MetaMask is the most widely used self-custody wallet in crypto, with tens of millions of users moving funds across Ethereum, Layer 2 networks, and dozens of DeFi protocols. That freedom comes with a catch most people learn too late: MetaMask gives you no tax forms, no automatic gain calculations, and no cost basis records. Every swap, bridge, mint, and reward sits on a public blockchain, and in 2026 the IRS is reading it.

This is the most complete MetaMask tax guide available. It covers exactly how wallet, DeFi, NFT, staking, and bridge activity is taxed, how to calculate cost basis the way the new wallet-level rules require, what the 1099-DA era means for self-custody, and how to stay audit ready. If you want one resource that answers every MetaMask tax question, this is it.

Disclaimer: This guide is for informational purposes only and is not tax or legal advice. Cryptocurrency rules change quickly. Always consult a qualified CPA about your specific situation.

What Is MetaMask?

MetaMask is a non-custodial cryptocurrency wallet that runs as a browser extension and mobile app. It lets you hold tokens, connect to decentralized applications, swap assets, and interact with smart contracts across Ethereum and EVM-compatible networks like Base, Arbitrum, Optimism, and Polygon. Unlike an exchange account, you control the private keys, which means you control the assets directly.

How MetaMask Works

When you create a MetaMask wallet, you generate a unique public address (your wallet ID) and a private seed phrase that only you hold. Funds you receive live at that address on the blockchain, not on a company server. When you swap a token, bridge to another chain, or mint an NFT, MetaMask signs a transaction with your key and broadcasts it to the network. That transaction is then recorded forever on a public ledger that anyone, including the IRS, can inspect.

Why MetaMask Taxes Are Different

With a centralized exchange like Coinbase, the platform tracks your buys and sells and hands you a tax summary. MetaMask does none of that. It is a key manager, not an accountant. This creates three challenges that make MetaMask taxes uniquely difficult:

- No cost basis tracking. MetaMask never records what you originally paid for an asset, so gains and losses are not calculated for you.

- High transaction complexity. A single DeFi session can generate dozens of taxable events: swaps, approvals, LP deposits, reward claims, and more.

- Multi-chain sprawl. Funds bridged across Ethereum, Base, Arbitrum, and other networks must be reconciled into one coherent tax picture.

MetaMask is a key manager, not an accountant. The tax math is entirely on you.

This is why connecting your wallet address to dedicated crypto tax software (compare Koinly vs CoinTracker comparison) or working with a crypto tax specialist is essential for active MetaMask users.

Does MetaMask Report to the IRS?

This is the single most searched MetaMask tax question, and the answer has real consequences. MetaMask does not file reports with the IRS the way a bank or broker does. But that does not mean your activity is invisible or untaxed. The blockchain itself is the report.

Does MetaMask Issue 1099 Forms?

No. As a self-custody, non-custodial wallet, MetaMask is generally not classified as a broker under current Treasury rules, so it does not issue Form 1099-DA for ordinary wallet swaps and transfers. The centralized exchange where you originally bought your crypto (Coinbase, Kraken, and others) is the entity that issues 1099-DA, starting with the 2025 tax year filed in 2026.

The absence of a form is not the absence of a tax obligation. You are legally required to report every taxable MetaMask transaction whether or not anyone sends you a document.

