Phantom makes self-custody easy. Taxes are where it gets complicated. If you trade Solana, collect NFTs, ape into memecoins, stake SOL, or touch DeFi through Phantom, you are generating taxable events the wallet will never report for you. Phantom is self-custody, which means it does not issue 1099s and it does not file anything on your behalf. You are responsible for tracking and reporting all of it.

This is the definitive Phantom Wallet Taxes guide for 2026, built specifically for Phantom and Solana users, not a generic crypto article with the word “Phantom” pasted in. We cover SPL token swaps, Jupiter and Raydium and Orca activity, Magic Eden and Tensor NFTs, memecoin disposals, staking and liquid staking, airdrops, bridges, the new Form 1099-DA mismatch problem, wallet-level cost basis, and an audit-ready reconciliation checklist.

Disclaimer: This guide is for informational purposes only and is not tax or legal advice. Cryptocurrency rules are evolving quickly. Always consult a qualified CPA about your specific situation.

Find Yourself: Which Phantom User Are You?

Phantom users are not all the same, and your tax exposure depends on how you use the wallet. Find your profile and jump to what matters most.

The SOL Holder

You bought SOL, moved it to Phantom, and mostly hold. Maybe a little staking.

You may owe little until you sell. Jump to Taxable Events →The Memecoin Trader

You swap Solana memecoins constantly through Jupiter and live on the volatility.

Every swap is a disposal. Jump to Memecoin Taxes →The NFT Collector

You mint, flip, and hold Solana NFTs on Magic Eden and Tensor.

Mints, sales, and royalties each have rules. Jump to NFT Taxes →The DeFi Power User

You provide liquidity, lend, stake, and farm across Raydium, Orca, Kamino, and Drift.

Your activity is income-heavy and messy. Jump to DeFi Taxes →The Cleanup Case

Years of Solana history, missing cost basis, and a 1099-DA that looks wrong.

You need reconciliation. Jump to the Audit Checklist →1. What Is Phantom Wallet?

Phantom is a self-custody crypto wallet. It started as the leading wallet for Solana and has grown into a multi-chain wallet that supports Ethereum, Bitcoin, Polygon, Base, and other networks depending on current support. You hold your own private keys, connect to decentralized apps, swap tokens, manage NFTs, and stake, all without a company holding your funds.

That self-custody design is the entire reason Phantom taxes are confusing. There is no broker sitting in the middle keeping clean records, matching your cost basis, and mailing you a finished tax form. Phantom gives you control. The trade-off is that the recordkeeping and the reporting are entirely on you.

Phantom’s own terms describe it as a wallet for self-custody, private-key control, decentralized apps, swaps, and related functionality. Nothing in that description includes tax preparation, because it is not a tax product.

Think of the difference this way. When you trade on a centralized exchange like Coinbase, the exchange knows exactly when you bought, what you paid, when you sold, and what you received. It can hand you a clean summary at year-end because it controlled both sides of every trade. Phantom never controlled your funds, so it has no equivalent ledger of your cost basis. It can show you the raw transactions on-chain, but it cannot tell you whether a given SOL came from a 50 dollar purchase or a 200 dollar purchase, because that information lives somewhere else, often on an exchange you used months earlier.

That gap is the heart of Phantom wallet taxes. The blockchain records what moved and when, but it does not record your cost basis in dollars, your intent, or which lot you disposed of. Reconstructing that context is the work, and it is why a Phantom tax return is more involved than a simple exchange-only return.

2. Do You Owe Taxes on Phantom Wallet?

Yes, if you had taxable events. The IRS treats virtual currency as property for federal tax purposes under Notice 2014-21. That single classification drives everything: when you dispose of property, you realize a capital gain or loss, and when you earn property, you realize ordinary income.

You owe taxes on Phantom activity when you sell, swap, spend, or earn crypto. You do not owe taxes simply for holding assets in the wallet or for moving your own assets between your own wallets. The rest of this guide is mostly about telling those two categories apart and reporting the taxable side correctly.

3. Does Phantom Report to the IRS?

Short answer: Phantom says it does not issue tax forms like 1099s, and it does not report your wallet activity to the IRS. As a self-custody wallet, it never takes custody of your funds, so it is not positioned as a broker that files information returns about you.

That is where most people stop reading, and that is the dangerous mistake. “Phantom does not report” is not the same as “my activity is invisible.”

Solana and Ethereum transactions live on public, permanent ledgers. Anyone can read them. The moment your Phantom wallet is connected to something that knows your identity, the chain becomes traceable back to you. Common links include:

- A withdrawal from a KYC exchange like Coinbase or Kraken into your Phantom address

- A fiat on-ramp used to fund the wallet

- A deposit back to an exchange that issues a 1099

- A wallet address you have publicly tied to your name

4. Does Phantom Give You Tax Forms?

No. Phantom does not give you a 1099, and it does not hand you a finished tax report. Phantom’s own help center states that because it is self-custody, users are responsible for tracking and reporting their own transactions.

What Phantom does offer is a help article on exporting your activity and a tax page that routes you to partner solutions such as Summ, CoinLedger, and CoinTracker. In other words, Phantom points you toward third-party tools rather than producing the report itself.

Phantom hands you the keys and the freedom. It does not hand you a 1099. The recordkeeping is yours.

