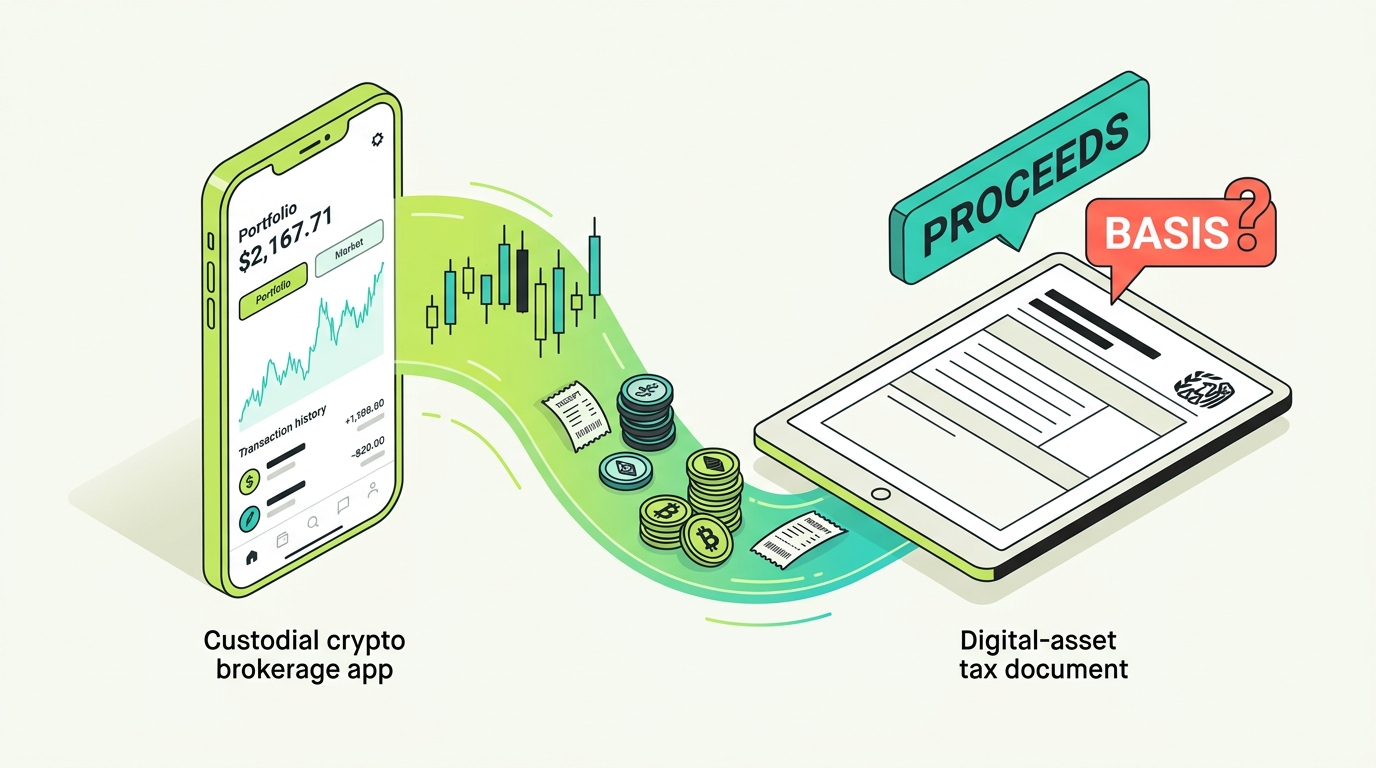

Robinhood reports your crypto dispositions, but it does not necessarily know the complete acquisition history behind every asset you sell. That single sentence explains almost every Robinhood crypto tax problem people run into. Robinhood will hand the IRS a number for what you sold. Whether that number turns into a fair tax bill or a wildly inflated one depends on cost basis, and cost basis is exactly the part Robinhood may be missing.

This is the definitive Robinhood crypto tax guide for 2026, written for the people who actually need it: US Robinhood Crypto users trying to make sense of Form 1099-DA, taxpayers who transferred crypto in from another exchange and now face missing basis, staking participants, Robinhood Wallet users with on-chain activity, high-volume traders bumping into import limits, and anyone reconciling a 1099-DA that does not match what they think they owe. Most existing Robinhood guides are either fragmented help-center pages or software signup flows that say connect an API and upload a CSV. They skip the questions that actually decide whether your return is right.

If one idea sticks from this guide, let it be this:

Form 1099-DA reports your proceeds. It does not always know your basis. Proceeds are not the same as taxable gain, and the gap is your responsibility to close.

On a Robinhood crypto return, the real work is rarely the arithmetic. It is separating which transaction year and filing season you are dealing with, reconciling daily-aggregated lines back to individual trades, reconstructing basis on transferred-in assets, understanding the zero-basis priority rule and tax-lot selection, keeping Robinhood Crypto separate from Robinhood Wallet, and handling staking and stablecoins that may not show up cleanly on a form.

This guide covers the full landscape of Robinhood crypto taxes:

- The 2025 versus 2026 reporting transition and why the year you mean matters

- Form 1099-DA, daily aggregation, proceeds versus gain, and the new Form 8949 digital-asset boxes

- Missing and transferred cost basis, customer-provided basis, the zero-basis priority rule, and tax-lot selection

- Average cost versus tax basis, account-specific basis, staking, stablecoins, fees, and transfers

- Robinhood Crypto versus Robinhood Wallet, exports and the activity-report trap, reconciliation, audits, and IRS notices

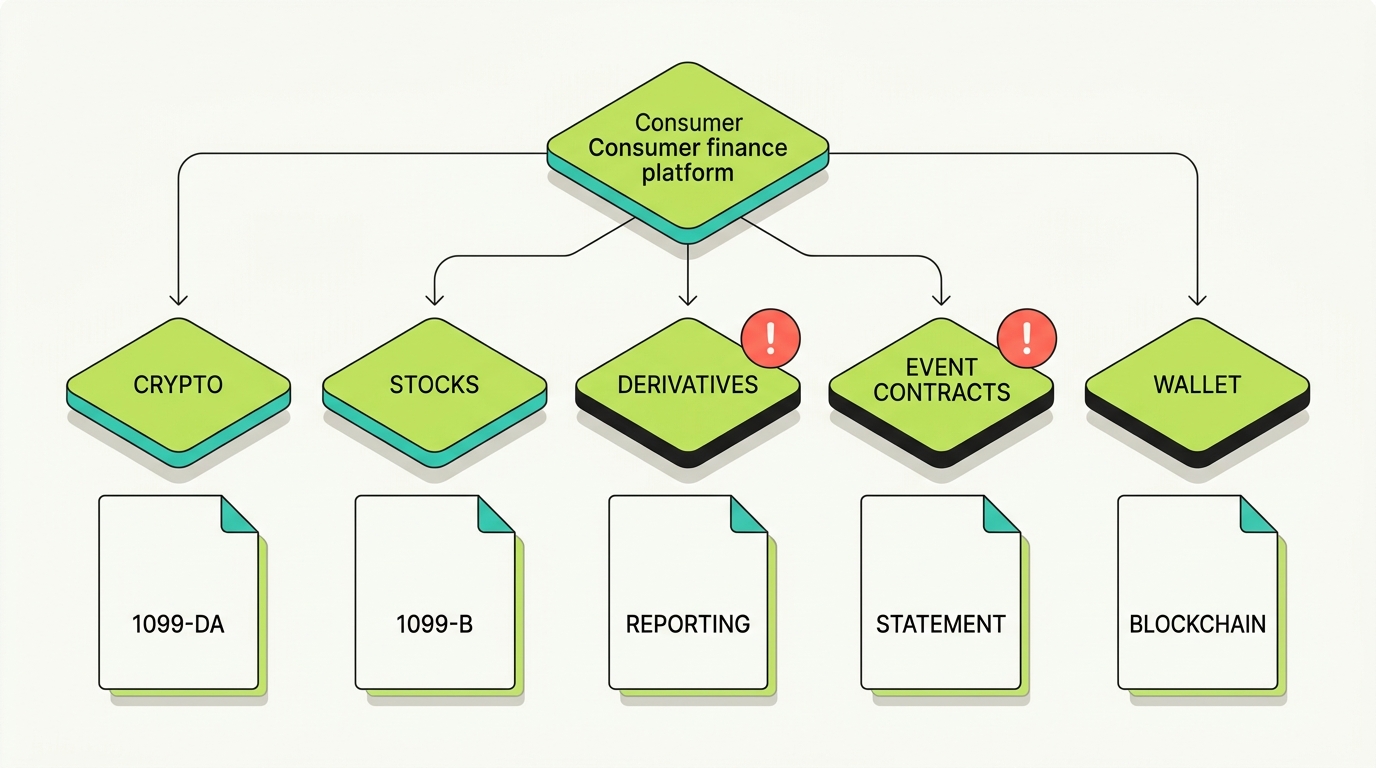

Before any numbers, here is the most useful mental model: Robinhood is several products bundled into one app and one consolidated tax package, and they are not interchangeable for tax purposes.

Quick Answer: How Are Robinhood Crypto Transactions Taxed?

Selling, exchanging, or spending crypto on Robinhood can create a capital gain or loss, and staking and other rewards can create ordinary income. Robinhood reports applicable custodial crypto dispositions on Form 1099-DA, but transferred cost basis and self-custody Robinhood Wallet activity may require separate reconciliation. The form shows proceeds; your taxable gain is proceeds minus basis minus applicable costs, and getting basis right is the whole game.

Robinhood Crypto Tax Changes at a Glance

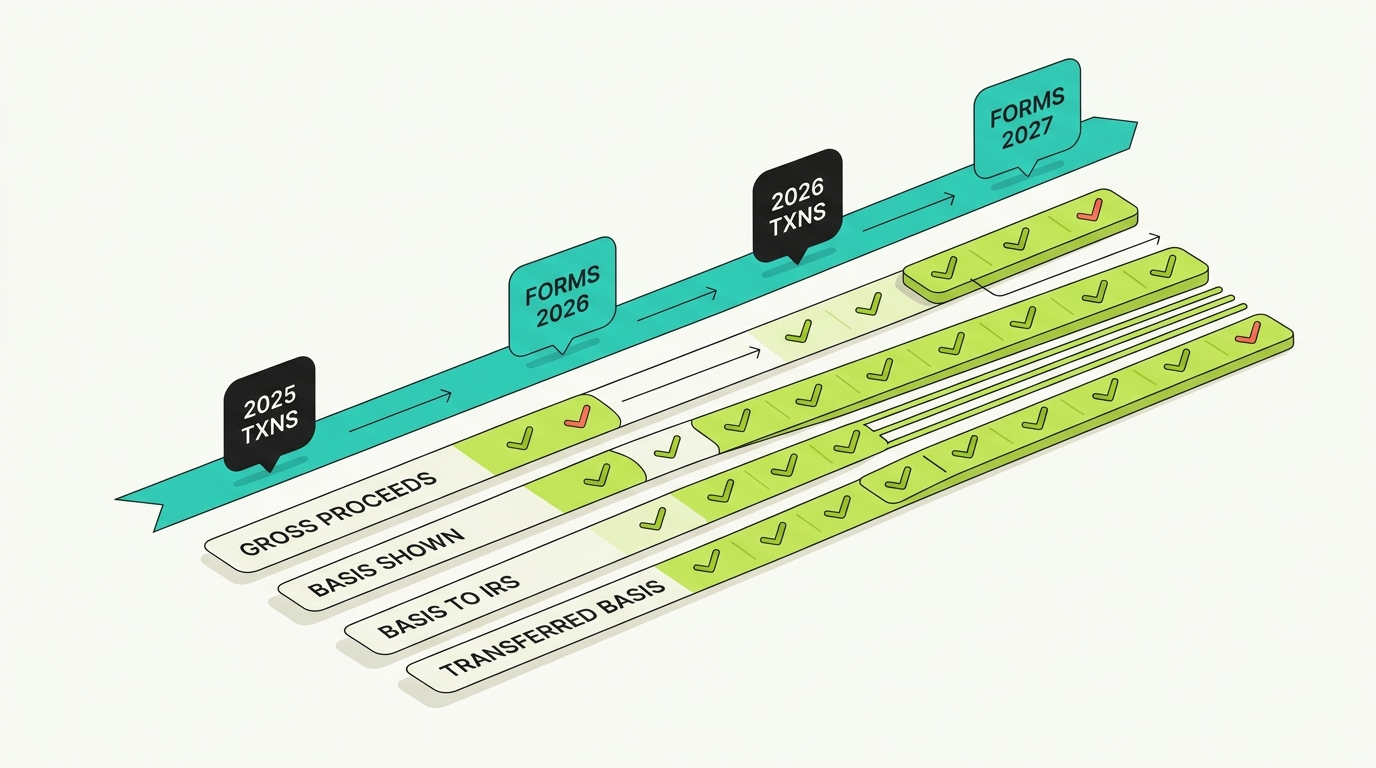

The phrase 2026 Robinhood taxes is ambiguous, and that ambiguity causes real errors. It can mean two different things: the 2025 transactions you report on forms issued in early 2026, or the 2026 transactions you report on returns generally filed in 2027. Keep them separate.

