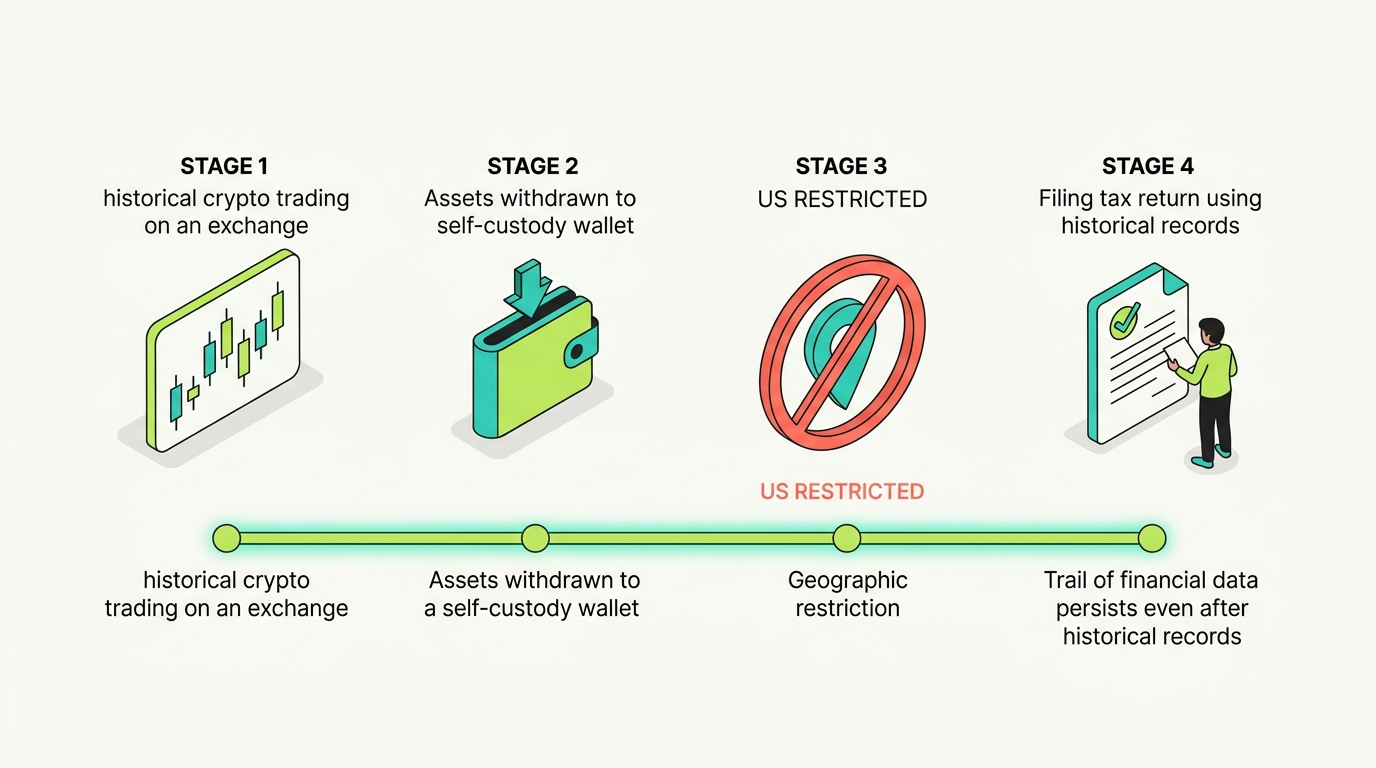

Bybit may be restricted for US users, but your historical Bybit tax trail is still open. That single sentence reframes everything. For years, Bybit was a go-to offshore venue for US traders who wanted deep derivatives markets, perpetuals, options, copy trading, trading bots, and structured Earn products that domestic platforms did not offer. Then the regulatory picture shifted, and the United States landed on Bybit’s restricted list. Ordinary trading access went away. The tax obligations did not.

This is the definitive Bybit tax guide for 2026, written for the audience that actually exists now: former US users reconstructing historical activity, derivative-heavy traders reconciling perpetuals and bots, taxpayers retrieving records from restricted accounts, traders reconciling Bybit with the US exchanges and self-custody wallets they moved assets to, and anyone amending prior-year returns or responding to an IRS inquiry. Most existing Bybit guides still read like a software signup flow: connect an API, upload a CSV, and call it done. That framing leaves the hardest questions, the ones that actually decide whether your return is right, completely unanswered.

If one idea sticks from this guide, let it be this:

A Bybit API connection is not a completed tax return. Derivatives, subaccounts, structured products, rewards, wallet activity, and transfers must all reconcile to one complete transaction ledger.

On a Bybit account, the real work is rarely the arithmetic. It is rebuilding a complete, accurate history out of exports that cap by date, API imports that quietly miss bots and copy trading, a Unified Trading Account where one collateral pool feeds many products, internal transfers that look like sales, derivatives that resist one-size-fits-all classification, and assets that arrived with no cost basis attached.

This guide covers the full landscape of Bybit taxes:

- The current US status, why historical activity is still reportable, and who this guide is for now

- How the IRS treats your activity, what Bybit does and does not report, and the Form 1099-DA reality

- How to retrieve and reconstruct records, and why API imports are not complete

- The Unified Trading Account, perpetuals, futures, options, TradFi perpetuals, margin, bots, copy trading, Earn, and structured products

- Card, Pay, P2P, Bybit Alpha, and Web3 wallet activity

- Missing cost basis, wallet- and account-specific basis rules, DAC8 and CARF, FBAR and Form 8938, and audit readiness

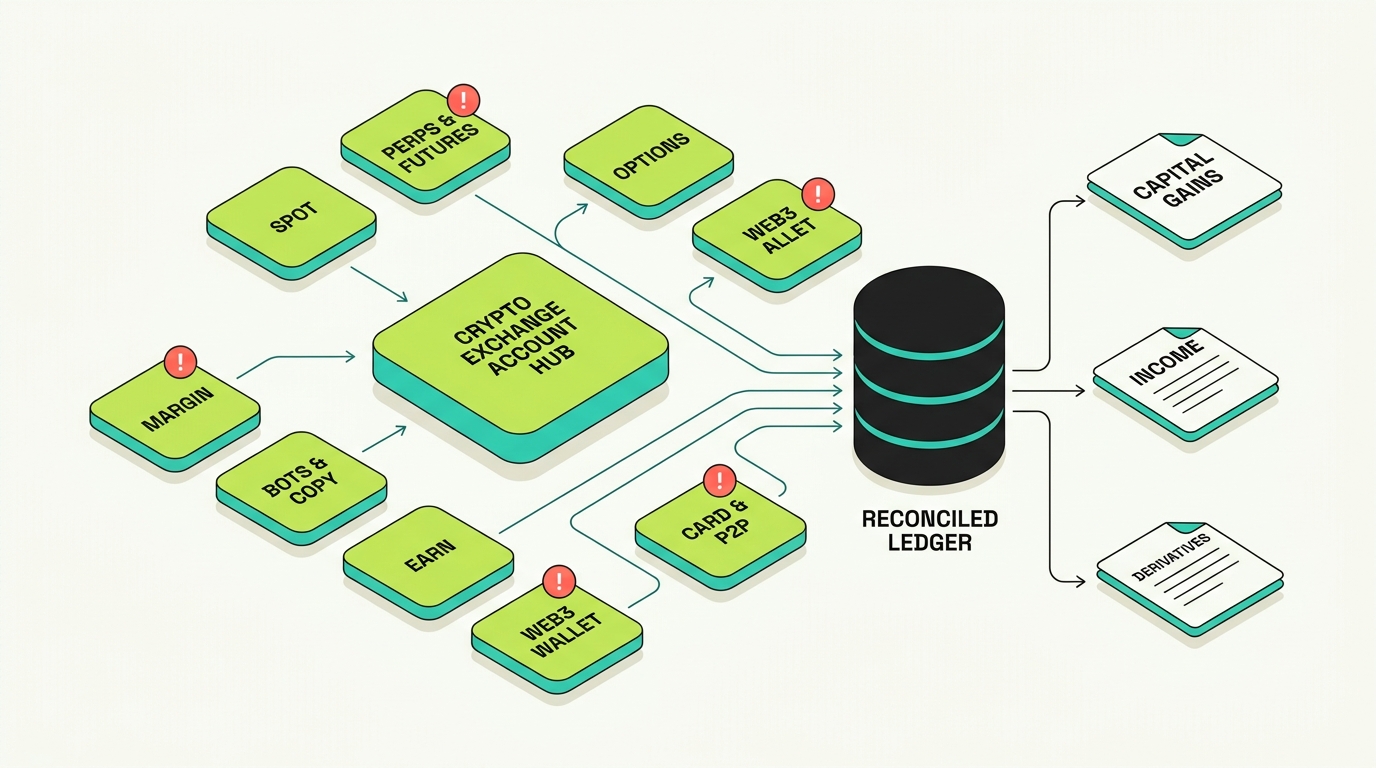

The way Bybit’s products feed into a single tax picture is the whole challenge in one image: many distinct activity types, one reconciled ledger, and a handful of tax outputs.

Important Update for US Bybit Users

Before a single number, the US status has to be clear, because it changes who this guide is for and what you actually need to do.

Is Bybit Currently Available in the United States?

In practical terms, no. Bybit’s restricted-jurisdiction notice lists the United States, and ordinary US access to spot, derivatives, and Earn products is no longer available the way it once was. If you are a US taxpayer reading this, you are almost certainly here to deal with activity that already happened, not to open a new account. This guide is written for that reality, and it does not explain VPN use, false residency information, or any other method of bypassing geographic restrictions.

Who Should Use This US Bybit Tax Guide?

The Bybit audience has shifted. This guide is built for:

- Former US customers reporting historical transactions.

- Derivative-heavy traders reconciling perpetuals, futures, options, and bots.

- Users retrieving historical data from a restricted or limited account.

- Taxpayers who transferred assets off Bybit and need to trace basis to where they sold.

- Users amending previous returns that left Bybit activity off.

- Taxpayers responding to an IRS notice or preparing audit support.

- Executors, trustees, or businesses reconstructing an account.

Does Bybit’s US Restriction Eliminate Previous Tax Obligations?

No. This is the point that trips up the most people. A platform restricting US access does not retroactively cancel taxes on activity that already occurred. Every taxable event you triggered while you were active (each sale, trade, derivative close, fee paid in an appreciated token, and reward received) remains reportable. If anything, the restriction raises the stakes, because it makes the records harder to retrieve while leaving the obligation fully intact.

What Former US Users Should Preserve Now

If you still have any access, preserve everything immediately: full exports, the wallet addresses you used, trade confirmations, subaccount lists, API records, and screenshots of balances. Access for restricted accounts can change without warning, and a record you cannot retrieve later is a basis you cannot prove.

Bybit may be restricted for US users, but your historical tax trail remains open.

What This Article Will Not Explain

To be explicit: this guide does not cover VPN usage, false residency information, geographic circumvention, or any method of evading exchange controls. Its purpose is accurate historical reporting, not continued access.

What Is Bybit?

To reconstruct Bybit activity accurately, you first need to understand how broad the platform is. Bybit was never a single buy-and-sell app. It is a sprawling ecosystem of products, each generating its own records and its own tax questions, and several of them have no clean equivalent on a US spot exchange.

Bybit’s Operating Entities

Bybit operates through more than one legal entity, including Bybit EU and other local entities, and the entity matters for tax and information-reporting purposes. A Bybit EU account should not automatically be treated the same as an account held through a different Bybit entity. Before drawing conclusions about reporting, identify which entity you actually used.