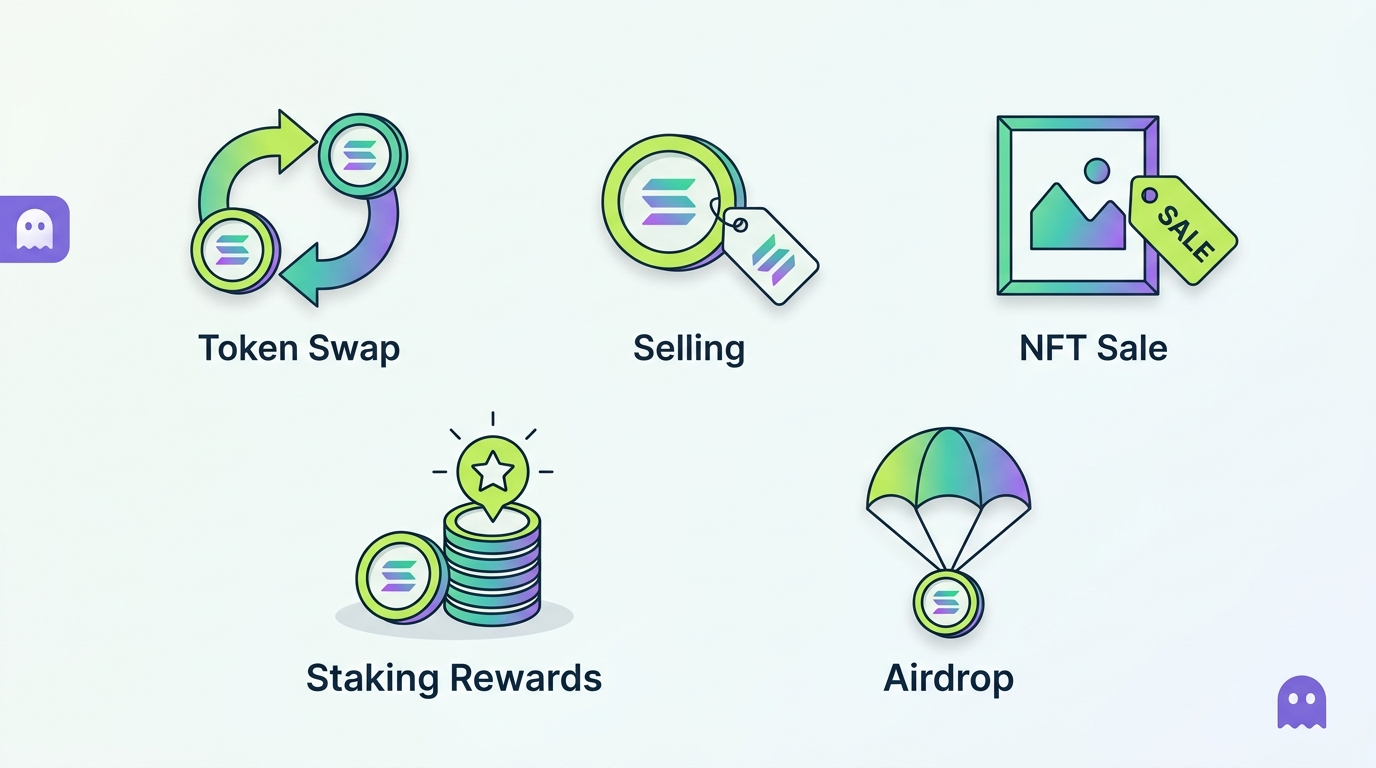

5. What Phantom Transactions Are Taxable?

A taxable event is any moment you dispose of crypto or earn crypto. In Phantom, the common taxable events are:

- Selling SOL or SPL tokens for fiat

- Swapping one token for another (SOL to USDC, USDC to a memecoin, one SPL token to another)

- Spending crypto on goods or services

- Selling an NFT on Magic Eden, Tensor, or any marketplace

- Receiving staking rewards from SOL or liquid staking

- Receiving DeFi yield, lending interest, or farming rewards

- Receiving payment in crypto for work or services

- Receiving airdrops that have value and that you control

- Liquidation events where collateral is sold to cover a loan

- Closing positions that dispose of an asset

The mental model: if an asset left your control and something of value came back, or if value showed up in your wallet that you now control, you probably have a taxable event to evaluate.

One nuance that trips up Phantom users: a token-for-token swap is taxable even though you never touched US dollars. The IRS does not require fiat for a disposal. Trading SOL for USDC realizes gain or loss on the SOL, and trading USDC for a memecoin realizes gain or loss on the USDC, even though USDC is a stablecoin pegged to a dollar. The peg keeps the gain or loss small, but the event still exists and still belongs on Form 8949.

6. What Phantom Transactions Are Usually Not Taxable?

Not everything triggers tax. These Phantom actions generally are not taxable events on their own:

- Buying crypto with fiat and simply holding it

- Holding SOL, SPL tokens, or NFTs without selling

- Moving assets between your own wallets (for example, Coinbase to Phantom, or Phantom to a Ledger), as long as you keep ownership of both

- Connecting Phantom to a dapp without transacting

- Approving a transaction or token allowance by itself

- Posting collateral, depending on how the protocol is structured

- Failed transactions, although any gas you paid still matters for records

7. Phantom Wallet and Solana Taxes

This is where a real Phantom guide separates itself from a recycled MetaMask article. Most Phantom users are Solana users, and Solana has its own quirks that change how you reconcile taxes.