The Transition Timeline

- 2024 and earlier: Crypto was often reported on Form 1099-B or not on a dedicated broker form at all, depending on the year and platform.

- 2025 transactions (forms issued early 2026): Robinhood has indicated it reported gross proceeds to the IRS, with cost basis shown to the customer where available. Transferred basis may be customer-provided. Robinhood has said it would not issue 2025 corrections solely for basis changes, because 2025 basis was informational and not reported to the IRS.

- 2026 transactions (forms generally issued 2027): Robinhood has said proceeds and cost basis will be reported to both the IRS and the customer, so covered-versus-noncovered status and accurate transferred basis become more important.

The IRS has emphasized that basis reporting is being phased in and that taxpayers remain responsible for correctly calculating basis and gain or loss regardless of what a form shows.

What Is Robinhood Crypto?

Robinhood Crypto is a custodial crypto account: Robinhood holds the assets and the keys, and it produces broker tax forms. That makes it very different from Robinhood’s other products and from a self-custody wallet.

Robinhood Crypto Versus the Rest of the Ecosystem

A Robinhood user might have stocks and securities through Robinhood Securities, futures and related products through Robinhood Derivatives, event contracts, cash features through Robinhood Money, and self-custody crypto through Robinhood Wallet. The forms and the substantive tax rules are not interchangeable across these. A single consolidated 1099 PDF can contain several different forms, which is exactly why people accidentally apply stock rules to crypto or vice versa.

Why the Product and Entity Matter

Because each product reports differently, the first step in any Robinhood crypto return is identifying which product an item came from. Crypto dispositions belong on Form 1099-DA. Securities belong on Form 1099-B. Reward income may appear on Form 1099-MISC. Self-custody Wallet activity generally is not on any of those and lives on-chain.

How Cryptocurrency Is Taxed

Almost everything about Robinhood crypto taxes flows from one classification.

Crypto Is Property

Under IRS Notice 2014-21, cryptocurrency is property for tax purposes, not currency. When you dispose of property you have a capital gain or loss; when you receive property as a reward you have ordinary income. Every Robinhood crypto scenario resolves to one of those two.

Capital Gains and Losses

Dispose of crypto for more than your basis and you have a capital gain; for less, a capital loss. Holding a year or less makes a gain short-term, taxed at ordinary rates of 10 to 37 percent. Holding more than a year makes it long-term, taxed at the preferential 0, 15, or 20 percent rates. The clock runs per lot, which is why holding periods and lot tracking matter so much.

Ordinary Income

Some Robinhood crypto activity is ordinary income at fair market value when received, including staking rewards and various promotional or referral rewards. That value becomes your basis for a later sale.

Proceeds Versus Taxable Gain

This is the distinction that trips up the most Robinhood users. Proceeds are the total dollar value of what you sold. Taxable gain is proceeds minus your adjusted cost basis minus applicable selling costs. A large proceeds number on a 1099-DA does not mean a large tax bill until basis is applied.

Does Robinhood Report Crypto to the IRS?

Yes, and understanding exactly what it reports, and does not, is the foundation of an accurate return.

What Robinhood Sends

Robinhood reports applicable custodial crypto dispositions on Form 1099-DA and may report reward income on Form 1099-MISC. Securities stay on Form 1099-B. For 2025 it has indicated proceeds went to the IRS with basis shown to customers where available; for 2026 it has said basis reporting to the IRS expands.

What Robinhood May Not Know

Robinhood does not necessarily know the acquisition history behind assets you did not buy on Robinhood. It may not know:

- Purchases you made on another exchange before transferring in.

- Historical wallet activity and DeFi transactions.

- Acquisition fees paid to another provider.

- Robinhood Wallet self-custody transactions.

- Transfers between external accounts.

Why No Form Does Not Mean No Tax

If an item does not appear on a 1099-DA, that does not make it tax free. Stablecoin aggregation, sub-threshold rewards, and self-custody Wallet activity can all be taxable while being absent from a form. The IRS expects you to report applicable income and dispositions whether or not you received an information return, and matching programs can flag mismatches between reported proceeds and your return.

Robinhood Form 1099-DA Explained

This is one of the most important sections, because the 1099-DA is the document most Robinhood crypto users actually hold in their hands.

What Form 1099-DA Is

Form 1099-DA is the dedicated broker information return for digital assets, replacing the old Form 1099-B treatment for crypto. It reports your dispositions and, increasingly, your basis.

The Key Fields

A Robinhood 1099-DA can include proceeds, cost basis where known, covered or noncovered status, customer-provided basis, transferred units and transfer dates, acquisition and disposal dates, the digital asset name and a DTIF code, and a gain or loss figure. There is also an additional-information section.

Why It Is Not a Finished Return

The form is a starting point, not a completed Form 8949. If basis is missing, customer-provided, or zero on transferred assets, the gain the form implies can be far off. You are responsible for reporting the correct gain or loss using your own records.

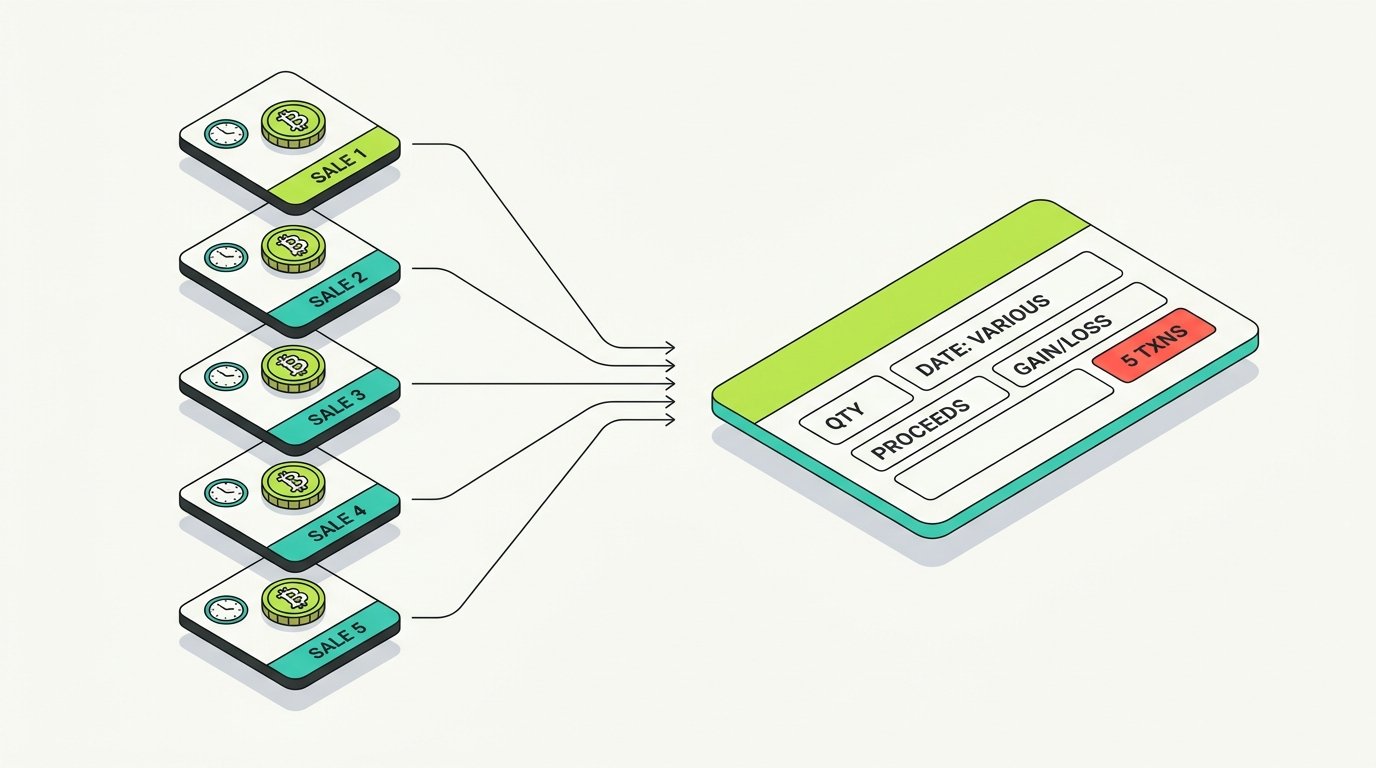

How Robinhood Aggregates Crypto Transactions

Robinhood may aggregate multiple sales of the same digital asset on the same day into one reported line. This is allowed, but it has real consequences for reconciliation.

What Aggregation Looks Like

An aggregated line can show a combined quantity, combined proceeds, an acquisition date that reads Various, short-term and long-term components, a count of included transactions, and transferred-unit information. One line can therefore represent many trades using different lots with different holding periods.

Why You Still Need Transaction-Level Records

Because a single aggregated line can mix lots and holding periods, you keep the detailed transaction records to reconcile it. The form summarizes; your records prove. This matters most when a Various line blends short-term and long-term pieces that must be split correctly on Form 8949.

Example: Five same-day BTC sales reported as one line

You sell Bitcoin five times in one day, drawing on several acquisition lots. Robinhood reports a single line: a combined quantity, combined proceeds, an acquisition date of Various, and a note that five transactions are included. To file correctly you break that line back into its underlying lots, assign the right basis and holding period to each, and report the pieces. The aggregated line is a summary, not the detail the IRS ultimately wants behind your gain.

Robinhood 1099-DA Proceeds Versus Actual Gain

A worked number makes the proceeds-versus-gain point concrete.

Example: A $95,000 proceeds line is not $95,000 of income

Your 1099-DA shows 95,000 dollars of BTC proceeds. You originally acquired that BTC for 30,000 dollars, and you paid 250 dollars in applicable selling costs. Your actual gain is 95,000 minus 30,000 minus 250, or 64,750 dollars, not 95,000. If the form showed basis as zero because the BTC was transferred in, the implied gain would look like the full 95,000. Supplying the real 30,000 basis is the difference between a fair result and a hugely overstated one.

Robinhood Stablecoin Tax Reporting

Stablecoins are a major source of confusion, because a reporting rule gets mistaken for a tax exemption.

The Aggregation Rule

Robinhood reports designated qualifying stablecoin sales on an aggregated basis once aggregate proceeds exceed 10,000 dollars, consistent with broker instructions that allow optional aggregation and de minimis reporting for qualifying stablecoins.

Why $10,000 Is Not an Exemption

This is a rule about when and how stablecoin activity appears on the form, not a rule that stablecoin sales below 10,000 dollars are tax free. Selling or converting a stablecoin is still a disposal of property and can create a small gain or loss. If your USDC sales do not appear line by line on your 1099-DA, that does not relieve you of reporting the underlying dispositions.

Robinhood Cost Basis Explained

Cost basis is where Robinhood crypto returns are won or lost. The arithmetic is simple; establishing accurate basis is the hard part.

When Robinhood Knows Your Basis

Robinhood generally knows basis for crypto you bought on Robinhood or received as a Robinhood reward. For those, the records are usually clean.

When Robinhood May Not

Robinhood may not know basis for crypto transferred in from another exchange or wallet. In that case basis can appear as zero or unknown, and you may need to supply it. Common complications include one transfer containing several acquisition lots, partial transfers, historical purchases, and gifts or inherited assets.

How to Reconstruct Missing Basis

Rebuild the original acquisition from the platform where you first bought the asset, your own purchase records, and on-chain history, then carry that basis to the disposal. Keep the evidence: trade confirmations, exchange statements, bank records, fee records, and blockchain transaction hashes.

How to Add Cost Basis to Robinhood

For transferred-in assets, Robinhood lets you supply basis, but it has to be done carefully.

What to Enter

Enter the acquisition date, quantity, and total acquisition cost including the fees you paid to acquire the asset. If a transfer contains several purchase lots, split it into those lots rather than entering one blended figure, so holding periods stay accurate.