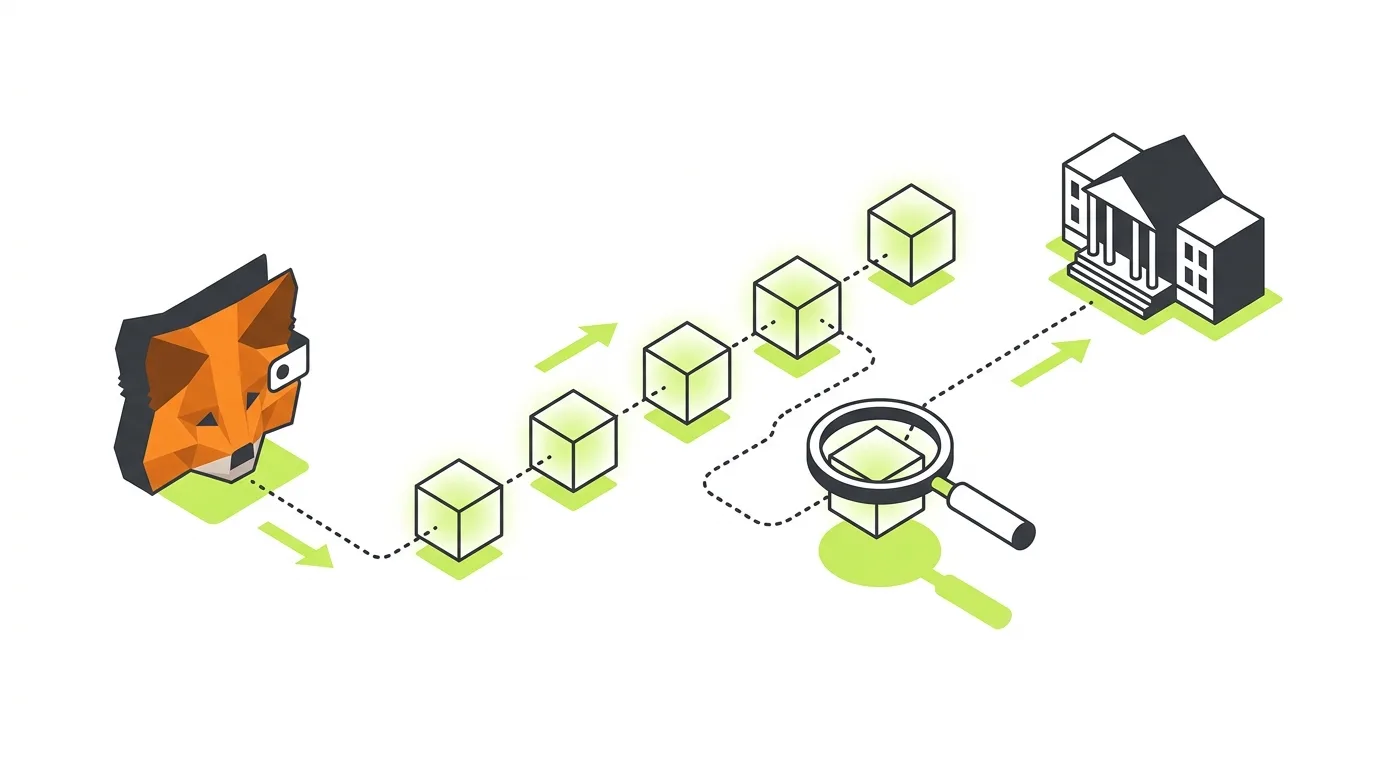

Can the IRS Track MetaMask Wallets?

Yes, more easily than most people assume. The IRS contracts with blockchain analytics firms such as Chainalysis to trace transactions across wallets and chains. The instant your MetaMask address interacts with a KYC exchange (where your identity is verified), that address can be linked to your legal name. From there, every connected wallet, swap, and transfer becomes part of a traceable graph.

Blockchain Transparency and Wallet Tracing

Public blockchains are pseudonymous, not anonymous. Your address is not your name, but it is a permanent identifier that links every action you take. Analysts cluster addresses by behavior, follow funds through bridges and mixers, and connect on-chain activity to off-chain identity through exchange records, IP data, and subpoenas. Treat your MetaMask history as a public financial statement, because functionally it is one.

MetaMask and 1099-DA Reporting

Here is the nuance most articles miss. The original broker rules targeted centralized platforms. Whether and how self-custody and DeFi front-ends fit into future 1099-DA reporting has been one of the most contested areas of crypto tax policy, and the rules have shifted. The practical takeaway for 2026 is straightforward:

- Centralized exchanges issue 1099-DA for the crypto you buy and sell there.

- MetaMask generally does not issue 1099-DA for self-custody swaps and transfers.

- You remain responsible for reconciling everything, including the gap between what an exchange reported and what you actually did after moving funds into MetaMask.

That reconciliation gap is exactly where audits start. When an exchange reports that you withdrew 5 ETH to a self-custody wallet, the IRS expects to eventually see what happened to it. For a deeper breakdown of the form itself, read our complete 1099-DA explainer.

How Crypto Taxes Work

Before diving into specific MetaMask scenarios, you need the foundation. The IRS treats cryptocurrency as property, not currency, under Notice 2014-21. That single classification drives almost every rule that follows. Because crypto is property, every disposal is a potential capital gains event, the same way selling a stock or a piece of real estate is. There are only two tax buckets that matter, and almost every MetaMask transaction falls into one of them: capital gains or ordinary income. Master the difference and the rest of this guide clicks into place.

Capital Gains

When you dispose of crypto (sell, swap, or spend it), you realize a capital gain or loss equal to the difference between your proceeds and your cost basis. Gains are taxable. This is the most common category of MetaMask tax. The formula never changes: proceeds minus cost basis equals gain or loss. What makes MetaMask hard is not the math, it is collecting accurate proceeds and basis figures across thousands of on-chain events.

Ordinary Income

When you receive new crypto as income (staking rewards, airdrops, mining, or payment for services), it is taxed as ordinary income at its fair market value on the day you gain control of it. That value also becomes your cost basis for when you later sell. Our crypto income guide covers this category in depth.

Short-Term vs Long-Term Gains

Holding period determines your rate.

- Short-term (held one year or less): taxed at ordinary income rates, up to 37%.

- Long-term (held more than one year, 366+ days): taxed at preferential rates of 0%, 15%, or 20%.

For active MetaMask traders who swap frequently, most gains end up short-term, which is why timing and cost basis optimization matter.

Cost Basis

Cost basis is what you paid for an asset, including acquisition fees. For MetaMask, this is the hard part: the wallet never records it. If you bought 1 ETH for $2,000 on Coinbase, sent it to MetaMask, and swapped it for USDC when ETH was worth $3,000, your basis is $2,000 and your gain is $1,000. Lose track of that $2,000 basis and the IRS can treat your entire $3,000 as gain.