Things to handle specifically on Solana:

- SOL disposals when you swap or sell native SOL

- SPL token swaps, which are the bulk of Solana trading activity

- Wrapped SOL (wSOL), which appears and unwraps constantly in DEX activity and can clutter your history

- Token account rent and closing token accounts, where small amounts of SOL are deposited to open an account and refunded when you close it

- Failed transactions, which are common on Solana and still cost fees

- Priority fees, the extra fees paid during congestion

- Solana DEX trades through Jupiter, Raydium, and Orca, which often route through multiple hops in a single transaction

- Missing market prices for new or thin tokens, which tax software frequently cannot value automatically

Wrapped SOL and the noise problem

Wrapped SOL deserves special attention because it generates so much confusion. Many Solana programs require SOL to be wrapped into the wSOL token to interact with them, then unwrapped afterward. To you it feels like nothing happened, you still have your SOL. But your transaction history fills with wrap and unwrap events that tax software can misread as swaps, creating phantom gains and losses that never really occurred. Wrapping SOL into wSOL at a one-to-one ratio is generally not an economic disposal, but an automated import may not know that. This is a classic line item to review and correct.

Token account rent

Solana charges a small amount of SOL to open a token account, refundable when you close it. These tiny deposits and refunds clutter your history and can be misclassified. They are generally not taxable income or a deductible loss on their own, but they are easy for software to mishandle, so they belong on your review list.

Failed transactions

Failed transactions are common on Solana, especially during congestion or when sniping new tokens. A failed transaction acquires nothing, yet you still paid a fee. The fee is a real economic cost, but the absence of an acquired asset makes the treatment less obvious than a normal fee that adds to basis. Keep the records and treat these consistently.

8. Phantom Memecoin Taxes

Phantom is a primary wallet for Solana memecoin trading, and memecoins are a tax minefield because of volume. Here is what actually happens at tax time.

Every swap may be a taxable disposal. When you swap SOL for a memecoin, you dispose of SOL. When you flip that memecoin back to SOL or to another token, you dispose of the memecoin. Hundreds of trades means hundreds of taxable events.

Frequent trading creates short-term gains and losses. Memecoins are usually held for days, hours, or minutes, so almost all of it is short-term, taxed at ordinary income rates. The upside: losses are real too, and they offset gains.

Rug pulls and worthless tokens need careful loss treatment. If a token goes to zero and the market is gone, you may have a loss, but how and when you can claim it depends on the facts. A token that still technically trades is different from one that is provably worthless or abandoned.

Missing cost basis is common. New tokens often have no clean price data, so software may import a swap with a blank or wrong value. These need manual review.

Spam tokens should not automatically be booked as income. Junk tokens that get airdropped into your wallet without your action are not automatically taxable income unless you have real dominion, control, and a verifiable fair market value.

Memecoin Flip Example

Now multiply that by a few hundred trades and you see the real problem. A heavy memecoin week can produce thousands of lines on Form 8949. The good news is that the losses are just as real as the gains, and in a volatile memecoin portfolio the losses are often substantial. Capturing every loss is how active traders avoid overpaying. The bad news is that thin, brand-new tokens frequently have no reliable price feed, so the software either guesses or leaves the value blank, and every one of those needs a human to assign a defensible fair market value.

