Key takeaways

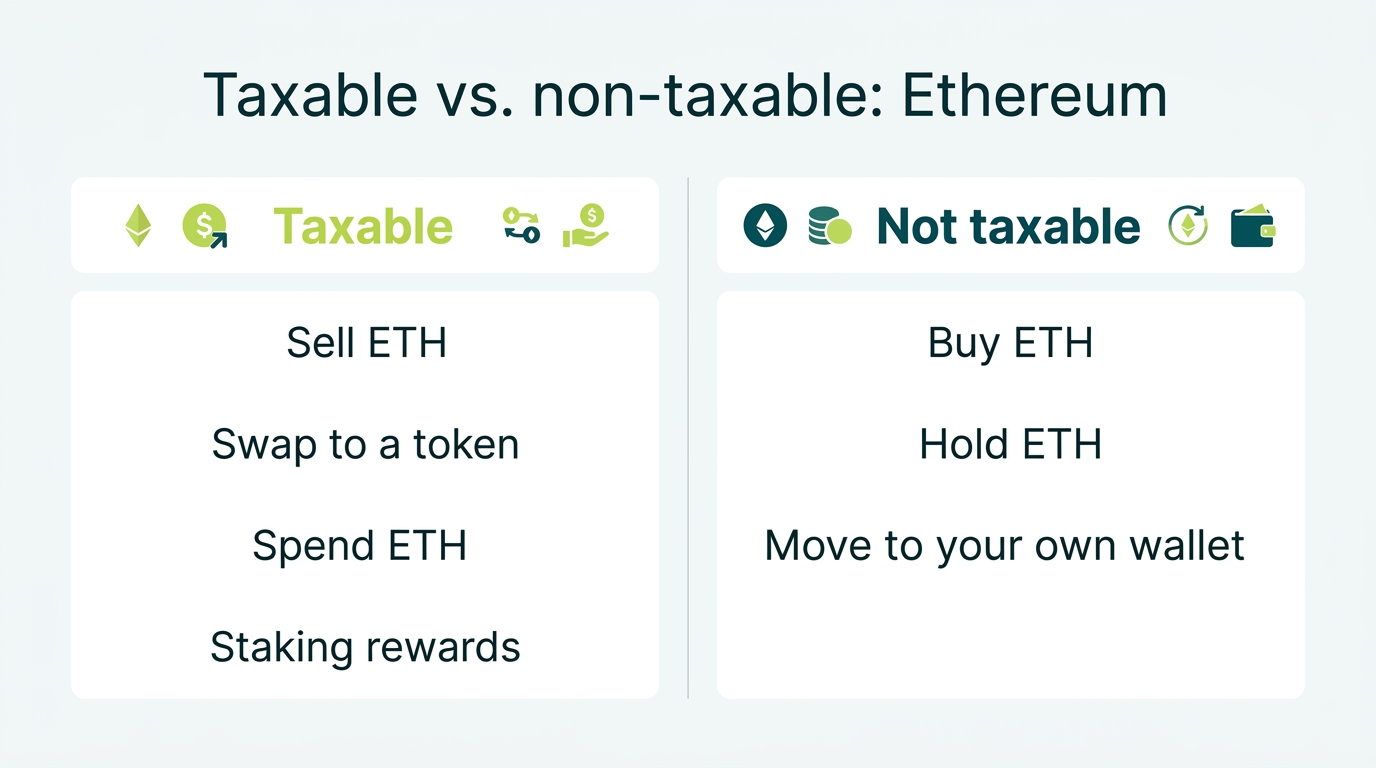

- Holding ETH is free; disposing of it is taxable. Selling, trading, or spending Ethereum triggers capital gains. Buying and holding does not, no matter how much it appreciates.

- Staking rewards are income, then capital gains. Rewards are ordinary income at fair market value when you control them, and the same ETH produces a separate gain or loss when sold. Liquid staking and restaking add gray areas the IRS has not resolved.

- Gas fees are small disposals with useful side effects. Paying gas spends ETH, and the fee usually either adds to an asset's cost basis or reduces sale proceeds.

- The IRS now gets a copy. Form 1099-DA reporting is live: US exchanges report your ETH sale proceeds directly to the IRS, and cost basis must be tracked wallet by wallet.

Ethereum is where crypto taxes stop being simple. A Bitcoin holder might have a dozen transactions a year. An Ethereum user who stakes, swaps tokens, provides liquidity, mints an NFT, and bridges to a Layer 2 can generate thousands of taxable events without ever touching dollars, and several of those events sit in genuine gray areas where the IRS has ruled on the principle but not the mechanics. Meanwhile the reporting rules tightened: brokers now send your sale proceeds straight to the IRS on Form 1099-DA, and cost basis must be tracked wallet by wallet. This guide walks through exactly when ETH is taxed, the 2026 rates, how staking and its liquid variants work, what gas fees do to your return, and how to report everything cleanly.

Do you have to pay taxes on Ethereum?

Yes, in two different ways. The IRS classified cryptocurrency as property in Notice 2014-21, so the framework that covers stocks and real estate covers ETH.

- Capital gains apply when you dispose of Ethereum: selling it for dollars, trading it for another token, spending it, or using it to pay gas. Your gain or loss equals what you received minus your cost basis.

- Ordinary income applies when you earn Ethereum: staking rewards, airdrops, most DeFi yield, and getting paid in ETH are all taxed at fair market value on the day you gain control of them.

What is never taxable matters just as much. Buying ETH with dollars is not taxable; it just sets your cost basis. Holding is not taxable through any amount of appreciation, because the US does not tax unrealized gains. And moving ETH between wallets you own, from Coinbase to a hardware wallet for example, is not a disposal. The basis and holding period travel with the coins, though the gas you pay to make the move is its own small disposal.

