital gains for taxpayers with federal AGI above $350,000, effective tax year 2025. Counties add their own income taxes on top (about 2.3% on average). A large crypto gain for a high earner in Maryland can face a combined state and local bite above 10%. Our Maryland crypto tax services page explains how we get messy records filing-ready.

Massachusetts

Massachusetts taxes long-term gains at a flat 5% but short-term gains at 8.5%. A 4% surtax applies to total income above roughly $1.08 million. Active crypto traders flipping positions inside a year face up to 12.5% with the surtax, among the highest short-term rates in the country. For done-for-you reconciliation, see our crypto tax services in Massachusetts.

Michigan

Michigan has a flat 4.25% income tax. Detroit and some other cities add a local income tax on top. Our Michigan crypto tax page covers how we help investors there.

Minnesota

Minnesota’s top rate is 9.85%, and a 1% net investment income tax applies to investment income (including crypto gains) above $1 million. That puts the effective ceiling at 10.85%, fourth highest in the country for large crypto gains. Need help with your records? Start with our Minnesota crypto tax services.

Mississippi

Mississippi reached a flat 4% income tax in 2026, with further phase-downs planned in future years. Crypto gains are taxed at the flat rate. If you want your Mississippi crypto activity reconciled before filing, see our Mississippi crypto tax services.

Missouri

Missouri is the sleeper pick of 2026. HB 594 made capital gains 100% deductible for individuals starting with tax year 2025, the first state to fully exempt them. Sell crypto as a Missouri resident and the state tax is zero. Mining, staking, and airdrop income is still ordinary income at rates up to 4.7%. We offer crypto tax help for Missouri investors.

Montana

Montana taxes ordinary income at up to 5.65% in 2026, but long-term capital gains get their own reduced rates of 3% and 4.1%. There is no state sales tax, and the 2023 right-to-mine law (SB 178) bans discriminatory utility rates for miners. More in the mining section below. Our Montana crypto tax services page explains how we get messy records filing-ready.

Nebraska

Nebraska’s top rate is 4.55% in 2026 and is scheduled to fall to 3.99% by 2027. Crypto gains are ordinary income. For done-for-you reconciliation, see our crypto tax services in Nebraska.

Nevada

No state income tax. Crypto gains, mining income, and staking rewards face zero state tax. Nevada funds itself through gaming and sales taxes instead. Our Nevada crypto tax page covers how we help investors there.

New Hampshire

No tax on crypto, full stop. New Hampshire repealed its interest and dividends tax effective 2025, and crypto capital gains never fell under that tax anyway. It now joins the true zero-income-tax states. Need help with your records? Start with our New Hampshire crypto tax services.

New Jersey

New Jersey taxes crypto gains as ordinary income at up to 10.75% on income over $1 million, with no long-term discount. It is one of the three most expensive states in the country for a large crypto exit. If you want your New Jersey crypto activity reconciled before filing, see our New Jersey crypto tax services.

New Mexico

New Mexico’s top rate is 5.9%, but taxpayers deduct the greater of $1,000 or 40% of net capital gains, which brings the effective top rate on crypto gains down to about 3.5%. The state also had the second-cheapest electricity in the country in early 2026, which is why it shows up on mining shortlists. We offer crypto tax help for New Mexico investors.

New York

Rates run from 3.9% to 10.9%, New York City adds up to 3.876%, and crypto businesses need a BitLicense. See the full New York section above. Our New York crypto tax services page explains how we get messy records filing-ready.

North Carolina

North Carolina has a flat 3.99% rate in 2026, with further scheduled cuts in the coming years. Crypto gains are taxed at the flat rate. For done-for-you reconciliation, see our crypto tax services in North Carolina.

North Dakota

North Dakota’s top rate is just 2.5%, and the state excludes 40% of long-term capital gains, putting the effective long-term rate near 1.5%. Pair that with the cheapest electricity in the country and you get one of the strongest all-around crypto states. Details in the mining section. Our North Dakota crypto tax page covers how we help investors there.

Ohio

Ohio taxes income above $26,050 at a flat 2.75% as of 2026. Many municipalities add local income taxes of 1% to 2.5%, so location within the state matters. Need help with your records? Start with our Ohio crypto tax services.