Wallet-Level Accounting

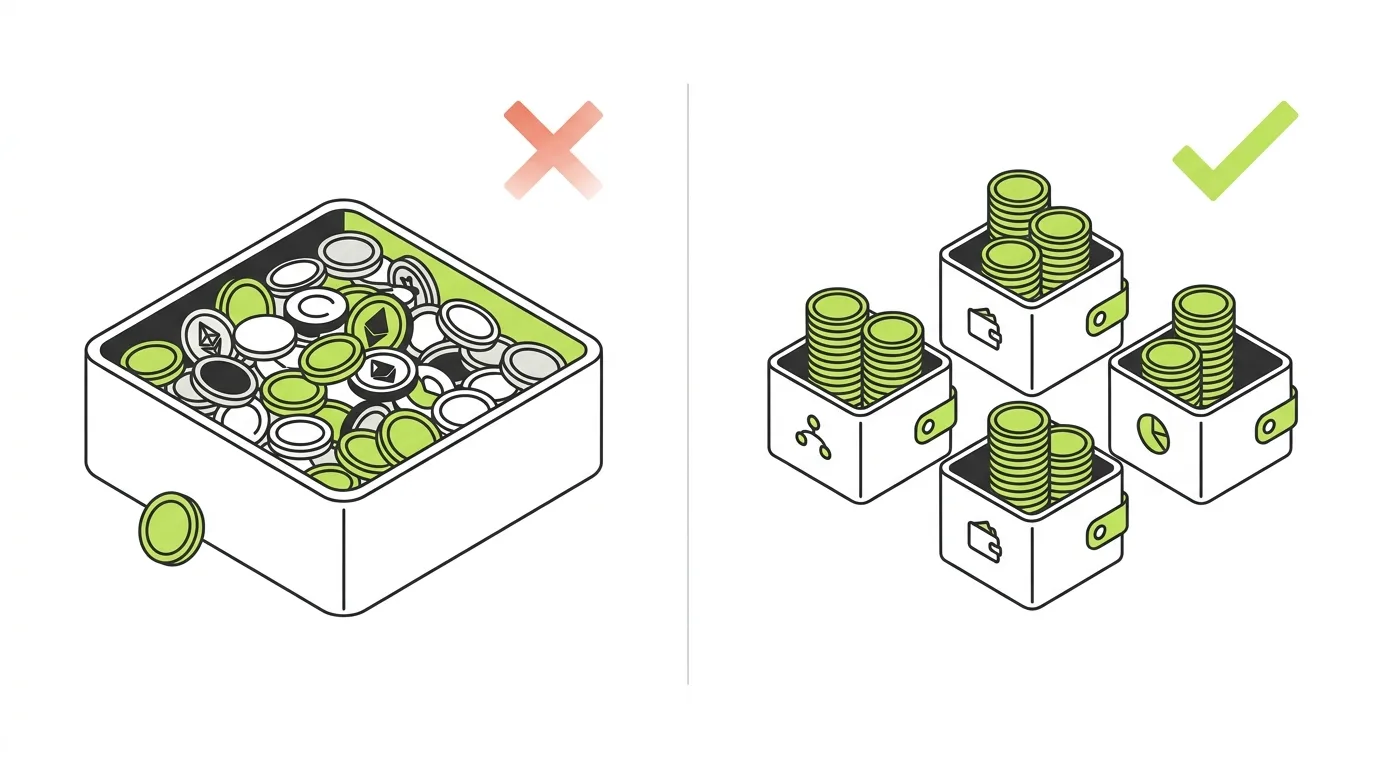

This is one of the most important 2026 changes. Under Rev. Proc. 2024-28, effective January 1, 2025, the old method of pooling all your crypto into one universal cost basis pile is gone. You must now track cost basis per wallet and per account.

For MetaMask users with multiple addresses, this means each wallet maintains its own basis records, and you can no longer freely assume a lot from one wallet covers a sale in another. We break down the mechanics in our per-wallet cost basis guide.

MetaMask Transactions That Are NOT Taxable

Not everything you do in MetaMask triggers tax. Knowing the non-taxable events prevents overpaying and reduces noise in your records.

Buying Crypto

Buying crypto with US dollars (for example, using MetaMask’s on-ramp to purchase ETH) is not taxable. You are simply converting cash into property. The purchase sets your cost basis.

Transfers Between Wallets

Moving crypto from one wallet you own to another (Coinbase to MetaMask, or MetaMask to a Ledger) is not a taxable event. You still own the same asset. You must, however, carry the original cost basis with it.

Moving Funds Between Chains

Bridging the same asset to another chain you control, without swapping it into a different token, is generally a non-taxable transfer. (Bridges that convert or wrap assets are a different story, covered below.)

Self-Custody Transfers

Sending funds to your own hardware wallet or another self-custody address is not a disposal. Ownership never changed hands.

Posting Collateral

Depositing crypto as collateral in a lending protocol, without disposing of it, is generally not taxable at the moment of deposit. The tax questions arise from what you do next: borrowing, earning yield, or liquidation.