What counts as a taxable event for Ethereum?

Here is how the common Ethereum actions are treated for the 2026 tax year.

| Action | Taxable? | Treatment |

|---|---|---|

| Buy ETH with USD | No | Not taxable. Sets your cost basis. |

| Hold ETH | No | No tax while holding, even through big rallies. |

| Sell ETH for USD | Yes | Capital gain or loss (proceeds − basis). |

| Swap ETH for an ERC-20 token | Yes | Disposal of ETH; capital gain or loss. |

| Spend ETH on goods or services | Yes | Treated as selling ETH; capital gain or loss. |

| Pay gas in ETH | Yes | Small disposal of ETH; fee often adjusts basis or proceeds. |

| Receive staking rewards | Yes | Ordinary income at FMV when you control them. |

| Receive an airdrop | Yes | Ordinary income at FMV when received. |

| Get paid in ETH | Yes | Ordinary income at FMV when received. |

| Move ETH between your own wallets | No | Not taxable; basis and holding period carry. |

| Bridge ETH to a Layer 2 (same asset) | No* | Generally a self-transfer; gray area for swap-style bridges. |

| Donate ETH to charity | No | No capital gain; possible fair market value deduction. |

The swap row catches more people than any other. Trading ETH for USDC, an ERC-20 token, or an NFT feels like a sideways move, but the IRS sees a completed sale of your Ethereum at that moment's price. No dollars need to touch your bank account for a taxable gain to exist, and on Ethereum those swaps stack up fast.

Ethereum tax rates for 2026

There is no special "Ethereum tax rate." Like all property, the rate depends on how long you held before disposing and your total taxable income. One date does most of the work: the one-year mark.

- Short-term gains (held one year or less) are taxed at your ordinary federal rate, 10% to 37%.

- Long-term gains (held more than a year) are taxed at 0%, 15%, or 20%. Most filers land at 15%.

- Staking rewards and other earned ETH are ordinary income at receipt, regardless of how long you later hold the coins.

- High earners may owe an extra 3.8% Net Investment Income Tax once modified income passes $200,000 single or $250,000 married filing jointly. Capital gains count, and staking income generally lands in the net investment bucket for passive stakers too.

- State tax can apply on top; most states tax crypto gains as ordinary income, while a handful (Texas, Florida, Wyoming, and others) have no state income tax at all.

Here are the 2026 federal long-term capital gains brackets that apply to ETH held more than one year:

| 2026 long-term rate | Single / MFS | Married Filing Jointly | Head of Household |

|---|---|---|---|

| 0% | Up to $49,450 | Up to $98,900 | Up to $66,200 |

| 15% | $49,451–$545,500 | $98,901–$613,700 | $66,201–$579,600 |

| 20% | Above $545,500 | Above $613,700 | Above $579,600 |

Short-term gains stack on top of your other income and get taxed at whatever ordinary bracket they land in. The 2025 tax law (the One Big Beautiful Bill Act) made the current 10% through 37% ladder permanent, so these brackets are a stable planning baseline rather than something scheduled to expire.

Notice the 0% band. A married couple with total taxable income under $98,900 in 2026, including the gain itself, pays zero federal tax on long-term ETH gains. Lower-income years are genuine opportunities to realize gains for free.

The same $44,000 gain realized inside a year by someone in the 32% bracket costs about $14,080. Holding past the one-year mark saved roughly $7,500 here, before state tax even enters the picture.