Oklahoma

Oklahoma’s graduated rates top out at 4.5%. Crypto gains are ordinary income with no preference. If you want your Oklahoma crypto activity reconciled before filing, see our Oklahoma crypto tax services.

Oregon

Oregon’s top rate is 9.9%, and local taxes in the Portland area can push the combined top rate above 13%. There is no sales tax, but for crypto sellers Oregon is one of the most expensive states on the West Coast after California. We offer crypto tax help for Oregon investors.

Pennsylvania

Pennsylvania has a flat 3.07% income tax, one of the lowest flat rates among taxing states. Crypto gains are taxed as one of the state’s eight income classes, and losses in one class cannot offset income in another, a quirk worth knowing for active traders. Our Pennsylvania crypto tax services page explains how we get messy records filing-ready.

Rhode Island

Rhode Island’s rates top out at 5.99% on income over $186,450. Crypto gains are ordinary income. For done-for-you reconciliation, see our crypto tax services in Rhode Island.

South Carolina

South Carolina’s top rate is 6%, but the state allows a 44% deduction on net long-term capital gains, bringing the effective top rate on long-held crypto to about 3.4%. Short-term gains pay the full rate. Our South Carolina crypto tax page covers how we help investors there.

South Dakota

No state income tax. Crypto gains and income face zero state tax. Need help with your records? Start with our South Dakota crypto tax services.

Tennessee

No state income tax. Tennessee’s old Hall tax on investment income was fully repealed in 2021, so nothing at the state level touches crypto. If you want your Tennessee crypto activity reconciled before filing, see our Tennessee crypto tax services.

Texas

No state income tax, and the biggest bitcoin mining industry in the country. See the full Texas section above. We offer crypto tax help for Texas investors.

Utah

Utah has a flat 4.5% income tax in 2026. Crypto gains and income are taxed at the flat rate. Our Utah crypto tax services page explains how we get messy records filing-ready.

Vermont

Vermont’s rates top out at 8.75%. The state offers a capital gains exclusion, but for assets like crypto it is generally capped at a flat $5,000, so most of a large gain is taxed at ordinary rates. For done-for-you reconciliation, see our crypto tax services in Vermont.

Virginia

Virginia’s top rate of 5.75% kicks in at just $17,000 of taxable income, so nearly all crypto gains are taxed at the top rate. No capital gains preference. Our Virginia crypto tax page covers how we help investors there.

Washington

Washington has no tax on wages or short-term gains, but its capital gains excise tax hits long-term gains above a standard deduction of $278,000 (2025 figure, indexed annually) at 7%, with a 2.9% surcharge on gains above $1 million (9.9% total). Crypto counts as a covered intangible asset. The strange result: flipping crypto inside a year is state tax free in Washington, while long-term holders with big gains pay. Need help with your records? Start with our Washington crypto tax services.

West Virginia

West Virginia’s top rate is 4.82% in 2026, down from 6.5% a few years ago as the state phases rates lower. Crypto gains are ordinary income. If you want your West Virginia crypto activity reconciled before filing, see our West Virginia crypto tax services.

Wisconsin

Wisconsin’s top rate is 7.65%, but the state excludes 30% of net long-term capital gains, so the effective top rate on long-held crypto is about 5.4%. Short-term gains pay the full rate. We offer crypto tax help for Wisconsin investors.

Wyoming

No state income tax, plus the deepest crypto legal framework in the country: DAO LLCs, special-purpose depository institutions for digital assets, a state stablecoin, and utilities that can negotiate power deals directly with miners. For crypto businesses, Wyoming is arguably the friendliest jurisdiction in the U.S. Our Wyoming crypto tax services page explains how we get messy records filing-ready.