Funding Account and the Unified Trading Account

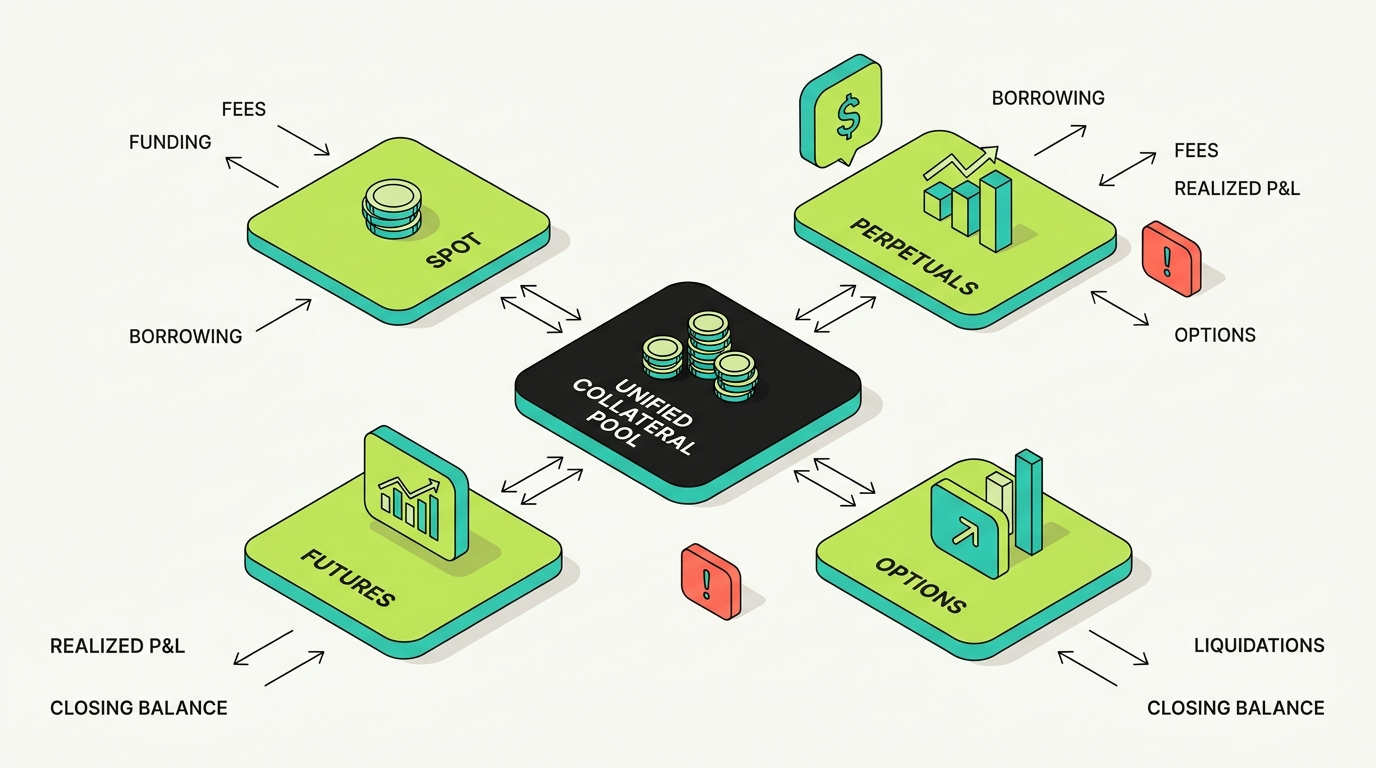

Bybit separates a Funding Account from the Unified Trading Account (UTA). The Funding Account holds assets for deposits, withdrawals, and certain products, while the UTA is where spot, spot margin, perpetuals, dated futures, and options all draw on a shared pool of collateral. This shared-collateral design is central to why Bybit reconciliation is harder than it looks.

Spot Trading

The spot market is buying and selling a wide range of cryptocurrencies. Spot trades are the most familiar taxable events, but the number of pairs and the volume of trades make completeness a challenge.

Perpetuals, Futures, and Options

Bybit is best known for derivatives: USDT perpetuals, USDC perpetuals, inverse perpetuals, dated futures, and options. Realized profit and loss, funding payments, fees, liquidations, and settlement all matter, and the tax characterization of these offshore derivatives is fact-specific rather than automatic.

Margin Trading

Spot margin lets users borrow against assets in the UTA to amplify positions. Borrowing itself is generally not a sale, but the trades made with borrowed funds, the interest paid, and any liquidation all carry tax consequences that must be tracked separately from spot.

Trading Bots and Copy Trading

Bybit is heavily associated with automated trading: spot and futures grid bots, DCA bots, and copy trading. A single bot strategy can execute hundreds or thousands of trades, each a separate taxable event, and copy trading layers on follower and lead-trader rewards. Both are data-heavy and commonly missed.

Bybit Earn and Structured Products

Bybit Earn bundles products such as Easy Earn, On-Chain Earn, Dual Asset, and other structured offerings. These do not all share the same economic structure, so they should not automatically receive the same tax label.

Bybit Card, Pay, and P2P

Bybit Card and Pay can involve spending appreciated crypto, automatic conversion, cashback, and rewards, while P2P involves direct crypto-for-fiat trades with other users. Each can carry different tax consequences.

Bybit Alpha and Web3 Wallet

Bybit Alpha bridges centralized balances into on-chain token trading, and Bybit offers self-custody wallets where you control the keys. These create a second data environment, on the public blockchain, that the exchange API alone does not fully capture.

Subaccounts and Institutional Accounts

Bybit lets users create subaccounts to separate strategies or bots, and it supports institutional and professional accounts. Subaccounts are a frequent blind spot, because activity siloed in a subaccount may never get imported if you only connect the main account.

Do You Owe Taxes on Bybit?

Owning crypto is not a taxable event. What creates a tax bill is an action, and Bybit offered many of them. Knowing which actions count is the groundwork for everything that follows.

IRS Treatment of Cryptocurrency

Under IRS Notice 2014-21, cryptocurrency is property for tax purposes, not currency. Almost everything about Bybit taxes flows from that one classification. When you dispose of property you have a capital gain or loss; when you receive property as a reward you have ordinary income. Every Bybit scenario, from a spot sale to a perpetual close to a card purchase, resolves to one of those two, sometimes with derivative-specific rules layered on top.

Capital Gains

Dispose of crypto for more than you paid and the difference is a capital gain. The rate depends on how long you held it. A holding period of a year or less makes the gain short-term, taxed at your ordinary income rate of 10 to 37 percent. More than a year makes it long-term, taxed at the preferential 0, 15, or 20 percent brackets. Because the clock runs per lot, holding period can dramatically change the bill on a large Bybit position.

Ordinary Income

Some Bybit activity is taxed as ordinary income at the moment you receive it, valued at fair market value:

- Staking and On-Chain Earn rewards on supported assets.

- Easy Earn and savings income.

- Launchpool, airdrop, referral, and promotional rewards.

- Certain reward elements of copy trading and other programs.

This income is taxed at your marginal rate. The timing rule is what matters: a reward becomes income the instant you gain dominion and control over it, valued in dollars at that moment. The capital gains system only re-enters later, when you sell those reward coins and account for the price change since receipt.

Why Derivatives Need Their Own Analysis

Derivative profit and loss is taxable, but the character (capital or ordinary, short-term or long-term, mark-to-market or not) is not automatic for offshore crypto contracts. This is the single biggest place where generic guides go wrong, and it gets its own detailed section below.

Taxable Events

On Bybit the events that most often trigger tax are selling crypto, trading one crypto for another, converting to a stablecoin, paying fees with an appreciated token, closing a perpetual or futures position, option exercise or expiration, margin liquidation, spending crypto with the card, P2P sales, and receiving rewards. At each point the IRS expects a number from you: a gain, a loss, or income.

Non-Taxable Events

Not everything is taxable. Buying crypto with fiat, holding it, transferring between your own wallets, moving funds between your own Bybit accounts and subaccounts, posting collateral, and borrowing are generally not taxable by themselves. These actions still affect your records, because basis has to follow the asset, but they do not by themselves create a tax bill.

Does Bybit Report to the IRS?

This is where Bybit differs sharply from a US broker, and where the most dangerous assumptions live.

What Information Bybit Retains

As a centralized exchange, Bybit holds records of your trades, deposits, withdrawals, derivative activity, and rewards while your account is active, and it collected identity information through KYC. But holding records is not the same as filing US tax forms, and Bybit’s offshore status means it generally does not send US information returns the way a domestic broker does.

Does Bybit Issue US Tax Forms?

Generally no. Bybit does not issue Form 1099-MISC or Form 1099-DA to US users in the way a US broker does. There is typically no form to download and no matching copy flowing to the IRS tied to your Social Security number. That absence is exactly what creates the trap.

Does Bybit Issue Form 1099-DA?

There is no current official Bybit publication confirming that its main offshore platform issues US customers a Form 1099-DA, and given the US-restricted status, you should not assume one is coming. Form 1099-DA is a US broker form for reportable digital asset dispositions beginning with 2025 transactions. The realistic 1099-DA scenario for a former Bybit user is receiving one from another exchange after transferring assets there and selling.

Why You May Receive No Bybit Tax Form

If you are a US user, the most likely outcome is that you receive nothing from Bybit at all. No form does not mean no obligation. It means the entire record-keeping and reporting burden sits with you.

Public Blockchain Records and Transfers to Regulated Exchanges

No form is not the same as no visibility. The IRS can still surface offshore activity through several channels:

- On-chain analytics. Transfers between Bybit and US exchanges or known wallets are traceable on public blockchains.

- US exchange reporting. When you move funds to a US broker and sell, that broker reports proceeds on a 1099-DA, creating a thread the IRS can pull.

- International information sharing. Cross-border data exchange between tax authorities, including DAC8 and CARF, continues to expand.

How to Reconcile Bybit History With a 1099-DA Received Elsewhere

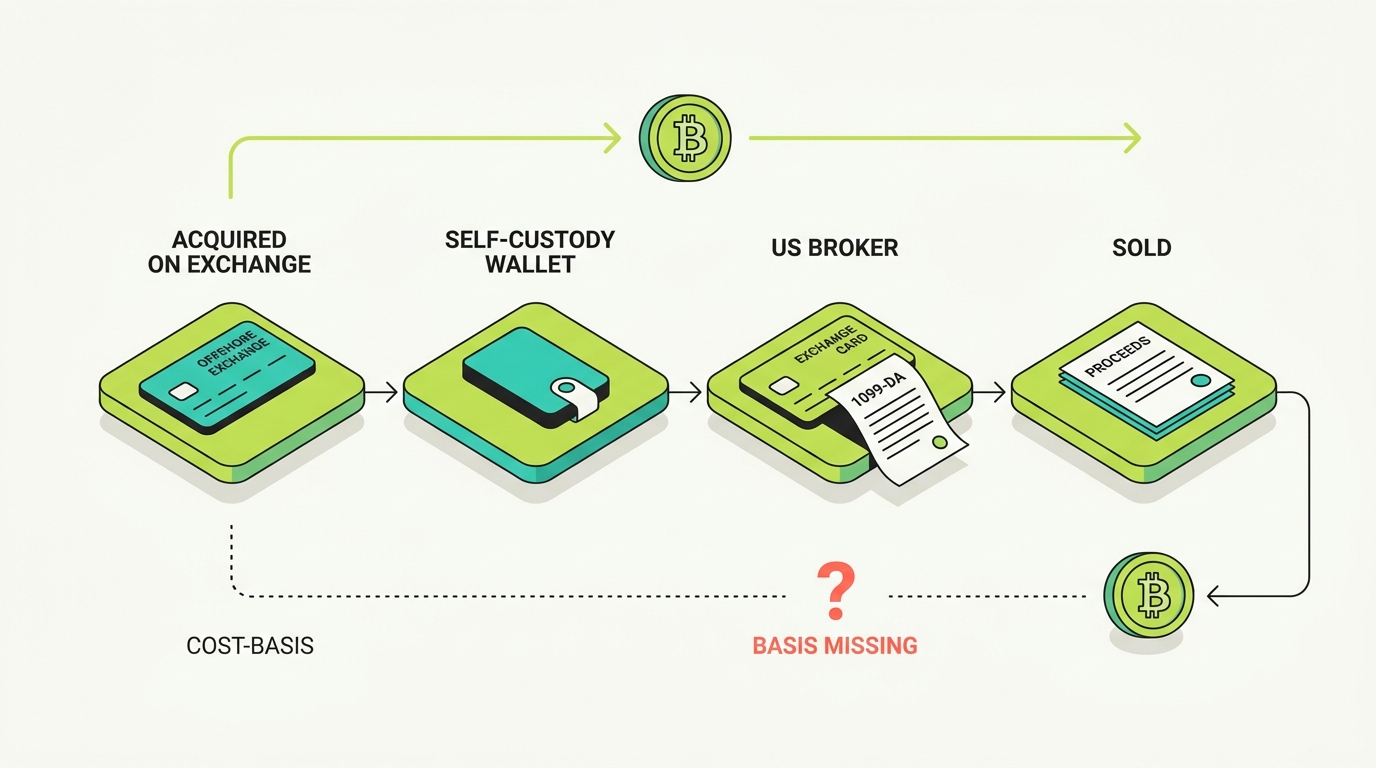

Here is the journey that catches people: you bought an asset on Bybit, transferred it to a self-custody wallet, deposited it into Coinbase or Kraken, and sold it there. The US broker issues a 1099-DA reporting the proceeds, but without your Bybit acquisition history, so the basis may show as missing. Reconciling means supplying that original Bybit basis so your Form 8949 shows the real gain, not the full proceeds.