Deadlines and Designation

Basis you supply is designated customer-provided, and there are annual deadlines after which adding basis in the app may no longer flow onto the form the same way. If you miss the in-app window, you can still report the correct basis directly on your Form 8949 using your records.

Records to Preserve

Keep original trade confirmations, exchange statements, wallet records, bank statements, fee records, and blockchain transaction hashes. Entering basis is only valid if you can support it under review.

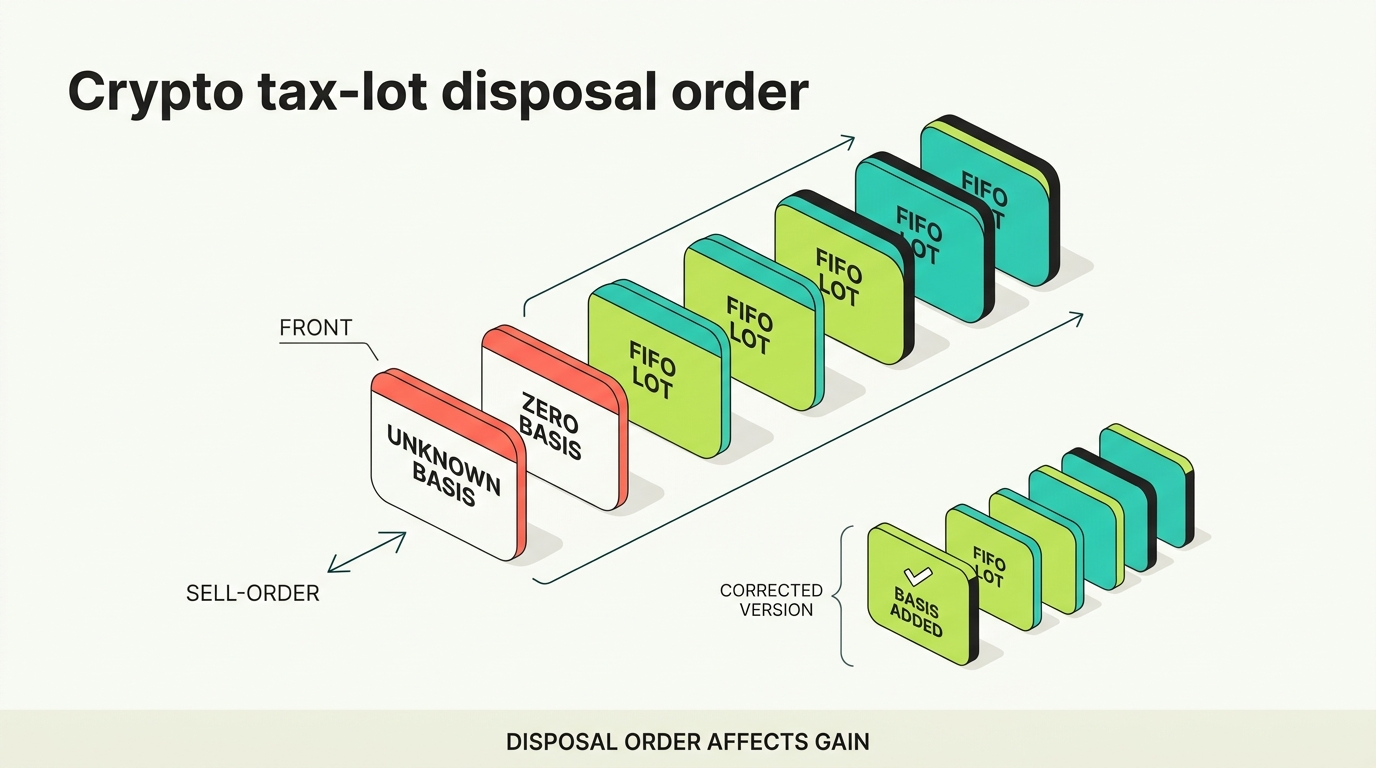

Robinhood’s Zero-Basis Priority Rule

This is one of the least-understood Robinhood mechanics, and it can dramatically distort an unprepared taxpayer’s gain.

What the Rule Does

Robinhood has said transferred lots with unknown or zero basis are closed before normal FIFO lots. So when you sell, unknown-basis units may be disposed of first, then ordinary FIFO ordering applies to the rest.

Why It Matters

A zero basis means the entire proceeds look like profit. If your earliest-disposed units are transferred-in lots with no basis attached, your estimated gain can be enormously overstated until you supply the real basis.

Example: A transferred lot closes before your Robinhood-purchased coins

You hold 0.50 BTC bought on Robinhood for 20,000 dollars and 0.25 BTC transferred in with no basis recorded. You sell 0.25 BTC. Under the zero-basis priority rule, the unknown-basis transferred lot may be closed first, so the sale appears to have zero basis and a fully taxable gain. Once you reconstruct that the transferred lot actually cost 12,000 dollars and report that basis, the real gain shrinks to what you actually earned.

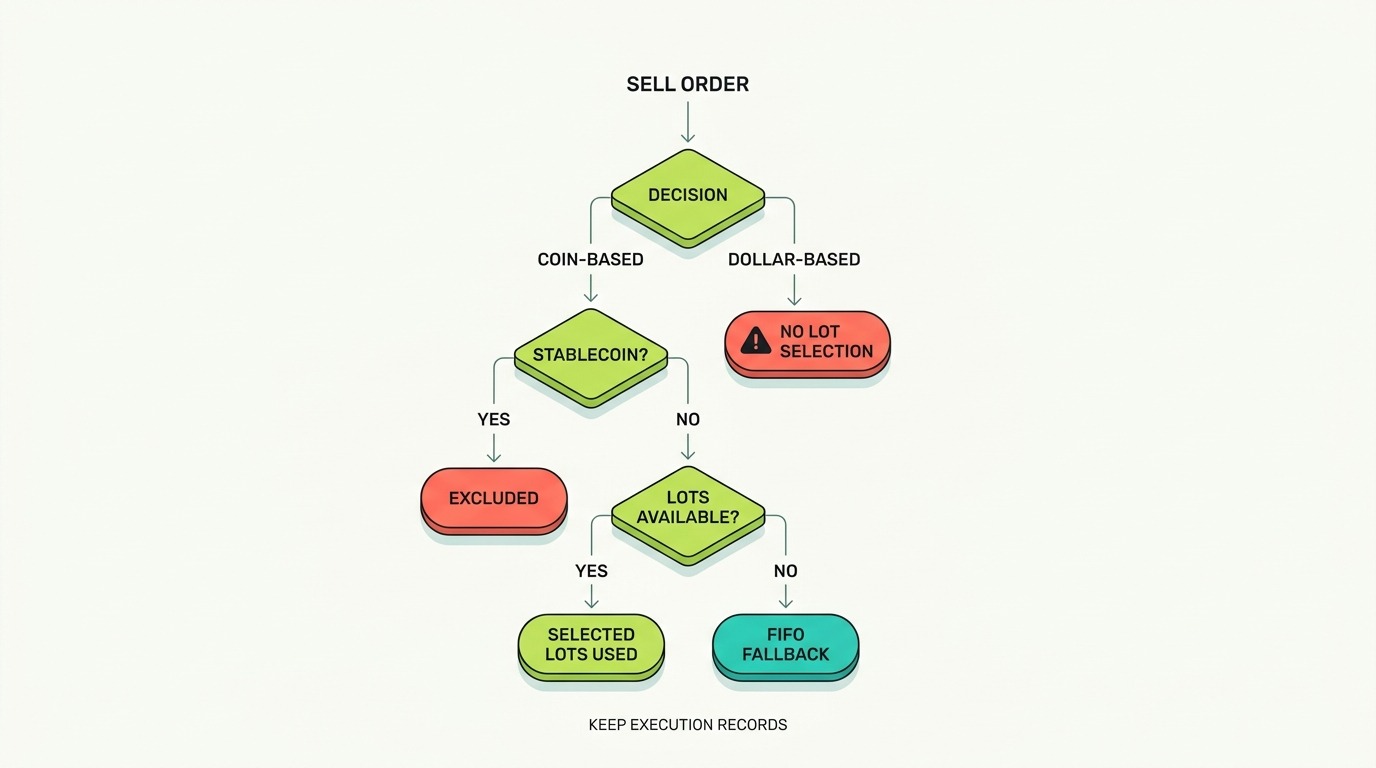

Robinhood Crypto Tax Lots

Robinhood now offers tax-lot selection, and it is one of the clearest places to publish fresher guidance than the rest of the SERP, which still often assumes pure FIFO.

What Tax-Lot Selection Allows

For eligible US users, Robinhood lets you select specific tax lots for certain coin-based sell orders, sorting lots by acquisition date or cost and choosing which to sell.

The Limits

The feature is not available for dollar-based orders, stablecoins, or withdrawals. If the selected lots cannot be filled, Robinhood may fall back to FIFO. Same-day rewards and unavailable lots add edge cases. Partial fills and multiple sell orders complicate matters further.

Why the In-App Estimate Is Not Your Final Record

The app’s gain estimate is a convenience, not a tax document. Keep the final execution records, because what actually filled, and in what order, is what you report.

Specific Identification Versus FIFO

The IRS places weight on adequate and timely identification of the units sold. If you identify lots at the time of sale and keep the order confirmations, you can support specific identification. If you do not, account-specific FIFO may apply. Hindsight selection after year end, choosing the best lots in retrospect, is risky and generally not respected without that timely identification.

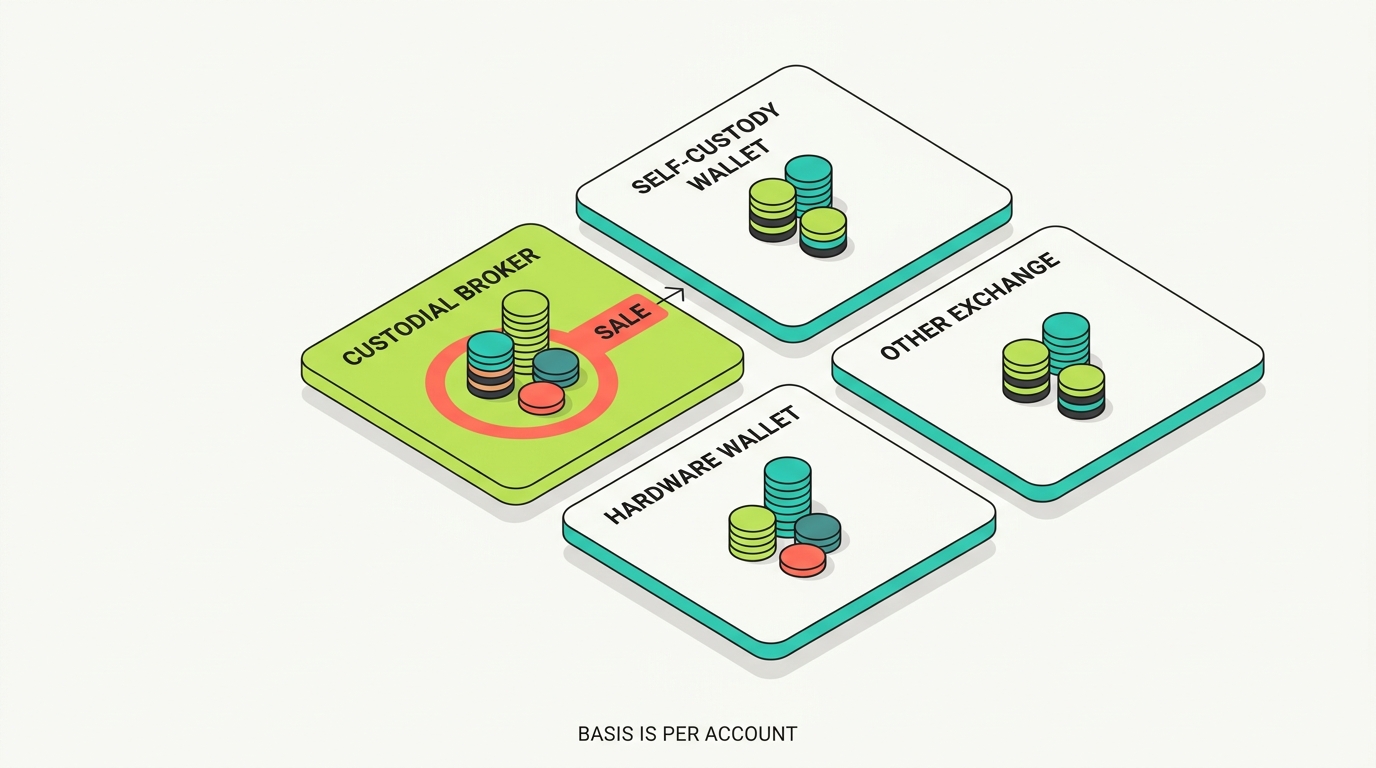

Wallet- and Account-Specific Cost Basis

Recent IRS guidance focuses on the units held in the particular wallet or account from which a disposition occurs, which matters for Robinhood users with crypto spread across platforms.