State-by-State Comparison Table

The table below shows the top state income tax rate that applies to crypto gains in all 50 states plus DC, as of January 1, 2026 (Tax Foundation data; local taxes excluded except where noted).

| State | State income tax on crypto gains (top rate) | Notes |

|---|---|---|

| Alabama | 5% | Federal income tax deductible, which lowers the effective rate |

| Alaska | None | No state income or sales tax |

| Arizona | 2.5% flat | Lowest flat income tax in the country |

| Arkansas | 3.9% (~1.95% effective on gains) | 50% of net capital gains excluded; gains over $10M exempt |

| California | 13.3% | No long-term preference; includes 1% surcharge over $1M |

| Colorado | 4.4% flat | Accepts crypto for state tax payments |

| Connecticut | 6.99% | No capital gains preference |

| Delaware | 6.6% | No state sales tax |

| District of Columbia | 10.75% | Top rate starts at $1M |

| Florida | None | State constitution prohibits an income tax |

| Georgia | 5.19% flat | Further cuts scheduled if revenue targets are met |

| Hawaii | 7.25% on long-term gains | Ordinary rates up to 11% for short-term gains and income |

| Idaho | 5.3% flat | |

| Illinois | 4.95% flat | See our dedicated Illinois guide |

| Indiana | 2.95% flat | Counties add local income tax |

| Iowa | 3.8% flat | |

| Kansas | 5.58% | |

| Kentucky | 3.5% flat | Sales tax exemption for commercial mining electricity |

| Louisiana | 3% flat | |

| Maine | 7.15% | |

| Maryland | 6.5% + 2% gains surcharge | Surcharge applies when federal AGI tops $350K; counties add ~2.3% |

| Massachusetts | 5% LT / 8.5% ST | 4% surtax on income over ~$1.08M |

| Michigan | 4.25% flat | Some cities add local income tax |

| Minnesota | 9.85% (+1% NIIT) | Extra 1% on investment income over $1M |

| Mississippi | 4% flat | Further phase-downs planned |

| Missouri | 0% on gains | Capital gains fully exempt from 2025; crypto income taxed up to 4.7% |

| Montana | 4.1% on long-term gains | Ordinary rates up to 5.65%; right-to-mine law |

| Nebraska | 4.55% | Falling to 3.99% by 2027 |

| Nevada | None | |

| New Hampshire | None | Interest and dividends tax repealed in 2025 |

| New Jersey | 10.75% | Top rate starts at $1M; no long-term preference |

| New Mexico | 5.9% (~3.5% effective on gains) | Deduct the greater of $1,000 or 40% of net capital gain |

| New York | 10.9% | NYC adds up to 3.876%; BitLicense for businesses |

| North Carolina | 3.99% flat | More cuts scheduled |

| North Dakota | 2.5% (~1.5% effective on LT gains) | 40% long-term gains exclusion; cheapest power in the U.S. |

| Ohio | 2.75% flat | Applies above $26,050; cities add local tax |

| Oklahoma | 4.5% | |

| Oregon | 9.9% | Portland-area local taxes can push the total above 13% |

| Pennsylvania | 3.07% flat | Losses in one income class cannot offset another |

| Rhode Island | 5.99% | |

| South Carolina | 6% (~3.4% effective on LT gains) | 44% deduction for long-term gains |

| South Dakota | None | |

| Tennessee | None | Hall tax fully repealed in 2021 |

| Texas | None | Largest U.S. bitcoin mining hub |

| Utah | 4.5% flat | |

| Vermont | 8.75% | Gains exclusion capped at $5,000 for most assets |

| Virginia | 5.75% | Top rate starts at just $17,000 |

| Washington | 7% to 9.9% on large LT gains | Excise on long-term gains above ~$278K; short-term gains not covered |

| West Virginia | 4.82% | Multi-year phase-down in progress |

| Wisconsin | 7.65% (~5.4% effective on LT gains) | 30% long-term gains exclusion |