Understanding the Unified Trading Account

The Unified Trading Account is the structural heart of Bybit taxes, and it is where most reconciliation goes wrong. Competing guides usually define it in a sentence and move on. It deserves more.

What the UTA Combines

In a Unified Trading Account, spot, spot margin, perpetuals, dated futures, and options all share a single collateral pool. A single asset can serve as collateral across products, so a position in one product can affect the available balance for another without a clean transfer between separate wallets. That is convenient for trading and confusing for tax software.

Cross-Collateral, Isolated, Cross, and Portfolio Margin

The UTA supports different margin modes (isolated, cross, and portfolio margin) that change how collateral is shared and how risk is calculated. The mode does not change the underlying tax events, but it changes how balances move, which affects how easy it is to misread an internal collateral shift as a taxable disposal.

Why UTA Balance Changes Get Misclassified

Because one pool feeds many products, the UTA produces balance changes from deposits, withdrawals, borrowing, interest, fees, funding, realized P&L, unrealized P&L, and liquidations, often without an obvious one-to-one trade behind each movement. Tax software can misread these as zero-basis deposits, phantom sales, or duplicate transfers. Untangling them is core to a correct Bybit return.

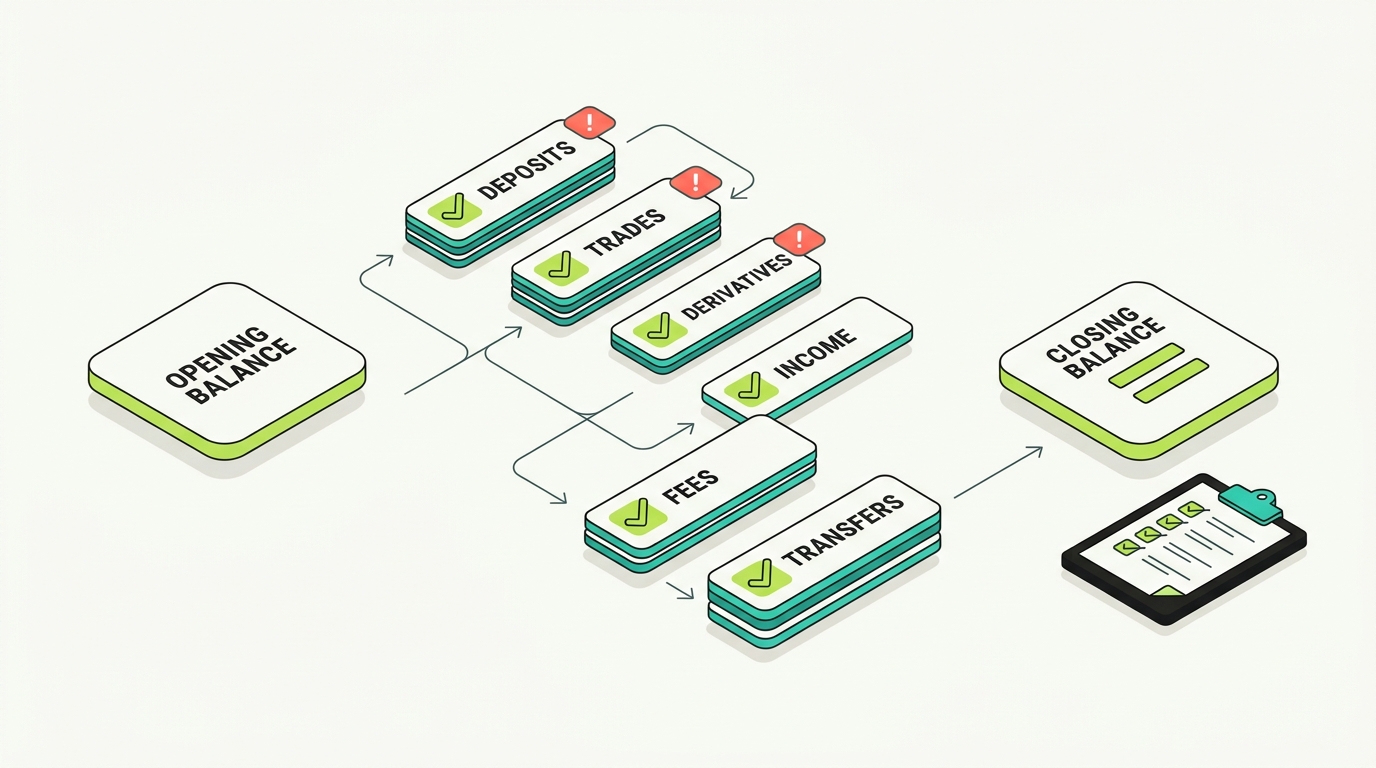

Reconciling the UTA

The reliable approach is a balance roll-forward: start from an opening balance, layer in every category of activity, and confirm you arrive at the actual closing balance. If you cannot tie out, something is missing or miscategorized. The UTA makes this discipline mandatory rather than optional.

Bybit Spot Trading Taxes

Spot trading is the most familiar part of a Bybit return, and the foundation for everything else.

Selling Crypto for Fiat

Selling crypto for fiat is a straightforward disposal. Your gain or loss is the proceeds minus your adjusted cost basis, and the holding period sets the rate.

Crypto-to-Crypto Trades

Trading one cryptocurrency for another is a disposal of the coin you gave up, even though no US dollars are involved. This is the single most overlooked category, because it does not feel like a sale. Each trade needs a US dollar value at the moment of the trade.

Stablecoin Trades and Conversions

Converting crypto into USDT or USDC is a disposal of the crypto you converted. Because so much Bybit activity, including derivatives collateral, runs through stablecoins, these dispositions accumulate quickly.

Fees and Partial Fills

Trading fees can affect the basis or proceeds of the underlying transaction, partial fills create multiple lots, and canceled or unfilled orders are not taxable events. All of this needs to be captured cleanly.

Example: Trading ETH for USDT on Bybit

You acquired 2 ETH for 4,000 dollars total (2,000 dollars each). Months later you trade them for USDT when ETH is worth 2,600 dollars each, with a small trading fee. You disposed of 2 ETH for 5,200 dollars of value, against a 4,000 dollar basis, for a 1,200 dollar capital gain (reduced slightly by the fee). The USDT you received takes a new basis equal to its value at receipt. The trade is taxable even though you never touched US dollars.

How Bybit Derivatives Are Taxed

This is the section generic guides get wrong, and the one most likely to change your tax outcome. Bybit is a derivatives venue first, so this deserves real depth.

Why There Is No Universal Answer

There is no single rule that correctly taxes every Bybit perpetual, future, and option. You should not automatically apply the favorable Section 1256 treatment to all of them, and you should not automatically assume they all fall outside Section 1256 either. The correct treatment depends on the exact instrument, the venue and contract terms, your status as an investor or trader, the settlement mechanics, and whether the contract meets the statutory Section 1256 definition.

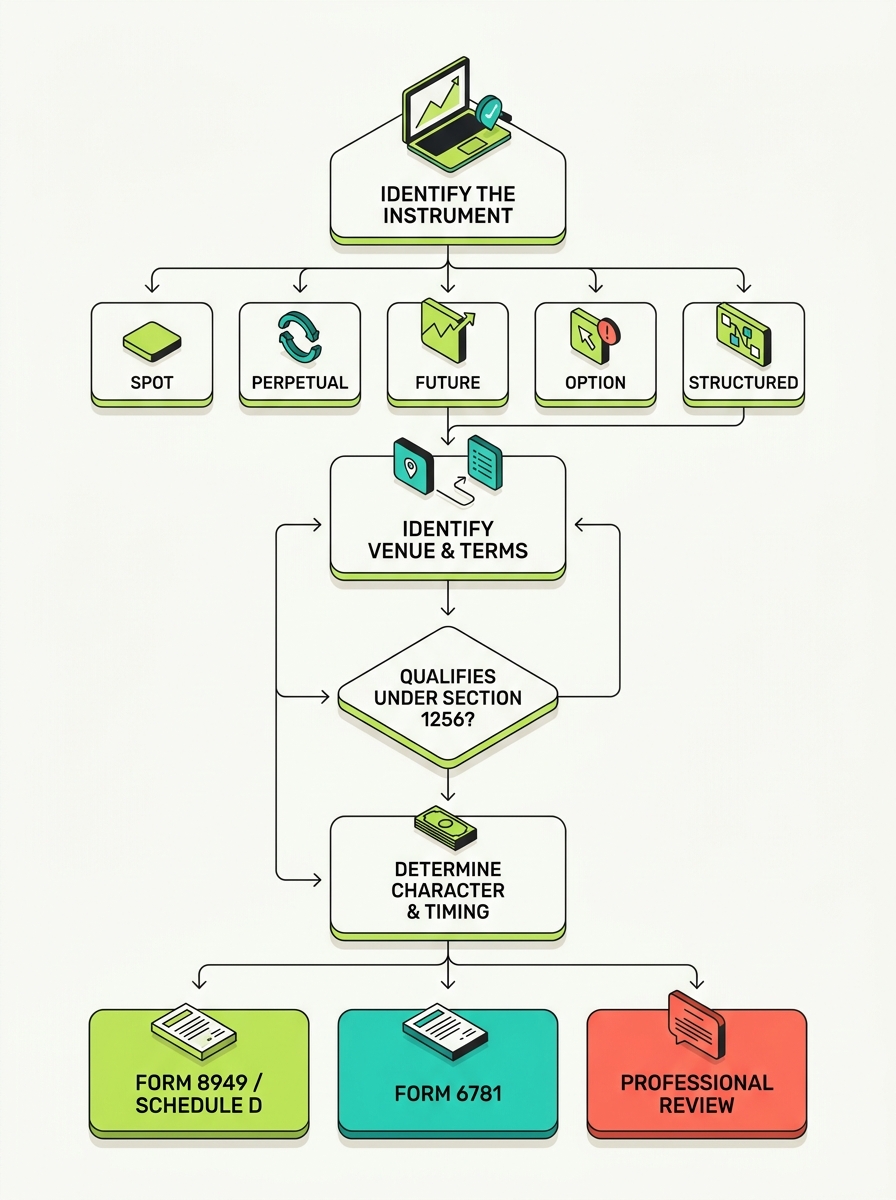

Step 1: Identify the Instrument

Start by naming exactly what you traded: a spot asset, a perpetual swap, a dated future, an option, a leveraged token, or a structured product. These are not interchangeable for tax purposes.

Step 2: Identify the Venue and Contract Terms

Note the issuing and trading entity and the specific contract terms, including settlement asset and mechanics. Offshore contracts and contracts on regulated venues can be treated differently.

Step 3: Determine Whether It Qualifies Under Section 1256

Section 1256 contracts receive mark-to-market treatment and the 60% long-term / 40% short-term split, reported on Form 6781, with open positions treated as sold at year end. Qualification turns on meeting the statutory definition, which offshore crypto derivatives do not automatically satisfy. This determination should not be made casually.