Why Account Location Matters

You generally cannot reach across every wallet and exchange after year end and cherry-pick the most favorable lot from your whole portfolio. Specific identification requires adequate and timely identification within the account; otherwise default ordering rules apply within that account.

Practical Implications

Treat Robinhood Crypto as one account, Robinhood Wallet as a separate wallet, and each outside exchange and hardware wallet as its own pool. Keep records that tie each disposal to the specific lot and account, and make sure basis travels with assets you move.

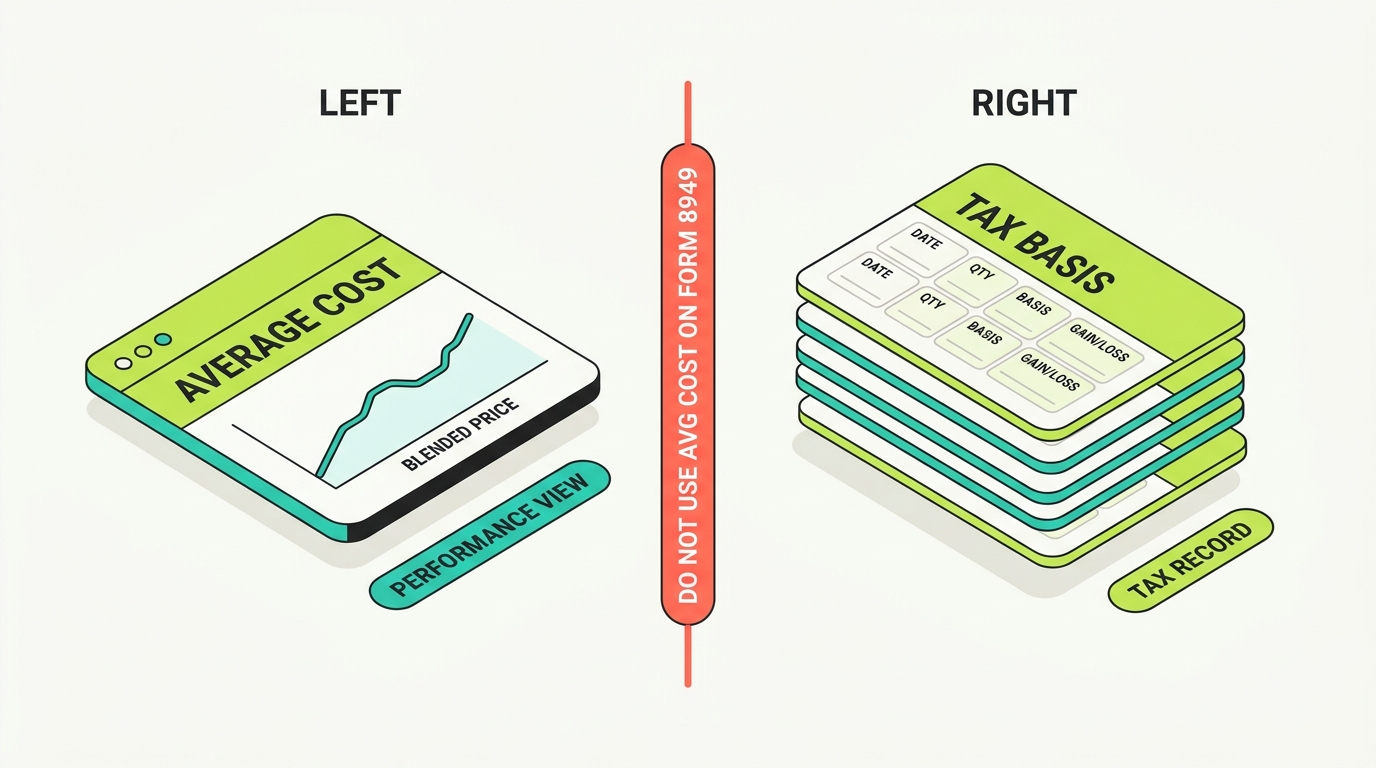

Robinhood Average Cost Versus Tax Cost Basis

This is a high-value distinction and a common, costly error.

Two Different Numbers

Robinhood has explicitly said its crypto average-cost figure should not be used to calculate realized gains or losses for tax reporting. Average cost is a portfolio-performance reference that changes as you buy and sell. Tax basis is assigned to specific acquired units and drives the gain or loss on each disposal.

Why You Cannot Copy Average Cost onto Form 8949

Using an average-cost number as your tax basis will generally produce the wrong gain or loss, sometimes by a lot. The official tax records, your tax-lot detail, are what belong on the return, not the average-cost display.

Robinhood Transactions That May Be Taxable

A fast-reference view of what triggers tax on Robinhood.

Potentially Taxable

- Selling crypto for US dollars.

- Exchanging one crypto for another.

- Spending crypto.

- Selling transferred-in crypto.

- Receiving staking rewards.

- Receiving promotional or referral rewards.

- Receiving a hard-fork asset.

- Disposing of stablecoins.

- Robinhood Wallet swaps and dapp transactions.

- NFT sales.

Usually Not Taxable by Themselves

- Buying crypto with US dollars.

- Holding crypto.

- Moving crypto between accounts you own.

- Depositing into Robinhood or withdrawing to your own wallet.

- Staking principal and token approvals.

- Canceled or failed orders.

Robinhood Spot Trading Taxes

The core of most Robinhood crypto returns is straightforward spot activity, with a few wrinkles.

Order Types and Fills

Market, limit, and stop orders, partial fills, and fractional crypto all create dispositions or acquisitions that need accurate dates and values. Canceled and unfilled orders are not taxable. Recurring purchases each create a new lot.

The Year-End Cutoff

Trades are generally recognized when they execute, and the tax year cutoff follows that timing. Be careful around year end, especially with the UTC versus local-time boundary, so a late-December trade lands in the correct year.

Example: Buying and selling ETH across several lots

You buy ETH in three separate purchases at different prices, then sell part of your position. Your gain depends on which lots are treated as sold and their holding periods. If you used tax-lot selection on a coin-based order, the lots you chose drive the result; if not, default ordering applies. Either way, you report the specific lots disposed, not an average.

Robinhood Crypto Fees and Order Routing

Older articles describe Robinhood crypto as simply commission-free. The current picture is more nuanced, and fees can affect basis and proceeds.

How Fees Arise

Robinhood distinguishes smart exchange routing, which can use percentage fee tiers based on eligible 30-day trading volume, from market-maker routing. Recurring investments can include the fee within the dollar amount entered. There is also the bid/ask spread and network fees.

How Fees Affect Tax

Acquisition fees can add to basis; disposal fees can reduce proceeds; fees paid in crypto can be a small disposition of the fee-paying asset; and transfer-only network costs are treated according to their purpose. Capturing fees correctly slightly changes many lines, which adds up over an active year.

Robinhood Crypto Transfer Taxes

Transfers are generally not taxable, but they are where basis goes missing and where a fee can hide a small disposal.

What Is and Is Not a Disposal

Depositing crypto into Robinhood, withdrawing it to your own wallet, and moving between accounts you own are generally not taxable. Sending crypto to another person can be a gift with its own rules. The network fee on a transfer, if paid in appreciated crypto, can be a small taxable disposition of that fee asset.

Why Withdrawing a Lot Is Different From Selling It

You cannot choose which tax lot is withdrawn, and a withdrawal is not a sale. So when you withdraw, track which units and basis left so the basis follows the asset to wherever it is eventually sold.

Example: Moving ETH from Robinhood to a hardware wallet

You withdraw 1 ETH from Robinhood to your hardware wallet. The withdrawal itself is not a taxable sale. But you record which lot and basis left, because when you eventually sell that ETH, from the wallet or after moving it again, the gain depends on that original Robinhood basis. The small network fee, if paid in crypto, is a separate tiny disposal to capture.