For a complete map of what does and does not trigger tax, see our taxable vs non-taxable crypto events guide.

MetaMask Transactions That ARE Taxable

These are the events that create reportable gains, losses, or income. Most MetaMask users underestimate how many of their actions land here.

Selling Crypto

Selling crypto for dollars is a disposal. Gain or loss equals proceeds minus cost basis.

Swapping Tokens

This is the big one for MetaMask. Swapping ETH for USDC, or one token for any other token, is a taxable disposal of the token you give up. You realize gain or loss on that token at its fair market value at the moment of the swap, even though no dollars touched your bank account.

The Token Swap Trap

You bought 1 ETH for $2,000. Months later you swap it for 3,000 USDC when ETH is worth $3,000. Even though you “just moved into a stablecoin,” you disposed of ETH and owe tax on a $1,000 gain.

Spending Crypto

Using crypto to buy goods, services, or NFTs is a disposal of that crypto. If the token appreciated since you acquired it, you owe tax on the gain even while spending it.

Buying an NFT With Appreciated ETH

You bought 0.5 ETH for $600. Later you spend that 0.5 ETH (now worth $1,800) to mint an NFT. You disposed of ETH, so you owe tax on an $1,200 gain, completely separate from whatever happens to the NFT afterward.

Receiving Payment

Getting paid in crypto for work or services is ordinary income at fair market value on the day received. That value becomes your cost basis going forward.

NFT Sales

Selling an NFT is a taxable disposal. Minting and flipping NFTs through MetaMask generates capital gains or losses (and possibly collectible treatment, discussed later).

Token Redemptions

Redeeming or burning a token for a different asset, unwrapping a wrapped token into something economically different, or claiming an underlying asset can all be taxable disposals depending on the mechanics.

The key question is whether you ended up holding an economically different asset. Burning a project token to claim a brand new token is usually a disposal. Redeeming a receipt token for the exact underlying you deposited may be closer to a non-event. Because protocols structure these mechanics differently, treat each redemption on its own facts and keep the contract interaction records.

MetaMask Staking Taxes

Staking through MetaMask, whether via liquid staking tokens or validator delegation, creates income tax events that catch many users off guard.

When Rewards Become Taxable

Staking rewards are taxable as ordinary income at fair market value when you gain dominion and control over them, meaning when you can freely sell or transfer them. This follows the IRS position in Rev. Rul. 2023-14.

Dominion and Control

If rewards accrue but are locked and you cannot move them, the income event may be deferred until they unlock. If they hit your wallet and you can transact immediately, that is your taxable moment. Track the date and value of each reward.

How Rewards Affect Cost Basis

The fair market value you report as income becomes the cost basis of those reward tokens. When you later sell them, you calculate gain or loss against that basis, avoiding double taxation on the same value.

Common Staking Mistakes

- Forgetting to report rewards as income because no form arrived.

- Using the wrong date or price for fair market value.

- Failing to set the reward’s cost basis, then overpaying capital gains later.

- Mishandling liquid staking tokens (like stETH) that rebase or accrue value.

Our full staking, mining, and airdrop income guide walks through the reporting mechanics.

MetaMask DeFi Taxes

DeFi is where MetaMask taxes get genuinely hard, and where the biggest reporting errors happen. Each protocol interaction can spawn multiple taxable events. Here is how the major categories are treated.

Uniswap Trades

Every swap on Uniswap (or any DEX) through MetaMask is a taxable disposal of the token you trade away. High-frequency DeFi traders can generate hundreds of these events in a year, each requiring a gain or loss calculation.

Liquidity Pools

Depositing two tokens into a liquidity pool can be treated as a disposal of those tokens in exchange for LP tokens, which is a debated but commonly conservative position. When you withdraw, you dispose of the LP token for the underlying assets, creating another event.

There are two schools of thought. Under the conservative (disposal) approach, contributing ETH and USDC to a Uniswap pool is a taxable exchange of those assets for a new LP token, and withdrawal is a taxable exchange back. Under the non-disposal approach, some practitioners argue a deposit is merely a change in form of a beneficial interest, not a true disposal. The IRS has not issued definitive guidance, so most CPAs default to the conservative treatment to avoid surprises in an audit. Whichever position you take, apply it consistently and document your reasoning.

Adding ETH to a Liquidity Pool

You deposit 1 ETH (basis $2,200, value $3,000) and 3,000 USDC into a pool and receive an LP token. Under the conservative approach, you disposed of ETH at $3,000, realizing an $800 gain on the ETH leg, even though you never cashed out. Your LP token takes a $6,000 combined basis.

LP Tokens

LP tokens represent your pool share. Receiving them, holding them while their value changes, and redeeming them all carry potential tax consequences. The conservative approach treats deposit and withdrawal as taxable exchanges.

Yield Farming

Reward tokens earned from farming are ordinary income at fair market value when claimed or controlled. Selling them later is a separate capital gains event. Auto-compounding vaults complicate this further by generating frequent reward events.

Aave Lending

Supplying assets to Aave and receiving aTokens, then earning interest, generally produces ordinary income on the yield. The deposit itself may or may not be a disposal depending on the mechanics of the receipt token.