| Wyoming | None | DAO LLCs, crypto banks, negotiated miner power rates |

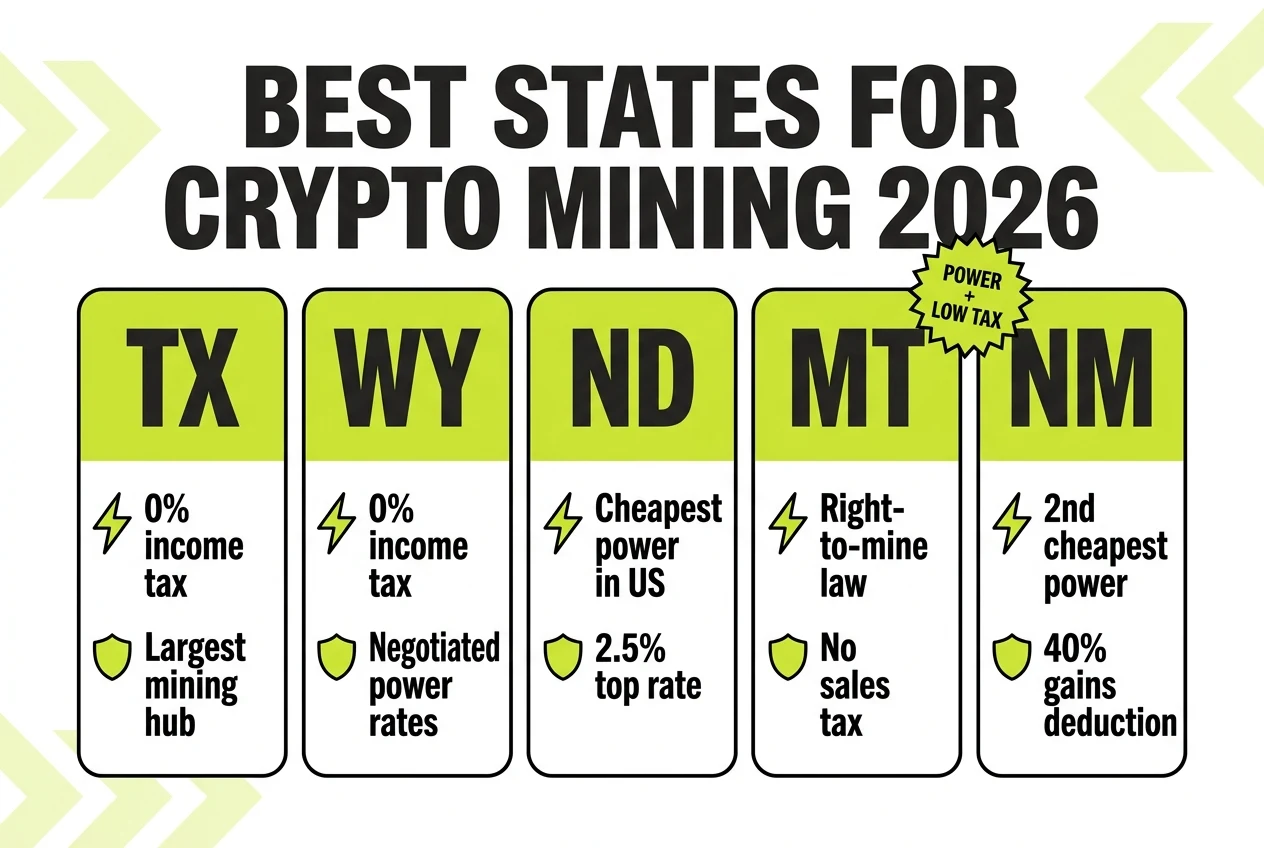

Best States for Crypto Mining in 2026

The best states for crypto mining in 2026 are Texas, Wyoming, North Dakota, Montana, and New Mexico. Three things drive that ranking: electricity cost (the largest expense in any mining operation), how the state taxes mining income, and whether the law actually protects your right to run machines.

One federal reminder before the state comparison: the IRS taxes mining rewards as ordinary income at fair market value the day you receive them, no matter where you live. Our guides on bitcoin mining taxes and crypto income from staking, mining, and airdrops cover the federal side in detail. The state layer is what changes below.

Texas remains the largest bitcoin mining hub in the country. The deregulated ERCOT grid runs demand response programs that pay large flexible loads, including miners, to power down during grid stress, which turns curtailment into a revenue stream. Add zero state income tax on mining income and you can see why so much hashrate lives here. The tradeoff: wholesale power prices in Texas are forecast to rise in 2026 as data center demand grows.

Wyoming lets utilities negotiate power rates directly with blockchain companies without public utility commission approval, and offers interruptible service tariffs that trade cheaper power for curtailment during peak demand. No state income tax, and the legislature keeps an active blockchain committee that reviews mining-related law every year.

