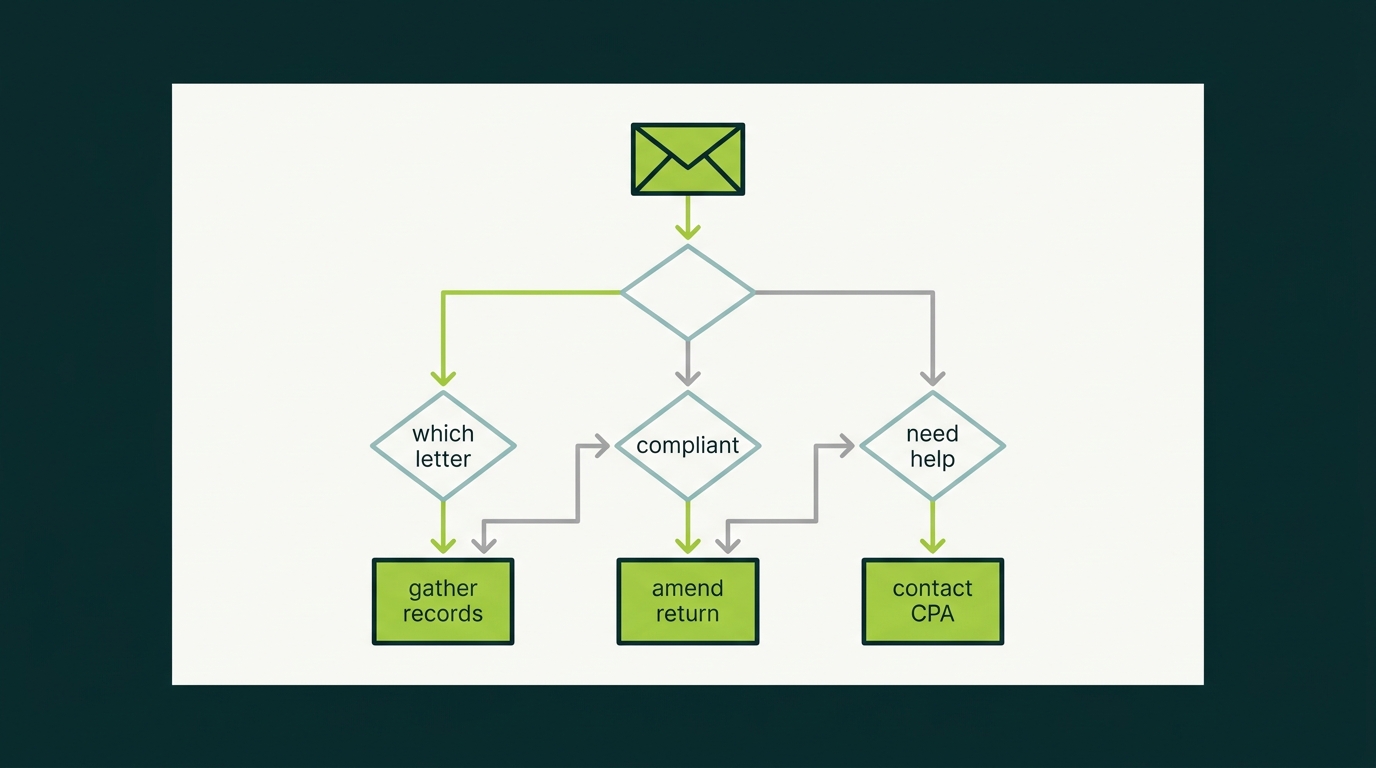

IRS crypto compliance letters are official notices the IRS sends to taxpayers it believes have bought, sold, or held cryptocurrency without properly reporting the activity on their tax returns. These letters come in three varieties: Letter 6173, Letter 6174, and Letter 6174-A. Each carries a different level of severity and requires a different response. If one of these letters has landed in your mailbox, the first thing to know is this: do not panic, but do not ignore it either.

For a complete overview of how crypto is taxed, start with our 2026 Crypto Tax Guide. This article focuses specifically on what to do when the IRS contacts you directly.

