Per-wallet cost basis tracking is the IRS requirement that each crypto wallet or exchange account must maintain its own independent pool of cost basis lots. Under Revenue Procedure 2024-28, this became mandatory on January 1, 2025. If you hold crypto across multiple wallets (and most active investors do), this rule fundamentally changes how your gains and losses are calculated.

Before this ruling, many taxpayers tracked their crypto cost basis in a single universal pool. That era is over. Every wallet is now its own tax universe.

For a broader overview of crypto tax rules, including cost basis fundamentals and reporting requirements, see our complete crypto tax guide for 2026.

What Does Rev. Proc. 2024-28 Actually Say?

Revenue Procedure 2024-28, published by the IRS in late 2024, establishes formal guidance for how digital asset holders must track and report cost basis. The key provision: cost basis lots are tied to the specific wallet or account where the asset is held.

In practical terms, the ruling does three things:

-

Defines “wallet” broadly. A wallet includes exchange accounts (Coinbase, Kraken), self-custody wallets (MetaMask, Ledger), and any other address or account where you hold digital assets.

-

Requires per-wallet lot tracking. When you sell or dispose of crypto from a specific wallet, you can only use cost basis lots that exist within that same wallet. You cannot pull a high-cost lot from your Coinbase account to offset a sale on your Ledger.

-

Provides a one-time safe harbor. Taxpayers had until January 1, 2025 to allocate their existing (pre-2025) holdings to specific wallets using any reasonable method.

The IRS signaled this direction for years through its broader digital asset reporting framework. Rev. Proc. 2024-28 simply codified it into a binding procedure that applies to all taxpayers.