Step 4: Determine Character and Timing

For contracts outside Section 1256, the character may be capital or ordinary and is generally recognized on settlement or close, depending on the instrument and your facts. Investor, trader, dealer, and hedging distinctions can all change the answer, as can straddle and foreign-currency considerations.

Step 5: Choose the Right Form

Qualifying Section 1256 contracts go on Form 6781. Other dispositions generally go on Form 8949 and Schedule D. When the classification is genuinely unclear, that is a signal to get professional review rather than guessing.

Bybit Perpetual Contract Taxes

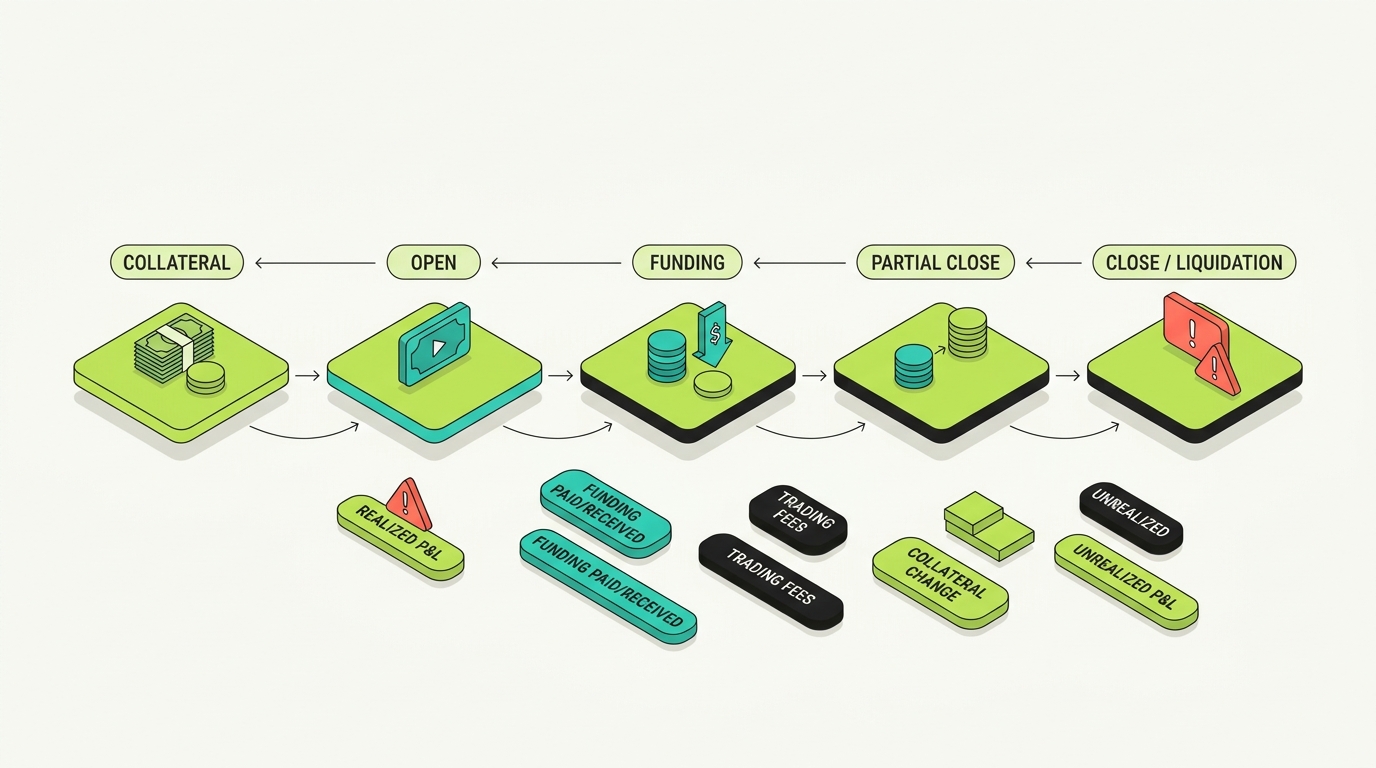

Perpetuals are Bybit’s signature product, and a single position is made of several tax-relevant components, not one number.

What a Perpetual Is

A perpetual contract tracks an underlying price without an expiration date, using funding payments to keep it near the spot price. Bybit offers USDT-margined, USDC-margined, and inverse (coin-margined) perpetuals.

The Components of a Perpetual Position

To report a perpetual correctly, separate it into its parts:

- Realized P&L when you close or partially close.

- Funding received and funding paid over the life of the position.

- Trading fees on entry and exit.

- Settlement asset and collateral changes.

- Liquidation and any liquidation fees, plus auto-deleveraging effects.

- Unrealized P&L on any year-end open position, which matters most if the contract is treated as Section 1256.

Why Net Account Change Is Not the Whole Story

Looking only at the net change in your account understates the work, because funding, fees, and collateral movements are bundled in. Each component needs to be identified so your reported result is accurate and defensible.

Example: Long BTC perpetual with funding and fees

You open a long BTC USDT perpetual, pay an entry fee, receive funding on some intervals and pay it on others, then close at a profit. Your reportable result is the realized P&L on the close, adjusted for the net funding and the trading fees. Reporting only the headline profit, while ignoring the funding paid and received, would misstate the gain. Each piece comes from your derivative records, not a single line.

Bybit Dated Futures Taxes

Dated futures differ from perpetuals because they expire and settle on a set date.

How Dated Futures Work

Bybit offers USDT, USDC, and inverse dated futures. You can close before expiration or hold through settlement, and mark price versus settlement price, fees, and collateral all factor into your result.

Tax Treatment

Like perpetuals, dated futures produce realized P&L, fees, and funding-style adjustments, and the Section 1256 question must be answered rather than assumed. Holding through settlement versus closing early can change the timing and details of your reportable result.

Example: Quarterly future held through settlement

You hold a quarterly USDC future to expiration. At settlement, your realized result is determined by the settlement price relative to your entry, net of fees. Whether the contract qualifies for Section 1256 treatment determines the form and character, which is exactly why the classification step matters before you report it.

Bybit Options Taxes

Options add another layer, because the buyer and the writer are taxed differently and the resolution path matters.

Buyer Versus Writer

As a buyer, you pay a premium and your result depends on whether you close, exercise, or let the option expire. As a writer, you receive a premium and your result depends on assignment, buyback, or expiration.

Resolution Paths

Closing, exercise, assignment, expiration, and cash settlement each have different consequences. Options used for hedging and positions that create straddles add further nuance, and some options may meet the Section 1256 definition while others do not.

Example: USDC-settled option expires in the money

You buy a call and it expires in the money with cash settlement. Your result reflects the settlement value against the premium you paid, net of fees. The character and form depend on the instrument’s classification, so the same decision tree applies here as for perpetuals and futures.

Bybit TradFi Perpetual Taxes

Bybit has expanded into TradFi perpetuals: USDT-denominated, USDT-settled contracts that track traditional stocks and commodities. These are an emerging search and reporting topic.

What TradFi Perpetuals Are

A TradFi perpetual tracks the price of a stock or commodity without giving you ownership of the underlying asset. It uses funding, margin, and liquidation mechanics like other USDT perpetuals.

Why the Underlying Does Not Decide the Form

Because you do not own the underlying stock or commodity, the tax form is not determined by the underlying asset by itself. The contract is a derivative, and the same classification analysis applies. Dividends and corporate actions on the real underlying are not the same as derivative adjustments on the contract.

Section 1256 Considerations

Whether a stock or commodity perpetual could meet the Section 1256 definition is a fact-specific question. Do not assume that a contract tracking a US stock automatically receives any particular treatment, and do not assume it cannot. Analyze the actual contract.

Example: Trading a perpetual tied to a US stock

You trade a USDT-settled perpetual that tracks a US stock and close it at a profit. You never owned the stock, so there are no dividends or share-level events to report; you have a derivative result. The character and form follow from the contract’s classification, not from how the underlying stock itself would be taxed.

Funding Payments, Fees, and Liquidations

These three items decide whether your derivative results are right, and they are the most commonly mishandled.

Funding Received and Paid

Funding flows occur at regular intervals across the life of a perpetual. Funding received improves your result and funding paid reduces it, and both are part of computing your derivative gain or loss. Many imports surface these poorly, so verify them.

Fees

Separate acquisition and disposal fees from transfer-only network costs, and remember that paying a fee with crypto can be a small disposal of the fee-paying asset. Margin interest and liquidation fees are their own categories.

Liquidations and Auto-Deleveraging

A liquidation is a forced close that generally creates a realized result plus fees and collateral effects, and auto-deleveraging can close positions outside your control. Both must be captured as real events, not ignored because they were involuntary.

Example: A liquidation creates realized P&L and collateral changes

Your position is liquidated when the market moves against you. The liquidation realizes a loss on the position, charges a liquidation fee, and disposes of some collateral. All three effects belong in your records. Treating the event as a simple balance drop would miss the realized loss you are entitled to report.

Bybit Margin Trading Taxes

Margin creates a more complex trail than a simple leveraged spot purchase, because borrowing, collateral, and interest all interact.

Borrowing Is Not Automatically Income

Borrowing an asset is generally not a taxable event by itself. What matters is what you do with the borrowed funds and what happens to your collateral.

The Taxable Pieces

Selling borrowed crypto, buying it back, repaying principal, paying interest, and any forced collateral sale or liquidation each have tax consequences. Short positions and cross-margin collateral effects add complexity, and negative balances or bad debt can arise.

Example: Borrowing ETH, selling it, and buying it back

You borrow ETH, sell it, then later buy ETH to repay the loan. The sale and the later purchase are distinct events with their own basis and proceeds, the interest you paid is its own item, and if your collateral was liquidated along the way, that is an additional realized event. Each leg is tracked separately from your spot trades.

Bybit Trading Bot Taxes

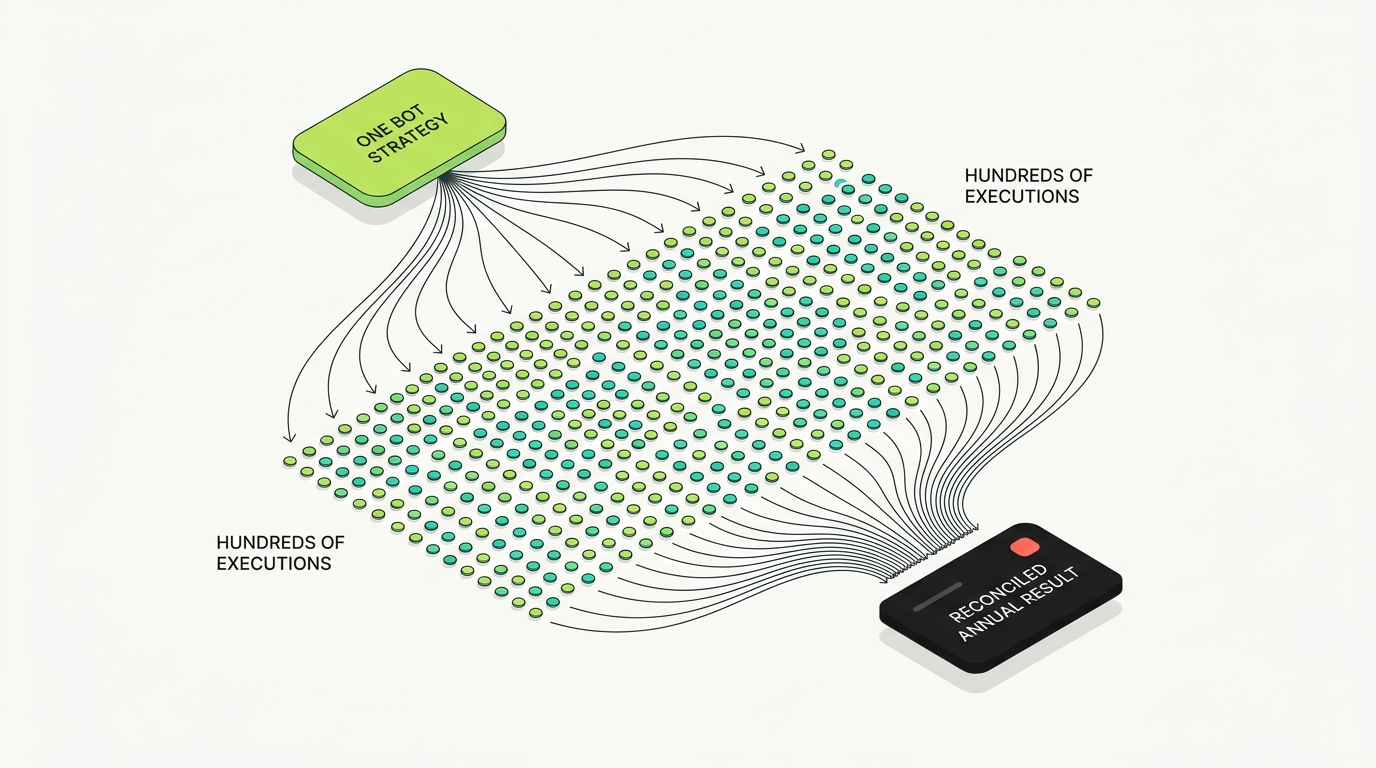

A bot is not one annual transaction. It is a transaction engine, and every execution it makes is potentially reportable.