9. Phantom NFT Taxes

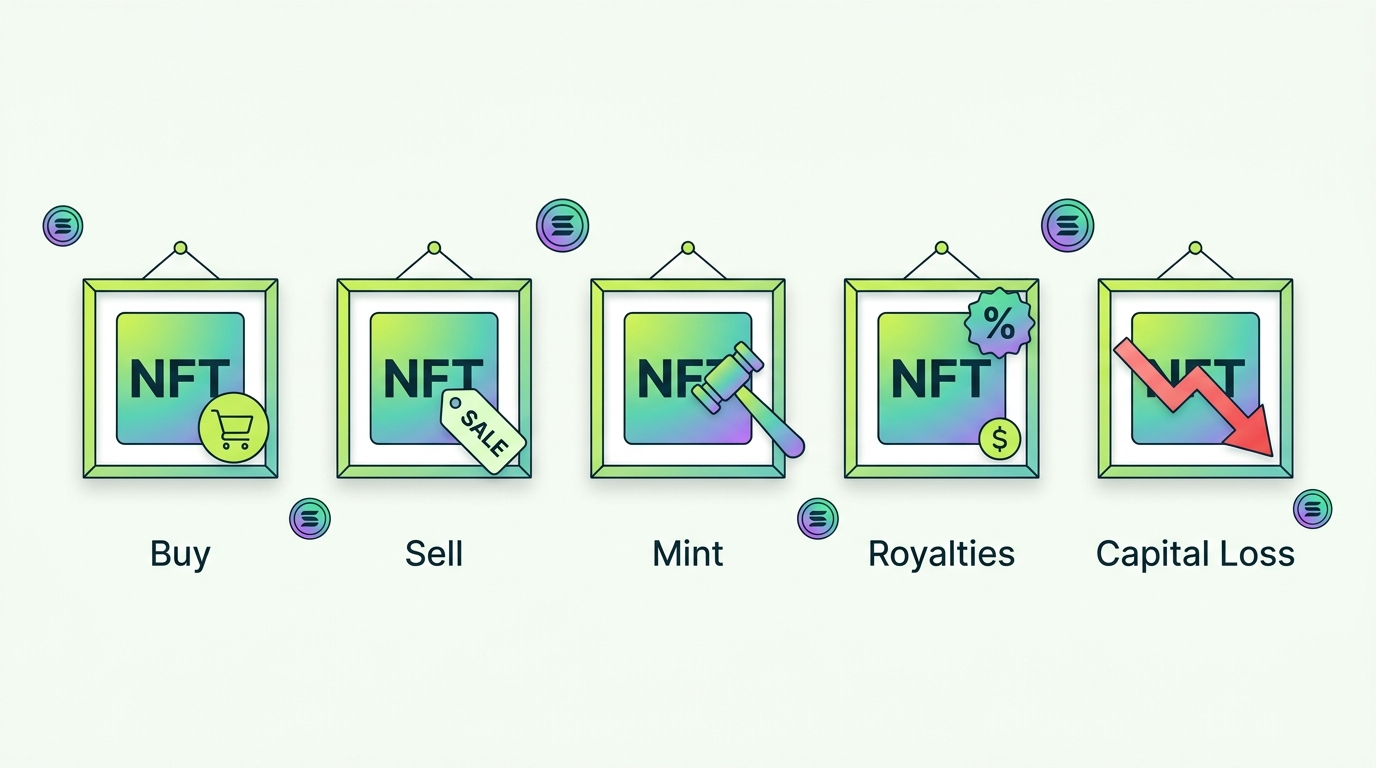

Phantom is heavily used for Solana NFTs, and NFTs are one of the most under-covered topics in existing Phantom guides. Each NFT action has its own treatment.

- Buying an NFT with crypto is a disposal of the crypto you spent. If you buy an NFT for 5 SOL, you dispose of that SOL and realize a gain or loss on it.

- Selling an NFT is a taxable disposal of the NFT. Proceeds minus your cost basis (including mint and marketplace fees) is your capital gain or loss.

- Minting an NFT typically uses crypto to mint, which disposes of that crypto. Your total mint cost, including fees, becomes the NFT’s cost basis.

- Airdropped NFTs with real value can be ordinary income at receipt, with that value becoming the basis. Many airdropped NFTs are spam and need scrutiny.

- Creator royalties received are ordinary income.

- NFT losses are capital losses when you sell below basis and can offset gains.

- Scam NFTs and rug pulls are common on Solana. Do not interact with suspicious NFTs, and treat worthless ones carefully.

- A collectible tax treatment caveat exists: certain collectibles can face a higher long-term capital gains rate, and how NFTs fit that category is an evolving area, so flag high-value long-term NFT sales for a professional.

A worked NFT example

Suppose you mint a Solana NFT for 1.5 SOL when SOL is worth 150 dollars, so your mint cost is 225 dollars plus a small network fee, call it 227 dollars of cost basis. Three months later you sell it on Magic Eden for 4 SOL when SOL is worth 160 dollars, so your gross proceeds are 640 dollars, less a marketplace fee and royalty, say 60 dollars combined, for net proceeds around 580 dollars. Your capital gain on the NFT is roughly 353 dollars, and because you held under a year it is short-term.

But do not forget the second event hiding inside the first. When you spent 1.5 SOL to mint, you also disposed of that SOL, so you have a separate gain or loss on the SOL itself measured from whatever you originally paid for it. Two assets moved, so two events exist. Missing the SOL disposal is one of the most common NFT reporting errors.

10. Phantom Staking Taxes

Staking is one of the most common ways Phantom users generate ordinary income, and the rules are specific.

- SOL staking rewards are ordinary income at fair market value when you gain dominion and control over them.

- Liquid staking through tokens like mSOL (Marinade) or jitoSOL (Jito) adds a wrinkle, because you receive a liquid token that tracks your staked position and accrues value.

- Staking rewards as income are recognized when you can actually control them, not necessarily when they are merely calculated.

- The cost basis of rewards equals the income value you reported at receipt.

- A later sale of reward tokens is a separate capital gain or loss measured from that basis.

SOL Staking Example

Native staking versus liquid staking

Native SOL staking and liquid staking are taxed differently in practice, and Phantom supports both, so it is worth separating them. With native staking, you delegate SOL to a validator and rewards accrue roughly every epoch. Those rewards are ordinary income as you gain control of them, and tracking the value at each accrual point across an entire year is tedious but necessary. Crypto tax software estimates these for you, but the per-epoch valuations are an area to spot-check because small timing differences add up.

Liquid staking is more subtle. When you stake SOL through Marinade and receive mSOL, or through Jito and receive jitoSOL, you typically receive a token whose exchange rate to SOL grows over time rather than receiving discrete reward payments. There are two competing interpretations: some treat the initial SOL-to-mSOL conversion as a taxable swap, while others treat it as a non-taxable deposit because you retain economic exposure to the same underlying SOL. The conservative position records a disposal at conversion; the more aggressive position defers until you redeem. The value accrual inside the liquid staking token is generally realized when you eventually swap or unstake it. Because the treatment is unsettled, this is a judgment call worth documenting and discussing with a professional.

For the broader rules on how staking, mining, and other crypto income are taxed, see our deep dive on crypto income tax for staking, mining, and airdrops.

11. Phantom DeFi Taxes

DeFi is the weakest-covered area in existing Phantom content, and it is where Phantom power users carry the most risk. Solana DeFi runs through protocols like Jupiter, Raydium, Orca, Kamino, Drift, Marinade, and Jito. Common DeFi events and their general treatment:

- Swaps on any DEX are disposals.

- Providing liquidity into a pool can be a disposal of the tokens you deposit, depending on how the protocol issues LP tokens, and LP tokens themselves can have their own basis and disposal events.

- Yield farming rewards are typically ordinary income at receipt.

- Lending interest (for example on Kamino) is ordinary income.

- Borrowing stablecoins against collateral is generally not income when you take the loan, but the mechanics matter.

- Liquidation events are taxable disposals of the collateral that was sold.