Compound Lending

Compound’s cTokens work similarly. The exchange-rate accrual model means your cToken grows in claimable value over time, raising questions about when income is recognized. Document supply, accrual, and redemption.

Borrowing Stablecoins

Borrowing against your crypto collateral is generally not a taxable event, because a loan is not income. But the moment your collateral is sold or liquidated, that disposal is taxable.

Leveraged DeFi

Looping (borrow, swap, redeposit) multiplies the number of taxable disposals. Each swap in the loop is its own event. Leveraged positions can create large, surprising tax bills even in a losing trade.

Consider a common leverage loop: you supply ETH to Aave, borrow USDC against it, swap that USDC for more ETH, and resupply. The borrow is not taxable, but the swap of USDC into ETH is a disposal of the USDC. Repeat the loop three times and you have generated three separate taxable swaps. If your collateral is later liquidated when the market drops, that forced sale is yet another taxable disposal, often at a loss, but a loss you still must report and document. Leverage amplifies both your market risk and your reporting complexity.

Flash Loans

Flash loans executed and repaid in a single transaction generally do not create income, but any swaps, arbitrage profits, or fees realized inside that transaction can be taxable. The profit is what matters.

In DeFi, one click can be five taxable events. The software you use to reconcile it matters as much as the trade itself.

For DeFi-heavy wallets, importing cleanly is half the battle. Our Koinly DeFi import guide and NFT and DeFi tax breakdown cover the specifics.

MetaMask NFT Taxes

NFTs bought, sold, and minted through MetaMask follow capital gains rules, with a few twists.

Buying NFTs

Buying an NFT with ETH is a disposal of that ETH. If your ETH appreciated since you acquired it, you owe capital gains tax on the ETH even as you spend it on the NFT. The NFT’s cost basis is the value you paid plus gas.

Selling NFTs

Selling an NFT is a capital gains event: sale proceeds minus your cost basis (purchase price plus minting and gas costs). Note that NFTs deemed “collectibles” may face a higher 28% long-term capital gains rate.

Royalty Income

If you are a creator earning royalties on secondary sales, those royalties are ordinary income at fair market value when received. If you mint and sell NFTs as a business rather than a hobby, your activity may rise to the level of self-employment, which changes how income is reported and can subject you to self-employment tax. The line between investor, creator, and dealer matters, so get advice if NFT activity is a meaningful part of your income.

NFT Airdrops

Receiving an NFT airdrop can be ordinary income at fair market value when you gain control, then a separate capital gains event when you sell. Valuing illiquid airdropped NFTs is a known gray area; document your reasoning.

Bridge Transactions and Cross-Chain Taxes

Bridges are one of the largest and least understood MetaMask tax gaps. Whether a bridge is taxable depends on what happens to your asset.

Ethereum to Base

Moving ETH from Ethereum mainnet to Base while keeping it as ETH is generally a non-taxable transfer of the same asset between chains you control.

Ethereum to Arbitrum

Same principle. Bridging native ETH to Arbitrum without converting it usually is not a disposal. Keep the bridge transaction records to prove continuity of ownership.

Ethereum to Optimism

Identical treatment for like-for-like asset bridging. The risk appears when the bridge issues a different representation of the asset.