Coinbase, Kraken, and Other Exchanges to Robinhood

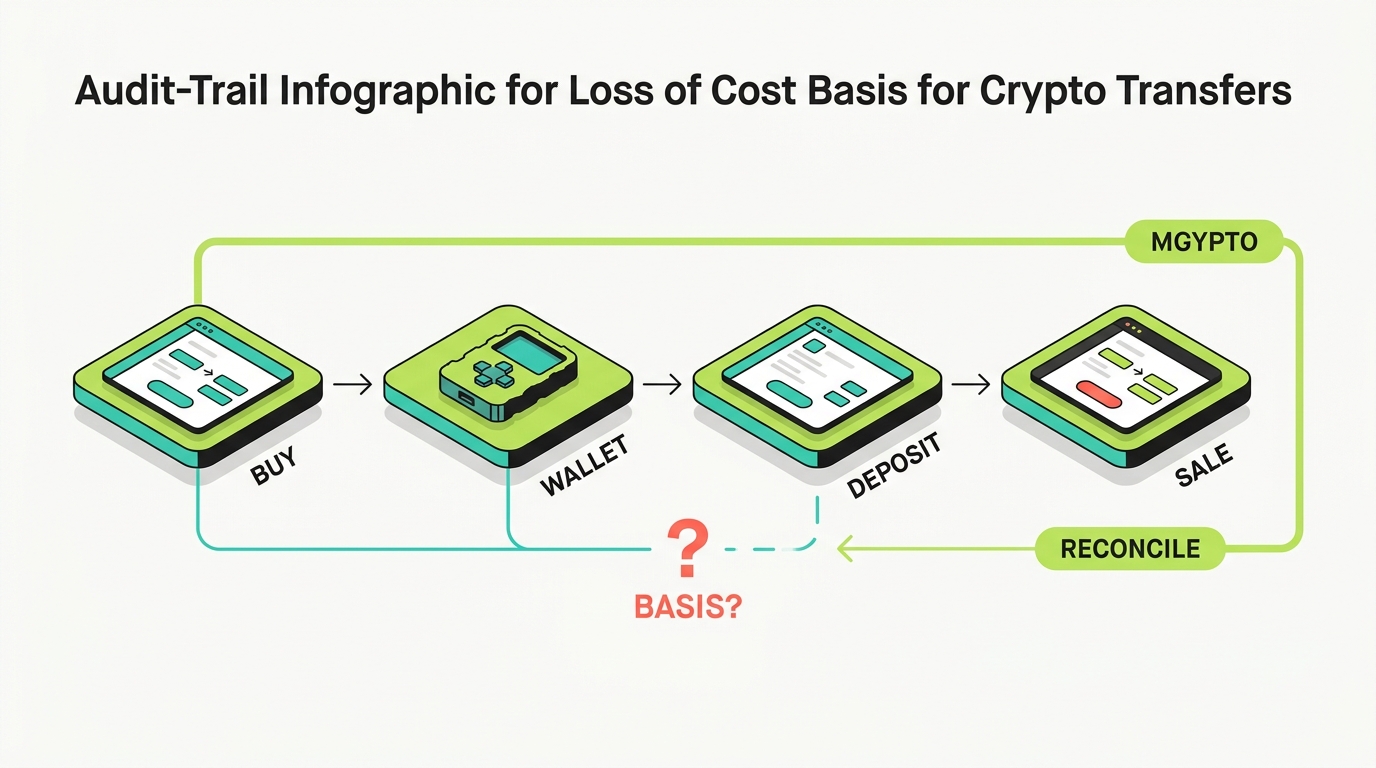

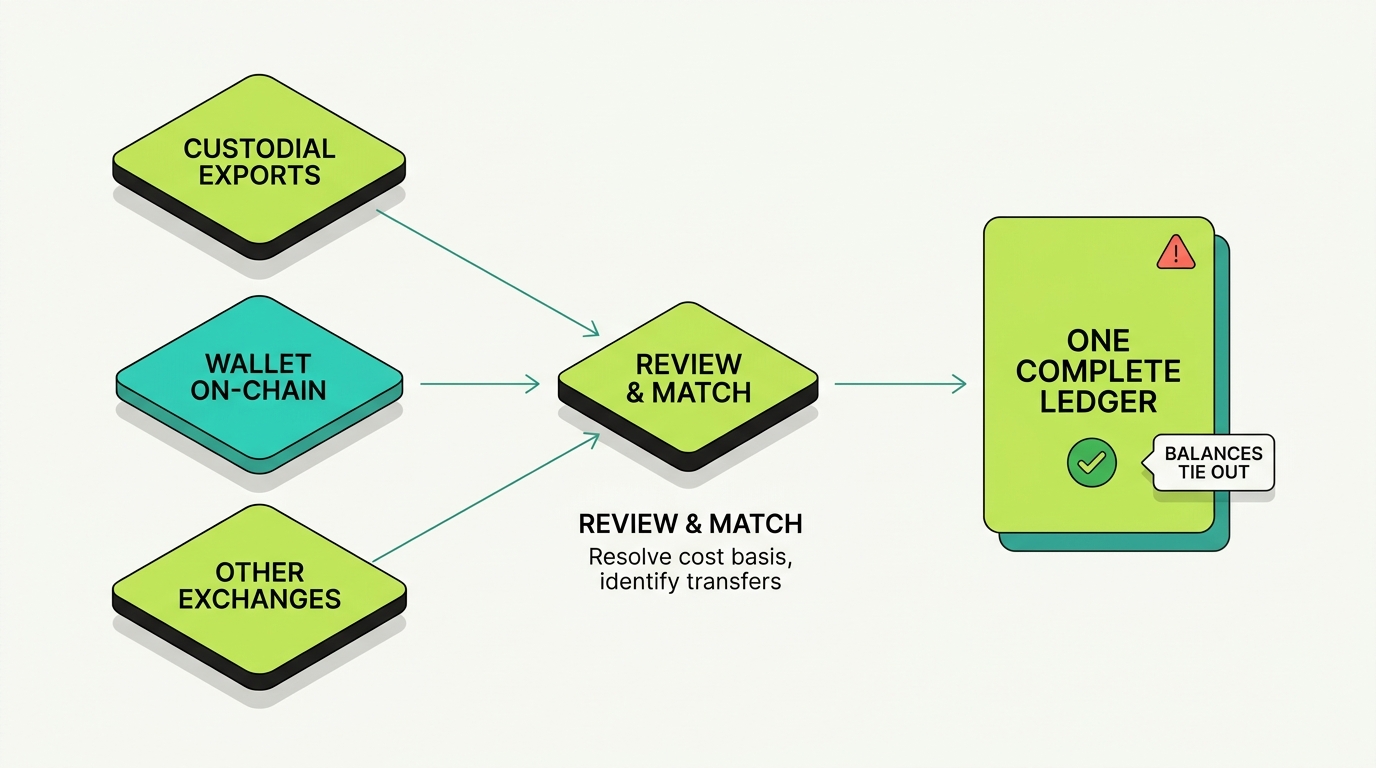

Cross-exchange transfers are the number-one source of missing basis, so they deserve their own attention.

Why Records Do Not Follow Automatically

When you move crypto from Coinbase, Kraken, Gemini, Crypto.com, or a hardware wallet into Robinhood, the acquisition records do not travel with the asset. Robinhood sees a deposit, not a purchase history.

How to Reconcile

Import both histories into one tax tool, match the withdrawal from the source to the deposit on Robinhood, carry the original basis through, watch for duplicate transactions, and reconstruct historical lots. If you later sell on Robinhood, the destination broker reports proceeds; you supply the basis.

Example: BTC bought on Coinbase, sold on Robinhood

You bought BTC on Coinbase, transferred it to Robinhood, and sold it there. Robinhood’s 1099-DA reports the proceeds but may show basis as zero or unknown, because it never saw your Coinbase purchase. You match the Coinbase withdrawal to the Robinhood deposit, supply the original basis, and report the real gain on Form 8949 rather than being taxed on the full proceeds.

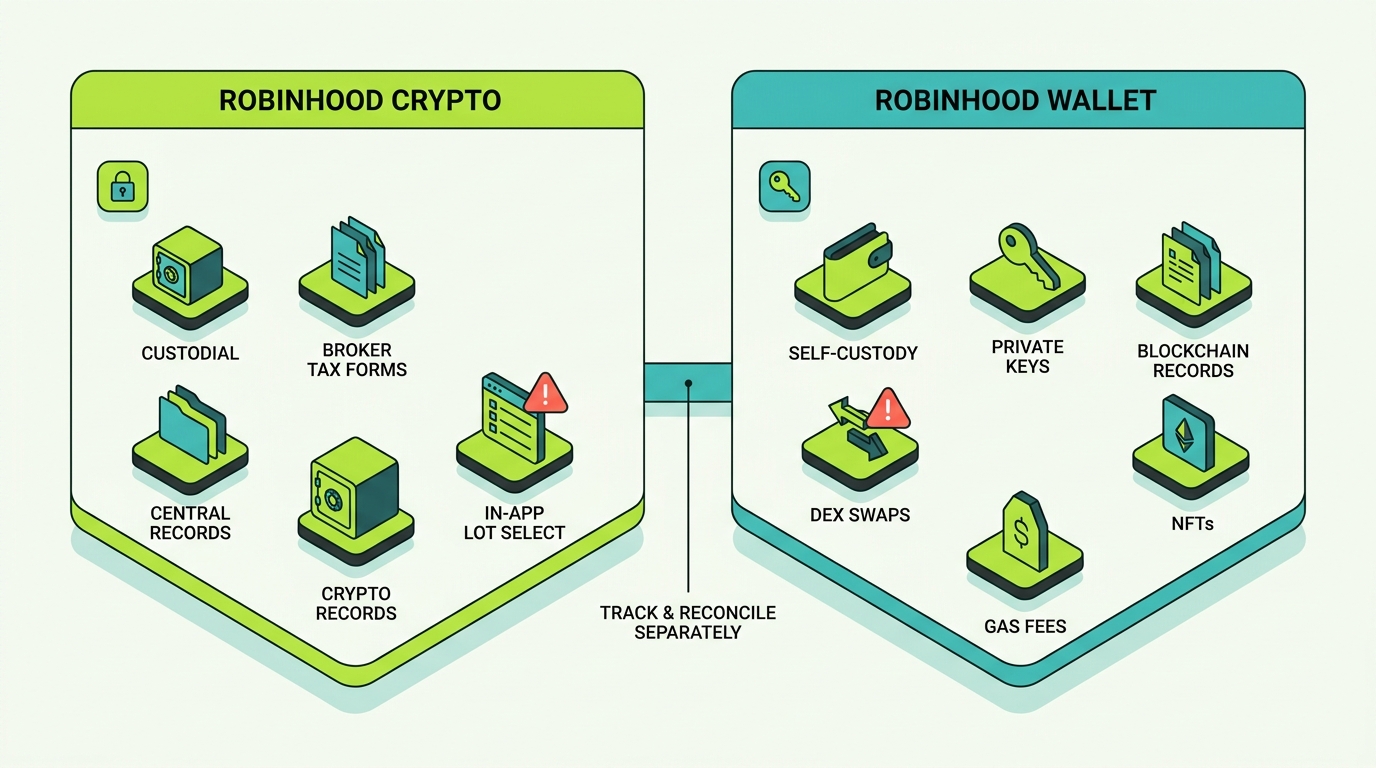

Robinhood Crypto Versus Robinhood Wallet

These two are constantly confused, and the confusion produces missed taxable events. They are different tax-data environments.

Robinhood Crypto

Custodial. Robinhood holds the keys, keeps centralized transaction records, issues broker tax forms, offers in-app tax-lot selection, and supports manual basis entry for transferred assets.

Robinhood Wallet

Self-custody. You hold the private keys and transact on public blockchains: DEX swaps, dapp interactions, token approvals, gas fees, wrapped assets, bridges, NFTs, on-chain staking, and airdrops. This activity generally is not on the custodial 1099-DA and must be reconciled from blockchain records.

Robinhood Wallet Taxes

Self-custody means the recordkeeping responsibility is entirely yours.

What Creates Tax in the Wallet

Sending and receiving, DEX swaps, dapp interactions, token approvals, gas fees, wrapped assets, bridges, NFTs, on-chain staking, and airdrops all have tax consequences. Swaps are crypto-to-crypto disposals; gas paid in crypto can be a small disposal; airdrops can be income.

Reconciling the Wallet

Import the wallet’s public addresses into tax software or pull history from a blockchain explorer, add missing prices, flag spam and scam tokens, and reconcile the Wallet against your Robinhood Crypto activity so transfers between them are not double-counted or treated as sales.

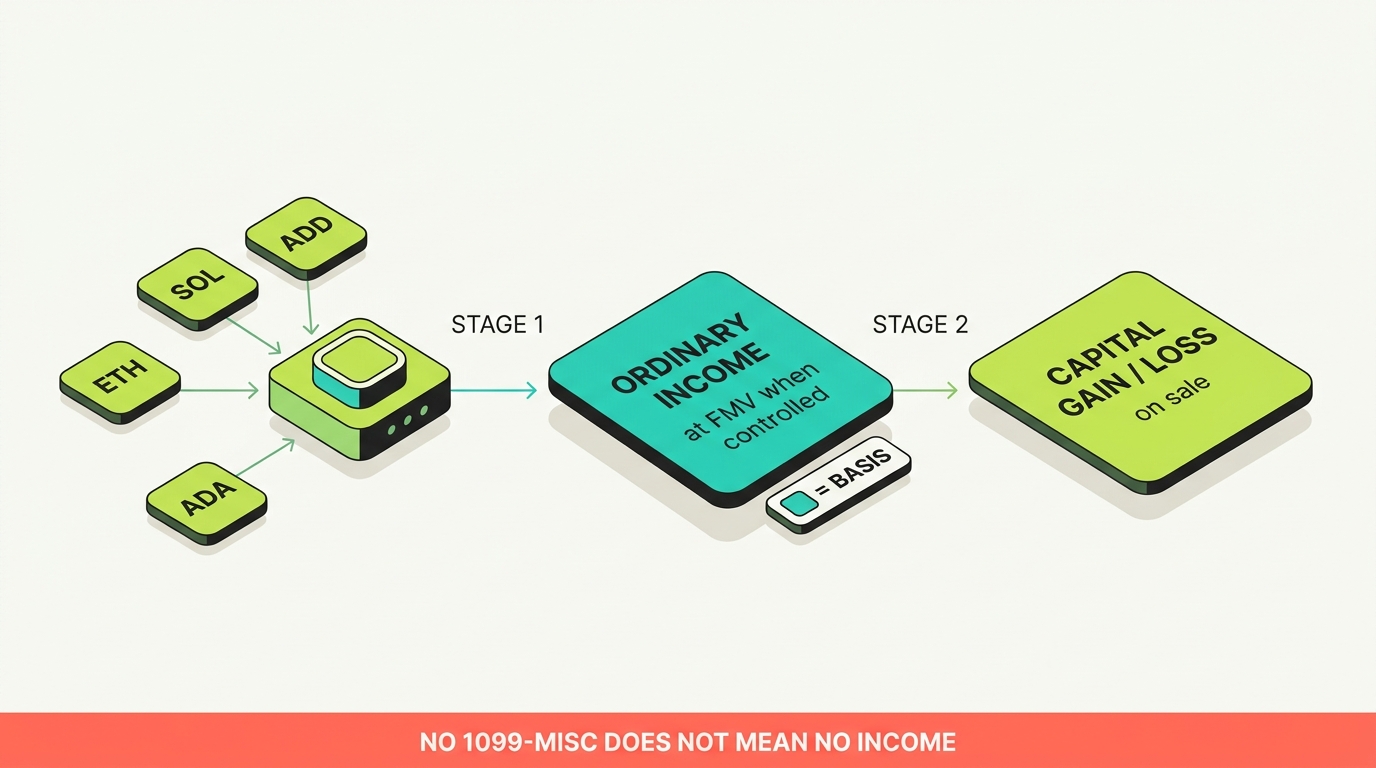

Robinhood Staking Taxes

Robinhood currently supports staking for assets such as SOL, ETH, and ADA in the US, subject to eligibility and location restrictions.

Income on Receipt, Capital Gain on Sale

Staking rewards are generally ordinary income at fair market value when you gain dominion and control over them. That value becomes your basis, so a later sale produces a separate capital gain or loss on the change in value since receipt. Bonding and unbonding periods affect when control is obtained.

The $600 Threshold Is Not a Tax Line

Robinhood may issue a Form 1099-MISC when reward income reaches the applicable threshold, often 600 dollars. The absence of that form does not make rewards nontaxable. You report applicable reward income whether or not a form is issued.