Ethereum staking taxes

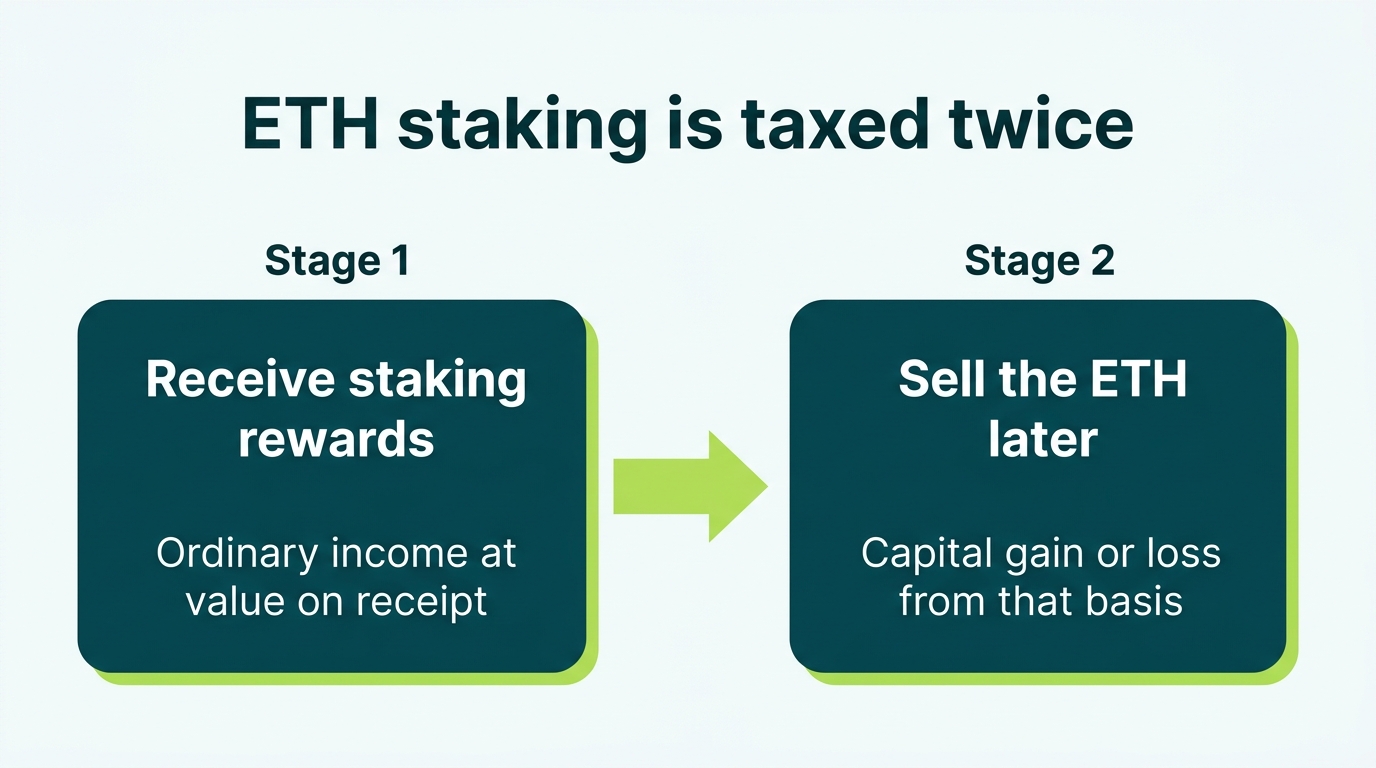

Staking rewards are taxed twice, in two separate layers, and the order matters. This is the defining Ethereum tax topic, and it applies whether you run a validator, stake through Coinbase or Kraken, or hold a liquid staking token.

- Income at receipt. Under Revenue Ruling 2023-14, each staking reward is ordinary income at its fair market value when you gain "dominion and control" over it. A reward worth $50 on the day you can access it is $50 of income, even if ETH drops the next week.

- Capital gain or loss at sale. That $50 becomes the reward's cost basis with a fresh holding-period clock. Sell it later for $70 and you have a $20 capital gain; sell for $30 and you have a $20 loss.

A validator earning rewards daily creates hundreds of tiny income events per year, each with its own date, dollar value, and basis. That is not hand-trackable, which is why staking is where most self-prepared Ethereum returns fall apart. One well-known couple, the Jarretts, sued the IRS arguing rewards should not be income until sold; the courts have not blessed that position, and Revenue Ruling 2023-14 is the standard the IRS enforces today.

When exactly are rewards taxed? The dominion-and-control question

Rewards become income when you can actually access, sell, or withdraw them, and on Ethereum that moment depends on how you stake. Since the Shapella upgrade enabled withdrawals in April 2023, the mechanics look like this:

- Exchange staking (Coinbase, Kraken). Rewards are usually income when the platform credits them to your account and you can sell or withdraw. The exchange's reward history is your record, and platforms report staking income on Form 1099-MISC once it passes $600.

- Solo validators. Consensus-layer rewards above 32 ETH sweep automatically to your withdrawal address every few days, a clean receipt point. Execution-layer income (priority fees and MEV) arrives at your fee recipient address immediately, which is also clearly income on arrival.

- Exit queues and lockups. Rewards you genuinely cannot withdraw yet, because they sit behind an exit queue or a protocol lockup, are arguably not income until they become accessible. This is the strongest deferral argument, but it is narrow: once withdrawals are open, "I just did not claim them" does not defer income.

The defensible approach is to pick a consistent, documented recognition method, recognize income no later than the point you could withdraw, and keep the per-reward valuation records to prove it. If staking is a large share of your activity, our full guide to Ethereum staking taxes walks through solo, pooled, and exchange staking in detail.

Liquid staking taxes: stETH, wstETH, rETH, and cbETH

Liquid staking creates two separate tax questions, and most guides blur them together: what happens when you enter the position, and what happens while you hold it.

Entering and exiting. Swapping ETH for stETH, rETH, or cbETH is unsettled territory. The conservative position treats it as a crypto-to-crypto disposal: you exchanged one asset for a different one, so you realize gain or loss on your ETH at that moment. The aggressive position treats the mint as a deposit, because the token is a receipt for ETH you still beneficially own. The IRS has not ruled. What matters is consistency: if you treat the entry as non-taxable, the exit must be treated the same way, and your basis in the ETH carries through the position.