- Liquid staking tokens accrue value and create disposal events when swapped or redeemed.

- Perps and derivatives on platforms like Drift have their own complex treatment.

Why DeFi breaks automated imports

The core reason DeFi is hard is that protocols move assets in ways that look identical on-chain but differ in tax treatment. Depositing tokens into a liquidity pool, receiving an LP token, having that LP token rebalance as the pool shifts, and then redeeming it can be read by software as a chain of swaps, deposits, and withdrawals with no clear basis. Lending protocols issue receipt tokens that accrue value silently. Liquid staking tokens like mSOL and jitoSOL change in value relative to SOL over time, so redeeming them is a disposal with a gain baked in that automated tools often miss.

The practical consequence is that a DeFi-heavy Phantom user almost always has to do hands-on reconciliation. The right approach is to map each protocol you used, list the position types you held, and verify how each one was imported, rather than trusting that the totals are correct because a number appeared.

12. Phantom Bridge Taxes

Phantom is multi-chain, so bridging is common, and the tax treatment is genuinely unsettled in places. What to watch:

- Bridging SOL or SPL tokens to another network may or may not be a taxable event depending on whether the asset is considered the same asset or is swapped for a different wrapped asset.

- Wrapped assets received on the destination chain can be treated as a new asset under some interpretations.

- Moving from Solana to Ethereum, Base, or Polygon through a bridge needs careful records on both sides.

- Bridge fees are part of your cost records.

- Bridge failures, where a transaction does not complete cleanly, can leave orphaned or stuck balances that confuse imports.

- Taxable versus non-taxable bridge interpretations differ, and conservative versus aggressive positions exist.

The conservative versus aggressive bridge question

The central debate is whether bridging is a disposal. Under a conservative reading, when you bridge SOL from Solana and receive a wrapped representation on another chain, you have exchanged one asset for a different asset, which is a taxable swap. Under a more aggressive reading, you still hold economic exposure to the same underlying asset, so bridging is more like moving your own property between your own accounts, which is not taxable. The IRS has not issued bright-line guidance specific to bridging, so both positions exist in practice.

What matters most for a Phantom user is not picking the most favorable interpretation in isolation, it is keeping records clean enough to support whatever position you take and to keep your cost basis intact across chains. The real damage from bridging is rarely the bridge event itself; it is the lost basis afterward. When an asset lands on a new chain with no recorded history, the next time you sell it the software assigns zero basis and your gain balloons. Treat the destination-chain asset as a continuation of the origin asset for basis purposes, and document the link with both transaction hashes.

13. Phantom Airdrop Taxes

Airdrops are common in the Solana ecosystem, and Phantom users see a lot of them, both real and junk.

- Taxable income on receipt applies when you have dominion and control over the airdropped tokens and they have a fair market value. That value is ordinary income.

- Spam token caution is essential. Unsolicited tokens dumped into your wallet without your action are different from a real airdrop you claimed. Junk with no genuine market should be reviewed rather than auto-booked as income.

- Token valuation can be hard when a token is brand new or thinly traded. Document how you valued it.

- A later sale of airdropped tokens creates a capital gain or loss measured from the income value you recorded.

- Documentation needed includes when you received control, the value at that time, and the transaction hash.

Real airdrops versus dust attacks

The Solana ecosystem has produced some of the largest token airdrops in crypto, and a Phantom user who farmed an ecosystem may receive a genuinely valuable distribution. When you claim a real airdrop and can freely move or sell the tokens, the fair market value at that moment is ordinary income, and that same value is your cost basis going forward. If the token then doubles before you sell, the extra gain is a separate capital gain.

The opposite case is the dust attack: tokens you never asked for that simply appear in your wallet, often as bait to lure you to a malicious site to swap them. These are not the same as a claimed airdrop. Generally, you do not have taxable income from a token you cannot meaningfully value or control, and unsolicited junk with no real market is not automatically income. The safe approach is to leave suspicious tokens untouched, never connect to an unknown site to deal with them, and document that you treated them as worthless spam rather than income. The difference between a real airdrop and a dust attack can be the difference between correctly reporting thousands of dollars of income and incorrectly inflating your income with worthless garbage.

14. Gas Fees and Phantom Taxes

Fees are small per transaction on Solana but add up across thousands of actions, and they affect your tax math.

- Swap fees and network fees paid to acquire an asset generally add to that asset’s cost basis.

- NFT mint fees add to the NFT’s cost basis.

- Fees on disposals generally reduce your proceeds.

- Failed transaction fees are tricky, because you paid a fee but acquired nothing. Keep the records and ask a professional how to treat them in your situation.

- Bridge fees belong in your cross-chain records.

The general rule for investors: fees to buy add to basis, fees to sell reduce proceeds, and fees on purely personal or failed actions are usually not separately deductible. Traders and businesses may have different options, which is a conversation to have with a CPA.

On Solana specifically, fees are tiny per transaction but enormous in count. A single active trader can rack up tens of thousands of fee entries in a year between swaps, mints, failed sniping attempts, and priority fees during congestion. Individually each is a fraction of a cent to a few cents; collectively they can total real money, and more importantly they are part of an accurate basis and proceeds calculation. The practical move is to let your tax software roll fees into the relevant acquisitions and disposals automatically, then verify it is doing so rather than dropping them. Do not try to hand-track every lamport, but do confirm fees are flowing into basis and proceeds rather than being ignored entirely.