Example: Monthly SOL rewards followed by a sale

You receive small SOL staking rewards each month. Each reward is ordinary income at its value on the day you control it, and each sets the basis for that small lot. Months later you sell the accumulated SOL and report a separate capital gain or loss on the change in value since each reward was received. Even the months that fell under 600 dollars and generated no form are still reportable income.

Robinhood Rewards, Promotions, and Hard Forks

Beyond staking, Robinhood crypto can arrive through promotions, referrals, learn-and-earn, hard forks, and protocol merges.

How They Are Taxed

Promotional and referral rewards and newly received fork or merge assets are generally income at fair market value when received, establishing basis for a later disposal. Form 1099-MISC thresholds determine whether a form is issued, not whether the income is taxable.

Robinhood Recurring Crypto Purchases

Recurring buys are convenient and quietly create a lot-tracking burden.

Many Small Lots

Each recurring dollar-based purchase creates a new lot with its own date, price, and holding period, and the fee may be included in the recurring amount. A year of weekly buys is 52 lots. Because recurring buys are dollar-based, tax-lot selection generally is not available for the corresponding sells.

Example: Weekly BTC purchases over a year

You buy 50 dollars of BTC every week for a year. You now hold 52 separate lots, each with a distinct basis and holding period. When you sell, the gain depends on which lots are treated as sold, and dollar-based mechanics limit lot selection. Accurate per-lot records are what keep the eventual sale from being misreported.

Tax-Loss Harvesting and Wash-Sale Considerations

This area invites two opposite errors, and the truth is in between.

Avoid Both Extremes

It is not correct that the wash-sale rule never applies to crypto, nor that every loss followed by a repurchase is automatically a wash sale. The federal wash-sale provisions refer to stock or securities, and Form 1099-DA can include wash-sale reporting where a digital asset is also treated as stock or a security. Classification, related-party rules, economic substance, and possible future legislation all matter.

Practical Stance

Harvest losses deliberately, document them, watch the year-end UTC cutoff, and keep an eye on Robinhood stocks versus Robinhood crypto, where stock wash-sale rules clearly apply to the securities side. When classification is genuinely unclear, get professional input rather than relying on a slogan. For the mechanics of harvesting, see our crypto tax-loss harvesting guide.

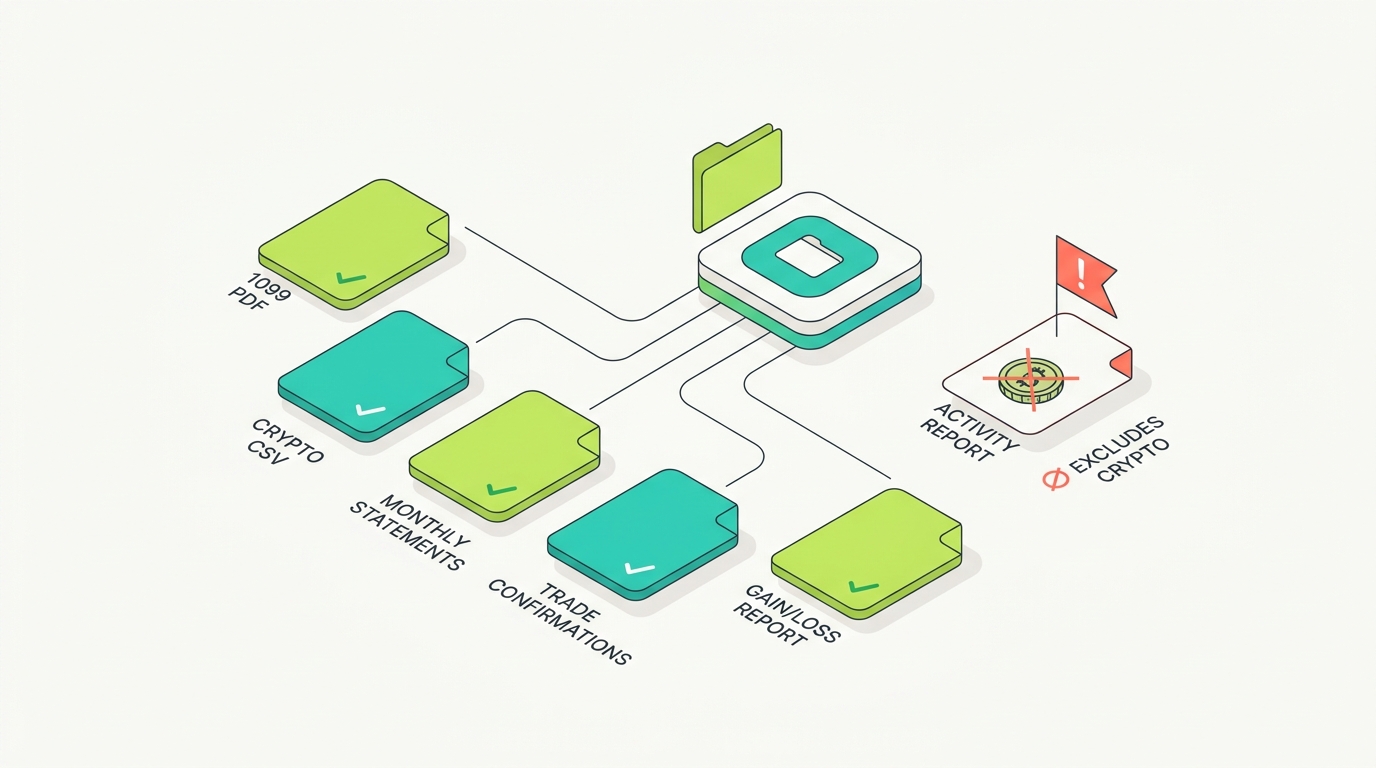

How to Download Robinhood Crypto Tax Records

Getting the right Robinhood tax documents is half the battle, because the obvious export is the wrong one for crypto.

What to Pull

From the Tax Center and your account: the consolidated 1099 PDF (containing Form 1099-DA and any 1099-MISC), the crypto transaction CSV, monthly statements, trade confirmations, and the realized gain/loss report, which for crypto can often be requested through chat support. Retrieve records before closing an account.

The Activity-Report Trap

Robinhood’s ordinary account activity report covers brokerage and retirement activity and explicitly excludes crypto, futures, and spending. If you download it expecting crypto, you will be missing your entire crypto history. Use the crypto-specific files instead.

The Trading API

Robinhood’s crypto Trading API exposes accounts, holdings, orders, products, and quotes. It is useful for active traders but is not proof that every tax-relevant transfer, reward, and Wallet transaction has been captured. Reconcile API output against statements and balances.

How to Reconcile Robinhood Crypto Activity

Reconciliation is the difference between a real return and a hopeful one. Work through this before you file.

Robinhood Form 8949 Reporting

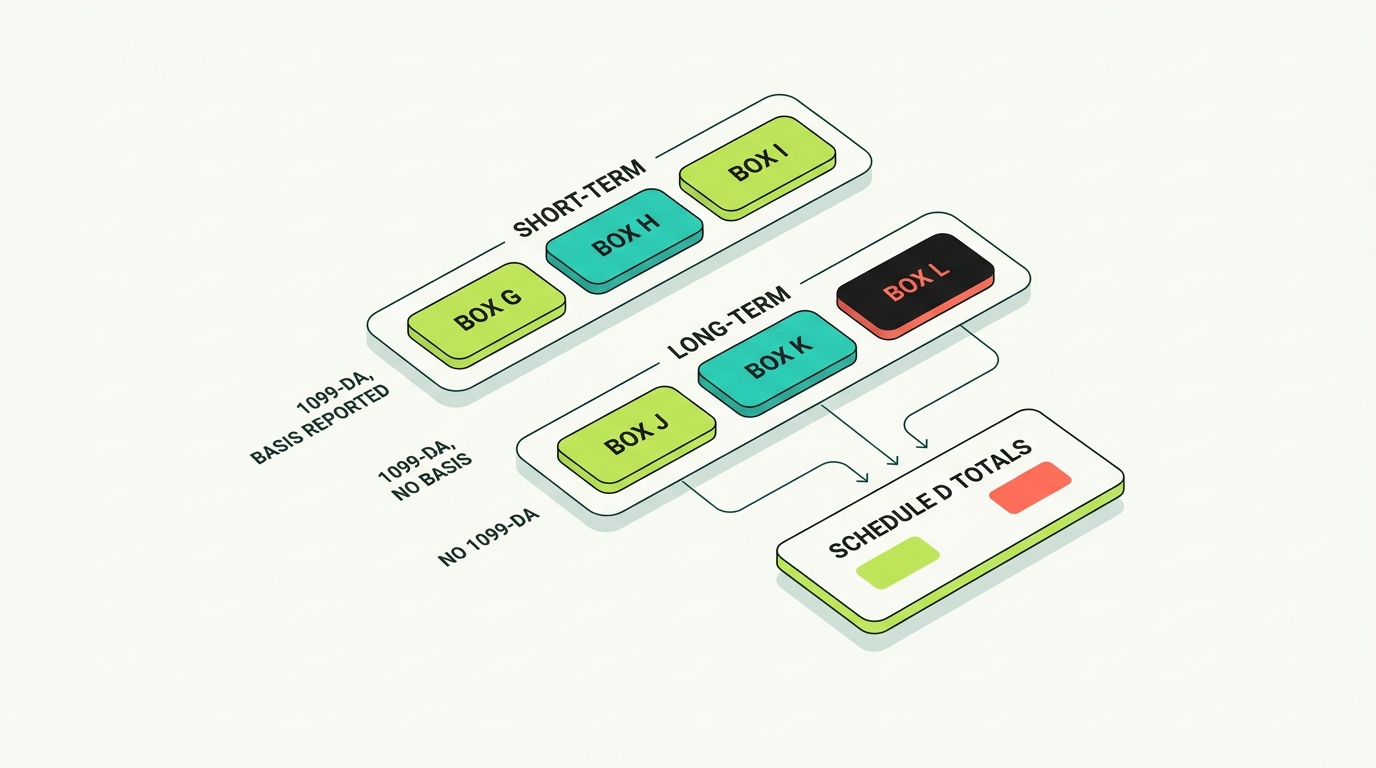

For 2025, Form 8949 added dedicated digital-asset categories, and using the right box matters.

The New Digital-Asset Boxes

Short-term: Box G when a 1099-DA was received and basis was reported to the IRS, Box H when a 1099-DA was received but basis was not reported, and Box I when no 1099-DA was received. Long-term: Boxes J, K, and L mirror those three. Which box you use depends on whether you received a 1099-DA and whether basis was reported.

Adjustments and Summary Reporting

When the form’s basis is wrong, you report the correct basis with an adjustment code rather than accepting the form. Daily-aggregated transactions and very high volumes can be reported in summary where permitted, with a supporting statement. Totals carry to Schedule D.

For the full mechanics of the form itself, see our Form 8949 guide and the Form 1099-DA explainer.

How to Report Robinhood Crypto on a Tax Return

Once your ledger is reconciled, reporting follows the standard framework.

The Forms

Capital dispositions go on Form 8949 and carry to Schedule D. Reward and staking income goes on Schedule 1 or the appropriate income form. Business-level activity may implicate Schedule C. Form 1099-MISC income is reported as income. The Form 1040 digital-asset question must be answered. Capital-loss limitations and carryforwards, the Net Investment Income Tax, state taxes, and estimated payments may all apply.

Filing Without a Form

If you had taxable activity that did not generate a form, such as sub-threshold rewards, stablecoin activity, or Wallet swaps, you still report it. The obligation does not depend on receiving an information return.

Importing Robinhood Into TurboTax or H&R Block

Imports help, but they have hard limits for active crypto traders.

The Volume Limits

Robinhood has indicated that users with more than 10,000 total transactions, or more than 4,000 uncovered transactions including crypto, may need help from their tax provider rather than a normal automatic import. In those cases, summary reporting with an attached, properly formatted statement is often cleaner than thousands of line entries.

When Software Is Not Enough

A failed or incomplete import, transferred-basis gaps, or Wallet activity that the import never saw are all signs you need manual reconciliation or a professional, not just a bigger software plan.

What to Do If Your Robinhood 1099-DA Is Wrong or Incomplete

Diagnose before you act.