The Three IRS Crypto Letters: A Quick Overview

Starting in 2019, the IRS began sending compliance letters to cryptocurrency holders whose exchange records did not match their filed tax returns (or who had no returns on file at all). The agency uses three letter types, each escalating in seriousness.

| Letter | Severity | Response Required? | What It Means |

|---|---|---|---|

| 6174 | Low | No | The IRS knows you hold crypto. This is purely informational. |

| 6174-A | Medium | No (but recommended) | The IRS suspects you may have unreported crypto income. Review your filings. |

| 6173 | High | Yes | The IRS believes you have unreported crypto income and demands a response. |

Think of these letters on a spectrum. Letter 6174 is a gentle nudge. Letter 6174-A is a firm tap on the shoulder. Letter 6173 is the IRS standing in your doorway asking questions.

Letter 6173: The One You Cannot Ignore

Letter 6173 is the most serious of the three. It explicitly states that the IRS has information suggesting you did not properly report your cryptocurrency transactions. It requires you to respond, typically within 30 days, by either:

- Filing or amending your tax return to include the unreported crypto activity.

- Providing a signed statement explaining why you believe your original return was correct.

The letter will include a response form and instructions. If you do not respond, the IRS may initiate an examination (audit) of your tax return. In some cases, the agency may assess taxes, penalties, and interest based on the information it already has, without giving you another opportunity to explain.

How to Respond to Letter 6173

Step 1: Read the letter carefully. Note the response deadline, the tax year(s) in question, and any specific transactions the IRS references.

Step 2: Gather your records. Pull transaction histories from every exchange and wallet you used during the relevant tax years. This includes Coinbase, Kraken, Binance, DeFi protocols, and any peer-to-peer transactions. If you need help understanding what forms are involved, see our guide on Form 8949 and Schedule D.

Step 3: Determine if you need to amend. Compare what you reported on your original return to your actual transaction records. If there are discrepancies, you will likely need to file a Form 1040-X (amended return).

Step 4: Respond before the deadline. Send your response via certified mail or the method specified in the letter. Keep copies of everything.

Step 5: Consider hiring a crypto-specialized CPA. If your situation involves large amounts, DeFi activity, NFTs, or multiple tax years, professional help can prevent costly mistakes. We offer this exact service at CountOnSheep.

Letter 6174: Informational Notice

Letter 6174 is the least alarming of the three. It does not accuse you of anything and does not require a response. Essentially, the IRS is telling you: “We know you have cryptocurrency. Make sure you are reporting it correctly.”

You might receive this letter if you have exchange accounts that reported your information to the IRS via Form 1099 (or now Form 1099-DA), and your filed return appears to match. The IRS is simply putting you on notice.

What to do: No formal action is required. However, use this as a prompt to double-check your past filings. If you have been reporting everything accurately, file the letter away and continue as normal. If you realize you missed something, it is better to correct it now rather than wait.

Letter 6174-A: The Middle Ground

Letter 6174-A sits between the other two in terms of severity. Like Letter 6174, it does not technically require a response. But unlike Letter 6174, it carries an implicit warning: the IRS has reason to believe you may not be fully compliant.

This letter often includes educational language about how cryptocurrency is taxed, along with a reminder to review your past returns. The subtext is clear. The IRS is giving you a chance to self-correct before it escalates.

What to do: Take it seriously. Review your prior year returns. If you find unreported transactions, consider filing amended returns proactively. This demonstrates good faith and can significantly reduce penalties if the IRS follows up later.

Why the IRS Is Sending More Crypto Letters in 2026

The volume of IRS crypto compliance letters has surged in 2026, and the reason is straightforward: Form 1099-DA.

Starting with the 2025 tax year, centralized exchanges and brokers are required to report detailed transaction data to the IRS via Form 1099-DA. This includes gross proceeds from sales, cost basis information (where available), and taxpayer identification. The IRS now has a direct data pipeline from major exchanges, making it trivially easy to identify taxpayers who bought and sold crypto but did not report the gains.