North Dakota had the cheapest electricity in the country as of January 2026, with industrial rates around 8 cents per kilowatt-hour. The cold climate cuts cooling costs, the top income tax rate is 2.5%, and 40% of long-term gains are excluded if you hold the coins you mine. State officials have flagged rising transmission demand from data centers, so cheap power is not guaranteed forever.

Montana passed SB 178 in 2023, one of the strongest right-to-mine laws in the country. It bans discriminatory utility rates for digital asset miners, limits local governments from zoning mining out of existence, and classifies digital assets as personal property. There is no state sales tax on hardware, and long-term gains are taxed at a reduced 4.1% top rate.

New Mexico had the second-cheapest electricity in the country in early 2026, behind only North Dakota. The state deducts 40% of net capital gains, so coins you mine and later sell at a long-term gain face an effective state rate around 3.5%. It has less crypto-specific legislation than the others on this list, which cuts both ways: fewer protections, but also fewer rules.

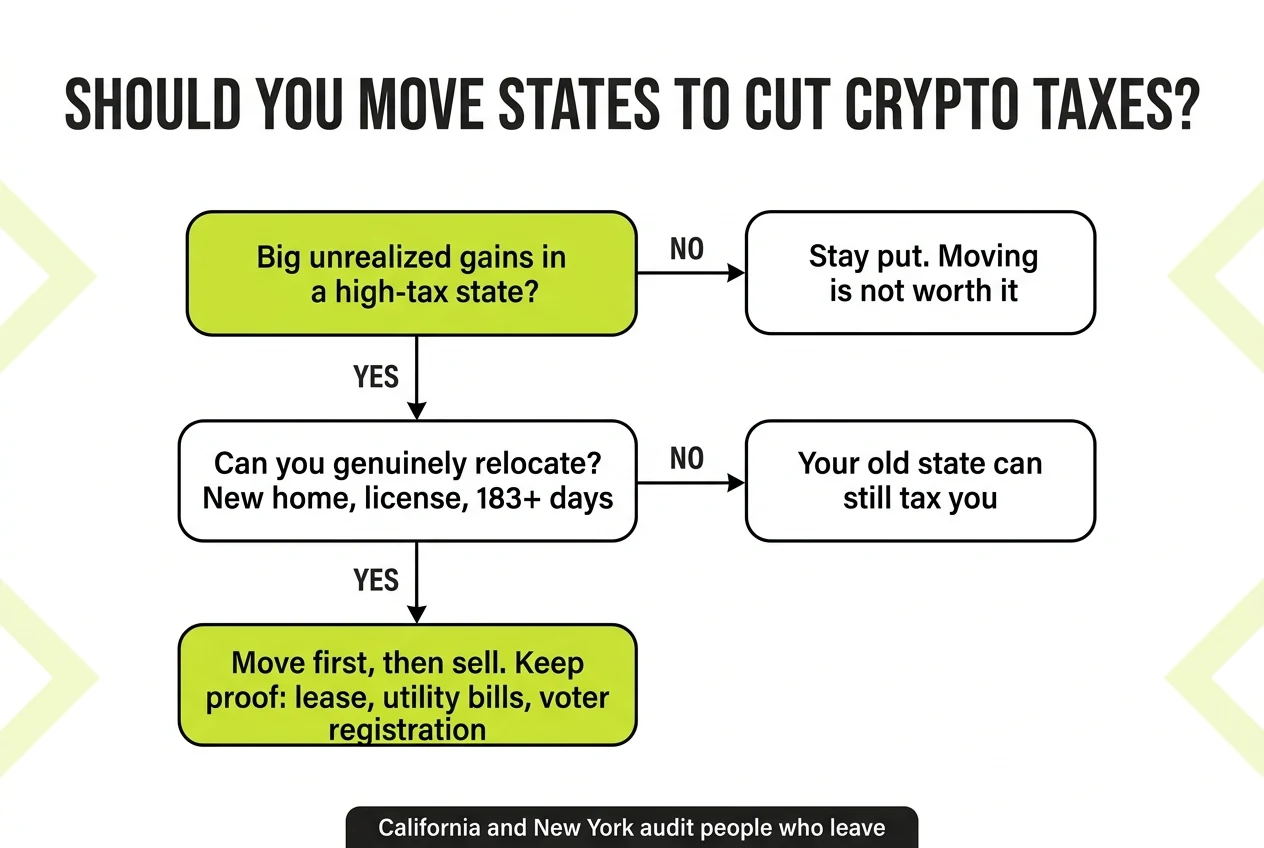

Residency Considerations: Moving to Save on Crypto Taxes

Relocating to a no-income-tax state is a legitimate tax planning strategy. Many crypto investors have moved to Texas, Florida, Wyoming, or Nevada for exactly this reason. However, there are important rules to follow.