Why Bots Explode Your Tax Lots

Grid bots, DCA bots, and futures bots can execute hundreds or thousands of trades in a year, each a separate taxable event with its own fees and timestamps. Moving funds into a bot is not itself taxable, but the resulting trades are.

Where Bots Go Wrong in Imports

Bot trades are frequently absent from API imports, and CSV plus API imports can duplicate the same activity. The result is either missing income or double-counted trades, and both distort your return.

Reconciling to Bot-Level P&L

The fix is to import the individual executions and reconcile them against the bot’s own P&L summary, so your transaction-level detail ties to the strategy-level result.

Example: A grid bot creates hundreds of taxable lots

Your grid bot runs all year and executes several hundred small buys and sells. Each is a taxable disposition with its own gain or loss and fee. The bot shows a tidy annual P&L, but your Form 8949 must reflect the underlying lots, reconciled so the detail matches the summary. Skipping the detail is how bot activity ends up unreported or double-counted.

Bybit Copy Trading Taxes

Copy trading splits activity between a lead trader and followers, and both sides have tax consequences.

Follower and Lead-Trader Activity

As a follower, the trades executed on your behalf are your taxable events, and profit-sharing or rewards can be income. As a lead trader, profit-sharing and commissions you receive are generally income, on top of your own underlying trading.

Separate Data and Internal Transfers

Copy trading moves funds between internal accounts and runs derivatives activity, and some of this data is not available through standard API integrations, which means separate exports are often required to reconcile it.

Example: Follower profits and leader rewards

You follow a lead trader and your account executes the copied trades, generating realized results, while you also pay a profit-sharing fee. The trades are your taxable events and the profit-sharing is a cost; if you were the leader instead, the profit-sharing you received would be income. Both roles require tracing internal transfers so nothing is double-counted or missed.

Bybit Earn and On-Chain Earn Taxes

Earn rewards are ordinary income when you control them, and the timing and value of each reward matter.

Easy Earn and Savings

Rewards from Easy Earn, flexible and fixed-term savings, and similar products are generally ordinary income at fair market value when you gain dominion and control, and that value becomes your basis for a later sale. They often pay frequently, creating many small income events.

On-Chain Earn and Staking

Proof-of-stake and on-chain staking rewards are ordinary income at fair market value when you gain dominion and control, including the ability to sell or dispose of them. Lockups, unstaking periods, and any liquid staking or replacement tokens add nuance to when control is obtained and what basis the rewards carry.

Example: Daily Earn rewards received over a year

You earn small daily rewards from a savings product all year. Each daily reward is ordinary income at its value on the day you control it, and each sets the basis for that small lot. When you later sell the accumulated rewards, you report a separate capital gain or loss on the change in value since receipt. Frequent rewards mean many tiny income and basis entries that must all be captured.

Bybit Structured Product Taxes

Structured products require contract-level analysis, because their economics differ from one product to the next.

Why One Rule Does Not Fit

Products such as Dual Asset and other structured offerings can involve a contributed asset, a yield or premium, a lockup, a settlement date, and settlement in a different asset than you contributed. Settlement in a different token can be a disposal, and early redemption or expiration changes the outcome.

What to Preserve

For each structured product, keep the exact product confirmation and settlement record, including the contributed asset, the yield, the settlement asset, and any conversion. That detail is what lets you analyze the product correctly rather than guessing.

Example: Dual Asset settles in a different cryptocurrency

You subscribe to a Dual Asset product with USDC, earn a yield, and at settlement the product converts your position into BTC. The yield is income, and the conversion may be a disposal that establishes a new basis in the BTC you receive. Without the settlement record, this is nearly impossible to report correctly, which is why preserving product confirmations matters.

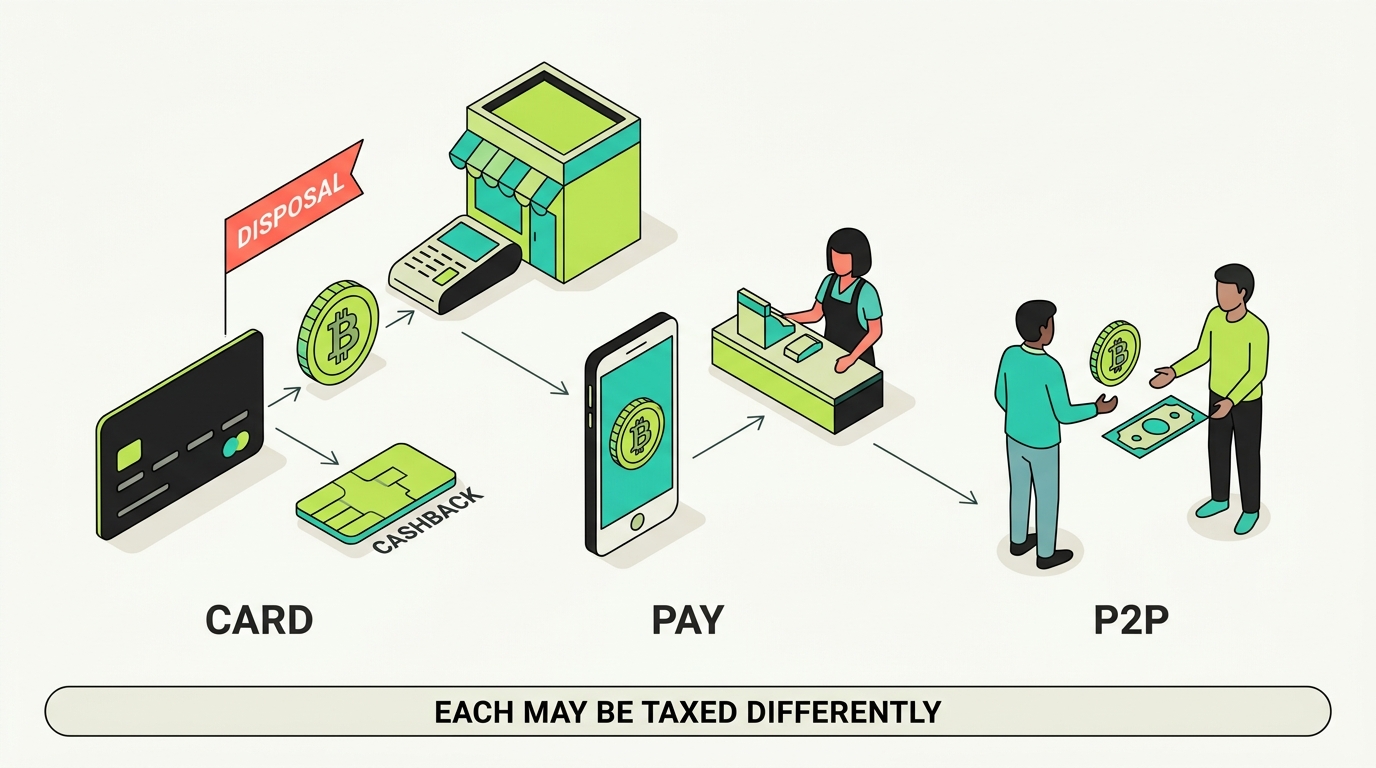

Bybit Card, Pay, and P2P Taxes

Payments and peer-to-peer activity are nearly absent from competing guides, which makes them a real long-tail opportunity and a real reporting gap.

Bybit Card

Spending appreciated crypto through the card is generally a disposal of that crypto, even when it converts to fiat automatically at the point of sale. Cashback and reward points are a separate question: not every reward is automatically taxable income, and the treatment can depend on the program structure, so track both the spending and the rewards and confirm the reward side with a professional.

Bybit Pay

Paying a merchant with crypto, directly or via conversion, is generally a disposal of the crypto used. Rewards and cashback on Pay raise the same reward-treatment questions as the card.

Bybit P2P

Selling crypto through P2P is a disposal with a gain or loss, and premiums, discounts, and fees affect the result; buying establishes basis. P2P uses a separate export process, and high-volume or business-like P2P activity can raise additional considerations.

Example: Spending appreciated crypto with the card

You bought ETH at 1,500 dollars and later spend it via the card when it is worth 2,500 dollars. Spending it is a disposal, so you have a 1,000 dollar gain on the amount spent, even though it felt like an ordinary purchase. Any cashback you received is analyzed separately under its own rules.

Bybit Alpha and Web3 Wallet Taxes

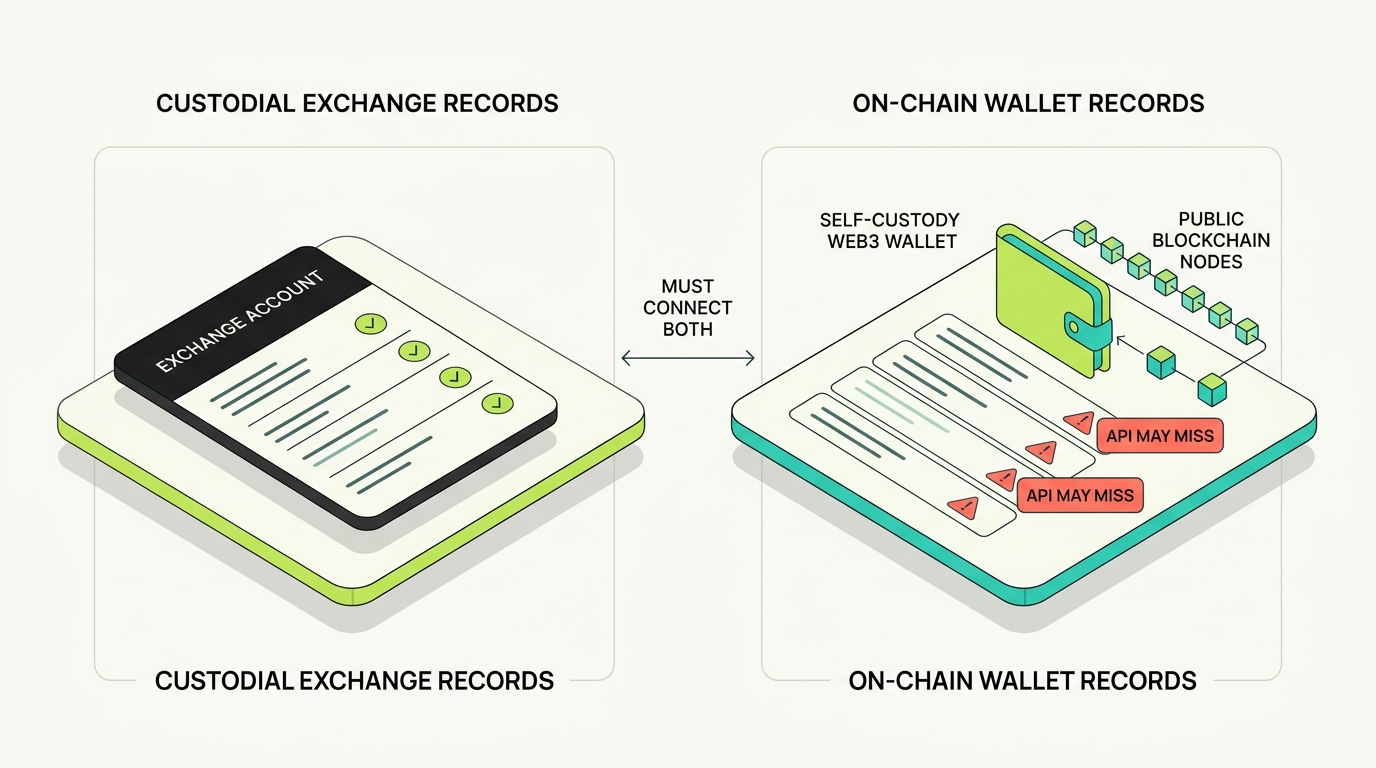

Bybit Alpha and self-custody wallets create a second data environment on the public blockchain that the exchange API does not fully capture.