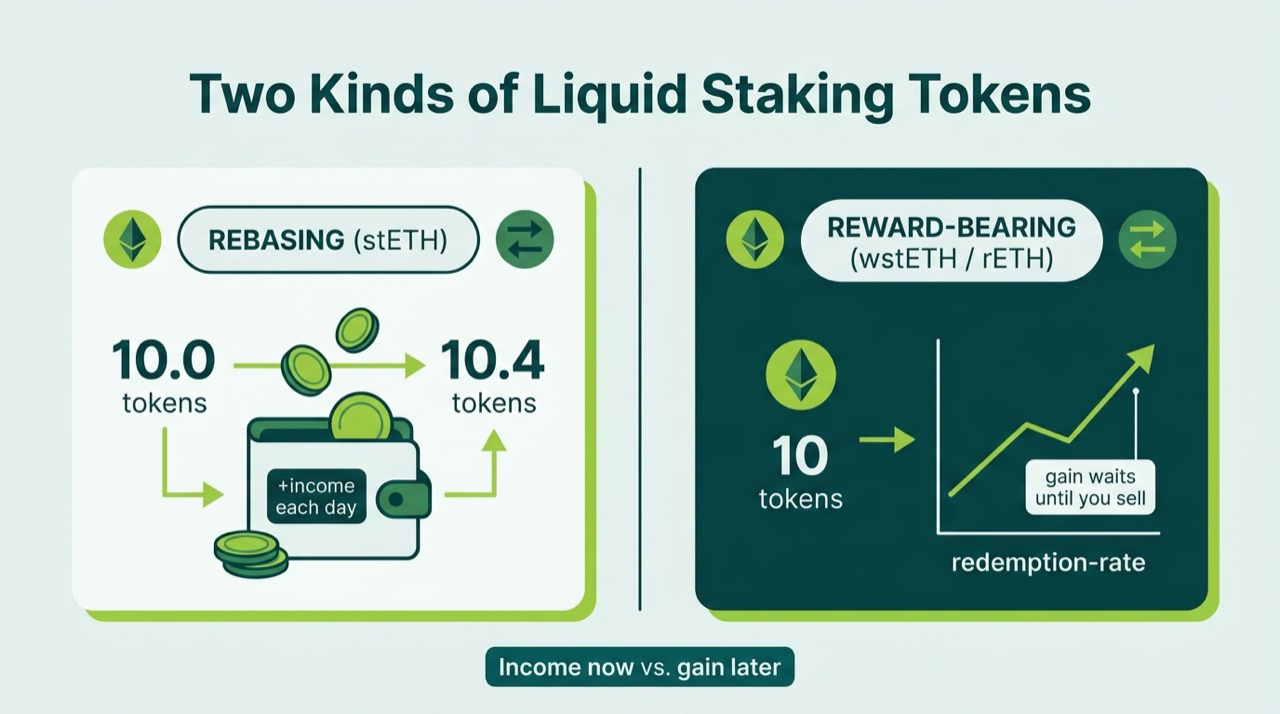

Holding stETH: the rebasing problem. Lido's stETH pays rewards by increasing your token balance every day. Each rebase puts new tokens in your wallet that you can sell immediately, which fits the dominion-and-control standard for ordinary income. That means a stETH holder plausibly has 365 small income events per year, each needing a dollar value. The alternative position, deferring everything until you sell, is simpler but harder to square with Revenue Ruling 2023-14.

Holding wstETH, rETH, or cbETH: value accrual instead. These tokens do not rebase. Your balance stays fixed while each token's redemption value climbs. No new tokens arrive, so there is a reasonable argument that no income accrues until you dispose of the position, at which point the staking yield shows up inside your capital gain. That structural difference, income every day versus gain at the end, is why the wrapped and value-accruing tokens are often the cleaner choice for taxable accounts.

Restaking and EigenLayer taxes

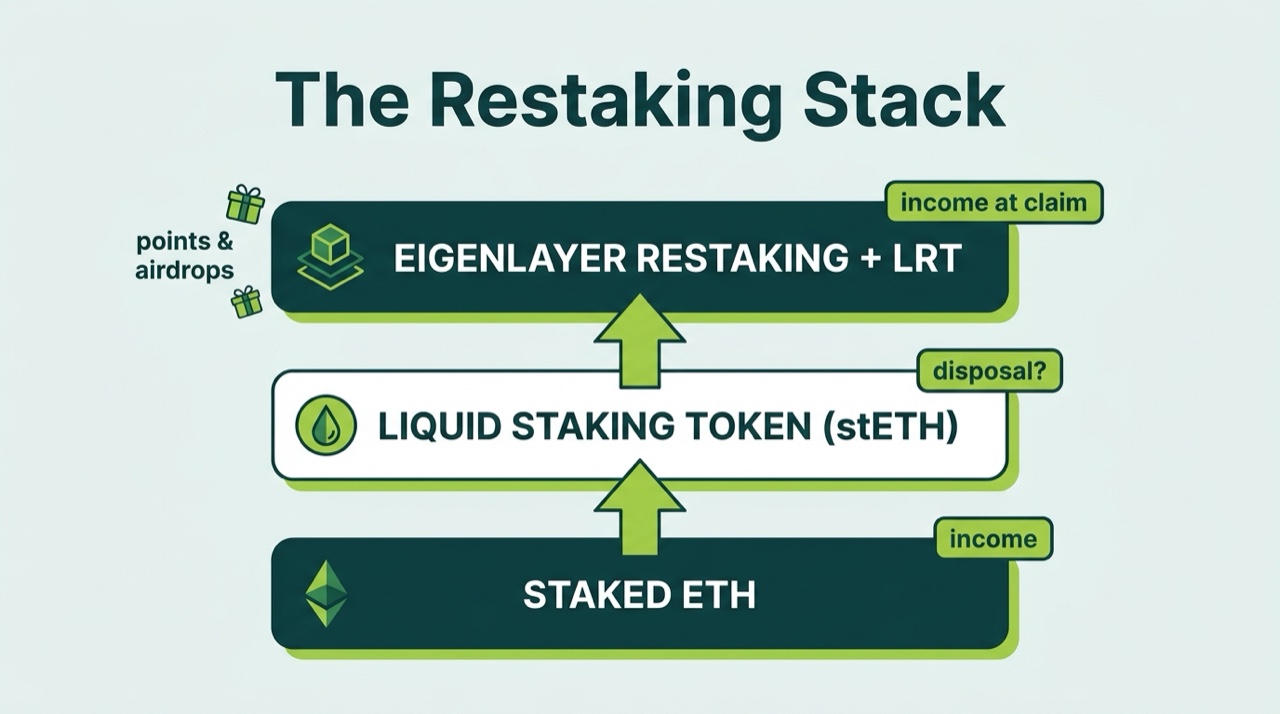

Restaking stacks new gray areas on top of the staking rules, and almost no tax guidance addresses it directly. The building blocks:

- Depositing into EigenLayer (natively or with an LST) is best analyzed like any other deposit-versus-disposal question. Depositing a token you still beneficially own, with a claim to withdraw the same asset, leans non-taxable. Receiving a different liquid restaking token (an LRT like ezETH or eETH) in exchange leans toward a disposal under the conservative view, same as liquid staking entry.