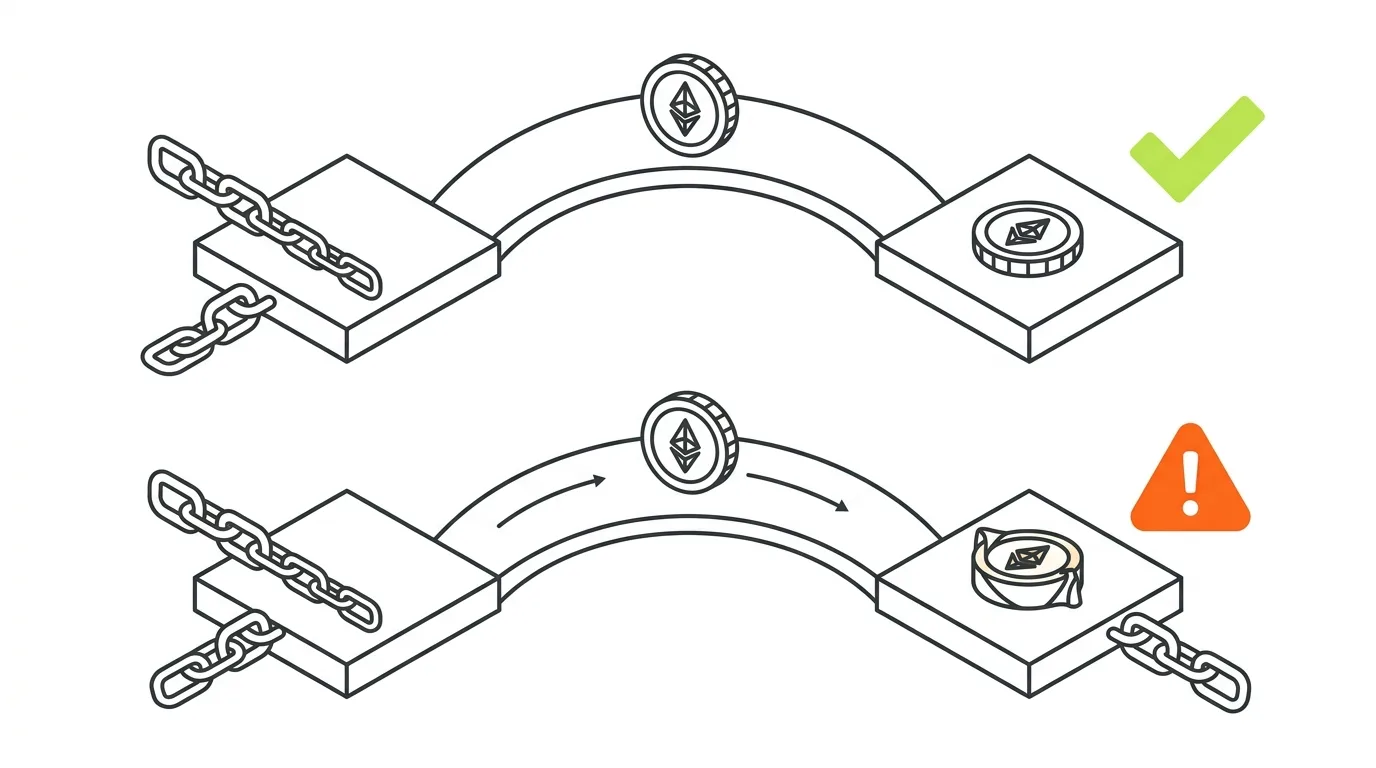

Wrapped Assets

This is the trap. If a bridge converts ETH into a wrapped or bridged variant that is economically a different token (for example a bridge-specific USDC or a wrapped asset), the IRS may treat that conversion as a taxable disposal. Wrapping ETH into WETH is often treated conservatively as a disposal as well, though the economic-substance argument cuts both ways. When in doubt, document and ask a CPA.

The practical risk is twofold. First, you may owe tax on a conversion you assumed was free. Second, and more common, your tax software may assign the wrapped token a zero cost basis because it cannot trace it back to the original ETH, which inflates your gain when you eventually sell the wrapped asset. Always link wrapped and bridged tokens back to their source so basis carries through correctly.

Bridge Failures

A failed bridge that consumes gas but does not move funds still costs you. The gas spent on a failed transaction is generally treated as a non-deductible personal loss for investors, though it may adjust basis in narrow cases. Record failures so they do not look like missing funds during reconciliation.

Gas Fees and Tax Reporting

Gas fees are unavoidable on MetaMask, and their tax treatment depends on what the gas was for.

Failed Transactions

Gas spent on a transaction that fails is generally not deductible for individual investors and does not reduce a gain because no disposal occurred. Keep the records anyway for reconciliation.

Swap Fees

Gas paid to execute a taxable swap can be added to the cost basis of the asset acquired or netted against proceeds of the asset sold, reducing your taxable gain.

Bridge Fees

Gas and bridge fees on a non-taxable transfer generally adjust the cost basis of the asset being moved rather than producing a deduction.

NFT Mint Fees

Gas paid to mint or buy an NFT is added to that NFT’s cost basis, lowering your gain when you eventually sell.

How to Calculate MetaMask Cost Basis

Choosing and applying a cost basis method correctly can change your tax bill by thousands of dollars. Here are the accepted methods.

FIFO

First In, First Out sells your oldest lots first. It is the IRS default. In a rising market, FIFO tends to produce larger gains because the oldest coins usually have the lowest basis.

LIFO

Last In, First Out sells your newest lots first. It can reduce gains in some scenarios but requires meticulous records and adequate identification.

Specific Identification

Spec ID lets you choose exactly which lot you are selling, which is the most powerful method for minimizing tax. It requires detailed records identifying the specific units at the time of sale.

Wallet-Level Cost Basis

As covered above, Rev. Proc. 2024-28 requires basis tracking per wallet starting in 2025. Your chosen method (FIFO, HIFO via Spec ID, and so on) now operates within each wallet, not across a single universal pool.

Sells Oldest, Cheapest Lot

You sell 1 ETH for $4,000. FIFO uses your oldest lot bought at $2,000. Gain = $2,000.

Sells Highest-Cost Lot

Same $4,000 sale, but you specifically identify a lot bought at $3,500. Gain = $500.

For a deeper comparison, read our guide on FIFO vs HIFO vs Spec ID.

How to Download MetaMask Transaction History

You cannot report what you cannot export. MetaMask gives you a few paths to your data.

MetaMask Tax Hub

MetaMask has partnered with tax tools to offer an in-wallet tax experience that estimates gains and connects to reporting software. It is a useful starting point, but for complex DeFi and multi-chain activity you will still want a full-featured tax platform.

Wallet Address Import

The cleanest method for most users: copy your public wallet address and paste it into crypto tax software. The software reads your entire on-chain history directly from the blockchain across supported networks. Add every address you have used.