Combined with the IRS’s $80 billion in additional funding from the Inflation Reduction Act, the agency has the data and the resources to pursue crypto non-compliance at a scale that was not possible even two years ago. If you hold crypto on any major exchange, assume the IRS knows about it.

For taxpayers with crypto held on foreign exchanges, additional reporting requirements like FBAR and Form 8938 may also apply. See our guide on FBAR and Form 8938 for crypto for details.

How to Respond: Step-by-Step

Regardless of which letter you received, here is a practical framework for responding.

1. Identify the Letter Type

Check the letter number in the upper-right corner. This determines your required level of response.

2. Confirm the Tax Years in Question

Letter 6173 will reference specific tax years. Focus your review on those years first, but also check adjacent years for similar issues. Letters 6174 and 6174-A are considered “soft notices” and do not identify a specific tax year. If you receive one of these notices, review prior-year returns to determine whether any cryptocurrency activity may have been improperly reported.

3. Reconstruct Your Transaction History

Pull records from every platform you used. Include:

- Centralized exchanges (Coinbase, Kraken, Gemini, etc.)

- Decentralized exchanges (Uniswap, SushiSwap, etc.)

- Wallet-to-wallet transfers

- Staking and lending rewards

- Airdrops and hard forks

- NFT purchases and sales

If you lost access to an exchange or cannot retrieve records, a crypto tax CPA can often help reconstruct activity using blockchain data.

4. Compare Against Filed Returns

Look at your Form 8949 and Schedule D for each year. Did you report all dispositions? Did you use the correct cost basis? Were staking rewards included as ordinary income?

5. File Amended Returns if Needed

If you find discrepancies, file Form 1040-X for each affected year. Include corrected Form 8949 and Schedule D. Pay any additional tax owed with the amendment to stop interest from accruing.

6. Respond to the IRS (Letter 6173 Only)

Use the response form included with the letter. Attach your amended return or a statement explaining your position. Send everything via certified mail and keep a copy for your records.

Amending Past Returns with Form 1040-X

Filing an amended return can feel daunting, but it is often the smartest move when you have unreported crypto activity. Here is what you need to know.

Statute of limitations: The IRS generally has three years from the date you filed your original return to assess additional tax. However, if you underreported your income by more than 25%, the window extends to six years. And if the IRS suspects fraud, there is no time limit at all.

What to include: Your 1040-X should include corrected Form 8949 (listing each transaction), an updated Schedule D, and a clear explanation of the changes. If you had losses you did not previously claim, you may actually receive a refund. For more on claiming losses, see our article on lost and stolen crypto tax deductions.

Processing time: Amended returns currently take 8 to 16 weeks to process. Electronic filing for 1040-X is available for tax years 2021 through 2025.

Penalties and What Is at Stake

The penalties for unreported crypto income vary depending on the severity of the non-compliance.

| Penalty Type | Rate | Details |

|---|---|---|

| Failure-to-file | 5% per month, up to 25% | Applies if you did not file a return at all |

| Failure-to-pay | 0.5% per month, up to 25% | Applies to unpaid tax balances |

| Accuracy-related | 20% of underpayment | Applies when the IRS determines negligence or substantial understatement |

| Fraud | 75% of underpayment | Applies in cases of intentional tax evasion |

| Criminal prosecution | Up to 5 years in prison | Reserved for the most egregious cases of willful evasion |

Interest compounds daily on any unpaid balance, starting from the original due date of the return. The longer you wait to address the issue, the more expensive it becomes.

The IRS generally does not need to prove that a taxpayer fully understood the tax code in order to assess taxes, penalties, or interest. It only needs to prove you knew about the income and chose not to report it. Willful blindness is not a defense.

When to Hire a Crypto Tax CPA

Not every IRS letter requires professional help, but certain situations make it strongly advisable:

- You received Letter 6173. A formal response is required, and mistakes can escalate the situation.

- You have multiple years of unreported activity. Amending several years of returns with complex crypto transactions is not a DIY project.