Key residency rules to know:

-

California’s “safe harbor” rule. California considers you a resident if you are in the state for more than nine months in a taxable year. Even after you move, the FTB may claim you are still a resident if you maintain significant ties (a home, a spouse, a business) in California.

-

New York’s 183-day rule. New York considers you a statutory resident if you maintain a “permanent place of abode” in the state and spend more than 183 days there. Selling or vacating your New York home is critical when establishing residency elsewhere.

-

The “tax year” matters. If you move mid-year, you may owe state taxes to your former state on crypto gains realized before the move. Plan the timing of large disposals carefully.

-

Federal taxes do not change. Moving states does not reduce your federal tax bill. It only affects the state layer.

The same $500,000 crypto gain costs roughly $46,500 more in California state taxes compared to Texas. For many investors, that difference alone justifies the cost of relocating.

When to Consult a CPA

State crypto tax rules interact with federal rules in ways that can be tricky to manage on your own. Consider working with a tax professional if:

- You are planning a move between states and want to time your crypto disposals correctly.

- You live in a high-tax state and have unrealized gains exceeding $100,000.

- You earn crypto income from multiple sources (mining, staking, DeFi) and need help with state-level reporting.

- You have received a residency audit notice from a former state.

- You operate a crypto business that may trigger BitLicense or state money transmitter requirements.

At CountOnSheep, our team specializes in crypto accounting and tax preparation for investors across all 50 states. We can help you understand your state-level obligations and plan around them.

Bottom Line: What to Do Next

Your state of residence has a real, measurable impact on how much you keep from your crypto investments. Eight states plus Missouri (for gains) take nothing at all. California, New York, New Jersey, DC, Oregon, and Minnesota take 9.85% or more from top earners, and the two biggest actively enforce residency rules against people who leave.

Here is what to do now:

- Know your state’s rules. Find your state in the list above and check whether it taxes crypto gains as ordinary income, offers an exclusion, or skips them entirely.

- Track your transactions. Accurate records are essential for both federal and state reporting. See our 2026 crypto tax guide for tools and methods.

- Plan large disposals carefully. If you are considering a move, time your sales to occur after you have established residency in your new state.

- Talk to a specialist. State and federal crypto taxes together can be complex. Book a consultation with our team to get a clear picture of what you owe and how to plan ahead.

Your crypto tax situation is unique. The right state-level strategy can save you thousands of dollars every year.

Frequently Asked Questions

Does Texas tax crypto gains?

No. Texas has no state income tax, so crypto capital gains and income are not taxed at the state level. You still owe federal taxes.

Does Florida tax crypto gains?

No. Florida has no state income tax. Crypto gains are only subject to federal taxes.

How does California tax crypto?

California conforms to federal tax rules and taxes crypto gains as regular income. State rates range from 1% to 13.3%, making it one of the highest-tax states for crypto investors.

Does New York have special crypto regulations?

Yes. New York requires crypto businesses to obtain a BitLicense. For individual investors, crypto gains are taxed at state income rates of 3.9% to 10.9%.

Which states have no state tax on crypto gains?

Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, and Wyoming have no state income tax, so crypto gains escape state tax entirely. Missouri also exempts capital gains from its income tax starting with the 2025 tax year, though mining and staking income is still taxed there.

What are the best states for crypto mining?

Texas, Wyoming, North Dakota, Montana, and New Mexico rank among the best. They combine cheap electricity, mining-friendly laws, and low or zero state income tax. North Dakota had the cheapest electricity in the country in early 2026, and Montana's SB 178 blocks discriminatory utility rates for miners.

Can I move to a no-income-tax state to avoid crypto taxes?

You can reduce your state tax burden by establishing residency in a no-income-tax state. However, you must genuinely relocate. Your former state may audit you to verify the move.