- Restaking rewards and AVS payouts are ordinary income at fair market value when you can claim or control them, the same Revenue Ruling 2023-14 logic that governs regular staking.

- Points and airdrops. Points themselves have no clear value and are generally not income when earned, but the airdropped token that follows (EIGEN, for example) is ordinary income at its value when you receive and can transfer it. Claim timing matters: tokens locked at launch are a genuine deferral argument until transfer restrictions lift.

- Slashing losses are murky. A capital loss usually requires a disposal, and ETH destroyed by a slashing event may not qualify cleanly. Document the facts and get advice before claiming it.

Liquid staking entries and exits, rebasing income, LRTs, and airdrop timing all get full treatment in our guide to liquid staking and restaking taxes.

Staking, stETH, and a wallet full of micro-rewards?

Daily rebases and validator sweeps create hundreds of income events a year. We reconcile all of it into clean, CPA-ready figures with defensible positions.

Are Ethereum gas fees tax deductible?

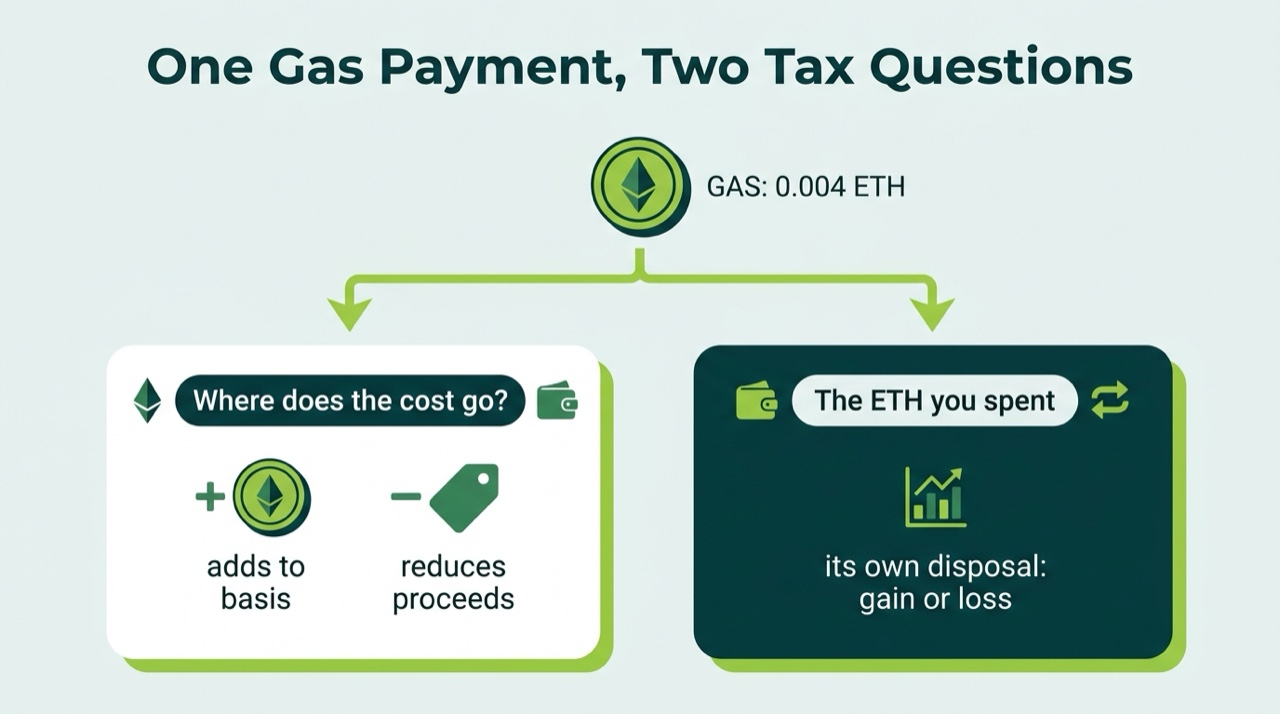

Often yes, but not as a line-item deduction. Gas fees work through cost basis and proceeds, and every gas payment is also a tiny disposal of the ETH used to pay it. Both halves matter:

- Gas to acquire an asset adds to its cost basis. Pay $30 of gas to buy a token and your basis in that token is the purchase price plus $30, which shrinks your future gain.

- Gas to sell or dispose of an asset reduces your proceeds. Pay $25 of gas to sell a token for $1,000 and your reported proceeds are $975, which also shrinks the gain.

- Gas on personal transfers is generally lost. Moving ETH between your own wallets is not a disposal of the transferred coins, and the gas on a personal-use transfer is generally not deductible for individual investors. Some preparers add transfer gas to the moved asset's basis; that position is aggressive, so treat it carefully.

- Failed transactions still burn gas. The ETH is gone, but with no acquired asset to attach it to, there is no clean deduction for an individual investor. It is one of Ethereum's small tax injustices.

- Business use is different. If you transact on Ethereum as a business (a Schedule C trader in NFTs, a protocol operator), gas can be an ordinary business expense.