15. How to Calculate Phantom Wallet Cost Basis

Cost basis is what you paid for an asset, and it determines your gain or loss when you dispose of it. For Phantom users, getting basis right is the single biggest driver of an accurate return. The accepted accounting methods:

- FIFO (First In, First Out): the IRS default, sells your oldest units first.

- HIFO (Highest In, First Out): sells your highest-cost units first to minimize gains.

- LIFO (Last In, First Out): sells your newest units first.

- Specific Identification: you choose exactly which units you are disposing of, the most control if your records support it.

Beyond the method, Phantom users face structural basis challenges:

- Wallet-level tracking now matters (see the next section on Rev. Proc. 2024-28).

- Transfers between exchanges and Phantom must carry basis with them or the gain is overstated.

- Missing acquisition history for old tokens has to be reconstructed from explorer and exchange data.

For a deeper breakdown of how these methods change your tax bill, see our guide to FIFO vs HIFO vs Spec ID for crypto taxes. The short version for Phantom users: HIFO and Specific Identification usually minimize your gains in a year of heavy trading, but they demand the cleanest records. If your Solana history is messy and you cannot prove which lot you sold, the IRS default of FIFO is what you are left with, and FIFO tends to produce larger gains in a rising market because it sells your oldest, cheapest units first.

16. Phantom Wallet and Form 1099-DA

Form 1099-DA is the new digital asset reporting form, and it changes the Phantom tax picture even though Phantom itself does not issue it. Here is the part most guides miss.

- Phantom generally does not issue 1099s because it is self-custody.

- Brokers may issue Form 1099-DA for assets you sold or exchanged through broker platforms. The IRS states Form 1099-DA reports digital asset proceeds from broker transactions.

- Early reporting focuses on gross proceeds, which means the form may show what you sold for without reliably showing what you paid.

- Cost basis may still need user reconciliation, because the broker often does not know your basis when the asset originally came from somewhere else.

- Wallet transfers can create missing basis issues. If you bought on an exchange, withdrew to Phantom, traded, and later sold somewhere that issues a 1099-DA, the proceeds and the basis can live in different systems.

This is the mismatch risk. The IRS may receive a 1099-DA showing high proceeds with little or no basis, while your real basis sits in your Phantom and exchange history. If you do not reconcile, the IRS sees a much larger gain than you actually had.

17. Wallet-Level Cost Basis: Rev. Proc. 2024-28

IRS Revenue Procedure 2024-28 created guidance for allocating digital asset basis to specific wallets and accounts, effective January 1, 2025. The old approach of pooling everything into one universal basis ledger is being replaced by per-wallet, per-account tracking.

For Phantom users who move assets between exchanges, Phantom, and other wallets, this matters a lot. Basis now has to be tracked at the wallet and account level, which means your Phantom wallet is its own bucket that needs accurate records of what came in, at what cost, and what left. This is exactly the kind of wallet-level accounting that generic Phantom guides barely mention.

The practical impact: the era of dumping every wallet and exchange into one big pile and applying a single FIFO queue across all of it is ending. Going forward, each account stands on its own for basis purposes, and you are expected to have made a reasonable allocation of your existing basis to your wallets as of the start of 2025. For a Phantom user, that means you should be able to answer, for your Phantom wallet specifically, what assets it held, what their basis was, and how that basis moved when assets entered or left. If you have never thought about your Phantom wallet as its own ledger, this is the moment to start, because the recordkeeping standard has tightened and the broker reporting that will be checked against it is expanding at the same time.

For the full picture on per-wallet tracking and the 2026 rules, see our Crypto Tax Guide 2026 and the dedicated Form 1099-DA explainer.

18. How to Export Phantom Transaction History

Phantom does not produce a finished report, so exporting is about getting your raw history into a tool that can. The practical path:

- Use your public wallet address. Your Solana address (and any addresses on other chains you used) is the key. Tax software imports on-chain history directly from the address.

- Follow Phantom’s tax export help article as the practical starting point for what Phantom offers.

- Use a Solana explorer like Solscan to view and export raw transaction data when you need to verify or fill gaps.

- Capture a CSV export where available so you have a portable record.

- Reconcile wallet by wallet. Each address is its own ledger under the new wallet-level rules.

- Account for multi-chain Phantom activity. If you used Phantom on Ethereum, Base, or Polygon, those addresses each need to be imported too.

A realistic export workflow looks like this. First, open Phantom and collect every receive address across every network you have used, not just your main Solana address. Second, paste each address into your chosen tax software so it pulls the on-chain history automatically. Third, separately import CSV files or API connections from every centralized exchange you used to buy crypto or cash out, because those records hold the cost basis that needs to follow your transfers into Phantom. Fourth, let the software attempt to match transfers between your exchange accounts and your Phantom wallet so basis carries across instead of resetting to zero. Fifth, review the flagged items: missing prices on thin Solana tokens, unmatched transfers, wrapped SOL noise, and anything labeled as income that is actually spam. The export is mechanical; the reconciliation is the work, and it is where accuracy is won or lost.

19. How to Report Phantom on Form 8949 and Schedule D

Once your Phantom history is reconciled, the actual filing for most users runs through two forms. Every taxable disposal, every swap, sale, NFT sale, and DeFi exit, becomes a line on Form 8949 with the asset, the date you acquired it, the date you disposed of it, your proceeds, your cost basis, and the resulting gain or loss. Short-term holdings (one year or less) and long-term holdings (more than one year) go in separate sections because they are taxed at different rates. The totals from Form 8949 then flow to Schedule D, which summarizes your net capital gain or loss for the year.