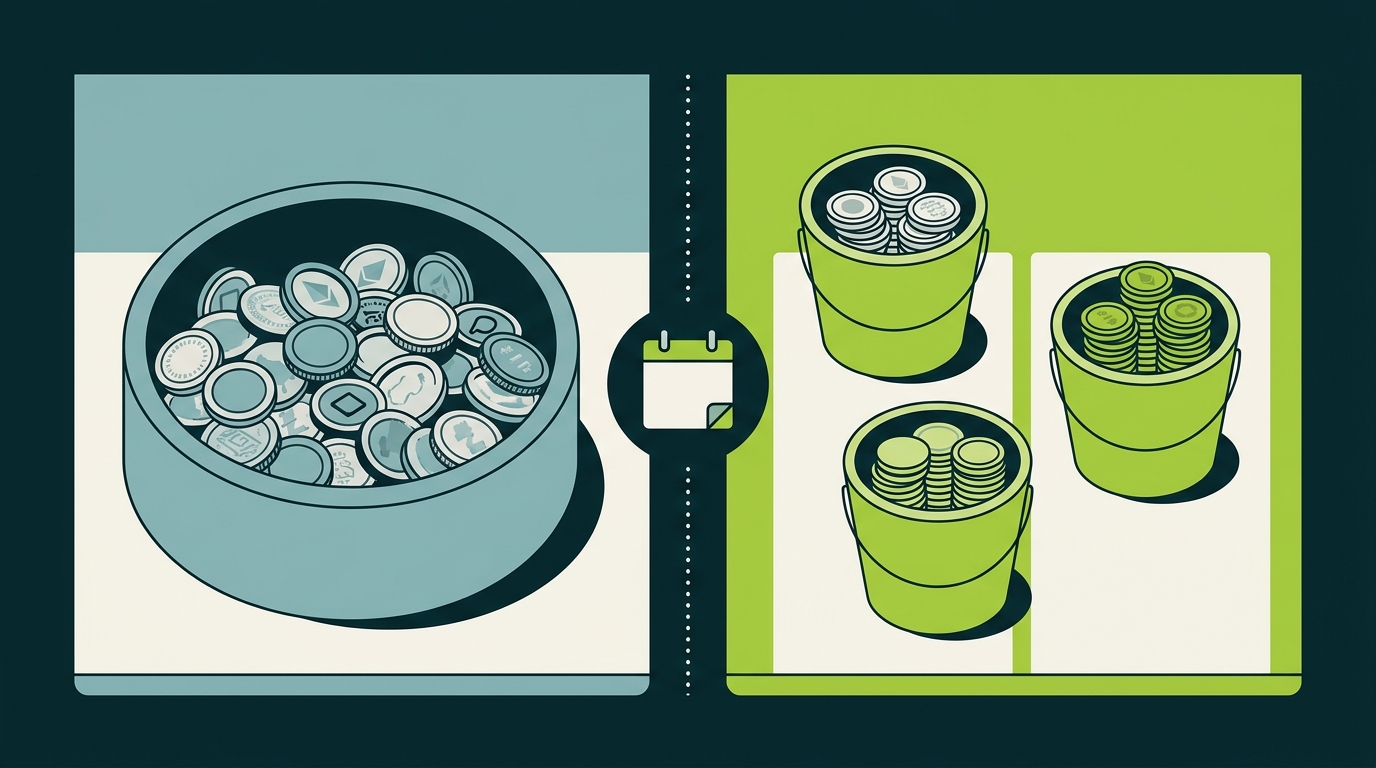

Universal vs. Per-Wallet Tracking: What Changed

The Old Way (Universal Pooling)

Before 2025, many crypto investors treated their entire portfolio as one big pool. If you bought 2 BTC on Coinbase and 1 BTC on Kraken, your cost basis software often lumped all three into a single bucket. When you sold 1 BTC from any wallet, the software would pick the optimal lot from the entire pool.

This approach was simpler. It was also more tax-efficient in many cases, because you could always select the highest-cost lot across all wallets when using HIFO or Specific Identification.

The New Way (Per-Wallet)

Starting January 1, 2025, each wallet is a silo. If you sell 1 BTC from your Coinbase account, you can only use cost basis lots that are associated with that Coinbase account. Your Kraken lots and your Ledger lots are irrelevant to that specific sale.

This means the same portfolio can produce very different tax outcomes depending on where your assets are held and where you sell them.

A Real Example: Universal vs. Per-Wallet Outcomes

Let’s walk through a concrete scenario to see the difference.

Setup: You own 3 ETH total, purchased at different times and held in different wallets.

| Lot | Purchase Date | Cost Basis | Wallet |

|---|---|---|---|

| Lot A | Jan. 2023 | $1,200 | Coinbase |

| Lot B | Jun. 2023 | $1,800 | Ledger |

| Lot C | Nov. 2024 | $3,400 | Coinbase |

Sale: You sell 1 ETH from Coinbase in March 2026 for $4,000.

Under universal cost-tracking (old rules): Using HIFO, the software picks Lot C ($3,400 basis) regardless of wallet. Your gain is $4,000 - $3,400 = $600.

Under per-wallet rules (current): Using HIFO within Coinbase, the software picks from Coinbase lots only (Lot A at $1,200 or Lot C at $3,400). HIFO selects Lot C. Your gain is still $4,000 - $3,400 = $600.

In this case, the outcome is the same. But watch what happens if you sell from the Ledger instead.

Now consider selling 1 ETH from your Ledger instead for $4,000.

Old Rules: HIFO Across All Wallets

HIFO picks Lot C ($3,400 basis) from Coinbase, even though you are selling from Ledger. Gain = $4,000 - $3,400 = $600.

Current Rules: HIFO Within Ledger Only

The only Ledger lot is Lot B ($1,800 basis). You cannot access Coinbase’s higher-cost lots. Gain = $4,000 - $1,800 = $2,200.

This is why per-wallet tracking matters.

The Safe Harbor Deadline: What If You Missed It?

Rev. Proc. 2024-28 included a one-time safe harbor provision. Taxpayers had until January 1, 2025 to allocate all pre-existing crypto holdings to specific wallets. During this window, you could use any “reasonable allocation method” to assign lots. For example, you could have assigned your highest-cost lots to wallets you planned to sell from first.

If you used the safe harbor correctly: Your allocations are locked in. The IRS will respect your chosen allocation as long as you documented it and it was reasonable.

If you missed the safe harbor deadline: The situation is more complicated, but not hopeless. You may need to reconstruct your allocation using transaction records, blockchain data, and exchange history. The IRS has not published specific penalties for missing the safe harbor window, but defaulting to a less favorable allocation (or having the IRS impose one during an audit) is a real risk.

How to Migrate to Wallet-Based Cost Tracking

There are two methods available to use per Rev. Proc. 2024-28:

-

Global Allocation Method. The Global Allocation Method assigns unused tax lots across wallets using a single governing rule. For example, with the rule “lowest cost basis to highest balance,” tax lots are sorted from lowest to highest cost basis and assigned first to the wallet with the largest balance.