- You used DeFi protocols, bridges, or wrapped tokens. These transactions create complicated tax events that are easy to misreport.

- You held crypto on foreign exchanges. FBAR and FATCA requirements add another layer of compliance risk.

- You are facing a potential audit. Having professional representation from the start changes the dynamic entirely.

At CountOnSheep, we specialize in exactly these situations. If you need help responding to an IRS letter or cleaning up past filings, schedule a consultation.

Voluntary Disclosure: A Last Resort Worth Knowing About

If your crypto non-compliance is significant (think six figures or more in unreported gains across multiple years), the IRS Voluntary Disclosure Practice may be worth considering. This program allows taxpayers to come forward and disclose previously unreported income in exchange for reduced penalties and, in most cases, protection from criminal prosecution.

Voluntary disclosure is not a casual decision. It requires full cooperation, payment of all back taxes and interest, and typically involves substantial penalties. But compared to the alternative (a criminal investigation), it is the far better outcome.

This is a situation where you absolutely need professional guidance. A crypto tax CPA or tax attorney experienced with IRS voluntary disclosure can evaluate whether this path makes sense for your circumstances.

Real Scenarios: What This Looks Like in Practice

The Casual Trader

Sarah traded BTC and ETH on Coinbase in 2023 and 2024, making about $8,000 in net gains. She forgot to report the activity. In early 2026, she received Letter 6174-A. She reviewed her records, filed amended returns for both years, paid the additional tax plus a small penalty, and resolved the issue quickly.

The DeFi User

Marcus earned $45,000 in staking rewards and LP fees across multiple DeFi protocols in 2024. He reported none of it. He received Letter 6173 referencing Coinbase data. He hired a crypto CPA, reconstructed his full DeFi history, filed amended returns, and responded within the 30-day window. The back taxes, interest, and penalties were significant, but he avoided an audit.

The Ignorer

David received Letter 6173 in 2025 and threw it away. Six months later, the IRS initiated an examination. His case was assigned to an agent who assessed tax higher than what David actually owed (using estimated figures). He then had to hire a CPA and tax attorney to dispute the assessment, costing far more than responding initially would have.

The pattern is consistent: early action leads to better outcomes. Delay and avoidance make everything worse.

Bottom Line: What to Do Next

If you have received any IRS crypto letter, here is your action plan:

- Identify the letter type (6173, 6174, or 6174-A) and understand the required response level.

- Gather all crypto transaction records for the years in question.

- Review your filed returns for accuracy and completeness.

- File amended returns if you find unreported activity. Do this before the IRS follows up.

- Respond formally if you received Letter 6173. Do not miss the deadline.

- Get professional help if the situation is complex, involves multiple years, or includes DeFi/foreign exchange activity.

The IRS is not going to stop sending these letters. With 1099-DA data now flowing in from every major exchange, the agency’s ability to identify unreported crypto income is only getting stronger. The best time to get compliant was yesterday. The second-best time is right now.

Need help responding to an IRS crypto letter or cleaning up past returns? Contact CountOnSheep to work with a CPA who specializes in cryptocurrency tax compliance.

Frequently Asked Questions

What is IRS Letter 6173?

Letter 6173 is the most serious IRS crypto letter. It requests a formal response and may indicate the IRS believes you have unreported crypto income. You must reply.

What is IRS Letter 6174?

Letter 6174 is an informational notice acknowledging your crypto activity. It does not require a response but indicates the IRS is aware of your holdings.

What is IRS Letter 6174-A?

Letter 6174-A is a soft reminder to report crypto properly. No response is required, but you should take it seriously and review your past filings.

Should I hire a CPA if I get an IRS crypto letter?

For Letter 6173, yes. It requires a formal response and may involve amending returns. For 6174 and 6174-A, consulting a CPA is recommended if you have unreported crypto activity.

Can I go to jail for not reporting crypto?

Tax evasion is a federal crime punishable by up to 5 years in prison. However, most crypto non-compliance cases result in penalties and back taxes, not criminal prosecution.