Bybit Alpha

Alpha bridges your centralized balance into on-chain token trading. The on-chain buys, sells, and swaps it executes are taxable dispositions, but prices for some tokens may be missing, gas handling adds detail, and the on-chain leg may not be captured by the exchange API alone.

Self-Custody Wallet Activity

Bybit’s self-custody wallets put the keys in your hands, which means dapp activity, swaps, bridges, liquidity pools, NFTs, staking, and gas fees live on the blockchain, not in the exchange’s records. Connecting wallet data to your exchange activity is essential.

Why the Exchange API Is Not Enough

A successful exchange API import does not capture the full self-custody and on-chain trail. You generally need to add wallet addresses and on-chain history to build a complete picture.

Bybit Transfers and Missing Cost Basis

Transfers are where basis disappears, and missing basis is where overstated tax bills come from.

Why Transfers Are Misclassified

Moving your own crypto between platforms and wallets you control is generally not a taxable event, but the basis must travel with the asset. When it does not, a later sale can appear to have no cost basis and overstate your gain. Common journeys include Coinbase to Bybit, Kraken to Bybit, Binance to Bybit, MetaMask to Bybit, a hardware wallet to Bybit, and Bybit back out to any of them.

How to Reconstruct Basis

Rebuild the original acquisition from the platform where you first bought the asset, your own purchase records, and on-chain history, then carry that basis through every transfer to the point of sale. Network fees paid in crypto during transfers are small disposals that should also be captured.

Example: BTC acquired on Bybit, held in self-custody, and sold elsewhere

You bought BTC on Bybit, withdrew it to a hardware wallet, later deposited it into a US broker, and sold it. The broker reports the proceeds on a 1099-DA but does not know your Bybit purchase price, so the basis may show as zero. Supplying the original Bybit basis is what turns an inflated, full-proceeds gain into the real gain you actually owe tax on.

Wallet- and Account-Specific Cost Basis

Recent IRS guidance puts more weight on the wallet or account holding the units you dispose of, which matters for Bybit users with assets spread across platforms.

Why Account Location Matters

Specific identification requires adequate and timely identification of the units sold; otherwise, FIFO may apply within the particular wallet or account under the applicable rules. That means basis is increasingly tracked per account rather than across your whole portfolio at once.

Practical Implications

Keep records that tie each disposal to the specific lot and account, distinguish main-account from subaccount activity, and make sure basis travels with assets you move to a destination broker. Pre-2025 historical records remain important for proving basis on older lots.

How to Retrieve Your Bybit Transaction History

For most former US users, this is the make-or-break step. You cannot file an accurate return on data you do not have.

Bybit’s Export System

Bybit’s export system distinguishes among account statements, transaction logs, and order history, each with its own scope, date-range, and entry limits. Data export can batch a main account and many subaccounts, while individual Unified Trading Account exports have their own caps. P2P uses a separate export process, and institutional reporting uses a separate portal.

What to Download

Pull each of these, for the main account and every subaccount:

- Account statements and transaction logs for a complete record.

- Order history for trade detail.

- Deposit and withdrawal records for transfer tracing.

- Derivatives records for realized P&L, funding, and fees across perpetuals, futures, and options.

- Margin and loan records for borrowing, interest, and liquidations.

- Earn and structured-product records for income and settlements.

- Bot and copy-trading records where available.

- P2P and card records through their separate processes.

Export Limits and Segmentation

Because exports cap by date and entry count, pull in segments, verify that segments connect with no gaps, name files clearly by account, type, and date range, and keep every file. Download links can expire, so save the files locally.

What to Do When Records Are Unavailable

If exports are incomplete or access is gone, reconstruct from the edges inward: use destination platforms you transferred to, email confirmations, bank records for fiat on-ramps, and public blockchain explorers for the wallet addresses you used. A reconstructed history built from multiple corroborating sources is both possible and defensible.

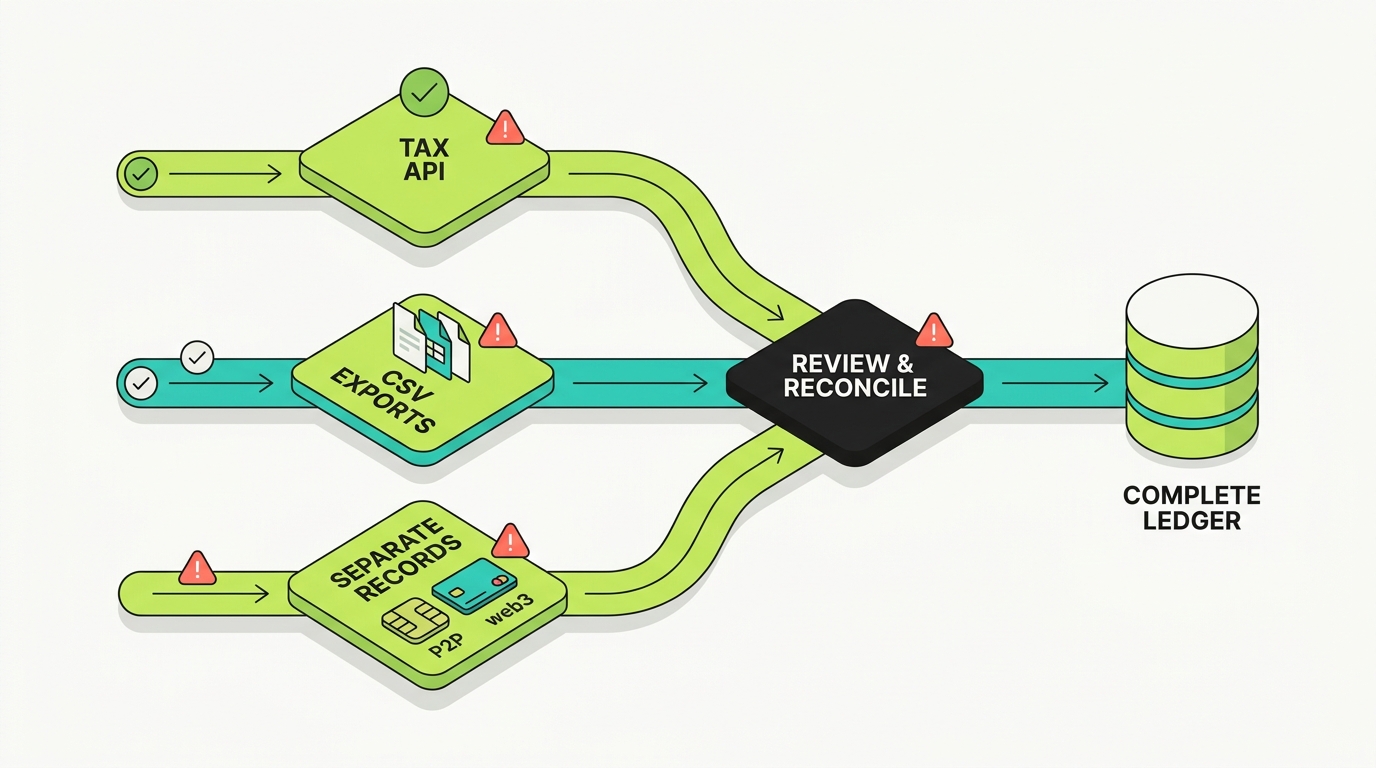

Bybit API vs CSV and Official Exports

Once you have data, the next trap is assuming an import is complete. On Bybit, it frequently is not.

Why a Successful API Connection Is Not a Complete History

Tax API support for Bybit is commonly described as beta or incomplete. Depending on the integration, API data may omit or complicate:

- Bot trades and copy-trading activity.

- Some rewards, including certain Launchpool rewards.

- Conversions and certain NFT or on-chain activity.

- Internal transfers and older activity.

- Subaccount activity, which often needs separate connections.

Advantages and Limitations of an API

A read-only API key pulls a deeper, automatically updating history than a manual CSV, but it can silently miss the categories above. Treat it as a starting point.

Advantages and Limitations of CSV and Official Exports

Official exports are authoritative for the periods they cover and can capture categories an API misses, at the cost of date caps and manual effort. Separate exports for P2P, institutional, and on-chain activity fill the remaining gaps.

Read-Only API Security

If you connect an API, use a read-only key and never enable withdrawal permissions. Tax software needs to read your history, not move your funds.

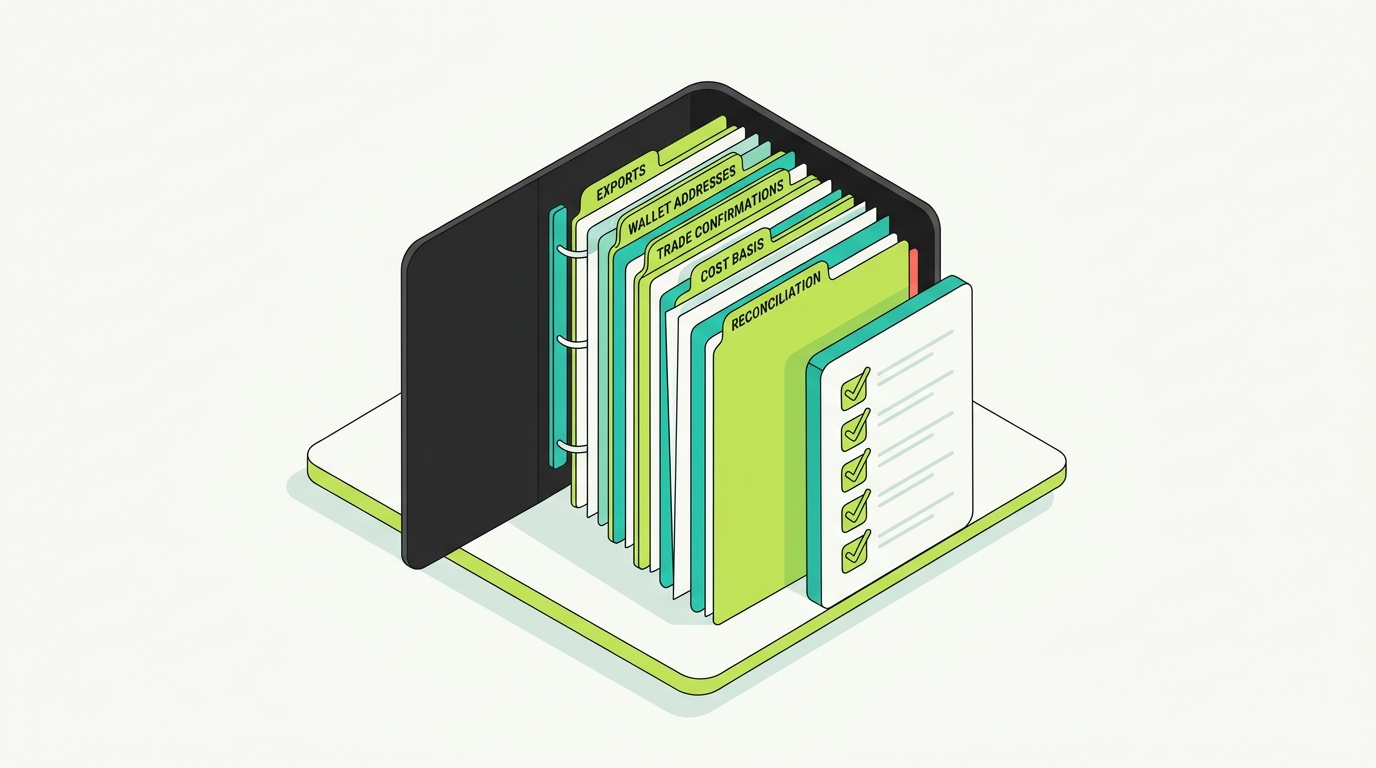

Bybit Reconciliation Checklist

Reconciliation is the difference between a real return and a hopeful one. Work through this before you file.