The disposal side is easy to forget. If you bought ETH at $1,500 and spend 0.01 ETH on gas when the price is $4,000, you disposed of 0.01 ETH at a $25 gain. Individually trivial, but an active wallet makes hundreds of these, and the IRS expects them on Form 8949. Good software handles gas automatically; our crypto tax software guide compares how the major tools treat it, and our dedicated guide to Ethereum gas fee taxes covers every scenario, including failed transactions and contract deployments.

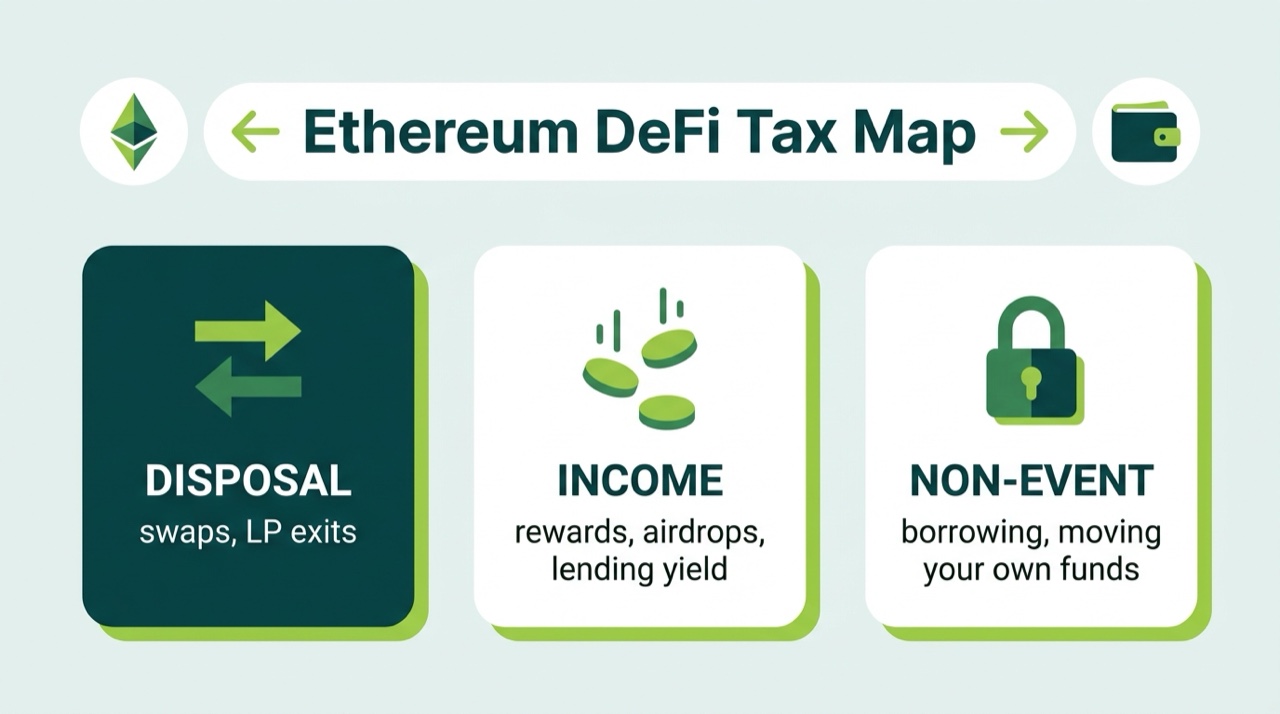

DeFi on Ethereum: swaps, wrapping, lending, and Layer 2 bridges

Almost everything you do in Ethereum DeFi is either a disposal or income; the hard part is knowing which. The quick map:

- Token swaps on Uniswap or any DEX are disposals of the token you give up. Capital gain or loss, every time.

- Wrapping ETH into wETH is the most defensible "non-taxable change of form" in crypto: wETH is the same asset in an ERC-20 jacket, redeemable one to one. Many practitioners treat wrap and unwrap as non-events, though the conservative view still calls it a swap. Pick a lane and stay in it.

- Lending and borrowing. Supplying ETH to Aave or Compound and receiving interest creates ordinary income as the interest accrues to your control. Borrowing against ETH is not taxable, which is why loans are a popular way to unlock liquidity without selling. Liquidations are forced disposals of your collateral, with gain or loss measured against your basis.

- Liquidity pools. Depositing two tokens and receiving an LP token is likely a disposal of both deposited assets under the conservative view. Fees and farming rewards are income. Exiting the pool is another disposal of the LP token.

- Bridging to Layer 2s. Moving ETH to Arbitrum, Optimism, or Base over the official bridge is generally treated as a self-transfer: same asset, same owner, new network. Third-party bridges that hand you a different derivative token on the far side are harder to defend as transfers and may be disposals. The gas burned to bridge is a disposal either way, and activity on the L2 follows all the same rules as mainnet.

Each of these has edge cases, protocol quirks, and record-keeping traps. Our full guide to Ethereum DeFi taxes works through lending, LPs, airdrops, and bridging with worked examples.

NFT taxes on Ethereum

Buying an NFT with ETH is a taxable disposal of the ETH, before you have sold anything. If you bought 2 ETH at $2,000 and spend it on an NFT when ETH is at $4,000, you have a $4,000 capital gain the moment you mint or buy. The rest of the lifecycle follows suit:

- Selling an NFT for ETH or stablecoins is a disposal of the NFT: proceeds minus your basis (purchase price plus mint gas).

- Creating and selling your own NFTs is ordinary income, and self-employment tax if it is a business.

- Collectibles risk. The IRS has signaled that some NFTs may be taxed as collectibles under a look-through test, which carries a higher 28% maximum long-term rate. Art-backed NFTs are the most exposed.