Your crypto income is reported separately. Staking rewards, airdrops with value, and other crypto earned as a hobby investor typically land on Schedule 1 as other income, while crypto earned as part of a trade or business may belong on Schedule C. And every filer answers the digital asset question on the front of Form 1040. Good crypto tax software generates the Form 8949 from your imported Phantom history, but you should still review it line by line, because a clean-looking total built on a missing wallet or a zero-basis import is exactly the kind of error that produces a real tax bill. For the step-by-step, see how to file crypto taxes with Form 8949 and Schedule D.

20. Best Phantom Tax Software

No tool is perfect for Solana, but several handle Phantom well as a starting point. Phantom’s own tax page lists partner solutions including Summ, CoinLedger, and CoinTracker. Common options:

- CoinTracker: broad support, Phantom partner, strong for portfolio plus tax.

- CoinLedger: clean TurboTax and TaxAct integration, Phantom partner. See our CoinLedger review.

- Koinly: wide exchange and chain coverage, popular for complex histories. See how to use Koinly.

- Summ: listed among Phantom’s partner tax solutions.

- Coinpanda: another option with Phantom wallet support.

- TokenTax: full-service leaning, higher touch.

- ZenLedger: established US-focused tool.

For a deeper comparison, see CoinLedger vs Koinly and CoinLedger vs CoinTracker.

21. Common Phantom Tax Mistakes

These are the errors we see most often on Phantom and Solana histories:

- Assuming no 1099 means no tax. Self-custody does not remove the tax obligation.

- Missing Solana wallet addresses. One uncovered address breaks the whole report.

- Ignoring NFTs. Mints, sales, and royalties are all taxable.

- Ignoring memecoin losses. Losses are real and valuable; not claiming them overpays tax.

- Not reconciling exchange withdrawals. Transfers into Phantom must carry basis.

- Duplicate wallet imports. Importing the same address twice double-counts activity.

- Missing cost basis. Untraced transfers default to zero basis and inflate gains.

- Treating every airdrop incorrectly. Real airdrops and spam tokens are different.

- Failing to document bridge activity. Cross-chain moves lose basis without records.

- Ignoring DeFi protocols. Liquidity, lending, and perps are routinely mishandled.

22. Phantom Wallet Tax Audit Checklist

Audit-readiness is a major gap in existing Phantom content, so here is a concrete reconciliation checklist. If you can check every box, your Phantom return is defensible.

Phantom Tax Audit-Ready Checklist

- ☐ Every wallet address, across every chain, identified and listed

- ☐ All exchange accounts imported, including closed ones via CSV

- ☐ Full transaction history pulled and de-duplicated

- ☐ Form 8949 generated and reviewed line by line

- ☐ Schedule D totals tie out to Form 8949

- ☐ Income report for staking, airdrops, and rewards

- ☐ Staking report with receipt dates and fair market values

- ☐ NFT report covering mints, sales, royalties, and losses

- ☐ DeFi report covering swaps, LPs, lending, and liquidations

- ☐ Bridge records with hashes on both chains

- ☐ Cost basis methodology chosen and applied consistently

- ☐ Screenshots and notes for unsupported or mispriced protocols

- ☐ Notes documenting scam and spam token handling

Phantom does not issue 1099s. Solana activity is public but messy. Tax software imports are not always perfect. That is exactly where reconciliation matters, and where Count On Sheep does the work.

Where Count On Sheep Fits

Phantom gives you self-custody and freedom. The cost is that the reconciliation layer is missing, and that is the exact problem we solve. Phantom does not issue 1099s, Solana activity is public but messy, tax software imports are imperfect, DeFi and NFT and memecoin activity often needs manual review, and 1099-DA will only increase mismatch risk while wallet-level cost basis raises the bar for clean records.

Count On Sheep prepares CPA-ready Digital Asset Reconciliation for Phantom and Solana users: we connect every wallet, match transfers, fix missing basis, handle the NFT, memecoin, and DeFi edge cases, and produce a defensible Form 8949 and income report you can actually file behind.

Not sure your crypto taxes are right?

Talk to a Count On Sheep specialist. We will spot the costly errors before you file. No obligation.

Book My Free Review- Reviewed by Former Big 4 Accountants

- Keep your CPA

- No pressure, no sales pitch

Related Reading

- Crypto Tax Guide 2026: IRS Rules, Forms and Rates

- Form 1099-DA Explained for 2026

- Crypto Income Tax: Staking, Mining and Airdrops

- How to File Crypto Taxes With Form 8949 and Schedule D

- FIFO vs HIFO vs Spec ID for Crypto Taxes

This guide is educational and not tax or legal advice. Digital asset rules change frequently. Consult a qualified CPA about your specific Phantom and Solana activity.

Frequently Asked Questions

Does Phantom report to the IRS?

Phantom is a self-custody wallet and says it does not issue tax forms like 1099s or report your activity to the IRS. That does not mean your activity is invisible. Solana and Ethereum transactions are recorded on public blockchains, and they can be traced when a wallet is linked to a KYC exchange, a fiat on-ramp, or a known address. You are still legally responsible for reporting every taxable Phantom transaction.

Does Phantom send 1099 forms?

No. Phantom's own help center states it does not issue 1099 forms because it never takes custody of your funds. Centralized brokers and exchanges may issue Form 1099-DA for assets you sold through them, but Phantom itself is not the 1099 source for your wallet activity. You reconcile any broker 1099-DA against your own Phantom records.

Do I pay taxes if I only hold crypto in Phantom?