How to Report Bybit Activity on a US Tax Return

Once your ledger is reconciled, reporting follows the standard US framework.

The Forms

Capital dispositions go on Form 8949 and carry to Schedule D. Ordinary income from rewards goes on Schedule 1 or the appropriate income form. Qualifying Section 1256 contracts go on Form 6781. Business-level activity may implicate Schedule C. The Form 1040 digital-asset question must be answered.

Reporting Without a 1099

Because Bybit sends no form, these entries only appear if you build them from your reconciled records. Reporting activity without a 1099 is normal and expected for offshore exchanges; the obligation does not depend on receiving a form.

Supporting Basis That Differs From a Broker Form

If a destination broker’s 1099-DA reports proceeds without basis, you supply the correct basis on your return and keep the workpapers that prove it. This is how you avoid being taxed on full proceeds rather than real gain.

Bybit, DAC8, and CARF

International information sharing on crypto is expanding, and the operating entity matters.

DAC8

DAC8 is an EU framework covering a broad range of crypto assets, with a first reporting year of 2026 and information exchanges scheduled to follow. Whether it touches your activity depends on the specific Bybit entity and your residency.

CARF

CARF is the OECD’s Crypto-Asset Reporting Framework for automatic exchange of crypto-account information between participating jurisdictions, with first exchanges anticipated around 2027 in many places. Like DAC8, relevance depends on entity and residency.

Why This Does Not Decide Your US Treatment

International reporting frameworks affect what authorities learn, not how your transactions are characterized for US tax. The practical takeaway is that accurate self-reporting matters more, not less, as information sharing grows. Avoid the categorical claim that an offshore exchange never reports to any authority.

Bybit, FBAR, and Form 8938

Foreign-account reporting for crypto is nuanced and fact-specific, so treat it carefully.

FBAR

FinCEN’s current guidance states that a foreign account holding solely virtual currency is not presently reportable on the FBAR, though FinCEN has signaled an intention to amend the regulations. If the account also held otherwise reportable assets, the analysis can change.

Form 8938

Form 8938 is a separate regime that may apply to certain specified foreign financial assets or accounts when thresholds and legal requirements are met. Whether a Bybit account triggers it depends on your facts, balances, and circumstances.

Why to Confirm With a Professional

Both regimes are fact-specific and evolving. Confirm your position with a qualified professional rather than assuming either extreme.

Correcting Prior-Year Bybit Returns

If an older return left off Bybit activity, you can fix it, and fixing it proactively is usually far better than waiting for a notice.

Signs a Return May Be Incomplete

Missing derivative P&L, missing funding, missing rewards, incorrect zero basis, duplicated imports, and incorrect contract classification are all red flags. Build a corrected ledger first, then amend, and keep both the original and corrected workpapers.

Preparing for a Bybit Tax Audit or IRS Notice

Audit readiness is about evidence, organized before you need it.

What to Preserve

Keep raw exports, the account and subaccount list, wallet addresses, blockchain explorer records, trade confirmations, derivatives and funding histories, liquidation records, Earn and structured-product settlement records, P2P and card records, bank statements, cost-basis workpapers, your reconciliation summary, and prior-year returns. A restricted account makes preserving these now essential.

Best Bybit Tax Software

The right tool depends on your history, and no import should be trusted without review.

The Landscape

Koinly, CoinLedger, CoinTracker, Coinpanda, CoinTracking, Divly, and TokenTax all support Bybit to varying degrees, differing in historical depth and in derivatives, bot, copy-trading, subaccount, Earn, and Web3 support. Several explicitly warn that Bybit API support is limited or beta.

Why Software Alone Is Not Enough

An apparently successful import may still be incomplete. The real differentiator is whether your history is fully reconciled across every source, not which logo is on the software. For derivative-heavy, multi-account Bybit users, software is a tool inside a reconciliation process, not a substitute for it.

What Is Digital Asset Reconciliation?

Importing data is not the same as reconciling it. Reconciliation means identifying every data source, connecting transfers, reconstructing cost basis, classifying derivatives correctly, reviewing rewards and structured products, tying opening to closing balances, and building an audit trail.

Signs You Need Professional Reconciliation

High transaction volume, perpetuals, futures and options, liquidations, trading bots, copy trading, multiple subaccounts, missing API records, structured products, Bybit Alpha or wallet activity, transferred-in assets, prior-year errors, an IRS notice, or an entity or trust account are all signals that software alone will not produce a clean, defensible return.

Not sure your crypto taxes are right?

Talk to a Count On Sheep specialist. We will spot the costly errors before you file. No obligation.

Book My Free Review- Reviewed by Former Big 4 Accountants

- Keep your CPA

- No pressure, no sales pitch

Common Bybit Tax Mistakes

The same mistakes recur, and they all have the same fix.

- Assuming no 1099 means no reporting obligation.

- Relying on a single API import as if it were complete.

- Forgetting subaccounts, bots, and copy trading.

- Treating internal transfers and collateral moves as sales.

- Assigning zero basis to transferred-in assets.

- Ignoring funding payments and liquidations.

- Reporting unrealized P&L as realized without an applicable rule, or ignoring year-end mark-to-market where it applies.

- Automatically forcing every derivative into Section 1256, or automatically rejecting it.

- Misclassifying structured-product settlement.

- Ignoring card, Pay, P2P, and Alpha activity.

- Filing before reconciling balances.

The Bottom Line on Bybit Taxes

Bybit’s US restriction changed who needs this guide, but it did not change the obligation. Historical activity remains reportable, no form does not mean no tax, derivatives require instrument-by-instrument analysis rather than a blanket rule, API imports must be validated against official records, transfers require complete basis records, and exchange activity must be connected to your on-chain and wallet history. Reconcile your complete picture before you file, and the rest follows.

If your Bybit history is large, derivative-heavy, or spread across accounts, wallets, and other exchanges, that is exactly the situation Digital Asset Reconciliation is built for. Count On Sheep retrieves and reconstructs your records, connects every source, traces basis across transfers, classifies derivatives deliberately, and produces a defensible return that works alongside your tax preparer.

Frequently Asked Questions

Is Bybit available in the United States?

Bybit's main platform currently lists the United States among its restricted jurisdictions, so ordinary US access to spot, derivatives, and Earn products is not available the way it once was. If you are a US taxpayer, the relevant question now is how to report historical Bybit activity and reconcile assets you transferred away, not how to keep trading there. This guide does not explain how to bypass geographic restrictions.

Do former US users still need to report Bybit activity?

Yes. A platform restricting US access does not erase taxes on activity that already happened. If you traded, closed derivative positions, earned rewards, or disposed of crypto on Bybit in prior years, those events remain reportable, and amended returns may be appropriate if you left them off. The restriction makes records harder to retrieve, but it does not make the underlying gains, losses, and income disappear.

Does Bybit report to the IRS?

Bybit is an offshore exchange and generally does not issue US tax forms like Form 1099-MISC or Form 1099-DA to US users, so it does not report your activity to the IRS the way a US broker does. That does not make your trades invisible or tax free. On-chain transfers to and from US exchanges, blockchain analytics, and expanding international information sharing can still surface offshore activity, and you are legally required to self-report all gains, losses, and income.

Does Bybit issue Form 1099-DA?

There is no current official Bybit publication confirming that its main offshore platform issues US customers a Form 1099-DA, and given its US-restricted status you should not assume one is coming. Form 1099-DA is a US broker form. The realistic 1099-DA scenario for a former Bybit user is receiving one from another exchange, such as Coinbase or Kraken, after transferring assets there and selling. That form reports proceeds without your Bybit acquisition history behind it.

Why did I not receive a Bybit tax form?

Because Bybit is an offshore exchange that generally does not issue US tax forms to US users, and because US access is restricted. There is usually no 1099 to download. This is the most misunderstood point about Bybit taxes: no form does not mean no tax. You must reconstruct your transaction history from exports, wallet records, and destination-platform records, then report it yourself.

Are Bybit spot trades taxable?

Yes. Selling crypto for fiat or a stablecoin is a taxable disposal, and trading one cryptocurrency for another is also a taxable disposal of the coin you gave up, even though no US dollars change hands. You calculate a capital gain or loss equal to the value received minus the cost basis of the coin you traded away. Crypto-to-crypto trades are among the most commonly overlooked taxable events on Bybit.

Are Bybit stablecoin trades taxable?

Yes. Converting crypto into a stablecoin like USDT or USDC is a disposal of the crypto you converted, so it is a taxable event with a gain or loss measured against your basis. Stablecoins are still property to the IRS, and a great deal of Bybit trading and derivatives collateral runs through stablecoins, so these dispositions add up quickly and must all be reported.

Are Bybit perpetuals taxable?

Yes. Realized profit and loss on closed perpetual positions is taxable, and funding payments, fees, and liquidations all factor in. The harder question is character. You should not automatically apply the favorable 60/40 Section 1256 treatment to every Bybit perpetual, and you should not automatically assume one universal non-Section-1256 treatment either. The correct classification depends on the specific contract and your facts, which is why perpetuals deserve careful, instrument-by-instrument analysis.

Are Bybit futures Section 1256 contracts?

Not automatically. Section 1256 treatment, with mark-to-market and the 60% long-term / 40% short-term split reported on Form 6781, applies only to contracts that meet the statutory definition. Offshore crypto futures and perpetuals do not automatically qualify, and they also should not be assumed to fall outside Section 1256 without analysis. Whether a given Bybit future qualifies depends on the contract terms, the venue, and your circumstances, so this is a classic area for professional review.

How are Bybit options taxed?

Bybit options taxation depends on whether you were the buyer or writer and how the option resolved: closed, exercised, assigned, expired, or cash-settled. The premium, the settlement asset, and any hedging or straddle considerations all matter, and some options may meet the Section 1256 definition while others do not. Because the outcomes diverge so much, each option position should be analyzed on its own terms rather than lumped into a single rule.

Are Bybit funding payments taxable?

Funding payments are a real economic item that must be tracked. Funding you receive increases your net result and funding you pay reduces it, and these flows are part of computing the gain or loss on your perpetual activity. They are easy to miss because they occur at regular intervals throughout the life of a position, and many imports do not surface them cleanly, so they are a frequent source of misstated derivative results.

Are unrealized Bybit gains taxable?

Generally not by themselves. Unrealized profit on an open position is usually not taxed until you close the position or a realization event occurs. The important exception is contracts that qualify for Section 1256 mark-to-market treatment, where open positions at year end are treated as if sold. Because that exception turns on classification, do not assume either that all open positions are tax free at year end or that all of them are marked to market.

How are Bybit liquidations reported?

A liquidation is a forced close of a position and generally creates a realized gain or loss, plus liquidation fees and collateral effects. It is reported like any other realized derivative result, but it often surprises users because it happens automatically and can dispose of collateral. Capturing liquidation events accurately, including the fees and any collateral sold, is essential to getting your derivative results right.

Is Bybit margin borrowing taxable?

Borrowing an asset on margin is generally not itself a taxable event, but the trades you make with borrowed funds and a liquidation of collateral can create reportable gains and losses. Selling borrowed crypto, buying it back, repaying principal, and paying interest each have separate consequences that must be tracked apart from your spot activity. Liquidations in particular are forced disposals that are easy to overlook.

Is Bybit margin interest deductible?

It depends on your facts. Interest paid on margin borrowing may be deductible in some circumstances, such as investment interest expense subject to limitations, but the rules are fact-specific and depend on how the borrowing was used and your tax profile. Do not assume margin interest is automatically deductible. Track the interest you paid and confirm the treatment with a qualified professional.