Marketplace royalties, wash-trading traps, and worthless NFT write-offs are covered in our guide to Ethereum NFT taxes.

Spot Ethereum ETF taxes: ETHA, FETH, and staking inside the wrapper

Spot Ether ETFs are taxed almost like holding ETH directly, with a few edges that matter. Since they began trading in July 2024, funds like ETHA and FETH have become the default ETH exposure in brokerage accounts.

- They are grantor trusts. The tax code looks through the wrapper: you are treated as owning your fractional share of the trust's ETH. Selling shares is a capital gain or loss at the same 2026 rates as ETH itself, tracked by your broker on a standard 1099-B.

- Sponsor fees create tiny pass-through sales. The trust sells slivers of ETH to pay its management fee, and a proportional piece of each sale passes through to you on the fund's year-end grantor trust tax statement. Small, but reportable.

- Staking has arrived inside the ETFs. Regulators cleared the way in 2025 for funds to stake a portion of their ETH. Those rewards pass through to shareholders as income on the year-end statement, so an "ETF-only" investor can now have staking income to report without ever touching a wallet.

- The wash sale rule applies to ETF shares. They are securities. Sell at a loss and rebuy within 30 days and the loss is disallowed, unlike wallet ETH under current law.

- In IRAs, the ETF wins. An Ether ETF inside a retirement account grows tax-deferred or tax-free, staking passthrough included, which self-custodied ETH cannot easily replicate.

Cost basis and the wallet-by-wallet rule

Your cost basis is what you paid for the ETH, including acquisition fees and gas. Get it wrong in one direction and you overpay; get it wrong in the other and you underreport to an agency that now has your sale proceeds on file. Two rules make Ethereum basis harder than it looks:

- Basis is now tracked per wallet. Since January 1, 2025, under Revenue Procedure 2024-28, cost basis must be tracked wallet by wallet and account by account. Pooling every wei you own into one universal average is no longer allowed. The IRS offered a one-time safe harbor to allocate existing basis across wallets as of that date; if you never did that allocation, do it before your next sale.

- Staking and DeFi create swarms of micro-lots. Every staking reward, rebase, and airdrop is its own lot with its own date, dollar value, and holding-period clock. Within each wallet, FIFO is the default ordering unless you specifically identify lots at or before the sale, documented. For a holder with 2017 ETH and 2025 rewards in the same wallet, lot selection can be the difference between a small gain and an enormous one.

Transfers are the other trap. Moving ETH from your wallet onto an exchange is not taxable, but the exchange has no idea what you originally paid. When you later sell there, the broker may report your basis as zero, and the burden of proving the real number falls on you. Rebuild the trail from old exchange exports and the public blockchain record now, not during an audit.

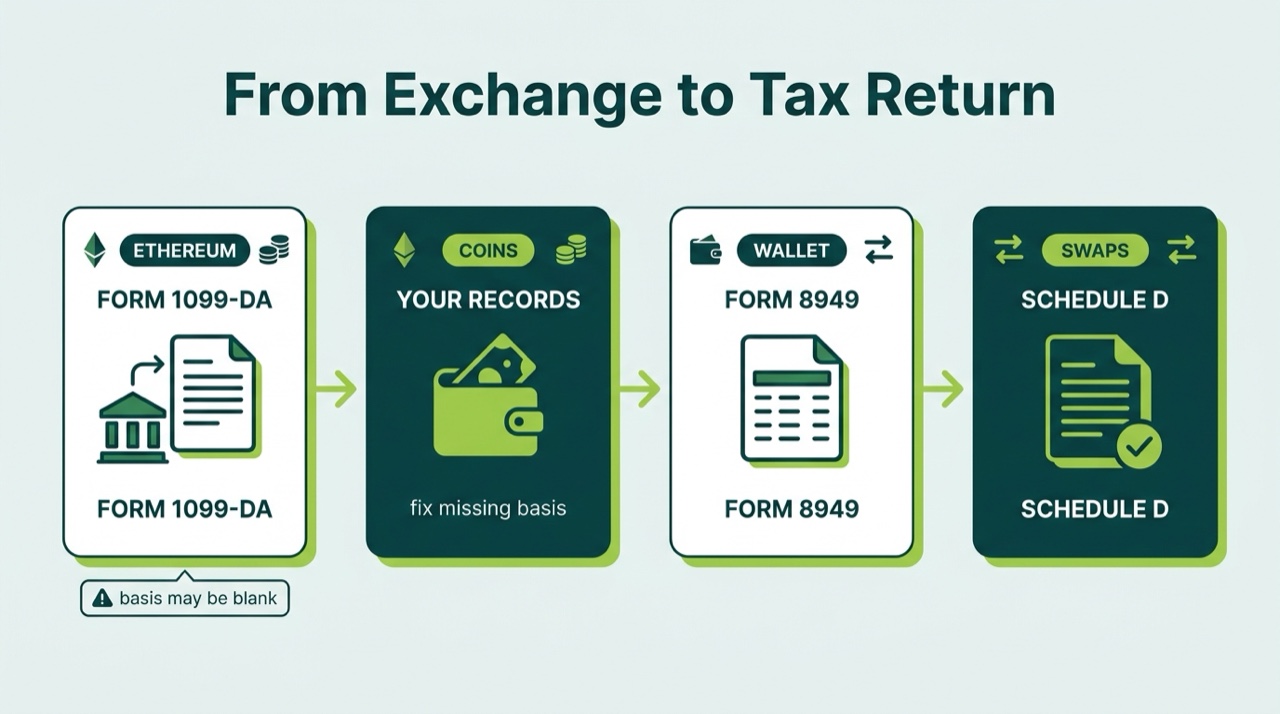

Form 1099-DA and how to report Ethereum on your return

Reporting is where Ethereum taxes changed the most. Starting with tax year 2025, US brokers must file Form 1099-DA, reporting your gross proceeds from ETH sales to both you and the IRS. The first forms arrived in early 2026, and cost basis reporting expands for 2026 sales of covered lots. If you sold ETH on Coinbase, Kraken, or any other US platform, the IRS already has a copy. Our full Form 1099-DA guide covers the form line by line.