Identify the Issue

Incorrect proceeds, missing basis, customer-provided basis, incorrect acquisition date, missing transfer information, stablecoin aggregation, or daily-aggregation confusion each have different fixes. Missing or incorrect basis, especially for 2025 where basis was informational, is frequently fixed by reporting the correct basis on your own Form 8949 with an adjustment rather than waiting for a corrected form.

When a Correction Versus an Adjustment Applies

A genuinely corrected information return suits some errors. A taxpayer adjustment on Form 8949 suits many basis situations. Robinhood has said it did not issue 2025 corrections solely for basis changes, so the adjustment path is often the realistic one. Preserve the records behind whatever you report.

Robinhood Crypto IRS Notices and CP2000 Responses

A mismatch notice is the predictable consequence of proceeds reported without basis.

Why They Happen and How to Respond

When proceeds are reported but basis is missing, the IRS may see a large apparent gain and send a CP2000 or similar matching notice. Compare the notice against your records, reconstruct the correct basis, prepare a transaction schedule, and respond with the corrected gain or loss and documentation. Depending on the situation you respond directly or amend. For larger or complex notices, professional representation is worth considering.

Correcting Prior-Year Robinhood Crypto Returns

Old returns built on outdated assumptions can be fixed.

Common Reasons and the Process

Old 1099-B assumptions, missing sales or rewards, incorrect zero basis, omitted Robinhood Wallet activity, duplicated trades, and mismatched transfers are all fixable. Build a corrected ledger first, then file an amended federal return, and remember a state amendment may follow. Keep both original and corrected workpapers, and mind statute-of-limitations timing.

Best Robinhood Crypto Tax Software

The right tool depends on your history, and no import should be trusted without review.

The Landscape

Koinly, CoinLedger, CoinTracker, Coinpanda, Awaken, TokenTax, and ZenLedger all handle Robinhood to varying degrees, differing in 1099-DA reconciliation, transferred-basis handling, Robinhood Wallet support, staking, multi-exchange transfers, high-volume capacity, Form 8949 output, and audit reports.

Why Software Alone Is Not Enough

An apparently successful import can still be incomplete, especially for transferred assets and self-custody Wallet activity. The real differentiator is whether your full history is reconciled across every source, not which logo is on the software.

Common Robinhood Crypto Tax Mistakes

The same mistakes recur, and most share one fix.

- Treating 1099-DA proceeds as taxable income.

- Assuming the 1099-DA is a finished return.

- Using average cost as tax basis.

- Ignoring transferred cost basis or accepting a zero basis.

- Missing the basis-entry deadline.

- Failing to split a transfer into multiple lots.

- Ignoring the zero-basis priority rule.

- Assuming Robinhood always uses plain FIFO.

- Not documenting selected tax lots.

- Treating the 10,000-dollar stablecoin threshold as a tax exemption.

- Ignoring rewards under 600 dollars.

- Treating Robinhood Wallet as part of the custodial 1099-DA.

- Using the standard activity report for crypto.

- Ignoring network fees.

- Mixing stocks, futures, event contracts, and crypto forms.

- Filing before reconciling aggregated sales and outside accounts.

Preparing for a Robinhood Crypto Tax Audit

Audit readiness is about evidence, organized before you need it.

What to Preserve

Keep your consolidated 1099, Form 1099-DA, any 1099-MISC, crypto transaction CSV, monthly statements, trade confirmations, realized gain/loss report, cost-basis entry records, selected tax-lot confirmations, wallet addresses, blockchain transaction hashes, staking reward history, bank records, other exchange exports, your transfer-matching schedule, the Form 8949 workpaper, the Schedule D reconciliation, and a written explanation of any manual adjustments.

What Is Digital Asset Reconciliation?

Importing data is not the same as reconciling it. Reconciliation means identifying every data source, connecting transfers, reconstructing basis, reviewing tax lots, reconciling the 1099-DA, reviewing staking and Wallet activity, tying opening to closing balances, and building an audit trail.

Signs You Need Professional Reconciliation

Transferred crypto with missing basis, Robinhood Wallet activity, several exchanges, more than 4,000 uncovered transactions, staking, prior-year errors, an IRS notice, high-value dispositions, or a trust, estate, or business account are all signals that software alone will not produce a clean, defensible return.

Not sure your crypto taxes are right?

Talk to a Count On Sheep specialist. We will spot the costly errors before you file. No obligation.

Book My Free Review- Reviewed by Former Big 4 Accountants

- Keep your CPA

- No pressure, no sales pitch

Worked Robinhood Crypto Tax Examples

A few combined scenarios show how the pieces fit together.

Example: Unknown-basis lot disposed before FIFO, then corrected

You sell BTC that includes a transferred-in lot with no recorded basis. The zero-basis priority rule closes that lot first, so your estimated gain spikes. You reconstruct the lot’s real 12,000-dollar basis from your old exchange statement, report it on Form 8949 with an adjustment, and your taxable gain drops to what you actually earned. The records behind the 12,000 are what make the adjustment defensible.

Example: Specific lot selection versus FIFO on a coin-based sale

You hold low-basis and high-basis ETH lots and place a coin-based sell. Using tax-lot selection, you choose the high-basis lot to reduce the gain, and you keep the execution confirmation. Had you placed a dollar-based order, lot selection would not have been available and default ordering would have applied. The saved confirmation is what supports your specific identification.

Example: Robinhood Wallet swap with gas fees

In Robinhood Wallet you swap one token for another and pay gas in crypto. The swap is a crypto-to-crypto disposal of the token you gave up, the new token takes a fresh basis, and the gas paid in crypto is a small separate disposal. None of this is on your custodial 1099-DA, so you reconstruct it from on-chain records and reconcile it with your Robinhood Crypto activity.

The Bottom Line on Robinhood Crypto Taxes

Form 1099-DA is one part of the process, not the finished return. Proceeds are not the same as taxable gain. Transferred basis must be substantiated, the zero-basis priority rule and tax-lot selection change which lots are sold, Robinhood Wallet must be tracked separately from Robinhood Crypto, and staking and stablecoin activity can be reportable even when no form is issued. Reconcile your complete picture before you file, use the correct Form 8949 boxes, and the rest follows.

If your Robinhood history involves transferred-in crypto, self-custody Wallet activity, several exchanges, staking, or a high transaction count, that is exactly the situation Digital Asset Reconciliation is built for. Count On Sheep imports and reconciles your Robinhood activity, reconstructs missing basis, connects every source, traces basis across transfers, and produces a defensible return that works alongside your tax preparer.

Frequently Asked Questions

Does Robinhood report crypto to the IRS?

Yes. Robinhood reports applicable custodial crypto dispositions to the IRS on Form 1099-DA, and reward income may appear on Form 1099-MISC. For 2025 transactions, Robinhood has indicated it reported gross proceeds to the IRS with cost basis shown to the customer where available, and it has said cost basis reporting to the IRS expands for 2026 transactions. Reporting to the IRS does not mean the form is a finished return: it often reports proceeds without complete acquisition history, so you still have to compute and report the correct gain or loss yourself.

Does Robinhood issue Form 1099-DA?

Yes. Robinhood Crypto dispositions are now reported on Form 1099-DA, the dedicated broker form for digital assets, rather than the old Form 1099-B used for securities. Robinhood combines applicable forms from its crypto, securities, derivatives, and money products into one consolidated PDF, so it is easy to confuse one product's tax treatment with another's. The 1099-DA reports proceeds and, increasingly, basis, but you still need supporting records behind every line.

Does Robinhood still issue Form 1099-B for crypto?

No. Crypto dispositions moved to Form 1099-DA. Form 1099-B generally still applies to stocks and other securities in your Robinhood Securities account. Any older article that tells you Robinhood crypto is reported on Form 1099-B is out of date. Because both forms can appear in the same consolidated 1099 package, check which form a given line actually came from before you report it.

Why is my Robinhood 1099-DA so high?

Usually because the form reports gross proceeds, which is the total dollar value of your sales, not your taxable gain. If you sold the same coins many times, the proceeds add up fast even when your actual profit is small. Daily aggregation can also combine several same-day sales into one large line. Your taxable gain is proceeds minus cost basis minus applicable selling costs, so a large proceeds figure does not mean a large tax bill once basis is applied.

Does Form 1099-DA show my taxable gain?

Not by itself. Form 1099-DA shows proceeds and may show cost basis, but the gain or loss it implies is only as good as the basis behind it. If basis is missing, customer-provided, or shown as zero on transferred assets, the gain on the form can be badly overstated. You are responsible for reporting the correct gain or loss on Form 8949, using supporting records, even when that differs from what the form implies.

Why is my Robinhood cost basis zero?

A zero or unknown basis almost always means the asset was transferred into Robinhood from another exchange or wallet and its purchase history did not follow it. Robinhood knows the basis of crypto you bought on Robinhood or received as a Robinhood reward, but it may not know the basis of assets you moved in. Do not accept a zero basis, because it overstates your gain. Reconstruct the original purchase and enter or report the correct basis.

What does customer-provided basis mean on Robinhood?

It means the cost basis came from you, not from Robinhood's own records. When you transfer crypto in, Robinhood may not know what you paid, so it lets you supply the acquisition date, quantity, and total cost. That figure is labeled customer-provided because you are responsible for its accuracy and for keeping the evidence behind it. Customer-provided basis is legitimate, but it must be supportable if your return is ever questioned.

What does Various mean on a Robinhood 1099-DA?

Various appears in the acquisition-date field when a single reported line covers units acquired on more than one date, which happens when Robinhood aggregates multiple sales or lots. It is not an error. It signals that you need transaction-level records behind that line to determine holding periods and basis for each underlying lot, because a single Various line can mix short-term and long-term pieces.

Why are several Robinhood trades shown on one line?

Robinhood may aggregate multiple sales of the same digital asset that occur on the same day into one reported line, with a combined quantity, combined proceeds, an acquisition date that may read Various, and a count of included transactions. Aggregation is allowed, but it means one line can represent many trades with different lots and holding periods, so you keep the detailed records to reconcile that line on Form 8949.

What is the DTIF code on my Robinhood 1099-DA?

DTIF refers to a Digital Token Identifier, a standardized code that identifies the specific digital asset on the form. It is a way to name the token precisely rather than relying only on a ticker. For your purposes it confirms which asset a line refers to. The important work is still attaching accurate proceeds, basis, and holding-period detail to that asset, not the identifier itself.

Does Robinhood report cost basis to the IRS?

It is being phased in. For 2025 transactions, Robinhood has indicated it reported gross proceeds to the IRS while showing basis to the customer where available, and it has said that for 2026 transactions both proceeds and cost basis will be reported to the IRS and the customer. The IRS has emphasized that basis reporting is phasing in and that taxpayers remain responsible for correctly calculating basis and gain or loss regardless of what the form shows.

How will 2026 Robinhood reporting differ from 2025?

The phrase 2026 Robinhood taxes is ambiguous, so separate the two meanings. 2025 transactions are reported on forms issued in early 2026, with proceeds reported to the IRS and basis shown to the customer where available. 2026 transactions are reported on returns generally filed in 2027, with basis reporting to the IRS expanding. The key practical change is that covered-versus-noncovered status and accurate transferred basis matter more as IRS basis reporting grows.

Why did Robinhood not correct my 2025 cost basis?

Robinhood has said it would not issue a corrected 2025 Form 1099-DA solely because cost basis changed, since 2025 basis was informational and was not reported to the IRS. That does not leave you stuck. You report the correct basis directly on your own Form 8949 using your records, with an adjustment if needed. A corrected information return is only one way to fix basis; a taxpayer adjustment on your return is the more common path here.

How do I add cost basis to Robinhood crypto?

For transferred-in assets with missing basis, Robinhood lets you enter the acquisition date, quantity, and total acquisition cost, including the fees you paid to acquire the asset. If one transfer contains several purchase lots, split it into those lots rather than entering one blended figure. Then preserve the underlying evidence: original trade confirmations, exchange statements, and blockchain records. Entering basis in the app is only valid if you can support it.

Can I add several purchase lots to one Robinhood transfer?

Yes, and you generally should. A single transfer into Robinhood can contain crypto you bought on different dates at different prices. Entering one blended cost hides the separate holding periods and can distort short-term versus long-term treatment. Splitting the transfer into its real acquisition lots, each with its own date, quantity, and cost, produces accurate basis and correct holding periods when you later sell.

Does Robinhood use FIFO for crypto?

FIFO is the default ordering, but it is not the whole story. Robinhood now lets eligible US users select specific tax lots for certain coin-based sell orders, and it has said unknown- or zero-basis transferred lots are closed before ordinary FIFO lots. So the actual disposal order can be: unknown-basis lots first, then your selected lots if you used the feature, then FIFO. Do not assume plain FIFO without checking how your order was actually filled.