Example:

- Wallet A: 1 ETH

- Wallet B: 5 ETH

- Wallet C: 10 ETH

Starting with unused tax lots as of 11:59 PM on 12/31/2024, the lowest cost basis lots would be assigned to Wallet C until it reaches 10 ETH, then to Wallet B until it reaches 5 ETH, and the remaining highest cost basis lots would go to Wallet A.

Other example rules include:

- “Oldest tax lots to highest balance”

- “Oldest tax lots to least active wallet”

- “Highest cost basis to lowest balance”

-

Specific Allocation Method. This method does not rely on a predefined allocation rule. Instead, it allows the taxpayer to manually assign each unused tax lot however they choose. Using the spreadsheet of unused basis, the taxpayer can review the tax lots line by line and allocate them to specific wallets or exchanges until each wallet or exchange reflects the correct asset balance.

Cost Basis Methods Within Each Wallet

Per-wallet tracking changes where your lots live. It does not change which cost basis method you can use. Within each wallet, you can still apply any IRS-approved method:

-

FIFO (First-In, First-Out): Sells the oldest lots first. This is the IRS default if you do not specify a method. Learn more in our FIFO vs. HIFO vs. Spec ID comparison.

-

HIFO (Highest-In, First-Out): Sells the highest-cost lots first, minimizing your taxable gain on each sale.

-

Specific Identification (Spec ID): You choose exactly which lot to sell. This offers the most control but requires the most detailed record-keeping.

You can use different methods for different wallets. You could run HIFO on your Coinbase account and FIFO on your Ledger if that produces the best overall outcome. The key constraint is consistency within each wallet for a given tax year.

Taxpayers must identify the specific unit of digital asset being sold, exchanged, or otherwise disposed of by reference to the wallet or account in which such unit is held.

Common Mistakes to Avoid

1. Treating transfers as disposals. Moving crypto from Coinbase to your Ledger is not a sale. But if your software does not recognize it as a transfer, it may generate a phantom gain or loss.

2. Forgetting to carry basis on transfers. When you transfer crypto between wallets, the cost basis must follow the asset. If Lot A ($1,200 basis) moves from Coinbase to Ledger, it should remain a $1,200 basis lot in the Ledger.

3. Using universal pooling after January 1, 2025. Some older software versions or manual spreadsheets may still default to universal pooling. This is no longer compliant.

4. Ignoring DeFi wallets. Every on-chain wallet counts, including wallets used for DeFi protocols, staking, or liquidity pools. These are not exempt from per-wallet tracking.

5. Not documenting your safe harbor allocation. Even if you made a reasonable allocation before the deadline, you need written records to prove it during an audit.

Bottom Line: What to Do Next

Per-wallet cost basis tracking is here to stay. Whether you handled the safe harbor allocation perfectly or you are just learning about these rules now, here is your action plan:

-

Audit your current setup. Confirm that your crypto tax software is tracking lots on a per-wallet basis, not pooling them universally.

-

Reconstruct if needed. If you missed the safe harbor deadline, start building your allocation records using exchange history and blockchain data.

-

Choose your methods strategically. Review which cost basis method (FIFO, HIFO, Spec ID) makes sense for each wallet based on the lots it contains.

-

Get professional help if your situation is complex. Multiple wallets, DeFi activity, cross-chain transfers, and large portfolios all increase the risk of errors.

At CountOnSheep, we help crypto investors and traders get per-wallet tracking right. From safe harbor reconstruction to ongoing tax preparation, our team handles the complexity so you do not have to. Schedule a consultation or learn more about our crypto accounting services.

Frequently Asked Questions

What is per-wallet cost basis tracking?

Per-wallet tracking means each crypto wallet or exchange account maintains its own independent cost basis lots. You can no longer pool purchases across all wallets into one universal bucket.

When did per-wallet tracking become mandatory?

Per-wallet cost basis tracking became mandatory on January 1, 2025, under IRS Revenue Procedure 2024-28.

What was the safe harbor deadline?

The safe harbor window for allocating legacy holdings to specific wallets closed on January 1, 2025. If you missed it, you may need to reconstruct records retroactively.

Can I still use HIFO with per-wallet tracking?

Yes. You can use any IRS-approved cost basis method (FIFO, HIFO, Spec ID) within each wallet. The per-wallet rule only changes how lots are grouped, not which method you apply.

What happens if I don't comply with per-wallet tracking?

The IRS may default your cost basis to FIFO within each wallet and could flag discrepancies during an audit. Non-compliance increases your risk of penalties.