Here is the filing flow for a typical Ethereum holder:

- Collect every 1099-DA from each exchange where you sold, plus 1099-MISC forms for staking income over $600.

- Fix the basis. If you transferred ETH into an exchange before selling, the broker may report zero or missing basis. Supply your true acquisition cost so you are not taxed on the entire sale price.

- List each disposal on Form 8949: every sale, swap, spend, and gas disposal, with dates, proceeds, cost basis, and gain or loss, split into short-term and long-term.

- Total everything on Schedule D, where gains and losses net against each other.

- Report ETH income on Schedule 1 (or Schedule C for a business): staking rewards, airdrops, and payments received in ETH.

- Answer "Yes" to the digital asset question on Form 1040 if you sold, swapped, spent, or received Ethereum during the year.

The $1,100 of rewards is ordinary income on Schedule 1, and the $4,000 gain on the sold ETH is long-term capital gain via Form 8949 and Schedule D. Two buckets, one return, and the reward lots keep their own basis for whenever they are sold.

The wash sale rule, tax-loss harvesting, and lost ETH

Under current law, the wash sale rule does not apply to Ethereum. The rule (IRC Section 1091) disallows a loss when you sell a security and rebuy it within 30 days, and the IRS treats ETH as property, not a security. You can sell ETH at a loss, harvest the deduction, and buy it back immediately. Harvested losses offset your capital gains dollar for dollar, then up to $3,000 of ordinary income per year, with the remainder carried forward indefinitely.

Three caveats keep this honest. First, the rule does apply to spot Ether ETF shares, which are securities. Second, Congress has repeatedly proposed extending the wash sale rule to digital assets, so confirm the current-year law before relying on the gap. Third, the economic substance doctrine gives the IRS a tool against round trips with no real market exposure. Our crypto wash sale guide covers the strategy and its limits.

Lost and stolen ETH follow their own rules. Lost keys are generally not deductible, because nothing was sold or completed; the coins are simply frozen along with their basis. Theft losses from profit-motivated arrangements, like fraudulent platforms and investment scams, can still be deductible under IRS guidance issued in 2025, while personal-use theft losses are not. Exchange bankruptcy claims resolve when distributions arrive, not when the platform freezes. The details are fact-specific; our guide to lost and stolen crypto deductions goes scenario by scenario.

How to reduce your Ethereum taxes legally

- Hold past one year. Long-term rates of 0%, 15%, or 20% beat ordinary rates of up to 37%. For appreciated ETH, patience is the cheapest strategy available.

- Harvest losses in down markets. Sell underwater lots to realize losses that offset gains plus $3,000 of ordinary income, and under current law you can rebuy ETH immediately.

- Mind your bracket. Realizing long-term gains in a lower-income year can land some or all of the gain in the 0% or 15% band, and splitting a large sale across two tax years can keep you under the 20% tier and the 3.8% surtax threshold.

- Pick tax-aware staking structures. Value-accruing tokens (wstETH, rETH, cbETH) concentrate yield into a future capital gain instead of daily income events, and an Ether ETF inside an IRA shelters both gains and staking passthrough entirely.

- Use specific identification. Choosing which lots to sell, documented per wallet, lets you sell high-basis coins first and leave 2017 lots undisturbed until you choose to realize them.

- Donate appreciated ETH. Giving long-held Ethereum to a qualified charity avoids the capital gain entirely and can support a deduction at full fair market value.

- Gift strategically. Gifts within the annual exclusion ($19,000 per recipient in 2026) transfer ETH without tax, and a recipient in the 0% long-term bracket can sell with no federal tax at all.

If your situation spans staking income, DeFi positions, and years of wallets, a crypto tax professional will usually find more than these basics. The rest of our coin-by-coin tax guides cover how the same framework applies to Bitcoin, Solana, and the other assets you might hold alongside ETH.

Want a professional to handle it?

Book a free 15-minute call and we will map out exactly what your Ethereum tax situation needs, from validator rewards to a wallet full of DeFi history.

Book a free 15-min callEthereum tax FAQ

Do you have to pay taxes on Ethereum?

How much tax do you pay on Ethereum?

Are Ethereum staking rewards taxable?

When are ETH staking rewards taxed, at receipt or at withdrawal?

Is converting ETH to stETH or wstETH taxable?

Are Ethereum gas fees tax deductible?

Do you pay taxes on Ethereum if you don't sell?

Does the IRS know about my Ethereum?

How are spot Ethereum ETFs taxed?

Does the wash sale rule apply to Ethereum?

Is bridging ETH to a Layer 2 like Arbitrum or Base taxable?

How do I report Ethereum on my taxes?

The 2025/26 Crypto Tax Guide. Built by former Big 4 accountants.

A printable, step-by-step guide and checklist to reconcile every coin and wallet, recover missing cost basis, and file accurately before the deadline.

- Form 8949, Schedule D, and Schedule 1 walkthroughs

- How to handle staking, DeFi, NFTs, and lost coins

- The $0-basis 1099-DA trap (and how to avoid it)

- FBAR, Form 8938, and foreign exchange reporting