CSV Exports

You can export transaction history as CSV from block explorers (like Etherscan) for each chain, then import into your tax tool. This is more manual and error-prone than address import but useful for chains your software does not auto-sync.

Best MetaMask Tax Software

The right software reads your MetaMask address, reconstructs your history across chains, and produces IRS forms. Here are the leading options for MetaMask users.

CoinTracker

Strong wallet and exchange coverage with solid MetaMask and EVM-chain support. A popular mainstream choice. See our CoinTracker review.

CoinLedger

User-friendly with good DeFi and NFT handling, and clean Form 8949 output. A frequent pick for self-custody users.

Koinly

Excellent multi-chain and DeFi coverage, widely used for complex MetaMask wallets. Read our Koinly review and the Koinly vs CoinTracker comparison.

TokenTax

A full-service option that pairs software with professional preparation, useful for high-complexity wallets.

Summ

A newer entrant focused on reconciliation accuracy for active on-chain users.

MetaMask Tax Forms Explained

Once your transactions are reconciled, they flow onto specific IRS forms.

Form 8949

Every capital asset disposal (sells, swaps, NFT sales) is listed on Form 8949 with acquisition date, disposal date, proceeds, cost basis, and gain or loss.

Schedule D

Totals from Form 8949 roll up to Schedule D, which summarizes your net short-term and long-term capital gains and losses.

Schedule 1

Crypto income (staking rewards, airdrops, certain DeFi yield) that is not self-employment income is generally reported as other income on Schedule 1.

1099-DA

The new digital asset form issued by centralized brokers. MetaMask itself generally does not issue it, but you will reconcile your MetaMask activity against any 1099-DA from the exchange you used. Full details in our 1099-DA guide.

Common MetaMask Tax Mistakes

These errors cost MetaMask users the most money and audit risk. Avoid all six.

Missing Cost Basis

When software cannot find what you paid for an asset, it often assigns a zero basis, making your entire sale look like profit. Always supply or verify basis for transferred-in assets.

Lost Wallets

Crypto in a wallet you lost access to is still tricky to write off. A true, documented loss may qualify for specific treatment; simply losing a key usually does not produce an easy deduction. See our lost and stolen crypto guide.

Untracked Bridges

Bridges mislabeled as sells inflate gains. Bridges mislabeled as zero-basis acquisitions inflate later gains. Review every bridge.

Incorrect LP Treatment

Liquidity pool deposits and withdrawals are frequently dropped or misclassified, leaving income unreported or gains overstated.

Duplicate Transactions

Importing the same activity from both a wallet sync and a CSV creates duplicates that double-count gains. De-duplicate before filing.

Missing Wallets

Forgetting a single address breaks the chain of cost basis and triggers zero-basis errors across every linked transaction.

How to Prepare for a MetaMask Tax Audit

Audit readiness is the differentiator almost no MetaMask guide covers. If the IRS asks, you want answers ready, not a scramble.

Recordkeeping

Keep a complete, dated record of every acquisition, disposal, reward, and transfer, including fair market values and the source of each figure. Export and archive your reconciled reports each year.

Wallet Hygiene

Use a consistent, documented set of wallets. Avoid mixing personal and business activity in one address. Label wallets and keep a register of which address did what.

Reconciling Multiple Wallets

Bring every address into one tax platform, reconcile balances against on-chain reality, and resolve every zero-basis flag and unknown transfer before you file. Wallet-level basis rules make this non-negotiable for 2025 and beyond.

Maintaining Audit Trails

For every reported number, you should be able to point to the on-chain transaction, the price source, and the method used. A clean audit trail turns a stressful inquiry into a paperwork exercise.

A defensible MetaMask audit file includes:

- The full transaction export from your tax software, reconciled and free of zero-basis flags.

- A wallet register listing every address, the chains it touched, and its purpose.

- Price source documentation showing where each fair market value came from and the timestamp used.

- Your cost basis method election and proof you applied it consistently across the year.

- Notes on judgment calls for gray areas (wrap/unwrap, LP deposits, bridge conversions, airdrop valuation), explaining the position you took and why.

- Copies of any 1099-DA forms from exchanges, with a reconciliation showing how exchange-reported proceeds connect to your self-custody activity.

If you can hand an examiner this package, most MetaMask audits resolve quickly. If you cannot, the IRS is free to make its own assumptions, and those assumptions rarely favor the taxpayer.

An audit is a documentation test. MetaMask users who keep clean, reconciled records pass it. Those who do not, pay for it.

If your MetaMask history is large or messy, do not face this alone. A crypto tax specialist can reconcile your wallets, fix basis errors, and build the audit trail for you.

Your MetaMask Tax Checklist

Use this checklist every tax season to keep your MetaMask reporting clean and audit ready. Save it, print it, or copy it into your notes.

- Gather every wallet address you have used, across every chain (Ethereum, Base, Arbitrum, Optimism, Polygon, and others).

- Connect each address to crypto tax software and pull the full transaction history.

- Import exchange data from any centralized platform you used to buy or off-ramp crypto.