No. Simply holding SOL, SPL tokens, NFTs, or any asset in Phantom is not a taxable event. You only owe tax when you trigger a taxable event such as selling, swapping, spending, or earning crypto. Unrealized gains on assets you still hold are not taxed.

Are Phantom swaps taxable?

Yes. Swapping one token for another inside Phantom, including through Jupiter, Raydium, or Orca, is a taxable disposal of the token you gave up. You calculate a capital gain or loss based on the fair market value at the moment of the swap minus your cost basis. This is true even when no US dollars are involved.

Are Solana swaps taxable?

Yes. Every Solana token swap is treated as selling one asset and buying another. The IRS taxes crypto as property, so trading SOL for an SPL token, or one SPL token for another, realizes a capital gain or loss on the token you disposed of.

Are Phantom NFT sales taxable?

Yes. Selling a Solana NFT on Magic Eden, Tensor, or any marketplace is a taxable disposal. Your gain or loss is the sale proceeds in fair market value minus what you paid to acquire or mint the NFT, including marketplace and network fees. NFT income such as royalties is ordinary income.

Are airdrops in Phantom taxable?

Generally yes, when you have dominion and control over the tokens and they have a fair market value. The value at receipt is ordinary income, and that value becomes your cost basis for a later sale. Be careful with unsolicited spam or scam tokens that appear in your wallet, because dumped junk tokens with no real market are a known gray area and should be reviewed rather than auto-booked as income.

Are staking rewards in Phantom taxable?

Yes. SOL staking rewards and liquid staking rewards are ordinary income at the fair market value when you gain dominion and control over them. That value becomes your cost basis, so when you later sell the reward tokens you also calculate a capital gain or loss from that point.

Are Phantom gas fees deductible?

It depends on the context. For investors, network fees paid to acquire an asset generally add to its cost basis, and fees paid to dispose of an asset generally reduce your proceeds. Fees on purely personal or failed transactions are usually not separately deductible. Treatment differs for traders and businesses, so document every fee and ask a professional how it applies to you.

How do I export Phantom transactions?

Phantom does not produce a finished tax report. The practical path is to take your public wallet address (or addresses) and import them into crypto tax software such as CoinTracker, CoinLedger, or Koinly, which pulls your on-chain history. You can also export transaction data from a Solana explorer. Because Phantom is multi-chain, you must capture every address on every network you used.

Can the IRS see Phantom wallet activity?

Potentially, yes. Phantom does not report to the IRS, but Solana and Ethereum ledgers are public and permanent. Once a wallet is connected to a KYC exchange withdrawal, a fiat ramp, or another identified address, blockchain analysis can link that wallet to you. Treat your Phantom activity as reportable and traceable.

What tax forms do I need for Phantom?

Most Phantom users report capital gains and losses on Form 8949 and Schedule D, and report crypto income such as staking, airdrops, and rewards on Schedule 1 or Schedule C depending on the activity. You also answer the digital asset question on Form 1040. If you sold through brokers, reconcile any Form 1099-DA against your own records.

How do I report Phantom on Form 8949?

Each taxable disposal becomes a line on Form 8949 with the asset, acquisition date, disposal date, proceeds, cost basis, and resulting gain or loss. Short-term and long-term holdings go in separate sections. The totals flow to Schedule D. Crypto tax software can generate a Form 8949 from your imported Phantom history, which you then review for accuracy.

How do I report Phantom staking rewards?

Report the fair market value of staking rewards as ordinary income for the year you received control of them, typically on Schedule 1 for a hobby investor. Record that value as the cost basis of the reward tokens. When you later sell or swap those tokens, report the capital gain or loss on Form 8949.

How do I report Phantom NFT losses?

If you sell an NFT for less than your cost basis, that capital loss goes on Form 8949 and offsets other capital gains, with up to 3,000 dollars of net loss usable against ordinary income per year and the rest carried forward. A truly worthless or abandoned NFT may support a loss claim, but the facts matter, so document the worthlessness carefully.

How do I handle scam tokens in Phantom?

Unsolicited scam and spam tokens that simply appear in your wallet are a known problem on Solana. Do not interact with them. Generally you do not book a token as income unless you have real dominion, control, and a verifiable fair market value. Flag these for review rather than automatically treating them as taxable income, and never sign transactions to dispose of suspicious tokens without checking they are not phishing approvals.

How do I handle missing cost basis in Phantom?

Missing cost basis is the most common Phantom tax problem, usually caused by transfers from an exchange or another wallet that the software cannot trace. Connect every wallet and exchange, import historical CSVs from closed accounts, and match transfers so the original purchase price follows the asset. When records are gone, you reconstruct basis from explorer data and exchange history, and document your method.

Does Phantom support tax reports?

Not directly. Phantom links users to partner tax solutions and provides a help article on exporting activity, but it does not generate a finished, filing-ready tax report itself. You use third-party crypto tax software or a crypto tax service to turn your Phantom history into Form 8949 and the rest of your filing.

What is the best Phantom tax software?

The strongest options for Phantom and Solana activity include CoinTracker, CoinLedger, and Koinly, all of which Phantom partners with or supports. The best choice depends on your transaction volume and how much DeFi, NFT, and memecoin activity you have. No tool fully automates messy Solana history, so plan on reviewing the import.

What happens if I don't report Phantom taxes?

Failing to report taxable crypto activity can lead to back taxes, penalties, and interest, and in serious cases it can escalate further. Because blockchains are permanent and broker 1099-DA reporting is expanding, the risk of mismatches the IRS can see is rising. If you are behind, the safest move is to reconcile your full history and file accurately, ideally with professional help.