Can I select crypto tax lots on Robinhood?

Yes, within limits. Robinhood offers tax-lot selection for certain coin-based sell orders for eligible US users, letting you sort lots by acquisition date or cost and choose which to sell. It is not available for dollar-based orders, stablecoins, or withdrawals, and if the selected lots cannot be filled, Robinhood may fall back to FIFO. Keep the final execution records, because the in-app estimate is not your final tax record.

Can I select tax lots for a dollar-based Robinhood order?

No. Robinhood's tax-lot selection is described as available for certain coin-based sell orders, not dollar-based orders. If you place a dollar-based sell, you generally cannot choose specific lots, and default ordering applies. If lot selection matters for your tax outcome, that limitation is worth knowing before you place the order, because you cannot retroactively choose lots after the fact in a way the IRS will respect without adequate, timely identification.

Can I select tax lots for Robinhood stablecoin sales?

No. Stablecoins are excluded from Robinhood's tax-lot selection feature. That does not make stablecoin sales tax free; it just means you cannot pick specific lots for them in the app. Stablecoin dispositions still need to be tracked and, where applicable, reported, even though they often sit very close to one dollar and produce small gains or losses.

Can I choose which Robinhood crypto lot is withdrawn?

No. Robinhood does not offer custom tax-lot selection for withdrawals. A withdrawal moves crypto to another wallet or account; it is generally not a sale, so it is not a disposal you report as a gain. But because you cannot choose which lot leaves, you must track which units and basis moved so that the basis follows the asset to wherever it is eventually sold.

Why does Robinhood sell zero-basis lots first?

Robinhood has said transferred lots with unknown or zero basis are closed before normal FIFO lots. The logic is that those unknown lots get resolved first, but the effect on an unprepared taxpayer can be a dramatically overstated gain, because a zero basis means the entire proceeds look like profit. The fix is to enter or report the correct basis for those transferred lots before you file, so the disposal reflects real gain.

Is Robinhood average cost the same as tax cost basis?

No. Robinhood has explicitly said its crypto average-cost figure should not be used to calculate realized gains or losses for tax reporting. Average cost is a portfolio-performance reference; tax basis is assigned to specific acquired units and drives the gain or loss on each disposal. Copying an average-cost number onto Form 8949 will generally produce the wrong result. Use your tax-lot records, not the average-cost display.

Are Robinhood stablecoin transactions taxable?

Selling or converting a stablecoin is still a disposal of property, so it can create a gain or loss, usually small because stablecoins track close to one dollar. The catch is reporting: Robinhood may report qualifying stablecoin sales on an aggregated basis only once aggregate proceeds exceed a threshold, so some stablecoin activity may not appear line by line on your form. That reporting rule is not a tax exemption, and you remain responsible for any gain or loss.

What is the Robinhood $10,000 stablecoin rule?

Robinhood reports designated qualifying stablecoin sales on an aggregated basis once aggregate proceeds exceed 10,000 dollars, consistent with broker instructions that permit optional aggregation and de minimis reporting for qualifying stablecoins. This is a broker-reporting rule about when and how the activity appears on the form. It is not a rule that stablecoin sales under 10,000 dollars are tax free or can be ignored. You still account for the underlying dispositions.

Why are my USDC sales missing from my Robinhood 1099-DA?

Because of the stablecoin aggregation rule. Robinhood may only report qualifying stablecoin sales in aggregate once proceeds pass the threshold, so individual USDC sales may not show up line by line. Missing from the form does not mean exempt. If you had stablecoin dispositions with gains or losses, you are still responsible for reporting them, which is one more reason to reconcile your full transaction history rather than relying solely on the form.

Are Robinhood crypto transfers taxable?

Moving crypto between accounts and wallets you own is generally not a taxable event. Depositing crypto into Robinhood or withdrawing it to your own wallet is a transfer, not a sale. Two things still matter: your cost basis must travel with the asset so a later sale is accurate, and a network fee paid in crypto during the transfer can itself be a small disposal of the fee-paying asset that you should capture.

Are Robinhood crypto network fees deductible?

It depends on the fee's purpose. The IRS distinguishes costs incurred to acquire or dispose of an asset, which can adjust basis or proceeds, from costs incurred solely to transfer an asset between your own accounts. A fee paid using appreciated crypto can also trigger a separate small disposition of the fee-paying asset. So rather than a blanket deduction, network fees are handled according to what they were for. Track them and apply the right treatment.

Are Robinhood staking rewards taxable?

Yes. Staking rewards are generally ordinary income at fair market value when you gain dominion and control over them, meaning you can sell or dispose of them. That value becomes your cost basis, so when you later sell the rewarded crypto you also have a separate capital gain or loss on the change in value since receipt. Robinhood currently supports staking for assets such as SOL, ETH, and ADA in the US, subject to eligibility and location rules.

Does Robinhood issue a 1099-MISC for staking?

It may, typically when reward income reaches the applicable reporting threshold, often 600 dollars. But the absence of a Form 1099-MISC does not make otherwise taxable income nontaxable. The IRS requires you to report applicable digital-asset income whether or not you receive an information return. So even small staking rewards that fall below the threshold and generate no form are still reportable income at their value when received.

Do I report Robinhood rewards below $600?

Yes. The 600-dollar figure is a reporting threshold for whether a payer issues a Form 1099-MISC, not a threshold for whether income is taxable. Reward and staking income is generally taxable when you gain control of it, regardless of amount. If your rewards came in under 600 dollars and you received no form, you still report that income, and you still establish basis in those reward units for a later sale.

Is Robinhood Wallet included on Form 1099-DA?

Generally no. Robinhood Wallet is self-custody, meaning you control the private keys and transact on public blockchains, so its activity lives on-chain rather than in Robinhood's custodial broker records. The Robinhood Crypto 1099-DA covers your custodial account, not your self-custody Wallet swaps, dapp interactions, and on-chain transfers. Wallet activity usually needs to be tracked and reconciled separately using blockchain records.

Are Robinhood Wallet swaps taxable?

Yes. A token swap in a self-custody wallet is a crypto-to-crypto trade, which is a disposal of the token you gave up and an acquisition of the token you received, each at fair market value. Gas fees, wrapped assets, and bridges add detail. Because these happen on-chain and outside the custodial 1099-DA, you generally reconstruct them from blockchain records rather than expecting them on a Robinhood tax form.

How do I export Robinhood Wallet transactions?

Robinhood Wallet activity is on-chain, so you export or reconstruct it from blockchain records using the wallet's public addresses, often by importing those addresses into crypto tax software or pulling history from a blockchain explorer. This is separate from your Robinhood Crypto custodial exports. Treat the custodial account and the self-custody Wallet as two distinct data sources that both need to be captured.

How do I download my Robinhood crypto transaction history?

Robinhood provides tax documents, monthly statements, trade confirmations, a crypto transaction CSV, and a realized gain/loss CSV that can be requested through chat support. The key trap is that Robinhood's ordinary account activity report excludes crypto, futures, and spending activity, so you need the crypto-specific files, not the standard brokerage activity report. Pull the crypto transaction CSV and the realized gain/loss report specifically.

Why is crypto missing from my Robinhood activity report?

Because Robinhood's custom account activity report covers brokerage and retirement activity and explicitly excludes crypto, futures, and spending. It is the wrong file for crypto reconciliation. Use the crypto-specific transaction CSV, the realized gain/loss report, monthly statements, and your tax documents instead. Many people miss crypto entirely because they downloaded the standard activity report and assumed it was complete.

How do I get a Robinhood crypto gain/loss CSV?

Robinhood provides a realized gain/loss CSV, which for crypto can often be requested through chat support in addition to the downloadable crypto transaction CSV and tax documents in the Tax Center. Use it alongside, not instead of, the raw transaction history, because a gain/loss summary still depends on the basis Robinhood had, which may be incomplete for transferred-in assets.

Can I access Robinhood tax records after closing my account?

You should retrieve and save everything before or as soon as you close an account, because access to documents and exports can become harder afterward. Download your consolidated 1099, crypto transaction CSV, realized gain/loss report, statements, and trade confirmations while you have full access. If you have already closed an account and are missing records, you can often still reconstruct activity from destination platforms and blockchain history.

How do I import Robinhood crypto into TurboTax?

Robinhood supports importing tax forms using a document ID and account number, but crypto imports have limits. Robinhood has indicated that users with very high transaction counts, such as more than 10,000 total transactions or more than 4,000 uncovered transactions including crypto, may need help from their tax provider rather than a normal automatic import. In those cases summary reporting with an attached statement, or specialist software, is often the cleaner path.

What if I have more than 4,000 uncovered Robinhood crypto transactions?

Robinhood has said that more than 4,000 uncovered transactions, or more than 10,000 total transactions, may exceed what a normal automatic import can handle, so you may need to summarize. The usual approach is to report totals on Form 8949 with a properly formatted supporting statement that lists the detail, rather than entering thousands of individual lines. This is a common situation for active traders and is exactly where reconciliation matters.

Which Form 8949 box applies to Robinhood crypto?

For 2025, Form 8949 added dedicated digital-asset categories. Short-term: Box G when a 1099-DA was received and basis was reported to the IRS, Box H when a 1099-DA was received but basis was not reported, and Box I when no 1099-DA was received. Long-term: Boxes J, K, and L mirror those three situations. Which box you use depends on whether you got a 1099-DA and whether basis was reported, so check the form before classifying.

Does the wash-sale rule apply to Robinhood crypto?

It is nuanced, so avoid both extremes. The federal wash-sale provisions refer to stock or securities, and Form 1099-DA can include wash-sale reporting where a digital asset is also treated as stock or a security for tax purposes. Whether the rule applies to a given crypto position depends on its classification, related-party rules, economic substance, and possible future legislation. Do not assume crypto is automatically exempt, and do not assume every loss-and-rebuy is automatically a wash sale.

What if my Robinhood 1099-DA is wrong or incomplete?

First identify the issue: incorrect proceeds, missing basis, customer-provided basis, or aggregation confusion. Missing or incorrect basis is frequently fixed by reporting the correct basis on your own Form 8949 with an adjustment, rather than waiting for a corrected form, especially for 2025 where basis was informational. A genuinely corrected information return is appropriate for some errors. Keep the records that support whatever figures you report.

How do I respond to a Robinhood crypto IRS notice?

A matching notice such as a CP2000 often arises when proceeds were reported without basis, so the IRS sees a large apparent gain. Compare the notice against your records, reconstruct the correct basis, prepare a transaction schedule, and respond with the corrected gain or loss and supporting documentation. Depending on the situation you may respond directly or amend a return. For larger or complex notices, professional representation is worth considering.

How do I correct a prior-year Robinhood crypto return?

Build a corrected transaction ledger first, then file an amended return for the affected year. Common reasons include older returns that used 1099-B assumptions, missing sales or rewards, incorrect zero basis, omitted Robinhood Wallet activity, duplicated trades, or mismatched transfers. Keep both the original and corrected workpapers, and remember an amended federal return may also require an amended state return.

What is the best tax software for Robinhood crypto?

The best tool depends on your history. Koinly, CoinLedger, CoinTracker, Coinpanda, Awaken, TokenTax, and ZenLedger all handle Robinhood to varying degrees, differing in 1099-DA reconciliation, transferred-basis handling, Robinhood Wallet support, staking, and high-volume capacity. Whichever you pick, an apparently successful import can still be incomplete, particularly for transferred assets and self-custody Wallet activity, so the real differentiator is whether your full history is reconciled.

When should I hire a crypto tax professional for Robinhood?

Consider help when you have transferred-in crypto with missing basis, Robinhood Wallet or other on-chain activity, several exchanges to reconcile, more than 4,000 uncovered transactions, staking income, prior-year errors, an IRS notice, high-value dispositions, or a trust, estate, or business account. At that point software alone often cannot produce a clean, defensible return, and a reconciliation specialist who traces basis across every transfer becomes worth far more than the fee.

Can Count On Sheep help with Robinhood crypto taxes?

Yes. Count On Sheep provides CPA-ready Digital Asset Reconciliation for Robinhood users: importing and reconciling your Robinhood Crypto activity, reconstructing missing or transferred cost basis, connecting Robinhood to your other exchanges and self-custody wallets including Robinhood Wallet, reconciling daily-aggregated 1099-DA lines, handling staking and stablecoin activity, classifying transactions into the correct Form 8949 boxes, and producing a defensible return that works alongside your tax preparer.