- Reconcile transfers so wallet-to-wallet moves are marked as non-taxable, not as sells.

- Review every swap to confirm it is captured as a disposal with correct proceeds and basis.

- Check bridges manually, since these are mislabeled most often.

- Verify staking and reward income is recorded at fair market value on the date received.

- Confirm NFT buys, sells, and mints carry correct cost basis including gas.

- Resolve all zero-basis and unknown-source flags before you file.

- De-duplicate any transactions imported from both a wallet sync and a CSV.

- Choose and apply one cost basis method consistently, within each wallet (per Rev. Proc. 2024-28).

- Generate Form 8949 and Schedule D and reconcile income onto Schedule 1.

- Archive your reconciled reports and price sources for your audit file.

Bottom Line: What to Do Next

MetaMask gives you total control of your crypto and zero help with your taxes. In 2026, with wallet-level cost basis mandatory, 1099-DA live at exchanges, and blockchain forensics in the IRS toolkit, accurate reporting is no longer optional and guesswork is dangerous.

Here is your action plan:

- List every wallet address you have ever used, across every chain.

- Connect them to crypto tax software and pull your full history.

- Review DeFi, bridge, and NFT transactions manually, since these cause the most errors.

- Fix zero-basis and unknown-transfer flags before filing.

- Archive your reconciled reports to stay audit ready.

If your MetaMask activity goes beyond simple buys and sells, the smartest move is to get a professional in your corner. A 15-minute call with a crypto tax specialist can save you thousands and a great deal of stress. Reach out to our team for a MetaMask tax review and let us handle the reconciliation, the forms, and the audit trail.

Not sure your crypto taxes are right?

Talk to a Count On Sheep specialist. We will spot the costly errors before you file. No obligation.

Book My Free Review- Reviewed by Former Big 4 Accountants

- Keep your CPA

- No pressure, no sales pitch

Frequently Asked Questions

Does MetaMask report to the IRS?

MetaMask itself does not file tax forms with the IRS and does not issue 1099 forms for self-custody activity. However, every MetaMask transaction is recorded permanently on a public blockchain, and the IRS uses chain-analysis tools to trace wallet activity. You are legally required to report all taxable MetaMask transactions whether or not a form is issued.

Does MetaMask issue 1099 forms?

No. As a self-custody wallet, MetaMask is generally not treated as a broker, so it does not issue Form 1099-DA for ordinary wallet swaps and transfers. Centralized exchanges where you bought the crypto will issue 1099-DA starting with the 2025 tax year. You still owe tax on MetaMask gains regardless of any form.

Are MetaMask swaps taxable?

Yes. Swapping one token for another inside MetaMask (for example ETH for USDC) is a taxable disposal. You realize a capital gain or loss on the token you give up, measured by its fair market value at the moment of the swap minus your cost basis.

Are MetaMask bridge transactions taxable?

It depends. Moving the same asset across a bridge while keeping ownership is usually a non-taxable transfer. But if the bridge swaps or wraps your token into a different asset (for example ETH to WETH or to a bridged USDC variant), the IRS may treat it as a taxable disposal. Keep detailed records of every bridge.

Are MetaMask gas fees tax deductible?

Gas fees are generally not deductible for individual investors, but they do affect your taxes. Gas paid to acquire an asset is added to your cost basis, and gas paid to sell or dispose of an asset reduces your proceeds. Gas on a purely personal transfer is usually not deductible at all.

How do I calculate MetaMask gains?

For each taxable disposal, subtract your cost basis (what you paid plus acquisition fees) from the proceeds (fair market value received). The result is your capital gain or loss. Crypto tax software connected to your MetaMask wallet address automates this across thousands of transactions.

Can the IRS see my MetaMask wallet?

If the IRS can link a wallet address to your identity, yes. Public blockchains are fully transparent, and the moment you move funds to or from a KYC exchange, your address can be tied to you. The IRS contracts with blockchain forensics firms to trace activity across wallets and chains.

What happens if I don't report MetaMask taxes?

Unreported crypto income can trigger IRS notices (such as Letters 6173, 6174, and 6174-A), back taxes, interest, and penalties. Willful failure to report can lead to accuracy or fraud penalties. Because blockchain data is permanent, unreported activity can surface years later during an audit.

Do I owe tax if I only moved crypto into MetaMask?

No. Transferring crypto from an exchange or another wallet you own into MetaMask is not a taxable event, because you still own the same asset. You only create a tax event when you sell, swap, spend, or earn crypto. You must still carry over the original cost basis.

Is moving from MetaMask to a hardware wallet taxable?

No. Self-custody to self-custody transfers are not disposals.

Are testnet transactions taxable?

No. Testnet tokens have no fair market value.

Do I report MetaMask activity if I had a net loss?

Yes. Losses must be reported, and they can offset gains plus up to $3,000 of ordinary income, with carryforward.

Is unwrapping WETH to ETH taxable?

It is a gray area. Many practitioners treat wrap/unwrap conservatively as a disposal. Document your position.

Does using a VPN hide my MetaMask activity from the IRS?

No. The blockchain record is independent of your network connection.