Are Bybit trading bots taxable?

Yes, at the level of the underlying trades. A bot does not change the tax character of what it does. Every buy and sell a grid bot, DCA bot, or futures bot executes is a separate taxable event, so a single bot strategy can generate hundreds or thousands of taxable lots in a year. Moving funds into a bot is not itself taxable, but the resulting trades are, and bot activity is frequently missing from API imports.

Is Bybit copy trading taxable?

Yes. As a follower, the trades executed on your behalf are still your taxable events, and any profit-sharing or rewards can be income. As a lead trader, profit-sharing and commissions you receive are generally income. Copy trading also moves funds between internal accounts and runs derivatives activity, and some of this data is not available through standard API imports, so it often requires separate exports to reconcile.

Are Bybit Easy Earn rewards taxable?

Yes. Rewards from Easy Earn and similar yield products are generally ordinary income at fair market value when you gain dominion and control over them, and that value becomes your cost basis for a later sale. Flexible and fixed-term products, promotional yields, and compounding rewards all count. Earn rewards often pay frequently and are commonly missing from API imports, making them a frequent source of unreported income.

Are Bybit On-Chain Earn rewards taxable?

Yes. Proof-of-stake and on-chain staking rewards are ordinary income at fair market value when you gain dominion and control, including the ability to sell or dispose of them. That value becomes your basis, so a later sale produces a separate capital gain or loss. Lockups, unstaking periods, and any liquid staking or replacement tokens add nuance, so the receipt timing and value of each reward need to be tracked.

How is Bybit Dual Asset taxed?

Dual Asset and similar structured products require contract-level analysis rather than a single label. Depending on the product, you may receive a yield or premium, and the position may settle in a different asset than you contributed. Settlement in a different token can be a disposal, and early redemption or expiration changes the picture. The right approach is to keep the exact product confirmation and settlement record and analyze each one, because the economics differ across products.

Are Bybit Card rewards taxable?

Not all card rewards are treated the same way, so avoid assuming every reward is taxable income. Some purchase rebates and promotional awards may be treated differently from staking-style reward income, and the analysis can depend on the structure of the program. What is clearer is that spending appreciated crypto through a card is generally a disposal of that crypto. Track both the spending events and the rewards, and confirm the reward treatment with a professional.

Does spending crypto with Bybit Card create a taxable event?

Generally yes. Spending crypto that has appreciated since you acquired it is a disposal of that crypto, so it can create a capital gain or loss measured against your basis, even when the card converts it to fiat automatically at the point of sale. Each purchase is potentially a small taxable disposition, which means frequent card use can generate many little gain-or-loss events that need to be captured.

Are Bybit P2P trades taxable?

Yes. Selling crypto through P2P is a disposal with a gain or loss, and premiums, discounts, and fees affect the result. Buying through P2P establishes basis in what you acquired. P2P activity uses a separate export process from the main account, so it is easy to leave out, and high-volume or business-like P2P activity can raise additional considerations that deserve professional input.

Is Bybit Alpha activity taxable?

Yes. Bybit Alpha bridges your centralized account into on-chain token trading, so the on-chain buys, sells, and swaps it executes are taxable dispositions just like other trades. The complication is data: the on-chain leg may not be fully captured by the exchange API, prices for some tokens may be missing, and gas handling adds detail. Alpha activity often needs on-chain reconstruction in addition to the exchange records.

Does the Bybit Tax API include every transaction?

No. Tax API support is commonly described as beta or incomplete, and it can miss categories such as certain bot trades, copy-trading activity, some rewards, conversions, and on-chain or NFT activity. Treat a successful API connection as a starting point, not proof of completeness. The only way to trust an import is to reconcile it against official exports and your opening and closing balances.

Why is my Bybit API missing transactions?

API imports are frequently incomplete because of how the data is exposed and because Bybit's account structure spans many products and subaccounts. Bot trades, copy trading, certain rewards, conversions, internal transfers, and older activity can all be omitted or imported incorrectly, and subaccounts often need separate connections. The fix is to compare API results against official CSV exports and reconcile balances rather than relying on a single method.

Should I use API or CSV for Bybit?

Use both and reconcile them against each other. A read-only API gives a deeper, automatically updating history but can silently miss categories. Official CSV and report exports are authoritative for the periods they cover and can capture items an API misses, at the cost of manual effort and date-range limits. Separate exports for P2P, institutional, and on-chain activity fill remaining gaps. No single source should be trusted without review.

How do I export Bybit subaccounts?

Bybit's data export tools support main-account and subaccount exports, and batch export can cover a main account and many subaccounts at once, while individual Unified Trading Account exports have their own date and entry limits. Generate exports for every subaccount, not just the main account, because activity siloed in a subaccount that never gets imported is one of the most common reasons a Bybit return comes out wrong.

How do I export Bybit P2P records?

P2P activity uses a separate export process from the main account statements, transaction logs, and order history, so you must pull it specifically. Keep the P2P records together with your bank-transfer documentation, since P2P trades involve fiat counterparties and the supporting evidence matters if your reporting is ever questioned.

How far back can I download Bybit data?

Bybit's export system distinguishes among account statements, transaction logs, and order history, each with its own date-range and entry limits, and some exports must be pulled in segments such as one year at a time. Historical availability and download-link expiration vary by export type. Because of these caps, export in segments, verify that segments connect with no gaps, and keep every file while you still have access.

How do I calculate Bybit cost basis?

For each disposal, take the US dollar proceeds and subtract your adjusted cost basis, which is what you paid for that specific lot including acquisition fees. The result is your capital gain or loss, and the holding period determines whether it is short-term or long-term. The hard part on Bybit is establishing accurate basis when assets were transferred in from other platforms or when records were lost after access changed, not the subtraction itself.

What do I do if Bybit shows zero cost basis?

A zero or missing basis usually means the asset was transferred into Bybit and the purchase history did not follow it. Do not accept a zero basis, because it overstates your gain. Reconstruct the original acquisition from the platform where you first bought the asset, your own purchase records, and on-chain history, then apply that basis to the disposal. Fixing this is often the difference between a fair tax bill and a wildly inflated one.

Are transfers from Bybit taxable?

Moving your own crypto between wallets and platforms you control is generally not a taxable event. Depositing crypto into Bybit, withdrawing it, or sending it to your own hardware wallet is a transfer, not a disposal. The catch is cost basis: your purchase history must travel with the asset, and a network fee paid in crypto during the transfer is itself a small disposal that should be captured.

How do I reconcile Bybit with Coinbase?

Import both your Bybit history and your Coinbase history into one tax tool, then match the transfers between them so basis follows each asset across the move. A common pattern is buying on Coinbase, sending to Bybit, trading, and later sending back to Coinbase to sell. Each leg must be traced so the eventual sale reflects true basis rather than a zero-basis, overstated gain on either side.

How do I reconcile Bybit with Kraken?

The approach mirrors any cross-exchange reconciliation: import both histories, match the withdrawal from one platform to the deposit on the other, and carry the original cost basis through the transfer. If you bought on Bybit, moved the asset to Kraken, and sold it there, Kraken may report proceeds without your Bybit basis, so supplying that basis is what keeps your reported gain accurate.

How do I report Bybit on Form 8949?

Each disposal (every sale, crypto-to-crypto trade, derivative close, fee paid in crypto, and card or P2P sale) goes on Form 8949 with the acquisition date, disposal date, proceeds, cost basis, and resulting gain or loss, split between short-term and long-term. Those totals carry to Schedule D. Reward and income items go on Schedule 1 or the appropriate income form, and qualifying Section 1256 contracts go on Form 6781. Because Bybit sends no form, these entries only appear if you build them from reconciled records.

When is Form 6781 used for Bybit?

Form 6781 is used for contracts that qualify as Section 1256 contracts, which receive mark-to-market treatment and the 60% long-term / 40% short-term split. Not every Bybit derivative qualifies, and qualification depends on the contract and your facts, so Form 6781 should be used only after a position has actually been determined to meet the Section 1256 definition, ideally with professional input.

Does Bybit activity require an FBAR?

It depends, and the rule is nuanced. FinCEN's current guidance states that a foreign account holding solely virtual currency is not presently reportable on the FBAR, though FinCEN has signaled an intention to amend the regulations. If the account also held otherwise reportable assets, the analysis can change. Because this is fact-specific and evolving, confirm your FBAR position with a qualified professional rather than assuming either extreme.

Does Bybit require Form 8938?

Possibly. Form 8938 is a separate regime from the FBAR and may apply to certain specified foreign financial assets or foreign financial accounts when the applicable thresholds and legal requirements are met. Whether a Bybit account triggers Form 8938 depends on your specific facts, balances, and circumstances, so this is another area where individualized professional advice is appropriate.

Does DAC8 apply to Bybit EU?

DAC8 is an EU framework covering a broad range of crypto assets, with a first reporting year of 2026 and corresponding information exchanges scheduled to follow. Whether it applies to your activity depends on the specific Bybit operating entity and your residency, since a Bybit EU account is not automatically treated the same as an account held through another Bybit entity. Identify the entity you actually used before drawing conclusions.

What is CARF?

CARF is the OECD's Crypto-Asset Reporting Framework, designed to enable automatic exchange of crypto-account information between participating jurisdictions, with first exchanges anticipated beginning around 2027 in many places. Like DAC8, its relevance to you depends on the operating entity and your residency. The practical takeaway is that international information sharing on crypto is expanding, which is one more reason accurate self-reporting matters.

Can I amend a return with missing Bybit activity?

Yes. If a prior-year return left off Bybit trades, derivative results, funding payments, rewards, or other activity, you can file an amended return to correct it. Signs that an older return may be incomplete include missing derivative P&L, missing funding, missing rewards, incorrect zero basis, duplicated imports, and incorrect contract classification. Build a corrected transaction ledger first, then amend, and keep both the original and corrected workpapers.

What records should I retain for Bybit?

Keep your full Bybit exports (account statements, transaction logs, order history), main and subaccount lists, wallet addresses, blockchain explorer records, trade confirmations, derivatives and funding histories, liquidation records, Earn and structured-product settlement records, P2P and card records, bank statements, cost-basis workpapers, and your reconciliation summary, along with prior-year returns. For a restricted account, preserving these now is essential because access can change without warning.

What is the best Bybit tax software?

The best tool depends on your transaction history. Koinly, CoinLedger, CoinTracker, Coinpanda, CoinTracking, Divly, and TokenTax all support Bybit to varying degrees, with differences in historical depth and in derivatives, bot, copy-trading, subaccount, Earn, and Web3 support, and several explicitly warn that Bybit API support is limited or beta. Whichever you choose, an apparently successful import may still be incomplete, so the real differentiator is whether your history is fully reconciled, not which logo is on the software.

When should I hire a crypto tax professional for Bybit?

Consider professional help when you have a restricted account, missing exports, large transferred-in positions, perpetuals, futures or options, liquidations, trading bots, copy trading, multiple subaccounts, structured products, Bybit Alpha or Web3 wallet activity, prior-year errors, an IRS notice, or high transaction volume. At that point, software alone often cannot produce a clean, defensible return, and a reconciliation specialist who connects every source and traces basis across transfers becomes worth far more than the fee.

What is the biggest Bybit tax mistake?

Assuming that no 1099 means no tax. That single assumption is what leads to unreported offshore activity, back taxes, and penalties. Close behind it are relying on a single API import as if it were complete, ignoring subaccounts and bot activity, treating internal transfers as sales, assigning zero basis to transferred-in assets, ignoring funding and liquidations, and automatically forcing every derivative into one tax category. The fix for all of them is the same: reconcile your complete history before you file.

Can Count On Sheep help with Bybit taxes?

Yes. Count On Sheep provides CPA-ready Digital Asset Reconciliation for current and former Bybit users: retrieving and reconstructing historical records, connecting every Bybit account and subaccount to your other exchanges and wallets, matching transfers so basis follows each asset, handling perpetuals, futures, options, margin, bots, copy trading, Earn, and structured products, reconciling against any 1099-DA you received elsewhere, and producing a defensible Form 8949, Form 6781 where appropriate, and income report. We are a reconciliation service that works alongside your tax preparer.